|

市場調査レポート

商品コード

1685920

アフリカのスポーツドリンク:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Africa Sports Drinks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカのスポーツドリンク:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 208 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

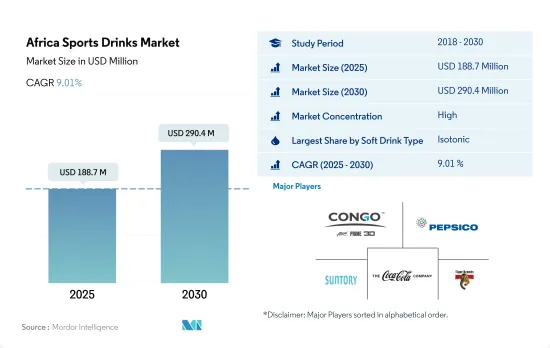

アフリカのスポーツドリンク市場規模は2025年に1億8,870万米ドルと推定され、2030年には2億9,040万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは9.01%で成長すると予測されます。

地域全体のスポーツ参加人口の増加によりアイソトニックスポーツドリンクが市場を牽引

- 同地域のスポーツドリンク市場は、陸上競技、ボディービル、ウェイトリフティング、サイクリングなどのスポーツ活動に従事する個人数の増加を主因として、堅調な成長を遂げています。例えば、南アフリカでは2022年にヘルス・フィットネス・クラブの会員数が240万人を記録しました。このようなスポーツ参加の急増は、2023年のスポーツドリンク売上高の2021年比14.66%増という顕著な成長につながりました。

- 2023年には、アイソトニック飲料が市場を席巻し、同地域で50%以上のシェアを占めました。これらの飲料は、激しい運動中の燃料補給と水分補給を目的として設計されており、人体に見られる炭水化物濃度を反映しています。この地域のスポーツ文化が強く、身体活動を重視することから、アイソトニック・スポーツドリンクはアフリカの人々に好まれる選択肢となっています。

- 同地域でスポーツ文化が引き続き盛んになるにつれ、電解質強化飲料水の需要も増加の一途をたどっています。これらの飲料は、最適な電解質バランスを維持する上で重要な役割を果たしており、特に肉体労働中や激しい運動中、あるいは電解質の損失が高まる高温多湿の条件下で重要です。特に、このセグメントは2020年と比較して2023年には13.36%の大幅な数量成長を示しています。

- プロテインベースのスポーツドリンクは、特にアスリートやフィットネス愛好家の間で人気が急上昇しています。これらの飲料は、特に運動後に摂取することで、筋肉組織の修復と再生を助けるなど、複数の利点を提供します。金額ベースでは、このセグメントは2018年から2023年にかけて7.38%という顕著なCAGRを示しました。

ブランドはソーシャル・プラットフォームで顧客と積極的に関わり、これが同地域の成長を促進すると予想される

- スポーツドリンク市場は同地域で着実に成長しています。2020年から2023年にかけて、金額ベースで26.9%の成長率を記録しました。アフリカでスポーツドリンクの需要が急増しているのは、スポーツドリンクを日常的な消費の一部と認識する若年人口が増加していることなど、複数の理由による。アフリカでは若者の数が増加しており、例えば2022年にはアフリカの総人口の49.79%が18~64歳です。ブランドはツイッター、インスタグラム、フェイスブックなどのプラットフォームで顧客と積極的に関わり、ファンのフォロワー数が多ければ多いほど、消費者の信頼を築くことができます。

- ナイジェリアは、この地域で主要な市場シェアを占めています。スポーツドリンク市場において、2020年から2023年までの成長率は金額ベースで51.2%を記録しています。スポーツや身体活動に携わる人口の増加がスポーツドリンク市場を牽引しています。若い世代の間で健康とフィットネスに対する関心が高まっていることが、市場プレイヤーを栄養価の高い製品や低カロリー製品の製造に駆り立てています。同国で人気のあるスポーツドリンクには、Lucozade、Red Bull、Power Horse、Monster Energy Drink、Fearless Energy Drinkなどがあります。

- アフリカでは、プレーヤーが新しく革新的なフレーバーを発売しており、2024年から2030年にかけて市場を牽引すると予測されています。2024年から2028年までの金額ベースのCAGRは8.90%と予測されます。Monster Energy South Africa社は、2022年にJuice Monsterシリーズに新フレーバー、Monster Mariposaを追加しました。同様に、Prime Hydrationはエナジードリンク製品に5つの新フレーバーを発売しました。具体的には、2023年4月にココナッツ、ライム、グレープフルーツ、トロピカルパンチなどのフレーバーを発売しました。

アフリカのスポーツドリンク市場動向

天然素材を使用したスポーツドリンクへの関心の高まりが市場成長を牽引

- 2022年、南アフリカ(成人人口+15歳)のスポーツドリンク消費者は850万人(25%)を超えます。また、スポーツドリンクの消費は主に、消費者の身体的健康志向の高まりと、フィットネスセンターやヘルスクラブの増加に起因しています。

- この地域の消費者は、全原材料を使用したブランドを求めており、製品の原産地に対する関心が高まっています。消費者は、スポーツドリンクに使用されているクリーンなラベルや原材料に注目しています。2022年には、アフリカ地域の消費者の52%が、買い物をする際には常にクリーンラベルを探すと主張しています。

- 健康飲料に対する需要の高まりに伴い、同地域のスポーツ飲料メーカーは売上高が急増しました。スポーツドリンクの価格変動は、原材料価格の上下と関連しています。

- 糖分摂取量の多い飲料の健康への影響から、消費者の無糖スポーツ飲料への嗜好がこの地域で人気を集めています。2022年には、南アフリカの消費者の28%が砂糖入り飲料の購入額を減らし、砂糖とカロリーの摂取量を減らしていると主張しました。南アフリカ国民の4分の1以上が肥満を抱えながら生活しており、同国は世界で最も肥満の多い国の上位20%に入っています。

アフリカのスポーツドリンク産業概要

アフリカのスポーツ飲料市場はかなり統合されており、上位5社で79.14%を占めています。この市場の主要企業は以下の通り。 Congo Brands, PepsiCo, Inc., Suntory Holdings Limited, The Coca-Cola Company and Tiger Brands Ltd.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 消費者の購買行動

- イノベーション

- ブランドシェア分析

- 規制の枠組み

第5章 市場セグメンテーション

- ソフトドリンクタイプ

- 電解質強化水

- ハイパートニック

- ハイポトニック

- アイソトニック

- プロテインベースのスポーツドリンク

- 包装タイプ

- 無菌パッケージ

- 金属缶

- ペットボトル

- サブ流通チャネル

- コンビニエンスストア

- オンラインショップ

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他

- 国名

- エジプト

- ナイジェリア

- 南アフリカ

- その他のアフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Aje Group

- BOS Brands(Pty)Ltd

- Congo Brands

- Ekhamanzi Springs(Pty)Ltd

- Kingsley Beverages Limited

- Oshee Polska Sp. Z.O.O.

- PepsiCo, Inc.

- Suntory Holdings Limited

- The Coca-Cola Company

- Thirsti Water(Pty)Ltd

- Tiger Brands Ltd.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Africa Sports Drinks Market size is estimated at 188.7 million USD in 2025, and is expected to reach 290.4 million USD by 2030, growing at a CAGR of 9.01% during the forecast period (2025-2030).

Isotonic sports drinks led the market due to the increasing sports participation population across the region

- The sports drink market in the region is witnessing robust growth, primarily driven by the rising number of individuals engaging in sports activities like athletics, bodybuilding, weightlifting, and cycling. For instance, in 2022, South Africa recorded a health and fitness club membership of 2.4 million. This surge in sports participation translated into a notable 14.66% growth in sports drink sales in 2023 compared to 2021.

- In 2023, isotonic drinks dominated the market, commanding over 50% share in the region. These drinks, designed to fuel and hydrate the body during intense workouts, mirror the carbohydrate concentrations found in the human body. With the region's strong sports culture and emphasis on physical activity, isotonic sports drinks have become a preferred choice among Africans.

- As the sports culture continues to flourish in the region, the demand for electrolyte-enhanced water is poised to rise. These drinks play a crucial role in maintaining optimal electrolyte balance, especially during physical exertion, intense workouts, or in hot and humid conditions when electrolyte loss is heightened. Notably, the segment witnessed a significant 13.36% volume growth in 2023 compared to 2020.

- Protein-based sports drinks have witnessed a surge in popularity, particularly among athletes and fitness enthusiasts. These drinks offer multiple benefits, such as aiding muscle tissue repair and regeneration, especially when consumed post-activity. In terms of value, the segment showcased a noteworthy CAGR of 7.38% from 2018 to 2023.

Brands are actively engaging with customers on social platforms, which is expected to drive growth in the region

- The sports drink market is growing steadily in the region. It registered a growth rate of 26.9% by value from 2020 to 2023. The demand for sports drinks is rising rapidly in Africa due to multiple reasons, such as the rising young population who perceive such drinks to be a part of daily consumption. The number of youths is rising in Africa; for instance, 49.79% of Africa's total population were aged between 18 and 64 years in 2022. Brands are actively engaged with their customers on platforms such as Twitter, Instagram, and Facebook, and the greater the number of fan followers, the greater it builds trust among consumers.

- Nigeria holds the major market share in the region. It has registered a growth rate of 51.2% by value from 2020 to 2023 in the sports drink market. The increased population involved in sports and physical activities is driving the sports drink market. Increasing concerns about health and fitness among the young generation are driving the market players to produce products with nutritional benefits and low-calorie products. Some of the popular sports drinks in the country are Lucozade, Red Bull, Power Horse, Monster Energy Drink, and Fearless Energy Drink.

- In Africa, players are launching new and innovative flavors, which are projected to drive the market between 2024 and 2030. It is projected to register a CAGR of 8.90% by value from 2024 to 2028. Monster Energy South Africa added a new flavor to its Juice Monster range, namely Monster Mariposa, in 2022. Similarly, Prime Hydration launched five new flavors of its Energy Drinks product. More specifically, the company launched flavors such as coconut, lime, Grapefruit, and tropical punch in April 2023.

Africa Sports Drinks Market Trends

Growing interest towards sports drinks made from natural ingredients is driving the market growth

- In 2022, there were more than 8.5 million (25%) sports drink consumers in South Africa (adult population +15 years). Also, the consumption of sports drinks can be primarily ascribed to the surge in consumer inclination toward physical well-being and an increase in the number of fitness centers and health clubs.

- Consumers in the region are seeking out brands that are made with whole ingredients with a growing interest in the origin of the product. Consumers pay attention to clean labels and ingredients used in sports drinks. In 2022, 52% of the consumers in the African region claimed that they always look for clean labels while shopping.

- With the growing demand for healthy beverages, sports drink manufacturers in the region experienced a surge in their sales. The fluctuation in the sports drinks price is connected with the rise and fall in the prices of its raw materials.

- Consumers' preference for sugar-free sports drinks is gaining popularity in the region due to the health effects of high-sugar intake drinks. In 2022, 28% of consumers in South Africa paid for fewer sugary drinks and claimed that they were reducing their sugar and calorie intake. More than a quarter of South Africans live with obesity, ranking the country among the top 20% of the most obese nations in the world.

Africa Sports Drinks Industry Overview

The Africa Sports Drinks Market is fairly consolidated, with the top five companies occupying 79.14%. The major players in this market are Congo Brands, PepsiCo, Inc., Suntory Holdings Limited, The Coca-Cola Company and Tiger Brands Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumer Buying Behaviour

- 4.2 Innovations

- 4.3 Brand Share Analysis

- 4.4 Regulatory Framework

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Soft Drink Type

- 5.1.1 Electrolyte-Enhanced Water

- 5.1.2 Hypertonic

- 5.1.3 Hypotonic

- 5.1.4 Isotonic

- 5.1.5 Protein-based Sport Drinks

- 5.2 Packaging Type

- 5.2.1 Aseptic packages

- 5.2.2 Metal Can

- 5.2.3 PET Bottles

- 5.3 Sub Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Retail

- 5.3.3 Specialty Stores

- 5.3.4 Supermarket/Hypermarket

- 5.3.5 Others

- 5.4 Country

- 5.4.1 Egypt

- 5.4.2 Nigeria

- 5.4.3 South Africa

- 5.4.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Aje Group

- 6.4.2 BOS Brands (Pty) Ltd

- 6.4.3 Congo Brands

- 6.4.4 Ekhamanzi Springs (Pty) Ltd

- 6.4.5 Kingsley Beverages Limited

- 6.4.6 Oshee Polska Sp. Z.O.O.

- 6.4.7 PepsiCo, Inc.

- 6.4.8 Suntory Holdings Limited

- 6.4.9 The Coca-Cola Company

- 6.4.10 Thirsti Water (Pty) Ltd

- 6.4.11 Tiger Brands Ltd.

7 KEY STRATEGIC QUESTIONS FOR SOFT DRINK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms