|

市場調査レポート

商品コード

1637834

インドのガラス包装:市場シェア分析、産業動向、成長予測(2025~2030年)India Glass Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドのガラス包装:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

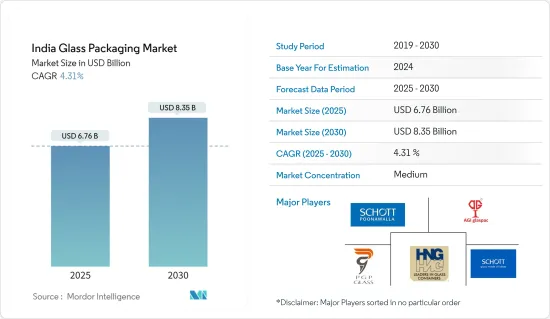

インドのガラス包装の市場規模は2025年に67億6,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは4.31%で、2030年には83億5,000万米ドルに達すると予測されます。

包装と関連産業の製造・生産は、包装がGDPに大きく貢献している多くの国でのみ機能しています。この動向は、国内のガラス包装業者から製薬業界への焦点の移行を示しました。

主なハイライト

- インドは製薬・バイオ産業の労働力において世界第2位のシェアを占めています。2021年のインド経済調査によると、医薬品市場は今後10年間で3倍に成長すると予想されています。同国の医薬品市場は2021年に410億米ドルと予測され、2024年には650億米ドルに達し、さらに2030年には1,200~1,300億米ドル規模に拡大します。

- 非多孔性、不浸透性、環境に優しい、美観に優れているなどのガラス瓶の特性により、包装産業での使用はますます増加しています。インドでは、ガラス産業はよく確立されており、長い間家内工業のままでした。この部門は最近、手作業の工程から近代的な自動化手法へと進化しつつあります。Hindusthan National Glass &Industries Ltd.によると、インドの一人当たりのガラス包装消費量(1.8kg)は他国に比べてはるかに少ないです。

- ガラス包装は再利用が可能で、プラスチック包装に代わる環境に優しい代替品であることから、消費者の環境意識の高まりもガラス包装業界を牽引しています。また、可処分所得の増加や消費者のライフスタイルの変化も市場の成長を促進すると予想されます。

- 市場の主な課題のひとつは、アルミ缶やプラスチック容器などの代替包装形態との競合が激化していることです。アルミ缶やプラスチック容器は、かさばるガラスよりも重量が軽く、運搬や輸送にかかるコストが低いため、メーカーや顧客の間で人気を集めています。さらに、ガラス包装業界は最近、国内での偽造行為を制限するため、トレーサビリティの向上に注力しています。各社は容器に恒久的な刻印を施し、偽造品メーカーによる有害な行為から消費者を守っています。

- 国内におけるCOVID-19用ワクチンへの最近の投資動向は、バイアル瓶成長の重要な推進力として浮上しています。例えば、IBEFによると、インドの製薬セクターは各種ワクチンの世界需要の50%以上、米国のジェネリック市場の約40%、英国の全医薬品の25%を供給しています。

インドのガラス包装市場の動向

大きな需要が見込まれるガラス瓶/容器

- インドでは、消費者が環境に優しく健康的な選択肢を重視し、他の選択肢よりもガラス包装を好むため、ガラス包装ソリューション、特にボトルの使用のみが増加しています。また、ヒンドゥスタン・ナショナル・グラス社やアサヒ・インド・グラス社など多くの企業が、あらゆる産業分野でガラスパッケージング・ソリューションを提供しています。

- 昨年、インドの容器用ガラスメーカーであるサンライズガラス社は、240TPDの設備能力を持つ新しい炉を増設しました。同社は現在2基の炉を操業しており、合計で380TPDの設備能力を有しています。同社は、このストーブにはAIS 10トリプルゴブ(TG)エムハートマシン3台を備えた4つのラインがあると述べています。全ラインにEVM(検査機)が設置されます。この生産能力拡大により、同社は酒類メーカーを中心に、食品用ジャーをアメリカや欧州に輸出しています。

- 多国籍の製薬用ガラスメーカーは、インドの製薬用ガラスメーカーとともに、過去3年間に設計能力の増強に投資してきました。また、世界の大手製薬用ガラスメーカーであるGerresheimer社、SGD Pharma社、Schott社は、インド事業に資本投資を行っています。他のプレーヤーによるこのような取り組みが近年行われ、国内のガラス瓶需要を促進すると推定されます。

- 飲食品、食品加工、パーソナルケア、医薬品の各エンドユーザー産業への多大な投資により、インドのボトル・容器用ガラス産業には大きなビジネスチャンスが生まれています。数量ベースでは酒類が最大のサブセグメントであり、飲食品、医薬用ガラス、化粧品・香水がこれに続く。

飲料分野は大きな需要が見込まれる

- ガラスびん・容器は、化学的不活性、無菌性、非透過性を維持できることから、アルコール・非アルコール飲料産業で主に使用されています。ガラスは飲料に含まれる化学物質と反応しないため、これらの飲料の香り、強さ、風味を保持し、優れた包装オプションとなることから、ビールなどの飲料が大きな市場シェアを占めています。こうした理由から、ビールの輸送量の大半はガラス瓶で輸送されており、この動向は調査期間中も続くと予想されます。ビールは、紫外線にさらされると腐敗しやすい内容物を保存するため、濃い色のガラス瓶で包装されます。

- 国内では、飲料のエンドユーザーが市場需要を牽引しています。ASSOCHAMによると、インドの飲料分野ではガラスと硬質プラスチックが包装の約3分の2を占めています。しかし、環境問題への関心の高まりから、ガラス包装の範囲は拡大しています。飲料、特にアルコール飲料のRTD(Ready to Drink)分野でのガラス包装の使用増加が、インドの飲料包装業界の現在の動向です。ガラス包装業界は、主に国内のアルコール飲料消費量の増加によって後押しされています。

- また、ICRIER(インド国際経済関係研究評議会)によると、今後10年間のインドにおけるアルコール飲料消費の伸びの70%以上は、中低所得層と高所得層が牽引することになり、製品のプレミアム化の傾向が強まっています。

- ソフトドリンクは、ノンアルコール飲料のビジネスを支える最も重要な貢献者です。インドにおけるコーラの売上シェアは、ガラス瓶が35%を占めています。飲料メーカーのCoca-Cola India Pvt. Ltd.は、リターナブルのガラス瓶を再び推進しています。昨年、一部の州で10インドルピー(0.15米ドル)の価格帯(200ml)で展開されたボトルは、コカ・コーラ、サムズアップ、スプライトといった同社の売れ筋ブランドで販売されています。一部の市場では、ガラス瓶が飲料売上の30%を占めるようになっている(出典:コカ・コーラ)。

- 多くの飲料がガラス瓶を使用すると予想され、特に大手メーカーのものはガラス瓶で装飾されています。ユーザーにとっての主な利点は、ジュースやその他の飲料の包装容器としてガラスびんを使用した場合、容器材料からの溶出がほとんどないことです。

インドのガラス包装業界の概要

インドのガラス包装市場は、複数のプレーヤーによる競争により、市場は適度に統合されています。Schott Kaisha Pvt Ltd.、AGI glaspac.、Piramal Glass Limited、Borosil Glass Works Limited、Haldyn Glass Limitedといった市場のプレーヤーは、市場シェアをさらに拡大するために、製品革新、パートナーシップ、M&Aといった戦略を採用しています。市場における重要な進展は以下の通り:

- 2022年8月-ソーダ灰メーカーのNirmaは、最も著名なHindustan National Glass Limited(HNGL)を買収する165億インドルピー(2億600万米ドル)の計画を提出しました。アフリカを拠点とするボトルメーカーMadhvani Groupと容器ガラスメーカーAGI Greenpacも、それぞれ別の決議計画を提出しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の業界への影響評価

- 貿易シナリオ分析

第5章 市場力学

- 市場促進要因

- 国民の環境意識の高まり

- 国内での飲料消費の増加

- 市場抑制要因

- アルミやプラスチックなどの代替包装オプション

第6章 市場セグメンテーション

- 製品別

- ボトル/容器

- バイアル

- アンプル

- シリンジ/カートリッジ

- エンドユーザー業界別

- 食品

- 飲料(ソフトドリンク、牛乳、アルコール飲料、その他の飲料タイプ)

- 化粧品、香水、パーソナルケア

- 医薬品

第7章 競合情勢

- 企業プロファイル

- Schott Kaisha Pvt Ltd(SCHOTT AG)

- AGI Glaspac(HSIL Ltd)

- Piramal Glass Limited

- Hindustan National Glass & Industries Limited(HNGIL)

- Schott Poonawalla Private Limited

- Gerresheimer AG

- Borosil Glass Works Limited(Klasspack Pvt. Ltd.)

- Haldyn Glass Limited(HGL)

- Sunrise Glass Industries Private Limited

- Ajanta Bottle Pvt Ltd

- G.M Overseas

- Empire Industries Limited-Vitrum Glass

第8章 投資分析

第9章 市場の将来展望

The India Glass Packaging Market size is estimated at USD 6.76 billion in 2025, and is expected to reach USD 8.35 billion by 2030, at a CAGR of 4.31% during the forecast period (2025-2030).

The manufacturing and production of packaging and relatable industries are only functional in many countries where packaging contributes significantly to GDP. The trend witnessed a shift of focus from glass packagers in the country to the pharmaceutical industry.

Key Highlights

- India contributes the second-largest share of the pharmaceutical and biotech workforce worldwide. According to the Indian Economic Survey of 2021, the pharmaceutical market is expected to grow three times in the next decade. The country's pharmaceutical market was projected at USD 41 billion in 2021 and will reach USD 65 billion by 2024 and further expand to around USD 120-130 billion by 2030.

- Glass bottle characteristics, such as being non-porous, impermeable, eco-friendly, and aesthetically pleasing, lead to ever-increasing use in the packaging industry. In India, the glass industry is well established and has remained a cottage industry for a long time. The sector is recently evolving from hand-working processes to modern automation methods. According to the Hindusthan National Glass & Industries Ltd, Indian per capita consumption of glass packaging (1.8 kg) is much lower than other nations.

- The glass packaging industry is also driven by the growing environmental awareness among consumers, with glass packaging being reusable and an environmentally friendly alternative to plastic packaging. The increasing disposable incomes and changing consumers' lifestyles are also expected to drive the market's growth.

- One of the main challenges for the market is the increased competition from alternative forms of packaging, such as aluminum cans and plastic containers. The items are lighter in weight than the bulky glass, gaining popularity among manufacturers and customers because of the lower cost involved in their carriage and transportation. Moreover, the glass packaging industry is recently concentrating on increasing traceability to restrict counterfeit activities in the country. The companies are mentioned using permanent engravings on containers, protecting consumers from harmful practices by spurious product manufacturers.

- The recent investing trend in vaccines for COVID-19 in the country is emerging as a significant driver for the vials growth. For instance, according to IBEF, the Indian pharmaceutical sector supplies more than 50% of the global demand for various vaccines, around 40% of the generic market for the United States, and 25% of all medicines for the United Kingdom.

India Glass Packaging Market Trends

Glass Bottles/Containers Expected to Witness Significant Demand

- In India, only the usage of glass packaging solutions, especially bottles, is increasing as consumers emphasize eco-friendly and healthy options and prefer glass packaging over other options. Also, the country comprises many companies, including Hindustan National Glass and Asahi India Glass, offering glass packaging solutions across industries.

- Last year, India's container glass producer Sunrise Glass added a new furnace with an installed capacity of 240 TPD. The company currently operates two furnaces with a combined installed of 380 TPD. The company stated that the stove would have four lines with three AIS 10 triple gob (TG) Emhart Machines. All the lines will have EVM (Inspection Machines). With this capacity expansion, the company focuses on catering to significant liquor clients and exports to the USA and Europe for food-grade jars.

- Multinational pharmaceutical glass producers, along with Indian pharmaceutical glass producers, have invested in increasing designed capacity over the last three years. In addition, leading global pharmaceutical glass producers Gerresheimer, SGD Pharma, and Schott have invested capital in Indian operations. Such initiatives by other players are estimated to take place in recent years and will fuel the demand for glass bottles in the country.

- Considerable investments in the beverages, food processing, personal care, and pharmaceutical end-user industries have created enormous opportunities for the country's bottles/container glass industry. Alcoholic beverages are the largest sub-segment for bottles/container glass consumption on a volume basis, followed by food, pharmaceutical glass, and cosmetics & perfumery.

Beverage Sector Expected to Witness Significant Demand

- Glass bottles and containers are majorly used in the alcoholic and non-alcoholic beverage industries due to their ability to maintain chemical inertness, sterility, and non-permeability. Drinks such as beer account for a significant market share, as glass does not react with the chemicals present in drinks and, therefore, preserves the aroma, strength, and flavor of these beverages, making them a good packaging option. Due to this reason, most beer volume is transported in glass bottles, and this trend is expected to continue over the study period. Beer is packaged in dark-colored glass bottles to preserve the contents, which are prone to spoilage when exposed to UV light.

- The beverage end-user vertical is driving the market demand in the country. According to ASSOCHAM, glass and rigid plastics constitute about two-thirds of packaging in India's beverage sector. However, the industry's glass packaging scope is expanding due to growing environmental concerns. Increasing glass packaging usage for Beverages, especially for the alcoholic Ready to Drink (RTD) segment, is a current trend in the Beverage packaging industry of India. The glass packaging industry is primarily boosted by increasing alcoholic beverage consumption in the country.

- Moreover, ICRIER (Indian Council for Research on International Economic Relations) said over 70% of the growth in alcoholic beverage consumption in India in the next decade would be driven by the lower middle and upper middle-income groups, and there is a growing trend toward product premiumization.

- Soft drinks are the most significant contributor on which the business of non-alcoholic drinks rests. Glass bottles retain a 35% share of sales for Coke in India. Beverage maker Coca-Cola India Pvt. Ltd. is again promoting returnable glass bottles. The bottles rolled out last year at INR 10 (USD 0.15) price point (200 ml) in select states are available across the company's top-selling brands, such as Coca-Cola, Thums Up, and Sprite. In some markets, glass bottles now make up 30% of beverage sales (source: Coca-Cola).

- Many beverages are expected to use glass bottles, particularly those from large manufacturers that have been decorated with glass bottles. The main advantage for the user is that there is almost no dissolution from container materials when glass bottles are used as packaging containers for juice or other drinks.

India Glass Packaging Industry Overview

The India Glass Packaging Market is competitive owing to multiple players, which led the market to be moderately consolidated. Players in the market, such as Schott Kaisha Pvt Ltd., AGI glaspac., Piramal Glass Limited, Borosil Glass Works Limited, and Haldyn Glass Limited are adopting strategies like product innovation, partnerships, and mergers and acquisitions to increase their market share further. Some of the critical advancements in the market are:

- August 2022 - Soda ash producer Nirma submitted an INR 16,500 million (USD 206 million) plan to acquire one of the most prominent Hindustan National Glass Limited (HNGL). Africa-based bottle maker Madhvani Group and container glass producer AGI Greenpac have also submitted separate resolution plans for the company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Industry

- 4.5 Trade Scenario Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Environmental Awareness Among the Population

- 5.1.2 Increasing Beverage Consumption in the Country

- 5.2 Market Restraints

- 5.2.1 Alternative Packaging Options such as Aluminum and Plastic

6 MARKET SEGMENTATION

- 6.1 By Product ( Revenue in USD Billion and Volume in Million Metric Tones)

- 6.1.1 Bottles/Containers

- 6.1.2 Vials

- 6.1.3 Ampoules

- 6.1.4 Syringe/Cartridges

- 6.2 By End-user Vertical ( Revenue in USD Billion and Volume in Million Metric Tones)

- 6.2.1 Food

- 6.2.2 Beverage (Soft Drinks, Milk, Alcoholic Beverages, Other Beverage Types)

- 6.2.3 Cosmetics, Perfumery and Personal Care

- 6.2.4 Pharmaceuticals

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Schott Kaisha Pvt Ltd (SCHOTT AG)

- 7.1.2 AGI Glaspac (HSIL Ltd)

- 7.1.3 Piramal Glass Limited

- 7.1.4 Hindustan National Glass & Industries Limited (HNGIL)

- 7.1.5 Schott Poonawalla Private Limited

- 7.1.6 Gerresheimer AG

- 7.1.7 Borosil Glass Works Limited (Klasspack Pvt. Ltd.)

- 7.1.8 Haldyn Glass Limited (HGL)

- 7.1.9 Sunrise Glass Industries Private Limited

- 7.1.10 Ajanta Bottle Pvt Ltd

- 7.1.11 G.M Overseas

- 7.1.12 Empire Industries Limited- Vitrum Glass