|

市場調査レポート

商品コード

1685890

アフリカのバイオスティミュラント:市場シェア分析、産業動向、成長予測(2025年~2030年)Africa Biostimulants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカのバイオスティミュラント:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 153 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

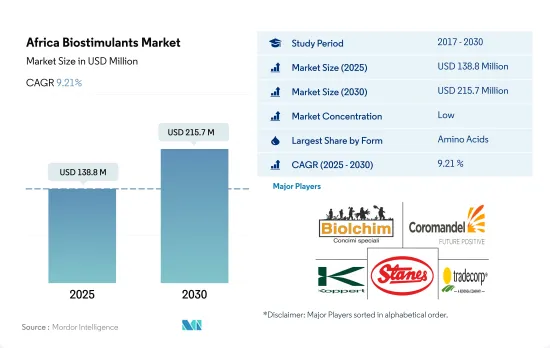

アフリカのバイオスティミュラント市場規模は2025年に1億3,880万米ドルと推定され、2030年には2億1,570万米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは9.21%で成長すると予測されます。

- アミノ酸ベースのバイオスティミュラントはアフリカ市場を独占し、2022年には3,530万米ドルと評価されます。アミノ酸ベースのバイオスティミュラントは、種子の発芽と苗の成長を促進し、様々な生物学的および生物学的ストレスに対する作物の回復力を向上させ、特に窒素とリンに関して栄養分の取り込みと利用を促進し、農薬や肥料などの他の農業投入物の効率を増幅する能力があるため、広く使用されています。

- フミン酸ベースのバイオスティミュラントは、ストレス耐性の向上、養分取り込み量の増加、化学投入の全体的な削減といった利点があり、さらに灌漑や土壌散布による施用が容易であることから、市場を牽引する可能性があり、市場価値は2029年までに約78.5%増の4,960万米ドルに成長すると予想されます。

- 腐植酸ベースのバイオスティミュラントは、土壌、泥炭、石炭、その他の化石鉱床に含まれる腐植物質に由来する有機土壌改良剤の一種であり、土壌の健康と植物の成長を促進することが知られています。腐植酸を豊富に含んでいます。これらのバイオスティミュラントは、2022年のアフリカのバイオスティミュラント市場の金額ベースで23.4%を占め、第2位の市場シェアを占めています。

- 海藻エキスベースのバイオスティミュラントは、多くの沿岸地域で豊富に入手可能であり、農業における化学肥料の必要性を減少させる能力があるため、アフリカ地域での市場シェアを向上させる可能性があります。これらの要因は、予測期間中に海藻ベースのバイオスティミュラントの需要を促進する可能性があります。海藻エキスベースのバイオスティミュラントは、2022年に約2,310万米ドルを占めました。

- フミン酸およびフルボ酸ベースのバイオスティミュラントは、2023年から2029年の間に他のバイオスティミュラントよりも急速に成長すると予測されています。

- アフリカは多様な農業システムで知られ、地域全体でさまざまな作物が栽培されています。農業はアフリカ経済において重要な役割を担っており、有機農業は2021年には約12万ヘクタールの有機作物栽培面積を持つまでに成長しました。トウモロコシ、小麦、とうもろこしなどの穀類は、この地域で最も広く栽培されている作物のひとつです。

- アフリカ農業の成長分野のひとつにバイオスティミュラント市場があり、2017年から2021年にかけて約18.7%上昇し、金額が大幅に増加しました。この成長は今後も続き、市場額は67.8%増加すると予測されています。

- アフリカのバイオスティミュラント市場の大部分はアフリカのその他の地域が占めており、2022年の市場金額の約81.1%を占める。チュニジアは面積でトップの有機生産国であり、エチオピアは2020年の有機生産者数が約22万人と最も多いです。しかし、ほとんどのアフリカ諸国では有機農業に関する法律が整備されていないため、一部の地域では確立されたバイオスティミュラント市場の確立が妨げられています。

- 海藻ベースのバイオスティミュラントは市場金額の43.8%を占め、2022年には約340万米ドルとなります。ナイジェリアでは海藻エキスベースのバイオスティミュラントの使用が普及しています。

- アフリカにおけるバイオスティミュラントの需要は、国内外の有機製品に対する消費者の関心の高まりによって、今後数年間で増加すると予想されます。農家は、化学投入物に過度に依存することの欠点や、バイオスティミュラントを使用することの経済的利点について、より多くの情報を得るようになっています。このような要因から、アフリカのバイオスティミュラント市場は大きく成長し、同地域の農家と企業の双方に機会を提供する態勢が整っています。

アフリカのバイオスティミュラント市場動向

この地域の有機セクターには8,34,000の有機生産者がおり、チュニジアの方が有機農地が多いです。

- 2022年、アフリカ地域の有機農地面積は120万ヘクタールを超え、世界の有機農地面積の9.0%を占めました。

- 2020年、アフリカは2019年より149,000ヘクタール多い有機栽培地を報告し、約834,000人の生産者の存在に伴い、前年比7.7%増を記録しました。チュニジアの有機栽培地が最も多く(2020年には29万ヘクタール以上)、エチオピアの有機生産者数が最も多かった(約22万人)。サントメ・プリンシペの島国は、この地域で有機農業に最も多くの土地を投入しており、農地面積の20.7%が有機作物です。

- アフリカ地域では、換金作物が有機農地に占める割合が大きく、有機農地面積の63.2%を占める81万7,400ヘクタールとなっています。畑作物はアフリカの有機農地で2番目に大きなシェアを占めており、有機農地全体の約25.6%、合計33万1,200ヘクタールにのぼる。園芸作物はアフリカの有機農地総面積の11.2%を占め、2022年には14万4,900ヘクタールとなります。

- 有機農地面積が大きいアフリカ諸国には、その他のアフリカ地域セグメント、エジプト、南アフリカが含まれます。2022年には、アフリカ残りの地域セグメントが120万ヘクタールでアフリカの有機農業総面積の95.0%を占め、エジプトが4万5,100ヘクタールで3.5%、南アフリカが1万2,600ヘクタールで1.0%のシェアを占める。

- アフリカでは2017年から2022年の間に有機農業の作付面積が6.9%増加しました。2029年には約52.2%増加し、200万米ドルに達すると予想されます。

一人当たりのオーガニック製品への支出はエジプト、南アフリカ、ナイジェリア諸国が優勢

- アフリカの1人当たり所得は長年にわたって一貫して増加しており、人々は栄養価の高い食品により多くの支出をするようになっています。アフリカ地域では、有機食品と飲食品がより多くの棚に並ぶようになっています。オーガニック認証を受けた農産物の国内消費量は比較的少ないため、オーガニック製品のほとんどは輸出用に生産されています。

- アフリカでは、特にエジプト、南アフリカ、ナイジェリアで有機製品の消費が大幅に増加しています。2021年の有機製品の1人当たり消費額は、エジプトが55.5米ドル、次いで南アフリカが7.1米ドルでした。オーガニック生産者数が最も多い国は、エチオピア(ほぼ222,000人)、タンザニア(ほぼ149,000人)、ウガンダ(139,000人以上)でした。

- アフリカ地域で一般的に消費されている有機製品には、新鮮な野菜や果物が含まれます。アフリカでは、有機農業を政策、国の改良普及システム、マーケティング、バリューチェーン開拓の主流に据えるための多大な努力がなされてきました。これらすべての要因が消費者の関心を集めています。

- フルーツ・ジュースを中心とする飲料の1人当たり消費量の増加、健康意識の高まり、化学成分を含まない有機飲料・食品への消費者のシフトに伴い、アフリカの有機食品市場の需要は2023年から2029年にかけて拡大すると予想されます。

- しかし、低所得層が多く、有機基準や現地市場認証のためのその他のインフラが整っていないことが、同地域の有機市場成長の主な阻害要因となっています。

アフリカのバイオスティミュラント産業の概要

アフリカのバイオスティミュラント市場は断片化されており、上位5社で18.64%を占めています。この市場の主要企業は以下の通りです。 Biolchim SPA, Coromandel International Ltd, Koppert Biological Systems Inc., T. Stanes and Company Limited and Trade Corporation International(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 有機栽培面積

- 一人当たりのオーガニック製品への支出

- 規制の枠組み

- エジプト

- ナイジェリア

- 南アフリカ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 形態

- アミノ酸

- フルボ酸

- フミン酸

- タンパク質加水分解物

- 海藻エキス

- その他のバイオスティミュラント

- 作物タイプ

- 換金作物

- 園芸作物

- 畑作物

- 生産国

- エジプト

- ナイジェリア

- 南アフリカ

- その他のアフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Atlantica Agricola

- Biolchim SPA

- Coromandel International Ltd

- Haifa Group

- Humic Growth Solutions Inc.

- Koppert Biological Systems Inc.

- Microbial Biological Fertilizers International

- T. Stanes and Company Limited

- Trade Corporation International

- UPL

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Africa Biostimulants Market size is estimated at 138.8 million USD in 2025, and is expected to reach 215.7 million USD by 2030, growing at a CAGR of 9.21% during the forecast period (2025-2030).

- Amino acid-based biostimulants dominate the African market, valued at USD 35.3 million in 2022. Amino acid-based biostimulants are widely used because of their ability to enhance seed germination and seedling growth, improve crop resilience to various biotic and abiotic stresses, boost nutrient uptake and utilization, especially with regard to nitrogen and phosphorus, and amplify the efficiency of other agricultural inputs such as pesticides and fertilizers.

- The benefits of humic acid-based biostimulants, such as increased stress tolerance, increased nutrient uptake, and an overall reduction in chemical inputs, as well as their ease of application via fertigation or soil application methods, may drive the market, with the market value expected to grow by about 78.5% to USD 49.6 million by 2029.

- Humic acid-based biostimulants, which are a type of organic soil amendment derived from humic substances found in soil, peat, coal, and other fossil deposits, are known to enhance soil health and plant growth. They are rich in humic acids. These biostimulants account for the second-largest market share, representing 23.4% of the African biostimulant market by value in 2022.

- Seaweed extract-based biostimulants can potentially improve their market share in the African region due to their abundant availability in many coastal areas and their ability to decrease the need for chemical fertilizers in agriculture. These factors may drive the demand for seaweed-based biostimulants during the forecast period. Seaweed extract-based biostimulants accounted for about USD 23.1 million in 2022.

- Humic and fulvic acid-based biostimulants are anticipated to grow faster than other biostimulants between 2023 and 2029.

- Africa is known for its diverse agricultural systems, with a wide range of crops grown across the region. Agriculture plays a vital role in the African economy, and organic farming gained traction, with approximately 120 thousand hectares of organic crop area in 2021. Cereal crops, such as maize, wheat, and corn, are among the most widely grown crops in the region.

- One area of growth in African agriculture is the biostimulants market, which saw a significant increase in value, rising by approximately 18.7% from 2017 to 2021. This growth is expected to continue, with the market value projected to increase by 67.8%.

- The majority of the African biostimulants market is dominated by the Rest of African region, accounting for about 81.1% of the market value in 2022. Tunisia is the top organic producer in terms of area, and Ethiopia has the highest number of organic producers, with approximately 220,000 in 2020. However, the lack of legislation for organic farming in most African countries has hampered the establishment of a well-established biostimulant market in some areas.

- Seaweed-based biostimulants make up 43.8% of the market value, valued at about USD 3.4 million in 2022. The use of seaweed extract-based biostimulants is prevalent in Nigeria.

- The demand for biostimulants in Africa is expected to rise in the coming years, driven by increasing consumer interest in organic products, both domestically and internationally. Farmers are becoming more informed about the drawbacks of heavy reliance on chemical inputs and the economic benefits of using biostimulants. With these factors in play, the biostimulants market in Africa is poised for significant growth, providing opportunities for both farmers and businesses in the region.

Africa Biostimulants Market Trends

8,34,000 organic producers are in the region's organic sector with Tunisia is having more organic land

- In 2022, the area of organic agricultural land in the African region amounted to over 1.2 million hectares, representing 9.0% of the global organic agricultural area.

- In 2020, Africa reported 149,000 hectares more in organic cultivation land than in 2019, recording a 7.7% increase Y-o-Y in line with the presence of nearly 834,000 producers. Tunisia had the largest amount of organic land (more than 290,000 hectares in 2020), whereas Ethiopia had the highest number of organic producers (almost 220,000). The island states of Sao Tome and Principe have the most significant amount of land committed to organic farming in the region, with 20.7% of their agricultural area dedicated to organic crops.

- In the African region, cash crops account for a significant share of organic agricultural land, amounting to 63.2% of the total organic acreage with 817.4 thousand hectares. Row crops hold the second-largest share of organic acreage in Africa, which amounts to about 25.6% of the total organic acreage, totaling 331.2 thousand hectares. Horticultural crops account for 11.2% of the total organic acreage in Africa, with 144.9 thousand hectares in 2022.

- The African countries with significant organic agricultural acreage include the Rest of Africa regional segment, Egypt, and South Africa. In 2022, the Rest of Africa segment accounted for 95.0% of the total organic agricultural acreage in Africa, with 1.2 million hectares, Egypt accounted for a 3.5% share with 45.1 thousand hectares, and South Africa accounted for a 1.0% share with 12.6 thousand hectares.

- Organic agricultural acreage rose by 6.9% between 2017 and 2022 in Africa. It is anticipated to increase by about 52.2% and reach USD 2.0 million by 2029.

Per capita spending on organic product predominant in Egypt, South Africa, and Nigeria countries

- Africa's per capita income has consistently increased throughout the years, encouraging people to spend more money on nutritious food. Organic foods and beverages are gaining more shelf space in the African region. Since the domestic consumption of certified organic produce is relatively small, most organic goods are produced for export.

- In Africa, consumption of organic products has increased significantly, especially in Egypt, South Africa, and Nigeria. In 2021, the per capita consumption of organic products was USD 55.5 in Egypt, followed by South Africa with USD 7.1. The countries with the highest number of organic producers were Ethiopia (almost 222,000), Tanzania (nearly 149,000), and Uganda (over 139,000).

- In the African region, commonly consumed organic products include fresh vegetables and fruits. In Africa, significant efforts have been made to mainstream organic agriculture into policy, national extension systems, marketing, and value chain development. All these factors have gained the attention of consumers.

- With the increasing per capita consumption of beverages, primarily fruit juices, growing health awareness, and consumers shifting toward organic drinks and food that do not contain chemical ingredients, the demand for the African organic food market is expected to grow between 2023 and 2029.

- However, low-income levels and a lack of organic standards and other infrastructure for local market certification are the major restraining factors for the growth of the organic market in the region.

Africa Biostimulants Industry Overview

The Africa Biostimulants Market is fragmented, with the top five companies occupying 18.64%. The major players in this market are Biolchim SPA, Coromandel International Ltd, Koppert Biological Systems Inc., T. Stanes and Company Limited and Trade Corporation International (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Egypt

- 4.3.2 Nigeria

- 4.3.3 South Africa

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Amino Acids

- 5.1.2 Fulvic Acid

- 5.1.3 Humic Acid

- 5.1.4 Protein Hydrolysates

- 5.1.5 Seaweed Extracts

- 5.1.6 Other Biostimulants

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 Egypt

- 5.3.2 Nigeria

- 5.3.3 South Africa

- 5.3.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Atlantica Agricola

- 6.4.2 Biolchim SPA

- 6.4.3 Coromandel International Ltd

- 6.4.4 Haifa Group

- 6.4.5 Humic Growth Solutions Inc.

- 6.4.6 Koppert Biological Systems Inc.

- 6.4.7 Microbial Biological Fertilizers International

- 6.4.8 T. Stanes and Company Limited

- 6.4.9 Trade Corporation International

- 6.4.10 UPL

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms