|

市場調査レポート

商品コード

1911749

インドネシア飼料添加物市場- シェア分析、業界動向、統計、成長予測(2026年~2031年)Indonesia Feed Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドネシア飼料添加物市場- シェア分析、業界動向、統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 80 Pages

納期: 2~3営業日

|

概要

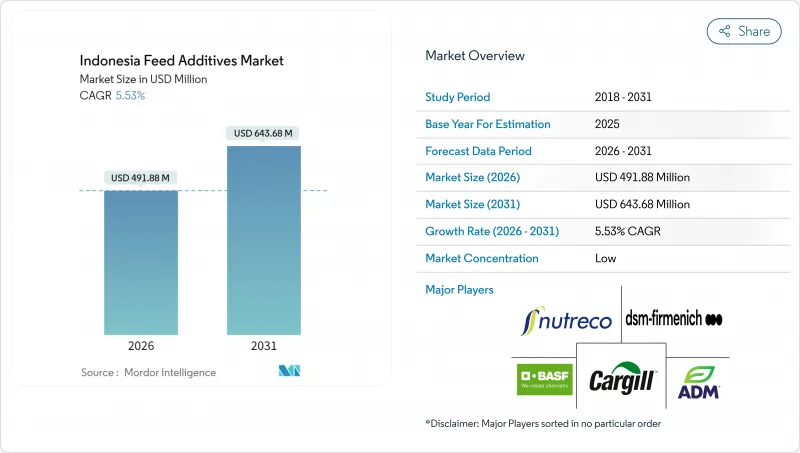

インドネシアの飼料添加物市場規模は、2026年に4億9,188万米ドルと推定されております。

これは2025年の4億6,610万米ドルから成長した数値であり、2031年には6億4,368万米ドルに達すると予測されております。2026年から2031年にかけての年間平均成長率(CAGR)は5.53%で推移する見込みです。

この着実な成長は、東南アジア最大の家禽生産国としてのインドネシアの地位、急速な都市化、そして政府主導による国内タンパク質摂取量増加の推進を反映しています。消費量の伸びが最も顕著なのはジャワ島とスマトラ島であり、大豆ミール価格が変動する中でも、工業用飼料工場が飼料効率向上のためにアミノ酸や酵素の配合率を調整しています。抗生物質成長促進剤の使用を禁止する規制の決定的な転換により、ハラール認証や輸出要件に適合するプロバイオティクス、フィトジェニック、有機酸の導入が促進されています。通貨変動は、現地メーカーが原材料調達先を拡大し輸入コストをヘッジすることを促す一方、ブロックチェーンを活用したトレーサビリティプラットフォームが新たな競合ベンチマーキングを生み出しています。パーム油産業と飼料産業の交差点には、独自の触媒が存在します。バイオディーゼル義務化により、豊富なパーム製品別を活用した高エネルギー密度添加物の需要が高まっているのです。

インドネシア飼料添加物市場の動向と分析

増加する国内家禽タンパク質需要

インドネシアの「無料栄養食プログラム」は8,200万人の受益者を対象としており、家庭のタンパク質嗜好を再構築し、2023年の1人当たり家禽摂取量を7.46kg(2022年比4.3%増)に押し上げています。飼料メーカーはこれに対応し、タンパク質利用効率を向上させるアミノ酸添加率を拡大。同時に生産者が政府調達スキームの価格目標を達成できるよう支援しています。この需要急増は酵素導入も促進し、飼料工場が現地原料からより多くの代謝エネルギーを抽出することを可能にしています。需要はジャワ島とスマトラ島に集中しており、コールドチェーン物流が鶏肉の広範な流通を支えることで、統合事業者がプレミックス施設と契約農場のネットワーク拡大を促しています。

抗生物質成長促進剤の政府規制が代替技術に機会をもたらす

インドネシア食品医薬品監視庁は抗生物質代替品の厳格な登録要件を施行し、プロバイオティクス、プレバイオティクス、フィトジェニックスの導入を加速させています。在来乳酸菌株を用いた商業試験では飼料添加抗生物質と同等の成長性能が実証され、耐性リスクの低減と輸出向けプレミアム基準の達成に貢献しています。早期に自然派ソリューションへ投資した企業は、規制関連費用の削減と製品承認の迅速化により、後発企業に対して明確なコスト優位性を享受しています。規制の明確化は、日本やシンガポールなどの抗生物質不使用家禽市場向け供給国としてのインドネシアの地位確立を支えています。

主要原料の輸入依存度の高さ

インドネシアは、中国、欧州、北米からの合成アミノ酸、ビタミン、特殊酵素の輸入に大きく依存しています。輸送の遅延や書類の不備は、ジャワ島にある工場の生産停止を招く可能性があります。小規模な事業者は、貿易省の輸入ライセンシング手続きに苦労しています。現在、各出荷ごとに電子分析証明書が要求されるため、通関手続きが長期化しています。多くの製造業者は3ヶ月分の安全在庫を保有しており、運転資金を拘束し、倉庫費用を増加させています。これは、価格に敏感な農家によって既に圧迫されている市場において、さらなる負担となっています。

セグメント分析

2025年時点で、アミノ酸はインドネシア飼料添加物市場規模の23.15%を占めており、大豆ミール依存度を低減するタンパク質効率化戦略における重要性を示しています。東ジャワの養鶏統合企業は、世界のサプライヤーからリシンのバルク契約を確保し、配合変動を抑制するため自社内にプレミックスラインを設置しています。また、高密度養殖池におけるエビの生存率向上を目的とした水産飼料への合成メチオニン添加も、本セグメントの成長に寄与しています。

酸性化剤は最も成長が速いカテゴリーであり、2031年までCAGR6.12%で推移すると予測されています。これは、病原菌を抑制し腸内pHを安定させるフマル酸や乳酸などの有機酸への、抗生物質後時代の転換を反映しています。プロバイオティクスと酵素は、現地の研究開発に後押しされ、高湿度環境でも生存するBS4のような熱帯環境耐性菌株を飼料メーカーが試験的に採用する中で、注目を集めています。ビタミン・ミネラルは全種共通の必須添加物であり続ける一方、フィトジェニックは自然派表示を採用する生産者から再び注目を集め、プレミアム輸出市場へのアクセスを可能にしております。

インドネシア飼料添加物市場レポートは、添加物別(酸性化剤、アミノ酸、抗生物質、抗酸化剤、結合剤、酵素、香料・甘味料、ミネラル、マイコトキシン解毒剤、フィトジェニック、色素、プレバイオティクスなど)、動物別(水産養殖、家禽、反芻動物、豚など)、地域別に分類されています。市場予測は、金額(米ドル)および数量(メトリックトン)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 エグゼクティブサマリー主要な調査結果

第2章 レポート提供

第3章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

- 調査手法

第4章 業界の主要動向

- 家畜頭数

- 家禽

- 反芻動物

- 豚

- 飼料生産

- 水産養殖

- 家禽

- 反芻動物

- 豚

- 規制の枠組み

- インドネシア

- バリューチェーン及び流通チャネル分析

- 市場促進要因

- 国内の家禽タンパク質需要の増加

- 政府による抗生物質成長促進剤の使用禁止が代替機会の創出につながっています

- 大豆ミール使用量を削減する費用対効果の高いアミノ酸補給

- インドネシアの研究所によるプロバイオティクス研究開発の急増

- パーム油バイオディーゼル政策の強化によりエネルギー密度添加剤の需要が増加

- ハラル飼料コンプライアンスのためのブロックチェーン追跡プログラム

- 市場抑制要因

- 主要原材料に対する高い輸入依存度

- ルピア相場の変動が添加剤の投入コスト上昇を招いています

- 複雑な規制環境がコンプライアンスコストを増加させております

- カリマンタン及びスラウェシにおけるインフラの不足が物流コストを押し上げております

第5章 市場規模と成長予測(数量と金額)

- 添加物

- 酸性化剤

- フマル酸

- 乳酸

- プロピオン酸

- その他の酸性化剤

- アミノ酸

- リジン

- メチオニン

- トレオニン

- トリプトファン

- その他のアミノ酸

- 抗生物質

- バシトラシン

- ペニシリン類

- テトラサイクリン系抗生物質

- タイロシン

- その他の抗生物質

- 抗酸化剤

- ブチル化ヒドロキシアニソール(BHA)

- ブチル化ヒドロキシトルエン(BHT)

- クエン酸

- エトキシキン

- プロピルガレート

- トコフェロール

- その他の抗酸化剤

- 結合剤

- 天然結合剤

- 合成結合剤

- 酵素

- 炭水化物分解酵素

- フィターゼ

- その他の酵素

- 香料および甘味料

- 香料

- 甘味料

- ミネラル類

- 主要ミネラル

- 微量ミネラル

- マイコトキシン解毒剤

- 結合剤

- バイオトランスフォーマー

- その他のマイコトキシン解毒剤

- 植物性原料

- 精油

- ハーブとスパイス

- その他の植物性原料

- 色素

- カロテノイド

- クルクミンとスピルリナ

- プレバイオティクス

- フルクトオリゴ糖

- ガラクトオリゴ糖

- イヌリン

- ラクツロース

- マンナンオリゴ糖

- キシロオリゴ糖

- その他のプレバイオティクス

- プロバイオティクス

- ビフィズス菌

- エンテロコッカス

- 乳酸菌

- ペディオコッカス

- 連鎖球菌

- その他のプロバイオティクス

- ビタミン

- ビタミンA

- ビタミンB

- ビタミンC

- ビタミンE

- その他のビタミン

- 酵母

- 生酵母

- セレン酵母

- 使用済み酵母

- トルラ乾燥酵母

- ホエイ酵母

- 酵母由来製品

- 酸性化剤

- 動物

- 水産養殖

- 魚類

- エビ

- その他の養殖魚種

- 家禽

- ブロイラー

- 採卵鶏

- その他の家禽類

- 反芻動物

- 肉用牛

- 乳用牛

- その他の反芻動物

- 豚

- その他の動物

- 水産養殖

第6章 競合情勢

- 主要な戦略的動き株式会社

- 市場シェア分析

- 企業概要

- 企業プロファイル.

- Cargill, Incorporated.

- DSM-Firmenich

- Ajinomoto Co., Inc.

- Nutreco NV(SHV Holdings NV)

- BASF SE

- Kemin Industries, Inc.

- Evonik Industries AG

- PT Japfa Comfeed Indonesia Tbk

- PT Charoen Pokphand Indonesia Tbk

- Alltech, Inc.

- Brenntag SE

- Novus International, Inc.(Mitsui & Co., Ltd.)

- ADM

- East Hope Group

- Zinpro Corporation