欧州の砂糖菓子類:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Europe Sugar Confectionery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 216 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684017

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

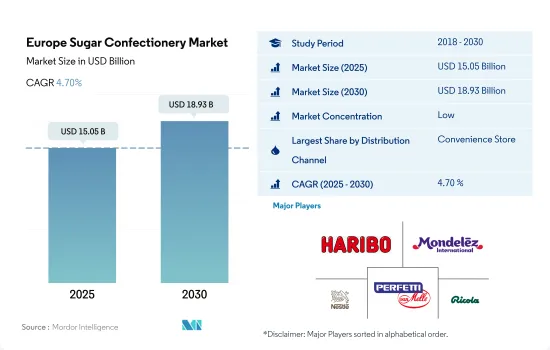

欧州の砂糖菓子類の市場規模は2025年に150億5,000万米ドルと推定・予測され、2030年には189億3,000万米ドルに達し、予測期間(2025年~2030年)のCAGRは4.70%で成長すると予測されます。

コンビニエンスストアは近接性要因で市場をリードし、2023年~2024年の成長率は3.84%を予測

- 欧州の砂糖菓子市場で最大のチャネルはコンビニエンスストアです。2023年には、他のすべての流通チャネルと比較して、金額ベースで43.89%の主要シェアを占めています。コンビニエンスストアは、消費者に広くリーチできること、プライベートブランドへのアクセスが容易であること、こうしたチャネルの拡大が消費者のコンビニエンスストアへの嗜好を高める主な要因となっています。欧州諸国の中でコンビニエンスストアの店舗数が最も多いのは英国で、2021年には47,000店舗以上が存在します。

- スーパーマーケットとハイパーマーケットは、欧州全域でコンビニエンスストアに次いで砂糖菓子類を購入するのに広く好まれている流通チャネルです。このセグメントは、2022年と比較して2023年には3.29%成長しました。これらの流通チャネルは、消費者が市場で入手可能な多種多様な砂糖菓子類から購入を決定する際に影響を与えるという利点があります。幅広い砂糖菓子ブランドにアクセスしやすいことから、スーパーマーケットとハイパーマーケットにおける砂糖菓子製品の販売額は、この地域の予測期間中にCAGR 3.15%を記録すると予想されます。

- オンライン・チャネルは、この地域で砂糖菓子類が消費される流通チャネルとして急成長しています。このセグメントは2024~2027年の間に金額ベースで18.3%の成長を記録すると予測されています。消費者は、迅速な配達オプションを提供するオンライン・チャネルを好む可能性が高いです。同地域のインターネット普及率の高さは、予測期間中、オンライン・チャネルを後押しすると思われます。2022年、この地域のインターネット利用者は7億5,000万人で、インターネット普及率は全人口の89.7%でした。

ドイツと英国の消費者が牽引するパスティーユ、グミ、ゼリーの高い消費量が市場拡大を促進

- ドイツと英国はこの地域の砂糖菓子類の主要市場であり、ロシアとフランスがこれに続きます。ドイツと英国は、2023年の同地域全体の砂糖菓子類販売額の38%を占めています。キャンディ、ロリポップ、パスティル、グミ、ゼリー、ミントなどさまざまな種類の入手可能性が高まっていることが、消費者の衝動的な購買行動に後押しされ、高い需要につながっています。便利で嗜好性の高い間食に対する消費者の嗜好が、この地域の主要な市場促進要因となっています。2022年には、ドイツのスナッカーの72%がキャンディーとチョコレートバーを週単位で消費しています。

- パスティーユ、グミ、ゼリーは主要カテゴリーであり、2023年にはドイツの砂糖菓子類市場全体で43%の金額シェアを占める。過去数年間にパスティルの消費が急増したのは、主に薬用トローチやのど飴の消費が増加したためと考えられます。また、亜鉛、ビタミンC、ハチミツなどの成分を含むフルーツ風味のパスティーユも、健康志向の消費者の間で人気となっており、これが市場の成長をさらに後押ししています。ドイツのパスティル、ゼリー、グミ市場は、2023年には販売額ベースで2022年比3%の成長を記録しました。

- トルコとスペインは欧州で最も急成長している菓子類市場です。トルコの砂糖菓子類市場は、予測期間中に金額ベースでCAGR 11%で拡大すると予測されます。宗教的なお祭りや結婚式、お祝い事の際の贈り物として砂糖菓子が伝統的に親しまれていることが、トルコ市場の成長を後押ししています。

欧州の砂糖菓子類市場の動向

欧州の人々の間で、クリスマスやその他のお祭りなどの機会にお菓子に耽溺する傾向が強まるとともに、衝動買いが増加していることが市場を支えています。

- 欧州における砂糖菓子類の消費は、同地域の人々の文化的な祝い事や定期的な間食などの要因によるものです。英国では、2022年には約58%の消費者が食間にスナックを食べることを好み、ドイツとフランスがそれぞれ44%と30%でこれに続きます。

- 消費者は砂糖の摂取量について適切な選択をするために、ラベルや内容物を絶えず吟味しています。さらに各社は、家族との内祝い用にお菓子を購入する場合でも、友人と分かち合うお菓子を選ぶ場合でも、自分へのご褒美の場合でも、糖分摂取量をコントロールしたいと考える消費者により多くの透明性、選択肢、分量ガイダンスの選択肢を提供しています。

- この地域では、砂糖菓子類は低価格帯から高級プレミアム帯の消費者に提供されています。2022年、年間平均消費者物価指数(CPI)によると、砂糖、ジャム、シロップ、砂糖菓子類の価格指数値は、英国で110.1指数ポイントと測定されました。

- 同地域では健康志向の消費者が増加しており、砂糖菓子類であっても、あらゆる製品に健康的な代替品を求める声が高まっています。多くの消費者は、健康的な食習慣を維持するのに役立つ製品を求めています。その結果、消費者はここ数十年、スーパーフード原料を使用した商品をより多く購入するようになっています。

欧州の砂糖菓子類産業の概要

欧州の砂糖菓子類市場は細分化されており、上位5社で38.67%を占めています。この市場の主要企業は以下の通り。 HARIBO Holding GmbH & Co. KG, Mondelez International Inc., Nestle SA, Perfetti Van Melle BV and Ricola AG(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 規制の枠組み

- 消費者の購買行動

- 成分分析

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 菓子類

- ハードキャンディ

- ロリポップ

- ミント

- パスティル、グミ、ゼリー

- トフィーとヌガー

- その他

- 流通チャネル

- コンビニエンスストア

- オンラインストア

- スーパーマーケット

- その他

- 国名

- ベルギー

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- スイス

- トルコ

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- August Storck KG

- Cloetta AB

- Ferrero International SA

- HARIBO Holding GmbH & Co. KG

- Katjes International GmbH & Co. KG

- Lavdas SA

- Mars Incorporated

- Mondelez International Inc.

- Nestle SA

- Perfetti Van Melle BV

- Ricola AG

- Soldan Holding+Candy Specialties GmbH

- Swizzels Matlow Ltd

- The Hershey Company

- Vidal Golosinas

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The Europe Sugar Confectionery Market size is estimated at 15.05 billion USD in 2025, and is expected to reach 18.93 billion USD by 2030, growing at a CAGR of 4.70% during the forecast period (2025-2030).

Proximity factor helps convenience stores lead the market, projecting a growth rate of 3.84% for 2023-2024

- Convenience stores are the largest channels in the European sugar confectionery market. The channel held the major share of 43.89% by value compared to all other distribution channels in 2023. The broader reach, easy access to private label brands, and the increasing expansion of these channels are the key factors driving consumer preference toward them. Among countries in Europe, the United Kingdom recorded the highest number of convenience stores, with over 47,000 stores existing in the country in 2021.

- Supermarkets and hypermarkets are the second most widely preferred distribution channels after convenience stores to purchase sugar confectionery products across Europe. The segment grew by a value of 3.29% in 2023 compared to 2022. The proximity factor of these channels in the countries provides them with an added advantage of influencing the consumer's decision to purchase from a large variety of sugar confectionery products available in the market. Owing to the accessibility to a wide range of sugar confectionery brands, the sales value of sugar confectionery products in supermarkets and hypermarkets is anticipated to register a CAGR of 3.15% during the forecast period in the region.

- Online channels are the fastest-growing distribution channel through which sugar confectionery products are consumed in the region. The segment is projected to register a growth of 18.3% by value during the period 2024-2027. Consumers are likely to prefer online channels as they provide quick delivery options. The high internet penetration in the region will likely aid online channels during the forecast period. In 2022, the region had 750 million internet users, with an internet penetration rate of 89.7% of the total population.

High consumption of pastilles, gummies, and jellies led by German and UK consumers fuels market expansion

- Germany and the United Kingdom are identified as the region's major markets for sugar confectionery, followed by Russia and France. Germany and the United Kingdom collectively accounted for a 38% share of the overall sugar confectionery value sales across the region in 2023. The increasing availability of different varieties of candies, lollipops, pastilles, gummies, jellies, and mints has led to their high demand, fueled by the impulsive purchase behavior of consumers. Consumer preference for convenient indulgent snacking is identified as the key market driver in the region. In 2022, 72% of German snackers consumed candy and chocolate bars on a weekly basis.

- Pastilles, gummies, and jellies are the leading categories, holding a 43% value share in the overall sugar confectionery market in Germany in 2023. The surge in consumption of pastilles over the past few years may be primarily attributed to the increased consumption of medicinal or throat lozenges, a type of pastille that helps provide temporary relief from coughs and other throat problems. The availability of fruit-flavored pastilles containing ingredients such as zinc, vitamin C, and honey has also become popular among health-conscious consumers, which is further boosting the market's growth. The pastilles, jellies, and gummies market in Germany observed a growth of 3% in 2023 compared to 2022 in terms of value sales.

- Turkey and Spain are identified as the fastest-growing confectionery markets in Europe. The Turkish sugar confectionery market is anticipated to expand at a CAGR of 11% in terms of value during the forecast period. The traditional popularity of sugar confectionery as gifts during religious festivals, wedding ceremonies, and celebrations fuels the market's growth in Turkey.

Europe Sugar Confectionery Market Trends

The rising impulse buying behavior, along with increasing indulgence in sweets during occasions like Christmas and other festivals, among Europeans support the market

- Sugar confectionery consumption in Europe is attributed to factors like cultural celebrations and regular snacking among the population in the region. In the United Kingdom, about 58% of consumers preferred consuming snacks between meals in 2022, followed by Germany and France with 44% and 30%, respectively.

- Consumers continuously scrutinize labels and contents to make sound choices about their sugar intake. Furthermore, companies are bringing more transparency, choice, and portion guidance options to consumers looking to control their sugar intake, whether they are purchasing candy for home celebrations with their family, selecting a treat to share with friends, or treating themselves.

- In the region, sugar confectionery is available to consumers in the low-range to high-end premium range. In 2022, as per the annual average Consumer Price Index (CPI), the price index value of sugar, jams, syrups, and sugar confectionery items was measured at 110.1 index points in the United Kingdom.

- With the rising number of health-conscious consumers in the region, there is an increasing demand for healthier alternatives to every product, even for sugar confectionery. Many are seeking products that can help them maintain healthy eating habits. As a result, consumers have been buying more items with superfood ingredients over the last couple of decades.

Europe Sugar Confectionery Industry Overview

The Europe Sugar Confectionery Market is fragmented, with the top five companies occupying 38.67%. The major players in this market are HARIBO Holding GmbH & Co. KG, Mondelez International Inc., Nestle SA, Perfetti Van Melle BV and Ricola AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Regulatory Framework

- 4.2 Consumer Buying Behavior

- 4.3 Ingredient Analysis

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Confectionery Variant

- 5.1.1 Hard Candy

- 5.1.2 Lollipops

- 5.1.3 Mints

- 5.1.4 Pastilles, Gummies, and Jellies

- 5.1.5 Toffees and Nougats

- 5.1.6 Others

- 5.2 Distribution Channel

- 5.2.1 Convenience Store

- 5.2.2 Online Retail Store

- 5.2.3 Supermarket/Hypermarket

- 5.2.4 Others

- 5.3 Country

- 5.3.1 Belgium

- 5.3.2 France

- 5.3.3 Germany

- 5.3.4 Italy

- 5.3.5 Netherlands

- 5.3.6 Russia

- 5.3.7 Spain

- 5.3.8 Switzerland

- 5.3.9 Turkey

- 5.3.10 United Kingdom

- 5.3.11 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 August Storck KG

- 6.4.2 Cloetta AB

- 6.4.3 Ferrero International SA

- 6.4.4 HARIBO Holding GmbH & Co. KG

- 6.4.5 Katjes International GmbH & Co. KG

- 6.4.6 Lavdas SA

- 6.4.7 Mars Incorporated

- 6.4.8 Mondelez International Inc.

- 6.4.9 Nestle SA

- 6.4.10 Perfetti Van Melle BV

- 6.4.11 Ricola AG

- 6.4.12 Soldan Holding + Candy Specialties GmbH

- 6.4.13 Swizzels Matlow Ltd

- 6.4.14 The Hershey Company

- 6.4.15 Vidal Golosinas

7 KEY STRATEGIC QUESTIONS FOR CONFECTIONERY CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 216 Pages

- 納期

- 2~3営業日