|

市場調査レポート

商品コード

1685797

アジア太平洋のバイオスティミュラント:市場シェア分析、産業動向、成長予測(2025年~2030年)Asia-Pacific Biostimulants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋のバイオスティミュラント:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 178 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

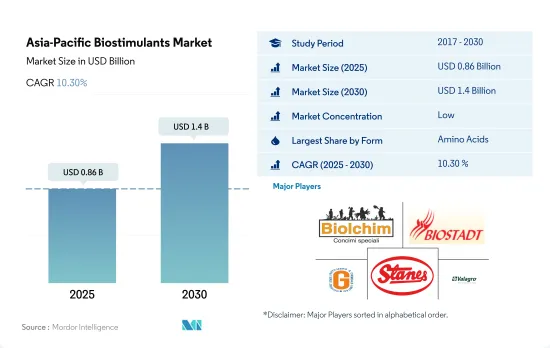

アジア太平洋のバイオスティミュラント市場規模は、2025年には8億6,000万米ドルと推定され、2030年には14億米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは10.30%で成長する見込みです。

- 現代農業は、人類の最も困難な課題の解決に中心的な役割を果たしています。アジア太平洋の人口が増加するにつれ、農業部門は食糧需要の増加に対応し、食糧安全保障の目標を達成する必要に迫られています。

- 土壌の質の悪化は、この地域の農家や農業従事者の間で大きな懸念となっています。その結果、肥沃度、生物多様性、生産能力が失われています。農業部門の最も大きな課題は、農業生産を高めるために合成肥料や農薬の使用が増加していることです。研究によれば、肥料の過剰使用は気候危機を早める可能性があります。

- その結果、革新的な解決策を用いた環境に優しく持続可能な農法が、現代農業の標準的な慣行となっています。十分な食糧生産を確保するためには、農業部門は資源の利用効率を向上させる新しい解決策やアプローチを取り入れなければならないです。この点で、バイオスティミュラントは、環境にやさしく、現代農業にとって有望な技術革新として浮上してきました。アミノ酸、フミン酸、フルボ酸、海藻エキス、タンパク質加水分解物などが、最も一般的に使用されているバイオ刺激剤のひとつです。

- アミノ酸は、アジア太平洋で最も一般的に使用されている生物刺激剤であり、2022年の市場シェアは25.2%で最大です。これは、特に生物的・生物学的ストレス条件下で植物の生産性を高める能力があるためです。

- インドや中国といったこの地域の主要農業国は、有機農業と持続可能な農業投入物の使用を促進するためにさまざまな取り組みを開始しています。これらの国は、市場を牽引する様々なインセンティブを提供しており、その結果、市場価値は2023年から2029年の間に11.9%のCAGRで推移すると予想されています。

- アジア太平洋では、有機栽培食品に対する需要が顕著に増加しており、その結果バイオスティミュラント市場が急成長しています。インド、中国、オーストラリア、日本などの国々が有機農業を推進しているため、有機栽培面積は2017年の310万ヘクタールから2022年には380万ヘクタールに増加しました。その結果、バイオスティミュラント市場は2017年から2022年の間に11.5%の成長率を経験しました。

- 気候変動の影響は作物生産に深刻な影響を及ぼしており、干ばつ、塩分、温度変化のような気候によるストレスを緩和するためにバイオスティミュラントを使用することが必須となっています。バイオスティミュラントの使用は、植物に良い影響を与えることが証明されており、農業生態系の生態学的バランスを維持し、農薬や化学肥料の必要性を減らすのに役立っています。

- アジア太平洋では、中国、インド、オーストラリアがバイオスティミュラントの主要な事業地域として浮上しています。2022年には、中国が27.6%のシェアでバイオスティミュラント市場を独占し、インドとオーストラリアがそれに続いた。これらの国々の政府は、インセンティブを提供し、研究開発に投資し、目標を設定することによって、農家が持続可能な農法を採用することを奨励しています。例えば日本は、2050年までに化学肥料と農薬の使用量をそれぞれ30.0%と50.0%削減するという目標を掲げています。

- アジア太平洋におけるバイオスティミュラントの需要は、有機農業の栽培面積の増加や持続可能な農業の必要性から増加傾向にあります。アジア太平洋のバイオスティミュラント市場は、気候変動が農業に及ぼす悪影響に対抗する一助となる可能性を秘めており、今後数年間でさらなる成長が見込まれています。

アジア太平洋のバイオスティミュラント市場動向

中国、インド、インドネシア、オーストラリアなどの国々における政府支援の拡大が、同地域の有機農業を後押し

- FiBLの統計によると、2021年にアジア太平洋の有機農地面積は370万ヘクタールを超え、世界の有機農地面積の26.4%を占めました。有機栽培面積は2017年から2022年にかけて19.3%増加しました。2020年時点で、この地域の有機生産者は約183万人で、インドが130万人でトップです。中国、インド、インドネシア、オーストラリアは、この地域で有機栽培面積が大きい主要国です。中国やインドなどの政府当局は、作物栽培における化学投入物への依存を減らすため、有機農業を継続的に推進しています。例えばインドは、Paramparagat Krishi Vikas YojanaやAll India Network Programme on Organic Farming(AI-NPOF)のような制度を実施しています。

- 2021年には、中国が250万ヘクタールで66.1%と最大のシェアを占め、インド、インドネシア、オーストラリアがそれぞれ19.3%、1.5%、1.4%のシェアで続いた。有機農地は、連作作物、園芸作物、換金作物の3種類に分けられます。連作作物はこの地域の有機農地の67.5%を占め、2021年には250万ヘクタールとなります。この地域で栽培されている主な連作作物には、水稲、小麦、豆類、大豆、雑穀が含まれます。

- 換金作物のシェアは第2位で、2021年には70万ヘクタールとなり、有機農地の18.5%を占める。砂糖や有機茶などの有機換金作物に対する需要は世界的に増加しています。中国とインドは、それぞれ有機緑茶と有機紅茶の世界最大の生産国です。国際的な需要の高まりにより、この地域の有機栽培面積は増加すると予想されます。

オーガニック製品への1人当たり支出はオーストラリアが優勢で、中国のオーガニック食品市場が大きく成長

- アジア太平洋の有機製品に対する1人当たり支出は、2021年には85.1米ドルを記録しました。オーストラリアは、2021年には58.3米ドルと、オーガニック製品に対する1人当たり支出がより高いことを目の当たりにしたが、これは、オーガニック食品は健康によいという消費者の認識による需要の高まりに起因しています。Global Organics Tradeによると、オーストラリアのオーガニック包装食品・飲食品市場は2021年に8億8,520万米ドルとなりました。

- 中国の有機食品市場は2021年に13.3%成長し、このプラス成長パターンは2023年から2029年にかけて推定CAGR 7.1%で継続すると予想されます。若い世代の間でオーガニック製品の重要性がますます強調され、働く母親の増加や健康とウェルネスの動向の採用増加によりオーガニック・ベビーフードの需要が増加していることから、オーガニック製品は2025年までに64億米ドルの規模に達すると予想されます。

- インドのオーガニック製品は世界需要の1.0%に遠く及ばず、2021年の1人当たり支出額はわずか0.08米ドルです。しかし、インドは今後数年間で有望な市場となり、2025年には1億5,330万米ドルに達します。現在、同地域のオーガニック商品市場は非常に断片的で、一部のスーパーマーケットや専門店でしか販売されていないです。消費者の知識と購買意欲の高まりは、同地域における有機食品の持続可能性の特質に対する理解を深めることにつながります。国民1人当たりの所得の増加は、有機食品摂取の重要性に対する消費者の意識の高まりとともに、アジア太平洋の有機食品に対する国民1人当たりの支出を増加させる可能性を秘めています。

アジア太平洋のバイオスティミュラント産業の概要

アジア太平洋のバイオスティミュラント市場は断片化されており、上位5社で8.79%を占めています。この市場の主要企業は以下の通り。 Biolchim SpA, Biostadt India Limited, Gujarat State Fertilizers & Chemicals Ltd., T. Stanes and Company Limited and Valagro(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 有機栽培面積

- 一人当たりのオーガニック製品への支出

- 規制の枠組み

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- フィリピン

- タイ

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 形態

- アミノ酸

- フルボ酸

- フミン酸

- タンパク質加水分解物

- 海藻エキス

- その他のバイオスティミュラント

- 作物タイプ

- 換金作物

- 園芸作物

- 畑作物

- 生産国

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- フィリピン

- タイ

- ベトナム

- その他のアジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Agrinos

- Atlantica Agricola

- Biolchim SpA

- Biostadt India Limited

- Coromandel International Ltd

- Gujarat State Fertilizers & Chemicals Ltd.

- Plant Response Biotech Inc.

- Rallis India Ltd

- T. Stanes and Company Limited

- Valagro

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Asia-Pacific Biostimulants Market size is estimated at 0.86 billion USD in 2025, and is expected to reach 1.4 billion USD by 2030, growing at a CAGR of 10.30% during the forecast period (2025-2030).

- Modern agriculture plays a central role in solving some of humanity's most challenging problems. As the population in the Asia-Pacific region grows, the agricultural sector is under pressure to meet the rising demand for food and achieve food security goals.

- The deterioration of soil quality has become a major concern among farmers and agriculturists in the region. This has resulted in a loss of fertility, biodiversity, and production capacity. The agriculture sector's most significant challenge is the increasing use of synthetic fertilizers and pesticides to boost agricultural production. According to studies, excessive fertilizer use could hasten the climate crisis.

- As a result, environmentally friendly and sustainable farming practices with innovative solutions are now standard practices in modern agriculture. To ensure adequate food production, the agricultural sector must embrace new solutions and approaches to improve resource utilization efficiency. Biostimulants have emerged as an environmentally friendly and promising innovation for modern agriculture in this regard. Amino acids, humic acid, fulvic acid, seaweed extract, and protein hydrolysates are among the most commonly used biostimulants.

- Amino acids are the most commonly used biostimulants in the Asia-Pacific region, with the largest market share of 25.2% in 2022. This is due to their ability to enhance plant productivity, especially under abiotic and biotic stress conditions.

- Major agricultural countries in the region, such as India and China, have launched various initiatives to promote organic farming and the use of sustainable agricultural inputs. They offer various incentives that may drive the market, and as a result, the market value is anticipated to record a CAGR of 11.9% between 2023 and 2029.

- The Asia-Pacific region has witnessed a remarkable increase in the demand for organically grown food, resulting in a surge in the biostimulants market. With countries like India, China, Australia, and Japan promoting organic farming, the area under organic cultivation increased from 3.1 million hectares in 2017 to 3.8 million hectares in 2022. As a result, the biostimulants market experienced a growth rate of 11.5% between 2017-2022.

- The impact of climate change has severely affected crop production, making it imperative to use biostimulants to mitigate climate-induced stresses like drought, salinity, and temperature variations. The application of biostimulants has proven to have a positive impact on plants and helps maintain the ecological balance of agroecosystems, reducing the need for pesticides and chemical fertilizers.

- China, India, and Australia have emerged as the major business areas for biostimulants in the Asia-Pacific region. In 2022, China dominated the biostimulants market with a 27.6% share, followed by India and Australia. The governments of these countries are encouraging farmers to adopt sustainable agricultural practices by providing incentives, investing in research and development, and setting targets to meet. For instance, Japan has set a goal to reduce the usage of chemical fertilizers and pesticides by 30.0% and 50.0%, respectively, by 2050.

- The demand for biostimulants in the Asia-Pacific region is on the rise due to the increasing area under organic farming and the need for sustainable agricultural practices. The biostimulants market in the Asia-Pacific region is expected to witness further growth in the coming years, with the potential to help combat the adverse effects of climate change on agriculture.

Asia-Pacific Biostimulants Market Trends

Growing government support in countries like China, India, Indonesia, and Australia, boosts organic farming in the region

- In 2021, the area of organic agricultural land in the Asia-Pacific region exceeded 3.7 million hectares, representing 26.4% of the global organic area, according to FiBL statistics. The organic area under cultivation grew by 19.3% between 2017 and 2022. As of 2020, the region had about 1.83 million organic producers, with India leading the way with 1.3 million organic producers. China, India, Indonesia, and Australia are the major countries with large organic cultivation areas in the region. Government authorities in countries such as China and India are continuously promoting organic agriculture to reduce reliance on chemical inputs for crop cultivation. India, for instance, has implemented schemes like Paramparagat Krishi Vikas Yojana and the All India Network Programme on Organic Farming (AI-NPOF).

- In 2021, China accounted for the largest share at 66.1% with 2.5 million hectares, followed by India, Indonesia, and Australia with shares of 19.3%, 1.5%, and 1.4%, respectively. The total organic land is divided into three crop types: row crops, horticultural crops, and cash crops. Row crops occupy the largest share of organic agricultural land in the region, accounting for 67.5% with 2.5 million hectares in 2021. Major row crops grown in the region include paddy, wheat, pulses, soybeans, and millets.

- Cash crops held the second largest share, with 0.7 million hectares in 2021, accounting for an 18.5% share of organic cropland. The demand for organic cash crops, such as sugar and organic tea, is increasing globally. China and India are the largest producers of organic green tea and organic black tea, respectively, globally. The growing international demand is expected to increase the organic acreages in the region.

Per capita spending on organic product predominant in Australia and China's organic food market growing significantly

- The per capita spending on organic products in the Asia-Pacific region was recorded at USD 85.1 in 2021. Australia witnessed a higher per capita spending on organic products, with USD 58.3 in 2021, which was attributed to the higher demand due to consumers' perception of organic food as healthy. According to Global Organics Trade, the organic packed food and beverage market in Australia stood at USD 885.2 million in 2021.

- China's organic food market grew by 13.3% in 2021, and the positive growth pattern is expected to continue with an estimated CAGR of 7.1% between 2023 and 2029. With an increasing emphasis on the importance of organic products among the younger generation and a rise in demand for organic baby food due to the growing number of working mothers and the increasing adoption of the health and wellness trend, organic products are expected to reach a value of USD 6.4 billion by 2025.

- Organic products in India represent far less than 1.0% of global demand, with a per capita expenditure of just USD 0.08 in 2021. However, India represents a promising market over the coming years, reaching a value of USD 153.3 million by 2025. Currently, the market for organic goods in the region is very fragmented, with just a few supermarkets and specialty stores selling them, as only people from higher-income families are potential customers. Growing consumer knowledge and buying motivations will lead to a better understanding of the sustainability qualities of organic food in the region. Increasing per capita income, along with increased consumer awareness of the importance of organic food intake, has the potential to raise per capita expenditure on organic food items in the Asia-Pacific region.

Asia-Pacific Biostimulants Industry Overview

The Asia-Pacific Biostimulants Market is fragmented, with the top five companies occupying 8.79%. The major players in this market are Biolchim SpA, Biostadt India Limited, Gujarat State Fertilizers & Chemicals Ltd., T. Stanes and Company Limited and Valagro (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Philippines

- 4.3.7 Thailand

- 4.3.8 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Amino Acids

- 5.1.2 Fulvic Acid

- 5.1.3 Humic Acid

- 5.1.4 Protein Hydrolysates

- 5.1.5 Seaweed Extracts

- 5.1.6 Other Biostimulants

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Philippines

- 5.3.7 Thailand

- 5.3.8 Vietnam

- 5.3.9 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Agrinos

- 6.4.2 Atlantica Agricola

- 6.4.3 Biolchim SpA

- 6.4.4 Biostadt India Limited

- 6.4.5 Coromandel International Ltd

- 6.4.6 Gujarat State Fertilizers & Chemicals Ltd.

- 6.4.7 Plant Response Biotech Inc.

- 6.4.8 Rallis India Ltd

- 6.4.9 T. Stanes and Company Limited

- 6.4.10 Valagro

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms