|

市場調査レポート

商品コード

1687715

フィリピンの飼料添加物:市場シェア分析、産業動向、成長予測(2025年~2030年)Philippines Feed Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| フィリピンの飼料添加物:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 415 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

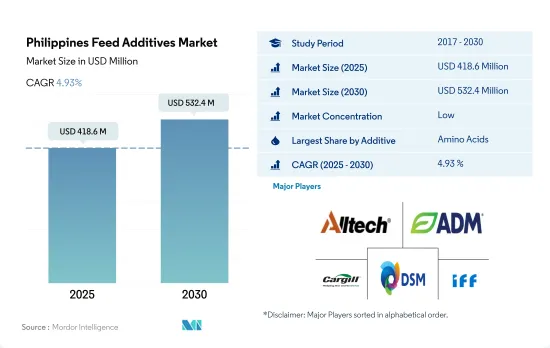

フィリピンの飼料添加物市場規模は2025年に4億1,860万米ドルと推定され、2030年には5億3,240万米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは4.93%で成長すると予測されます。

- 2022年には、アミノ酸、結合剤、ミネラル、プロバイオティクスが、国内の動物飼料産業で使用される主な飼料添加物の種類でした。これらの添加物の種類を合計すると、金額ベースで同国の飼料添加物市場全体の55.1%を占める。これらの種類の飼料添加物の中では、メチオニンとリジンが最も重要な飼料用アミノ酸であり、それぞれ市場シェアの34.1%と30.2%を占めました。これらのアミノ酸の人気は、腸内環境を改善し、消化を助け、家畜の肉生産を高める能力があるためです。

- 2022年の国内飼料用粘結剤市場全体では、合成粘結剤が66.7%を占め、最大のシェアを占めました。合成結合剤はペレット飼料の役割を果たすだけでなく、動物の消化と栄養摂取を改善することで病気の予防にも役立つため、好まれました。2022年の飼料添加物市場では豚が主要な動物種であり、市場シェア値の52%を占めました。この高いシェアは、飼料摂取量と飼料生産量が多いためで、2022年には780万トンを超えていました。

- 同国の飼料添加物市場では、顔料とアミノ酸が最も急成長する分野と予想され、予測期間中のCAGRはそれぞれ5.5%と5.4%を記録します。色素は動物飼料の外観と栄養価を高めるために使用され、動物はカロテノイドを合成できないため、飼料中に供給する必要がありました。

- 動物栄養における飼料添加物の重要性に基づき、国内では飼料添加物の需要が予測期間中にCAGR 4.9%を記録すると予想されます。この成長は、動物の腸内環境の改善と消化の容易さ、および高品質の動物性タンパク質に対する需要の高まりによってもたらされると予想されます。

フィリピンの飼料添加物市場動向

同国では、鶏肉消費の増加と鶏卵需要の増加により、鶏肉生産が増加しています。

- 鶏肉産業は近年著しい成長を遂げており、2017年から2019年にかけて生産量は6.3%増加しています。この成長は、鶏肉消費の増加と、パンデミック時の手頃なタンパク質源としての鶏卵需要の増加に起因します。卵製品の調理のしやすさも鶏卵の需要拡大に寄与しています。

- さらに、商業養豚場が鶏卵生産にシフトしており、これが今後数年間のレイヤー部門の成長を促進すると予想されます。しかし、2020年の鶏卵生産量は2019年比で4.2%減少したが、これは主にCOVID-19の蔓延対策としてホテルやレストランが閉鎖されたためです。投入資材の供給不足も生産量の減少につながりました。

- 2020年に直面した課題にもかかわらず、家禽部門は2021年以降、動物性タンパク質に対する需要の高まりと、制限緩和後の2022年の経済再開による恩恵により、生産量が増加しています。例えば、2022年の鶏肉生産量は前年から130万頭増加しました。家禽の農家出荷価格の上昇も市場成長の原動力となっており、商業農場におけるブロイラー用鶏肉の年間平均農家出荷価格は、2021年には前年比10.7%増の1kg当たり1.82米ドルとなります。

- アフリカ豚熱の蔓延により、消費者が動物性タンパク源として豚肉から鶏肉にシフトしているため、同国では鶏肉の需要が増加しています。このシフトは生産者に増産圧力をもたらしており、2021年の鶏肉生産量は134万トンを占め、2020年より3%増加します。

養殖動物の生産性とパフォーマンスを向上させ、水産物の消費量が増加することで、養殖用飼料の需要が増加すると予想されます。

- フィリピンにおける養殖用配合飼料生産は、養殖動物の生産性とパフォーマンスを向上させるための栄養バランスの取れた飼料の重要性に対する意識の高まりと、水産物の消費量の増加を背景に、近年急速に拡大しています。2022年、養殖用配合飼料の生産量は同国の配合飼料生産量全体の28.5%を占め、2017年から62万1,300トン増加しました。

- 魚はフィリピンの消費者にとって最も有望な蛋白源です。所得水準の上昇と消費パターンの変化による動物性タンパク質への需要の高まりが、魚食への需要を押し上げています。その結果、生産者が動物の成績を向上させ、タンパク質が豊富な食品を生産しようとするため、配合魚用飼料の生産量は2023年の145万5,800トンから2029年には177万7,200トンに増加すると予想されます。

- 同様に、フィリピンにおけるエビ飼料の生産量も、養殖場数の増加、エビ生産による利益率の上昇、収量と生産性を高めるための健康・栄養管理への関心の高まりにより、急速に増加しています。エビ飼料の生産量は2017年から100.7%増加し、2022年には3万1,800トンに達します。しかし、乱獲や、マングローブや内陸部での養殖場の過剰な拡大に対する政府の規制により、フィリピンの魚の価格は他の食肉商品と比べて大幅に上昇しています。このため、飼料を使用して収量を増やすことへの関心が広まっています。

フィリピンの飼料添加物産業の概要

フィリピンの飼料添加物市場は断片化されており、上位5社で27.02%を占めています。この市場の主要企業は以下の通り。 Alltech, Inc., Archer Daniel Midland Co., Cargill Inc., DSM Nutritional Products AG and IFF(Danisco Animal Nutrition)(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 動物頭数

- 家禽

- 反芻動物

- 豚

- 飼料生産

- 水産養殖

- 家禽

- 反芻動物

- 養豚

- 規制の枠組み

- フィリピン

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 添加物

- 酸味料

- サブ添加物別

- フマル酸

- 乳酸

- プロピオン酸

- その他の酸味料

- アミノ酸

- 添加物別

- リジン

- メチオニン

- スレオニン

- トリプトファン

- その他のアミノ酸

- 抗生物質

- 添加物別

- バシトラシン

- ペニシリン

- テトラサイクリン

- タイロシン

- その他の抗生物質

- 酸化防止剤

- 添加物別

- ブチルヒドロキシアニソール(BHA)

- ブチル化ヒドロキシトルエン(BHT)

- クエン酸

- エトキシキン

- 没食子酸プロピル

- トコフェロール

- その他の酸化防止剤

- 結合剤

- サブ添加物別

- 天然結合剤

- 合成バインダー

- 酵素

- 副添加物別

- 炭水化物分解酵素

- フィターゼ

- その他の酵素

- 香料・甘味料

- サブ添加物別

- 香料

- 甘味料

- ミネラル

- サブ添加物別

- マクロミネラル

- 微量ミネラル

- マイコトキシン解毒剤

- 副添加物別

- 結合剤

- バイオトランスフォーマー

- その他のマイコトキシン解毒剤

- フィトジェニック

- 副添加物別

- エッセンシャルオイル

- ハーブ&スパイス

- その他の植物性食品

- 色素

- 副添加物別

- カロテノイド

- クルクミン&スピルリナ

- プレバイオティクス

- 副添加物別

- フラクトオリゴ糖

- ガラクトオリゴ糖

- イヌリン

- ラクチュロース

- マンナンオリゴ糖

- キシロオリゴ糖

- その他のプレバイオティクス

- プロバイオティクス

- 添加物別

- ビフィズス菌

- 腸球菌

- 乳酸菌

- ペディオコッカス

- レンサ球菌

- その他のプロバイオティクス

- ビタミン

- 添加物別

- ビタミンA

- ビタミンB

- ビタミンC

- ビタミンE

- その他のビタミン

- 酵母

- 添加物別

- 生きた酵母

- セレン酵母

- 使用済み酵母

- トルラ乾燥酵母

- ホエイ酵母

- 酵母誘導体

- 酸味料

- 動物

- 水産養殖

- サブアニマル別

- 魚類

- エビ

- その他の養殖種

- 家禽類

- 小動物別

- ブロイラー

- レイヤー

- その他の鳥類

- 反芻動物

- 小動物別

- 肉牛

- 乳牛

- その他の反芻動物

- 豚

- その他の動物

- 水産養殖

第6章 競争情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Adisseo

- Alltech, Inc.

- Archer Daniel Midland Co.

- BASF SE

- Cargill Inc.

- DSM Nutritional Products AG

- IFF(Danisco Animal Nutrition)

- Lallemand Inc.

- Novozymes AS

- SHV(Nutreco NV)

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

The Philippines Feed Additives Market size is estimated at 418.6 million USD in 2025, and is expected to reach 532.4 million USD by 2030, growing at a CAGR of 4.93% during the forecast period (2025-2030).

- In 2022, amino acids, binders, minerals, and probiotics were the main types of feed additives used in the animal feed industry in the country. These types of additives together represented 55.1% of the country's total feed additives market in terms of value. Among these types of feed additives, methionine and lysine were the most significant feed amino acids, accounting for 34.1% and 30.2% of the market share, respectively. The popularity of these amino acids was due to their ability to improve gut health, aid in easy digestion, and enhance meat production in animals.

- Synthetic binders held the largest share of the total feed binders market in the country in 2022, accounting for 66.7%. Synthetic binders were preferred because they not only served in pellet feed but also aided in preventing diseases by improving digestion and nutrition intake in animals. Swine was the major animal type in the feed additives market in 2022, accounting for 52% of the market share value. This high share was due to the high feed intake and feed production, which was more than 7.8 million metric tons in 2022.

- Pigments and amino acids are expected to be the fastest-growing segments in the feed additives market in the country, registering CAGRs of 5.5% and 5.4%, respectively, during the forecast period. Pigments were used to enhance the appearance and nutritional value of animal feed, and as animals were unable to synthesize carotenoids, they needed to be supplied in the diet.

- Based on the importance of feed additives in animal nutrition, the demand for feed additives is anticipated to register a CAGR of 4.9% during the forecast period in the country. This growth is expected to be driven by improved gut health and easy digestion in animals, as well as the growing demand for high-quality animal protein.

Philippines Feed Additives Market Trends

The poultry production is increasing in the country because of the rise in consumption of poultry meat and an increase in demand for poultry eggs

- The poultry industry has experienced significant growth in recent years, with production increasing by 6.3% from 2017 to 2019. This growth can be attributed to the rise in consumption of poultry meat and an increase in demand for poultry eggs as an affordable protein source during the pandemic. The ease of cooking egg products has also contributed to the growth in demand for poultry eggs.

- In addition, commercial pig farms are shifting to egg production, which is expected to drive the growth of the layers segment in the coming years. However, the production of poultry decreased by 4.2% in 2020 compared to 2019, primarily due to the closure of hotels and restaurants to combat the spread of COVID-19. The shortage of input supply also led to a decline in production.

- Despite the challenges faced in 2020, the poultry sector has experienced an increase in production since 2021 due to the rising demand for animal protein and the benefit from the reopening of the economy in 2022 after the ease of restriction. For instance, poultry production increased by 1.3 million heads in 2022 from the previous year. The rising farmgate prices of poultry are also driving the growth of the market, with the annual average farmgate price of broiler chicken in commercial farms increasing by 10.7% from the previous year to USD 1.82 per kg in 2021.

- The demand for chicken is increasing in the country as consumers shift from pork to chicken as a source of animal protein due to the spread of African swine fever. This shift is creating pressure on producers to increase production, with chicken meat production accounting for 1.34 million metric tons in 2021, an increase of 3% over 2020.

To improve the productivity and performance of aquaculture animals and rising consumption of seafood is expected to increase the aquaculture feed demand

- The aquaculture compound feed production in the Philippines has been rapidly expanding in recent years, driven by increasing awareness about the importance of nutritionally balanced feed for improving the productivity and performance of aquaculture animals and the rising consumption of seafood. In 2022, the production of aquaculture compound feed accounted for 28.5% of total compound feed production in the country, and it increased by 621.3 thousand metric tons from 2017.

- Fish is the most promising source of protein for the Philippines' consumers. The rising demand for animal protein due to increasing income levels and changing consumption patterns are boosting the demand for fish food. As a result, the production of compound fish feed is expected to increase from 1,455.8 thousand metric tons in 2023 to 1,777.2 thousand metric tons in 2029 as producers seek to improve the performance of the animals and produce protein-rich food.

- Similarly, shrimp feed production in the Philippines has also been increasing rapidly due to an increase in the number of farms, rising profit margins from shrimp production, and a growing focus on health and nutrition management to increase yields and productivity. The production of shrimp feed increased by 100.7% from 2017, reaching 31.8 thousand tons in 2022. However, overfishing and government regulations against the overexpansion of fish farms in mangrove and inland areas have caused fish prices in the Philippines to increase considerably compared to those of other meat commodities. This has led to a widespread interest in increasing yields with the use of feeds.

Philippines Feed Additives Industry Overview

The Philippines Feed Additives Market is fragmented, with the top five companies occupying 27.02%. The major players in this market are Alltech, Inc., Archer Daniel Midland Co., Cargill Inc., DSM Nutritional Products AG and IFF(Danisco Animal Nutrition) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 Philippines

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Additive

- 5.1.1 Acidifiers

- 5.1.1.1 By Sub Additive

- 5.1.1.1.1 Fumaric Acid

- 5.1.1.1.2 Lactic Acid

- 5.1.1.1.3 Propionic Acid

- 5.1.1.1.4 Other Acidifiers

- 5.1.2 Amino Acids

- 5.1.2.1 By Sub Additive

- 5.1.2.1.1 Lysine

- 5.1.2.1.2 Methionine

- 5.1.2.1.3 Threonine

- 5.1.2.1.4 Tryptophan

- 5.1.2.1.5 Other Amino Acids

- 5.1.3 Antibiotics

- 5.1.3.1 By Sub Additive

- 5.1.3.1.1 Bacitracin

- 5.1.3.1.2 Penicillins

- 5.1.3.1.3 Tetracyclines

- 5.1.3.1.4 Tylosin

- 5.1.3.1.5 Other Antibiotics

- 5.1.4 Antioxidants

- 5.1.4.1 By Sub Additive

- 5.1.4.1.1 Butylated Hydroxyanisole (BHA)

- 5.1.4.1.2 Butylated Hydroxytoluene (BHT)

- 5.1.4.1.3 Citric Acid

- 5.1.4.1.4 Ethoxyquin

- 5.1.4.1.5 Propyl Gallate

- 5.1.4.1.6 Tocopherols

- 5.1.4.1.7 Other Antioxidants

- 5.1.5 Binders

- 5.1.5.1 By Sub Additive

- 5.1.5.1.1 Natural Binders

- 5.1.5.1.2 Synthetic Binders

- 5.1.6 Enzymes

- 5.1.6.1 By Sub Additive

- 5.1.6.1.1 Carbohydrases

- 5.1.6.1.2 Phytases

- 5.1.6.1.3 Other Enzymes

- 5.1.7 Flavors & Sweeteners

- 5.1.7.1 By Sub Additive

- 5.1.7.1.1 Flavors

- 5.1.7.1.2 Sweeteners

- 5.1.8 Minerals

- 5.1.8.1 By Sub Additive

- 5.1.8.1.1 Macrominerals

- 5.1.8.1.2 Microminerals

- 5.1.9 Mycotoxin Detoxifiers

- 5.1.9.1 By Sub Additive

- 5.1.9.1.1 Binders

- 5.1.9.1.2 Biotransformers

- 5.1.9.1.3 Other Mycotoxin Detoxifiers

- 5.1.10 Phytogenics

- 5.1.10.1 By Sub Additive

- 5.1.10.1.1 Essential Oil

- 5.1.10.1.2 Herbs & Spices

- 5.1.10.1.3 Other Phytogenics

- 5.1.11 Pigments

- 5.1.11.1 By Sub Additive

- 5.1.11.1.1 Carotenoids

- 5.1.11.1.2 Curcumin & Spirulina

- 5.1.12 Prebiotics

- 5.1.12.1 By Sub Additive

- 5.1.12.1.1 Fructo Oligosaccharides

- 5.1.12.1.2 Galacto Oligosaccharides

- 5.1.12.1.3 Inulin

- 5.1.12.1.4 Lactulose

- 5.1.12.1.5 Mannan Oligosaccharides

- 5.1.12.1.6 Xylo Oligosaccharides

- 5.1.12.1.7 Other Prebiotics

- 5.1.13 Probiotics

- 5.1.13.1 By Sub Additive

- 5.1.13.1.1 Bifidobacteria

- 5.1.13.1.2 Enterococcus

- 5.1.13.1.3 Lactobacilli

- 5.1.13.1.4 Pediococcus

- 5.1.13.1.5 Streptococcus

- 5.1.13.1.6 Other Probiotics

- 5.1.14 Vitamins

- 5.1.14.1 By Sub Additive

- 5.1.14.1.1 Vitamin A

- 5.1.14.1.2 Vitamin B

- 5.1.14.1.3 Vitamin C

- 5.1.14.1.4 Vitamin E

- 5.1.14.1.5 Other Vitamins

- 5.1.15 Yeast

- 5.1.15.1 By Sub Additive

- 5.1.15.1.1 Live Yeast

- 5.1.15.1.2 Selenium Yeast

- 5.1.15.1.3 Spent Yeast

- 5.1.15.1.4 Torula Dried Yeast

- 5.1.15.1.5 Whey Yeast

- 5.1.15.1.6 Yeast Derivatives

- 5.1.1 Acidifiers

- 5.2 Animal

- 5.2.1 Aquaculture

- 5.2.1.1 By Sub Animal

- 5.2.1.1.1 Fish

- 5.2.1.1.2 Shrimp

- 5.2.1.1.3 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 By Sub Animal

- 5.2.2.1.1 Broiler

- 5.2.2.1.2 Layer

- 5.2.2.1.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.3.1.1 Beef Cattle

- 5.2.3.1.2 Dairy Cattle

- 5.2.3.1.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Adisseo

- 6.4.2 Alltech, Inc.

- 6.4.3 Archer Daniel Midland Co.

- 6.4.4 BASF SE

- 6.4.5 Cargill Inc.

- 6.4.6 DSM Nutritional Products AG

- 6.4.7 IFF(Danisco Animal Nutrition)

- 6.4.8 Lallemand Inc.

- 6.4.9 Novozymes AS

- 6.4.10 SHV (Nutreco NV)

7 KEY STRATEGIC QUESTIONS FOR FEED ADDITIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms