|

市場調査レポート

商品コード

1851000

米国リテールバンキング:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)US Retail Banking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国リテールバンキング:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月06日

発行: Mordor Intelligence

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

概要

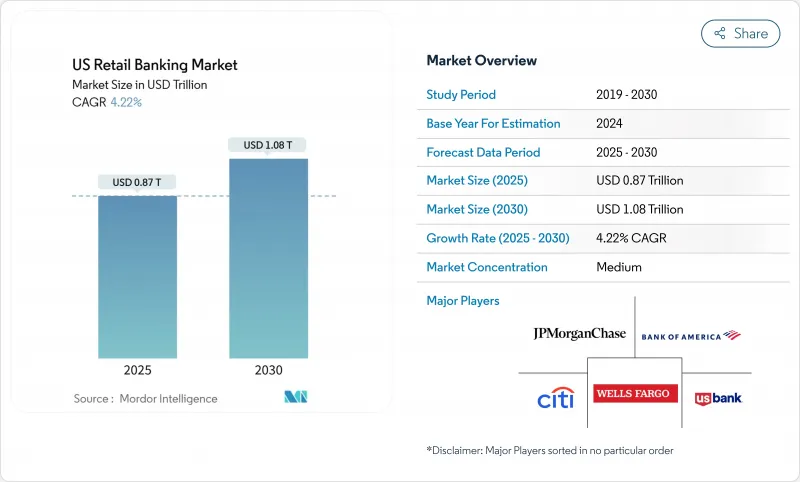

米国のリテール・バンキング市場は、2025年に8,700億米ドル、2030年には1兆800億米ドルに達すると予測され、2025~2030年のCAGRは4.22%となります。

堅調なローン需要、底堅い預金基盤、消費者のデジタル・バンキングへの急速な移行が成長を支えています。銀行は、進化する顧客の期待に応えるため、手数料無料のモバイル商品を拡大する一方、人工知能を活用して営業コストを削減し、新サービスを迅速に立ち上げています。フィンテック専門企業からの競合圧力は利ざやを圧縮しているが、国内金融機関は引き続き規模を活用して収益性を維持しています。当座貸越手数料や公正融資基準をめぐる規制の開発により、銀行は収益源をアドバイザリー主導の商品やサブスクリプション・モデルに多様化する必要に迫られています。

米国リテールバンキング市場動向と洞察

家計債務の増加がローン需要を促進

2025年第1四半期の家計債務は18兆2,000億米ドルに達し、四半期ベースで0.9%増加し、住宅ローン残高だけでも1,990億米ドル拡大した。金融政策が制限されているにもかかわらず、消費者は住宅、自動車、教育のために借り入れを続けています。銀行は、機械学習によるリスク管理ツールを導入し、債務不履行率を大幅に上昇させることなく、十分なサービスを受けていない借り手にも融資を拡大しています。そのため、米国のリテール・バンキング市場は、この債務増加を活用して純利息収益の拡大を図るとともに、クレジット商品に関連する付帯保険やアドバイザリー業務を拡大しています。

デジタル口座開設を加速させるZ世代のモバイル・ウォレット普及の急増

世界のデジタル・ウォレット利用者数は、予測期間中に大幅な伸びが見込まれます。Z世代の顧客は、生体認証とインスタント・オンボーディングを優先し、代替決済の採用率が高年齢層よりも3倍高いです。大手銀行は現在、数分以内に当座預金の承認と入金を行い、デジタル・ネイティブの金融生活に早くから影響力を持つようになっています。モバイル預金や個人間決済への嗜好の高まりは、新規リテール口座のデジタルシェアを高め、米国リテール・バンキング市場のオムニチャネル化を促進しています。

フィンテック主導の金利圧縮が純利鞘を圧迫

急成長するデジタル金融機関は、無駄のないコスト構造とアルゴリズムによるプライシングを実現し、預金利回りの向上とローン金利の引き下げを可能にしています。伝統的な銀行は、オファーに応じなければシェア低下のリスクを負うことになるが、この対応はスプレッドを狭め、利益の伸びを制限します。この制約は、フィンテックの導入が最も進んでおり、金利に敏感な家計がオンライン・チャネルを通じて残高を素早く移動させる大都市圏で最も深刻です。

セグメント分析

2024年の米国リテール・バンキング市場シェアの29.3%はローンであり、堅調な住宅ローンと自動車需要を反映しています。クレジットカードに関連する米国のリテール・バンキング市場規模は、発行会社が体験型特典と即時仮想プロビジョニングを展開するにつれて、2030年までCAGR 6.4%で拡大すると予測されます。柔軟な返済プランと早期賃金アクセス機能の急速な普及により、高金利下でもリボルビング残高が好調を維持しています。取引口座は依然として顧客維持の基盤となっているが、マルチバンキングが主流になるにつれて伸びは緩やかになっています。貯蓄性商品は、デジタル専業銀行が2%を超える利回りを宣伝しており、新たな魅力を享受しているが、利ざやの圧力が長期的な貢献の上限に達しています。

消費者金融保護局は、汎用カードを上回る小売店向けカードのコストについて消費者に注意を促し、発行会社はより明確な価格開示の導入に拍車をかけています。デビットカードは引き続き日常的な決済を支配しているが、モバイルウォレットや非接触クレジットに相対的にシェアを奪われています。そのため銀行は、ユーザーが1つのアプリケーション内で当座預金、貯蓄、後払い、クレジットカードの各機能をシームレスに利用できる統合エコシステムを設計しています。

2024年、米国リテール・バンキング市場の58.2%をオンライン・バンキングが占める。ドルではなくセントと推定される取引単価の低さが、さらなる移行を後押ししています。モバイル・ログインがデジタル・トラフィックの4分の3を占め、ピアツーピア決済とモバイル・チェック・デポジットが牽引。米国のリテール・バンキングの市場規模は、支店網に縛られ、複雑な相談に対応することに変わりはないが、支店の形態は、伝統的な窓口ではなく、ラウンジスタイルの相談拠点へとシフトしています。

AIを搭載したチャットボットは24時間体制で日常的な問い合わせに対応し、音声認識ツールは数秒で顧客を認証するため、顧客満足度のスコアが向上しています。銀行は、アプリで予約したビデオ予約を支店で完結できるようにすることで、チャネルを融合させています。このアプローチは、デジタルの利便性を維持しながら、人間によるカウンセリングの信頼性を維持するものです。コンプライアンス基準では、各チャネルにおける同意の文書化が義務付けられており、堅牢なデータ同期が業務上不可欠となっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 家計債務の増加が融資需要を刺激

- Z世代のモバイルウォレット導入が急増、デジタル口座開設が加速

- 連邦準備制度理事会(FRB)の金融引き締め政策下で競争力のある預金金利が貯蓄残高を押し上げる

- 組み込み型金融小売業との提携によりPOSクレジットカード発行を拡大

- FHA政策のアップデートにより、初めて住宅を購入する人の住宅ローン増加が促進される

- クラウドネイティブのコアアップグレードにより、製品のリリースサイクルを短縮

- 市場抑制要因

- フィンテックによる金利圧縮が純金利マージンを圧迫

- CFPBの当座貸越手数料上限案が非金利収入を脅かす

- 支店合理化コストが地方への展開を制限

- サイバー詐欺の増加がコンプライアンス費用の増加とデジタル化の遅れを招いている

- バリュー/サプライチェーン分析

- 規制の見通し

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品別

- 取引口座

- 貯蓄口座

- デビットカード

- クレジットカード

- ローン

- その他の製品

- チャネル別

- オンラインバンキング

- オフラインバンキング

- 顧客年齢層別

- 18~28歳

- 29~44歳

- 45~59歳

- 60歳以上

- 銀行の種類別

- 国立銀行

- 地方銀行

- ネオバンクとその他

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- JPMorgan Chase & Co.

- Bank of America Corp.

- Wells Fargo & Co.

- Citigroup Inc.

- U.S. Bancorp

- Truist Financial Corp.

- PNC Financial Services Group Inc.

- TD Group US Holdings LLC

- Capital One Financial Corp.

- Fifth Third Bancorp

- KeyCorp

- Regions Financial Corp.

- Citizens Financial Group

- First Citizens BancShares

- Synchrony Financial

- Ally Financial Inc.

- Discover Financial Services

- SoFi Technologies Inc.

- Chime Financial Inc.

- Navy Federal Credit Union