|

市場調査レポート

商品コード

1684089

欧州のジュース:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Juices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のジュース:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 254 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

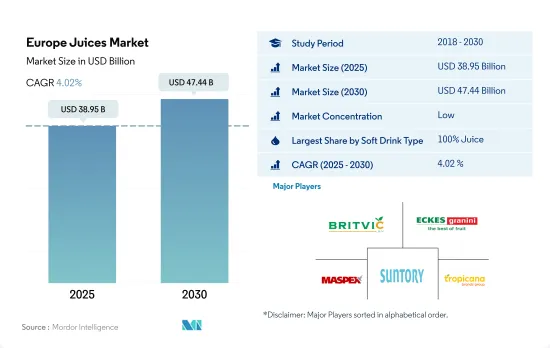

欧州のジュース市場規模は2025年に389億5,000万米ドルと推定され、2030年には474億4,000万米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは4.02%で成長する見込みです。

同地域の消費者による砂糖摂取量の減少が100%ジュース分野の成長を牽引

- 2023年には、100%ジュース分野が市場を独占し、最大の市場シェアを獲得しました。2022年には、成人の約50%~55%が砂糖の摂取量を積極的に減らそうとしており、この成分に対する懸念が広がっていることが浮き彫りになりました。英国では、砂糖の削減を目指す女性の53%、男性の45%が、砂糖の含有量が低減またはゼロの食品と飲料を好んでいた。より健康的なものを選ぼうとするこの動向は、夜の飲酒シーンにも及んでおり、低糖質で甘くないフレーバーが重視されるようになっています。

- この地域ではジュースの需要が急増し、輸入もそれに追随しました。2022年には、オランダ、フランス、ドイツ、英国、ベルギーが上位輸入国に浮上し、合計で欧州の輸入の80%を占めるようになりました。欧州で最も生産されているジュースはオレンジジュースで、市場の24%を占める。その他の主要ジュースには、ミックスジュース(21%)、アップルジュース(15%)、グレープジュース(8%)などがあります。フルーツピューレや濃縮フルーツピューレは、特定のジュース(イチゴ、モモ、アプリコットなど)の製造に使用されます。例えば、果汁を除去せずに、皮をむいた果実の可食部をふるい分け、粉砕、製粉することによって得られます。

- 果汁含有率が24%までのジュース飲料が人気を集めており、2024~2030年のCAGRは4.15%と予測されます。企業は、健康志向の消費者の嗜好に応えるため、ジュース飲料のラインナップをますます増やしています。英国では、2021年には16~24歳の半数以上が毎日ジュース飲料を消費しています。英国では、特に若年層でオレンジジュースが最も好まれるジュースとして君臨しています。2022年、同国における1人当たりのフルーツジュース消費量は約16.1リットルでした。

気候の影響と多忙なライフスタイルの増加が同地域での各種ジュースの消費を促進

- 欧州では、消費者の自然志向の高まりを背景に、チルド・オーガニック・ジュースの需要が急増しています。気候、プレミアム化、ライフスタイルの進化といった要因に影響され、消費者はますます情報を得るようになり、製品の品質を見分けられるようになっています。ペースの速いライフスタイルの増加は、「外出先で」ジュースを消費する機会をもたらします。健康志向で倫理観の高い消費者は100%ジュース形式のフルーツジュースに引き寄せられ、2023年の金額シェアは62.56%を占めました。

- 欧州諸国の中では、ドイツが2023年のジュース消費額でトップでした。同国の飲料文化に加え、ジュース加工施設の数が増加していることがジュース需要を促進しています。しかし、消費量ではオランダがリードしており、調査期間中もリードを維持すると予想されます。味覚の嗜好と健康上の利点がオランダのジュース消費を牽引しています。例えば2022年には、オランダの消費者の大多数(80%)がフルーツジュースを消費する主な理由として味を挙げており、その他の33%は健康上のメリットを挙げています。

- トルコは急成長市場として際立っており、2024年から2030年までのCAGRは金額ベースで6.46%を記録すると予測されています。この成長の一因は、学校でのネクター販売を禁止する規制にあります。この政策転換により、多くのネクターメーカーがフルーツジュース製造に軸足を移し、学校施設での継続的なプレゼンスを確保しています。

欧州のジュース市場動向

ジュースは他の清涼飲料よりも健康的であると認識されており、これが同分野の売上を牽引しています。

- 欧州、特に英国では、2022年には16~24歳の半数以上が1日1回以上ジュース飲料を飲んでいます。英国ではオレンジジュースが最も人気があり、若年層で消費頻度が高いです。

- 消費者の多くは、ビタミン、ミネラル、抗酸化物質を多く含み、糖分やカロリーの低いジュースを求めており、人工甘味料や加糖を含むジュースを避けています。

- ジュース部門の売上は、同国の健康とウェルネスの動向に関連しています。革新的なフレーバーに対する消費者の嗜好の変化に加え、市場における他のフレーバーの浸透により、欧州のオレンジジュースの需要は減少する可能性があります。

- 成人の約57%は砂糖の摂取を制限/削減するために積極的に取り組んでおり、これはこの成分に対する懸念が広がっていることを反映しています。

欧州のジュース産業の概要

欧州のジュース市場は断片化されており、上位5社で8.58%を占めています。この市場の主要企業は以下の通り。 Britvic PLC, Eckes-Granini Group GmbH, Maspex Wadowice Grupa, Suntory Holdings Limited and Tropicana Brands Group(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 消費者の購買行動

- イノベーション

- ブランドシェア分析

- 規制の枠組み

第5章 市場セグメンテーション

- 清涼飲料タイプ

- 100%ジュース

- ジュース飲料(果汁24%以下)

- 濃縮ジュース

- ネクター(果汁25~99%)

- 包装タイプ

- 無菌パッケージ

- 使い捨てカップ

- ガラス瓶

- 金属缶

- ペットボトル

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン小売

- スーパーマーケット/ハイパーマーケット

- その他

- オン・トレード

- オフトレード

- 国名

- ベルギー

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Britvic PLC

- Brynwood Partners

- Conserve Italia-Consorzio Italiano Fra Cooperative Agricole Soc Coop Agricola

- Eckes-Granini Group GmbH

- Keurig Dr Pepper, Inc.

- La Linea Verde Societa'Agricola S.p.A.

- Maspex Wadowice Grupa

- Ocean Spray Cranberries, Inc.

- PepsiCo, Inc.

- Rauch Fruchtsafte GmbH & Co OG

- Suntory Holdings Limited

- The Coca-Cola Company

- The Kraft Heinz Company

- Tropicana Brands Group

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Europe Juices Market size is estimated at 38.95 billion USD in 2025, and is expected to reach 47.44 billion USD by 2030, growing at a CAGR of 4.02% during the forecast period (2025-2030).

Reduced sugar intake by consumers in the region is driving the growth of the 100% juice segment

- In 2023, the 100% juice segment dominated the market, capturing the largest market share. In 2022, approximately 50% to 55% of adults actively sought to reduce their sugar intake, highlighting widespread concerns over this ingredient. In the United Kingdom, 53% of females and 45% of males who aimed to cut down on sugar preferred food and drinks with reduced or no sugar content. This trend toward healthier choices extends to night-time drinking occasions, with a growing emphasis on low-sugar and non-sweet flavors.

- As the demand for juices surged in the region, imports followed suit. In 2022, the Netherlands, France, Germany, the United Kingdom, and Belgium emerged as the top importers, collectively accounting for 80% of European imports. Orange juice leads the pack as the most-produced juice in Europe, accounting for 24% of the market. Other significant juice varieties include juice mixtures (21%), apple juice (15%), and grape juice (8%). Fruit purees and concentrated fruit purees are used in the manufacturing of specific juices (such as strawberry, peach, and apricot). They are obtained by suitable processes; for instance, by sieving, grinding, and milling the edible part of the whole/ peeled fruit, without removing juice.

- Juice drinks, with juice content up to 24%, are gaining traction and are projected to witness a CAGR of 4.15% during 2024-2030. Companies are increasingly tailoring their juice drink offerings to cater to the preferences of health-conscious consumers. In the United Kingdom, over half of the 16 to 24 age group consumed juice drinks daily in 2021. Orange juice reigns supreme as the most favored juice in the United Kingdom, especially among younger adults. In 2022, the per capita fruit juice consumption in the country stood at approximately 16.1 liters.

Climatic influences with a rise in hectic lifestyles drive the consumption of different juices in the region

- In Europe, the fruit juices market is witnessing a surge in demand for chilled organic variants, driven by a growing consumer preference for natural products. Consumers are becoming increasingly informed and able to distinguish the quality of products, influenced by factors like climate, premiumization, and evolving lifestyles. The increase in fast-paced lifestyles presents an opportunity for "on-the-go" juice consumption. Health-conscious and ethically-minded consumers are gravitating toward fruit juices in the 100% juice format, which accounted for a 62.56% value share in 2023.

- Among European countries, Germany led in terms of juice consumption by value in 2023. The country's beverage culture, coupled with a rising number of juice processing units, is fueling the demand for juices. However, in terms of consumption volume, the Netherlands took the lead and is expected to maintain the lead throughout the study period. Taste preferences, followed closely by health benefits, drive juice consumption in the Netherlands. For instance, in 2022, a significant majority (80%) of Dutch consumers cited taste as the primary reason for consuming fruit juices, while an additional 33% highlighted health benefits.

- Turkey stands out as the fastest-growing market, and it is projected to record a CAGR of 6.46% in value from 2024 to 2030. This growth is partly attributed to a regulation that bans the sale of nectars in schools. This policy shift has prompted many nectar producers to pivot toward fruit juice production, ensuring their continued presence in school establishments.

Europe Juices Market Trends

Juices are perceived as healthier than other soft drinks, which is driving sales in the segment

- In Europe, especially the United Kingdom, more than half of people aged 16 to 24 consumed juice drinks at least once a day in 2022. Orange juice is the most popular type of juice in the UK, and it is consumed more frequently by younger adults.

- Many consumers are looking for juices that are high in vitamins, minerals, and antioxidants, and low in sugar and calories and avoid juices containing artificial sweeteners and added sugar.

- The sales of the juice segment are related to the health and wellness trends in the country. European demand for orange juice could decline due to the penetration of other flavors in the market in addition to the changing consumer preference towards innovative flavors.

- The majority of adults around 57% are actively taking steps to limit/reduce their sugar intake, reflecting widespread concerns over this ingredient.

Europe Juices Industry Overview

The Europe Juices Market is fragmented, with the top five companies occupying 8.58%. The major players in this market are Britvic PLC, Eckes-Granini Group GmbH, Maspex Wadowice Grupa, Suntory Holdings Limited and Tropicana Brands Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumer Buying Behaviour

- 4.2 Innovations

- 4.3 Brand Share Analysis

- 4.4 Regulatory Framework

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Soft Drink Type

- 5.1.1 100% Juice

- 5.1.2 Juice Drinks (up to 24% Juice)

- 5.1.3 Juice concentrates

- 5.1.4 Nectars (25-99% Juice)

- 5.2 Packaging Type

- 5.2.1 Aseptic packages

- 5.2.2 Disposable Cups

- 5.2.3 Glass Bottles

- 5.2.4 Metal Can

- 5.2.5 PET Bottles

- 5.3 Distribution Channel

- 5.3.1 Off-trade

- 5.3.1.1 Convenience Stores

- 5.3.1.2 Online Retail

- 5.3.1.3 Supermarket/Hypermarket

- 5.3.1.4 Others

- 5.3.2 On-trade

- 5.3.1 Off-trade

- 5.4 Country

- 5.4.1 Belgium

- 5.4.2 France

- 5.4.3 Germany

- 5.4.4 Italy

- 5.4.5 Netherlands

- 5.4.6 Russia

- 5.4.7 Spain

- 5.4.8 Turkey

- 5.4.9 United Kingdom

- 5.4.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Britvic PLC

- 6.4.2 Brynwood Partners

- 6.4.3 Conserve Italia - Consorzio Italiano Fra Cooperative Agricole Soc Coop Agricola

- 6.4.4 Eckes-Granini Group GmbH

- 6.4.5 Keurig Dr Pepper, Inc.

- 6.4.6 La Linea Verde Societa' Agricola S.p.A.

- 6.4.7 Maspex Wadowice Grupa

- 6.4.8 Ocean Spray Cranberries, Inc.

- 6.4.9 PepsiCo, Inc.

- 6.4.10 Rauch Fruchtsafte GmbH & Co OG

- 6.4.11 Suntory Holdings Limited

- 6.4.12 The Coca-Cola Company

- 6.4.13 The Kraft Heinz Company

- 6.4.14 Tropicana Brands Group

7 KEY STRATEGIC QUESTIONS FOR SOFT DRINK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms