|

市場調査レポート

商品コード

1686564

欧州のガラスパッケージング:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Glass Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のガラスパッケージング:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

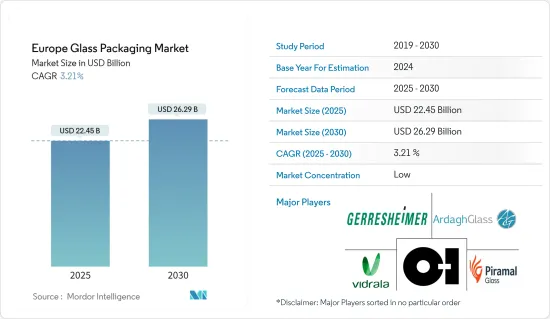

欧州のガラスパッケージング市場規模は2025年に224億5,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは3.21%で、2030年には262億9,000万米ドルに達すると予測されます。

主なハイライト

- 欧州のガラス産業は、飲食品、化粧品、薬局、香水産業向けにガラスパッケージング製品を提供しています。包装材料としてのガラスの適合性は、市場の成長を促進する重要な要因です。環境に優しい包装材を使おうという傾向が強まっていることも、ガラスパッケージング市場の促進要因となっています。

- 安全で健康的な包装に対する消費者の需要の高まりは、様々なカテゴリーにおけるガラスパッケージングの成長を後押ししています。ガラスにエンボス加工を施し、成形し、芸術的な仕上げを加える革新的な技術は、ガラスパッケージングをエンドユーザーの間でより望ましいものにしています。さらに、環境に優しい製品に対する需要の増加や飲食品業界からの需要の高まりといった要因も、市場の成長を促しています。

- この地域における持続可能性とリサイクル性に関する新しい規則も、ガラスパッケージングの成長を後押しする顕著な要因です。欧州連合の包装・包装廃棄物規制(PPWR)提案では、各EU加盟国は一人当たりの包装廃棄物を2030年までに5%、2035年までに10%、2040年までに15%削減することが求められており、これが再生ガラスの需要をさらに押し上げています。

- ガラスは、ワイン、蒸留酒、ビールなどの主要なアルコール飲料の包装材料として、引き続き基準となっています。ガラスは食品、水、乳製品産業で顕著なシェアを獲得しています。この背景には、地元産、有機、自然食品に対する新たな消費動向、ガラスパッケージングのポジティブなイメージ、環境・健康・味覚保存の観点から好ましい包装材としてのガラスに対する消費者の強い信頼があります。

- この地域のガラスパッケージング産業が直面している主な課題の一つは、エネルギー価格の高騰であり、これが市場の成長を妨げています。ガラス生産にはエネルギー集約的な性質があるため、メーカーがこうしたコスト上昇を吸収するのは困難です。加えて、ロシアとウクライナの紛争が続いているため、英国のガラスパッケージングメーカーにとっては状況が激化し、エネルギー費用の高騰につながっています。その結果、こうしたエネルギー価格の高騰が生産コストを押し上げ、ガラス価格の上昇につながっています。

- さらに、いくつかのワイン・メーカーは、サプライ・チェーンの寸断や不活発な炉のために、代替品としてプラスチックに切り替えています。例えば、英国ではアルコール飲料メーカーがガラス製パッケージから紙製ボトルに切り替える動きが加速しています。最近、大手小売業者のアルディが、食品用パウチを備えた94%再生板紙製のボトル入りワインを発売しました。

欧州のガラスパッケージング市場の動向

飲料分野が大きな市場シェアを占める

- 欧州の飲料市場は力強い成長を遂げ、大きな市場シェアを確保する見込みです。持続可能で利便性の高い飲料パッケージへの需要が高まる中、業界専門家は欧州飲料市場の拡大を予測しています。欧州のパッケージング生産と製造プロセスにおける継続的な進歩は、業界の環境適合性を高めています。パッケージング企業は、エネルギーと水の消費を抑え、二酸化炭素排出量を削減するリサイクル材料から製品を生産することで、持続可能な実践にますます力を入れるようになっています。

- 魅力的なデザインと魅力的な配色を備えた革新的で軽量な製品を、より低い生産コストで製造することは、成長を促進する重要な要因であり続けています。著名な飲料メーカーもガラスパッケージングの採用を増やしており、これが欧州における飲料セグメントのシェアに拍車をかけています。例えば、2023年9月、コカ・コーラHBCはオーストリアのエーデルスタール工場に高速リターナブルガラスボトリングライン(RGB)を新設しました。コカ・コーラHBCによる1,200万ユーロ(1,299万米ドル)の投資は、包装の実際の循環経済を可能にするための飲料会社および小売業者向け基金の一環として、オーストリア政府からの400万ユーロ(433万米ドル)の助成金によって支援されました。

- 輸出の増加とともに、ワインなどのアルコール飲料の生産が伸びていることが、ガラスパッケージングの需要をさらに押し上げています。例えば、欧州委員会によると、EUにおけるワイン生産量は2022年の1億5,290万ヘクトリットルから2023年には1億5,900万ヘクトリットルに達します。国連貿易委員会(UN Comtrade)によれば、2023年の欧州におけるワインの最大輸出国はフランスとイタリアで、それぞれ127億8,940万米ドルと84億320万米ドルでした。

- 深刻化するプラスチック汚染に対応するため、この地域の飲料メーカーは、飲料製品の需要が急速に伸びていることから、詰め替え可能なガラス瓶への移行を進めています。例えば、コカ・コーラは2023年8月、プラスチック汚染削減へのコミットメントを果たすため、コーク・ゼロのガラス瓶を顧客と直接配送、回収、再利用する新しいシステムを開始しました。この飲料は、宅配サービスのミルク&モアと提携し、英国の家庭に配られます。この試みは2023年6月5日に開始され、ロンドン南部とイングランド南部中心部で夏の間継続される予定でした。

大幅な市場成長が期待されるポーランド

- ポーランドは、予測期間中、東欧で最も顕著なパッケージングの成長を遂げると予想されています。ガラス瓶の開発は、ボトル入り飲料水、ジュース、エナジードリンク、プレミアム飲料によって促進されると予想されます。

- ポーランドのガラスパッケージング市場におけるM&Aの動向は、競争力と市場シェアを強化するための企業間の統合傾向を示しています。このような統合は、効率性の向上、技術革新、潜在的な価格ダイナミクスにつながり、ポーランドのガラスパッケージング市場情勢を形成すると思われます。例えば、2024年4月、キャンパック・グループとBA Glass社は、キャンパックのポーランドにおけるガラス事業をBA Glass社に売却することを発表しました。その結果、オルゼゼのガラス工場はBA Glassに譲渡され、ポーランドでの事業の一部となりました。

- ポーランドのガラス産業は製造能力を多様化しています。ポーランドのガラス産業では、容器用ガラスの製造に大量のガラス砂が使用されています。このような制度への移行を開始するため、ポーランド政府は2022年にガラス瓶とペットボトルのデポジット義務化の導入準備を開始しました。デポジット制度には、1.5リットルまでの再利用可能なガラス瓶も含まれます。ポーランドは、ガラス瓶が主要な包装材料であり、他の種類の包装材料が占める割合はわずかである飲料産業において、強力な業績を維持すると予想されます。

- この業界で事業を展開する企業は、国内での事業拡大を通じて新しいソリューションの革新に注力しています。例えば、2023年1月、Ardagh Glass Packaging社はポーランドで持続可能なガラス炉を設計しました。この新しい炉は、ガス、電気、水の使用量を複数の持続可能な方法によって最小化する一方で、低排出レベルを獲得・維持することができます。同社によると、ガス、電気、水の使用は、熱回収、ターボ・コンプレッサー、水回収、クローズド・ループ冷却手順によって最小化されます。このガラスメーカーは、排出量を削減し、環境への影響を高めることは、ガラス産業にとって極めて重要な目標であると述べています。大手企業によるこのような技術革新は、予測期間中の市場成長を促進すると予想されます。

- さらに、日本ではガラスパッケージングを使用する飲料やその他の製品の輸出が大きく伸びています。例えば、UN Comtradeによると、2023年のポーランドの飲料、蒸留酒、食酢の輸出額はほぼ横ばいの約16億ユーロです。このような輸出の伸びにより、ポーランドではガラスパッケージング製品に対する需要がさらに高まると予想されます。

欧州のガラスパッケージング業界の概要

欧州のガラスパッケージング市場は競争が激しく、多くの地域企業が大きなシェアを占めています。これらの企業は、市場シェアと収益性を高めるために戦略的イニシアチブを活用しています。

- 2024年7月、著名な飲食品用ガラスパッケージングメーカーであるヴェラリア社は、イタリアのヴィドラーラ社のガラス事業を買収しました。企業価値2億3,000万ユーロ(2億4,890万米ドル)のこの取引には、コルシコを拠点とする工場が含まれていました。この工場は、最近改修された2つの炉を備え、年産能力225キロトンの近代的な生産能力を特徴としています。食品、ビール、蒸留酒市場で積極的に事業を展開しています。

- 2024年5月、ゲレスハイマーAGの間接子会社であるゲレスハイマー・グラスは、ボルミオリ・ファーマ・グループの持株会社であるブリッツ・ルクスコSarlを買収する契約を締結しました。この買収により、ゲレスハイマーは南欧を中心とした欧州での生産拠点が増加し、欧州での事業基盤が強化されました。また、製薬・バイオテクノロジー業界をリードするフルサービスプロバイダーおよび世界パートナーとしての市場地位も強化されます。

- 2023年9月、オーアイは先進的なエンボス・カスタマイズパッケージングの提供を開始しました。O-I:エクスプレッションズ・シグネチャー」により、O-Iは可変データ印刷を使用して装飾ガラス瓶を製造する初のガラスメーカーとなりました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- ミクロ経済要因が市場に与える影響の評価

第5章 市場力学

- 市場促進要因

- 厳しい規制による持続可能な包装への急速なシフト

- 飲料や化粧品などのエンドユーザー産業におけるプレミアムガラスパッケージングの採用拡大

- 市場の課題

- 市場成長の課題となる代替包装形態

第6章 市場セグメンテーション

- 製品タイプ別

- ボトル

- アンプル

- バイアル

- シリンジ

- ジャー

- エンドユーザー産業別

- 飲料

- 酒類

- ビール

- ソフトドリンク

- その他飲料

- 食品

- 化粧品

- 医薬品

- 飲料

- 国別

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ポーランド

- オランダ

- その他欧州

第7章 競合情勢

- 企業プロファイル

- Owens-Illinois Inc.

- Origin Pharma Packaging

- Verallia

- Vidrala SA

- Vetropack Holding Ltd

- Vitro SAB de CV

- APG Europe

- Saverglass Group

- Wiegand-Glass GmBH

- Crestani SRL

- Verescene France SASU

- Stolzle Glass Group

- Ardagh Packaging Group PLC

- SGD Pharma SA

- Beatson Clark PLC

- Stevanato Group

- Gerresheimer AG

- BA Vidro SA(BA Glass BV)

- Glassworks International Limited

- Gaasch Packaging(UK)Ltd

第8章 投資分析

第9章 市場の将来

目次

Product Code: 52667

The Europe Glass Packaging Market size is estimated at USD 22.45 billion in 2025, and is expected to reach USD 26.29 billion by 2030, at a CAGR of 3.21% during the forecast period (2025-2030).

Key Highlights

- The European glass industry offers glass packaging products for the food and beverage, cosmetics, pharmacy, and perfumery industries. The compatibility of glass as a packaging material is a significant factor propelling the market's growth. The growing inclination toward using environment-friendly packaging material is another driver for the glass packaging market.

- Increasing consumer demand for safe and healthier packaging is helping glass packaging grow in different categories. Innovative technologies for embossing, shaping, and adding artistic finishes to glass make glass packaging more desirable among end users. Furthermore, factors such as the increasing demand for eco-friendly products and the rising demand from the food and beverage industry are stimulating the market's growth.

- The new rules for sustainability and recyclability in the region are also prominent factors pushing the growth of glass packaging. The European Union's Packaging and Packaging Waste Regulation (PPWR) proposals outline that each EU Member State could be required to reduce its packaging waste per capita by as much as 5% by 2030, 10% by 2035, and 15% by 2040, which is further driving the demand for recycled glass.

- Glass continues to be the reference packaging material for leading alcoholic beverages such as wines, spirits, and beer. It is gaining a prominent share in the food, water, and dairy industries. This is due to new consumption trends for local, organic, and natural food, the positive image of glass packaging, and strong consumer trust in glass as the preferred packaging for environmental, health, and taste preservation reasons.

- One of the primary challenges facing the glass packaging industry in the region is the surge in energy prices, which is hindering market growth. The energy-intensive nature of glass production makes it difficult for manufacturers to absorb these rising costs. Additionally, the ongoing conflict between Russia and Ukraine has intensified the situation for glass packaging producers in the United Kingdom, leading to soaring energy expenses. As a result, these escalating energy prices have driven up production costs, thereby increasing the price of glass.

- Furthermore, several wine manufacturers have switched to plastic as an alternative due to disrupted supply chains and inactive furnaces. For instance, the trend of alcoholic beverage companies in the United Kingdom replacing glass packaging with bottles made of paper has picked up pace. Recently, Aldi, a leading retailer, recently introduced wine in bottles made from 94% recycled paperboard, featuring a food-grade pouch.

Europe Glass Packaging Market Trends

Beverages Segment to Hold a Significant Market Share

- The European beverages market is poised for robust growth and is expected to secure a significant market share. As demand for sustainable and convenient beverage packaging increases, industry experts anticipate an expansion in the European beverages market. Continuous advancements in Europe's packaging production and manufacturing processes are enhancing the industry's environmental friendliness. Packaging companies are increasingly focusing on sustainable practices by producing products from recycled materials, which consume less energy and water while reducing carbon emissions.

- Creating innovative, lightweight products with appealing designs and appealing color schemes at lower production costs has continued to be a key growth facilitator. Prominent beverage companies are also raising the adoption of glass packaging, which adds to the beverage segment's share in Europe. For instance, in September 2023, Coca-Cola HBC established a new, high-speed returnable glass bottling line (RGB) at the Edelstal plant in Austria. An investment of EUR 12 million (USD 12.99 million) from Coca-Cola HBC was supported by a grant of EUR 4 million (USD 4.33 million) from the Austrian government as part of its fund for beverage companies and retailers to enable an actual circular economy for packaging.

- The growth in the production of alcoholic beverages, such as wine, along with a rise in exports, is further boosting demand for glass packaging. For instance, according to the European Commission, wine production in the European Union reached 159 million hectoliters in 2023 from 152.9 million hectoliters in 2022. As per the UN Comtrade, France and Italy were the largest exporters of wine in Europe in 2023, with values of USD 12,789.4 million and USD 8,403.2 million, respectively.

- In response to the escalating plastic pollution, beverage manufacturers in the region are increasingly transitioning to refillable glass bottles due to the rapidly growing demand for beverage products. For instance, in August 2023, to fulfill its commitment to reducing plastic pollution, Coca-Cola launched a new system for delivering, collecting, and reusing glass bottles of Coke Zero directly with customers. The beverage is being distributed to homes in the United Kingdom in partnership with delivery service Milk & More. The trial began on June 5, 2023, and was to continue throughout the summer in south London and central southern England.

Poland Expected to Witness Significant Market Growth

- Poland is anticipated to experience the most significant growth in packaging in Eastern Europe during the forecast period. The development of glass bottles is expected to be fueled by bottled water, juice, energy drinks, and premium beverages.

- The rising mergers and acquisitions in the Polish glass packaging market indicate a consolidation trend among companies to enhance competitiveness and market share. This consolidation is likely to lead to increased efficiency, innovation, and potential pricing dynamics, shaping the landscape of the Polish glass packaging market. For instance, in April 2024, CANPACK Group and BA Glass announced the finalization of the sale of CANPACK's Glass operations in Poland to BA Glass. Consequently, the glass plant in Orzesze was transferred to BA Glass and became part of its operations in Poland.

- The Polish glass industry has diversified its manufacturing capabilities. In the Polish glass industry, significant amounts of glass sand are used to produce container glass. To initiate the country's transition to such a system, the Polish government began preparing the introduction of a mandatory deposit for glass and plastic bottles in 2022. The deposit system included reusable glass bottles of up to 1.5 liters. Poland is expected to remain a strong performer in the beverages industry, where glass bottles may be the primary packaging material, with a small share held by other packaging types.

- Companies operating in the industry are focused on innovating new solutions through expansions in the country. For instance, in January 2023, Ardagh Glass Packaging designed a sustainable glass furnace in Poland. The new furnace can gain and maintain lower emission levels while gas, electricity, and water usage will be minimized via multiple sustainable methods. According to the firm, gas, electricity, and water usage will be minimized via heat recovery, turbo compressors, water recovery, and a closed-loop cooling procedure. The glass manufacturer stated that reducing emissions and enhancing the effect on the environment is a crucial goal for the glass industry. Such technological innovations by major companies are expected to fuel market growth during the forecast period.

- Moreover, the country has witnessed significant growth in the export of beverages and other products that use glass packaging. For instance, according to UN Comtrade, in 2023, the value generated from the export of beverages, spirits, and vinegar in Poland remained nearly unchanged at around EUR 1.6 billion. This growth in exports is anticipated to further create demand for glass packaging products in Poland.

Europe Glass Packaging Industry Overview

The European glass packaging market is highly competitive, with many regional players holding significant shares in the market. These companies are leveraging strategic initiatives to increase market share and profitability.

- In July 2024, Verallia, a prominent producer of glass packaging for food and beverage products, acquired Vidrala's glass business in Italy. The transaction, valued at an enterprise value of EUR 230 million (USD 248.9 million), included a Corsico-based plant. This facility, equipped with two recently renovated furnaces, features modern production capabilities with an annual capacity of 225 kilotons. It actively operates in the food, beer, and spirits markets.

- In May 2024, Gerresheimer Glas, an indirect subsidiary of Gerresheimer AG, signed an agreement to acquire Blitz LuxCo Sarl, the holding company of Bormioli Pharma Group. This acquisition enhances Gerresheimer's European footprint with additional production sites, particularly in Southern Europe. It also strengthens its market position as a leading full-service provider and global partner for the pharmaceutical and biotech industries.

- In September 2023, O-I launched an advanced, embossed, customized packaging offering. With its O-I: Expressions Signature, O-I became the first glass manufacturer to produce decorated glass bottles using variable data printing.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of Microeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid Shift Toward Sustainable Packaging Due to Stringent Regulations

- 5.1.2 Growing Adoption of Premium Glass Packaging in End-user Industries, such as Beverages and Cosmetics

- 5.2 Market Challenge

- 5.2.1 Alternative Forms of Packaging Challenging the Market's Growth

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Bottles

- 6.1.2 Ampoules

- 6.1.3 Vials

- 6.1.4 Syringes

- 6.1.5 Jars

- 6.2 By End-user Industry

- 6.2.1 Beverage

- 6.2.1.1 Liquor

- 6.2.1.2 Beer

- 6.2.1.3 Soft Drinks

- 6.2.1.4 Other Beverages

- 6.2.2 Food

- 6.2.3 Cosmetics

- 6.2.4 Pharmaceuticals

- 6.2.1 Beverage

- 6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Spain

- 6.3.6 Poland

- 6.3.7 Netherlands

- 6.3.8 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Owens-Illinois Inc.

- 7.1.2 Origin Pharma Packaging

- 7.1.3 Verallia

- 7.1.4 Vidrala SA

- 7.1.5 Vetropack Holding Ltd

- 7.1.6 Vitro SAB de CV

- 7.1.7 APG Europe

- 7.1.8 Saverglass Group

- 7.1.9 Wiegand-Glass GmBH

- 7.1.10 Crestani SRL

- 7.1.11 Verescene France SASU

- 7.1.12 Stolzle Glass Group

- 7.1.13 Ardagh Packaging Group PLC

- 7.1.14 SGD Pharma SA

- 7.1.15 Beatson Clark PLC

- 7.1.16 Stevanato Group

- 7.1.17 Gerresheimer AG

- 7.1.18 BA Vidro SA (BA Glass BV)

- 7.1.19 Glassworks International Limited

- 7.1.20 Gaasch Packaging (UK) Ltd