|

市場調査レポート

商品コード

1683095

米国の種子処理:市場シェア分析、産業動向、成長予測(2025~2030年)United States Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の種子処理:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 70 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

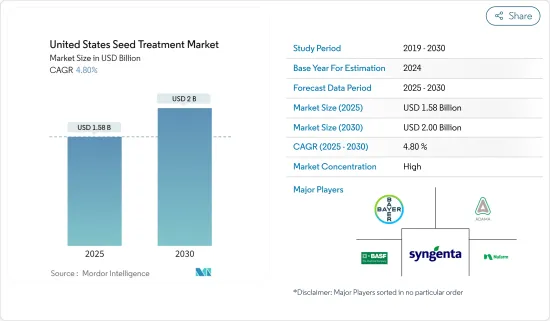

米国の種子処理市場規模は2025年に15億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.8%で、2030年には20億米ドルに達すると予測されています。

米国の種子処理市場は、食糧安全保障に対する需要の増加、種子処理製品の採用率の上昇、種子処理の利点に関する農業従事者の意識の高まりなどの要因によって、大幅な成長を遂げています。種子処理製品は、米国で毎年植えられるトウモロコシのほぼ全エーカーに適用され、米国の農業従事者が栽培する約800億米ドル相当の作物を支えるのに役立っています。

人口が増え続ける中、農業生産性を高め、食料安全保障を確保する必要性が高まっています。こうした目的を達成する上で、種子処理は重要な役割を果たしています。種子を処理することで、農業従事者は作物の成長を妨げ収量を減少させるさまざまな病気や害虫、環境ストレスから種子を守ることができます。種子処理は初期の防御線を提供し、成長の重要な段階で種子と幼苗を保護します。

米国の種子処理市場の動向

高品質種子のコスト上昇

ハイブリッドや遺伝子組み換え種子に関連する高コストは、種子処理市場の成長を促進する主要要因のひとつです。種子処理は、燻蒸や農薬の葉面散布に関する規制問題が増加しているため、農業従事者が高品質の種子への投資を保護する手段として検討されるようになっています。望ましい農学的形質を備えた高品質の種子に対する需要の増加により、種子のコストは上昇すると予想されます。企業も農業従事者も、高品質の種子を保存するために、種子処理ソリューションに費用をかける用意があります。GM種子のほとんどはコストが高く、化学処理で処理されているため、GM作物の栽培面積が増加しており、これが市場成長にプラスの影響を与えています。

処理済み種子の使用増加

農作物の消費量の急激な増加による高収量への需要が、米国における種子処理市場の需要を増大させています。農場規模の拡大と輪作の減少が、種子処理製品の需要増加につながる主要要因です。トウモロコシは米国で栽培されている主要作物の一つであり、2018年には約3,310万ヘクタールが収穫されました。米国ではトウモロコシ種子の約90%が種子処理されており、種子処理の成長率は大きいです。

米国の種子処理産業概要

主要市場参入企業が最も広く採用している戦略には、新製品の上市(他の全戦略市場シェアの41%で採用されている)があり、次いで買収(20%超)です。研究開発の拡大、パートナーシップや合弁事業も、市場の主要企業が採用しているその他の重要な戦略の一部です。農業における種子処理の意義を理解するための調査を行いながら、より広い地域をカバーするために販売チームを拡大している主要企業によって、大面積の機会に対処するための戦略的パートナーシップのライセンス契約や販売契約が利用されています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ

- 殺虫剤

- 殺菌剤

- 殺線虫剤

- 作物タイプ

- 穀物

- 油糧種子と豆類

- 果物と野菜

- 商業作物

- 芝と観賞用作物

第6章 競争情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Syngenta International AG

- Bayer CropScience AG

- BASF SE

- Corteva Agriscience

- Adama Agricultural Solutions Ltd

- Germains Seed Technology

- UPL Limited

- Incotec Group BV

第7章 市場機会と今後の動向

The United States Seed Treatment Market size is estimated at USD 1.58 billion in 2025, and is expected to reach USD 2.00 billion by 2030, at a CAGR of 4.8% during the forecast period (2025-2030).

The seed treatment market in the United States has been witnessing substantial growth driven by factors such as increasing demand for food security, rising adoption of seed treatment products, and growing awareness among farmers about the benefits of seed treatment. Seed treatment products, applied to nearly every acre of corn planted in the United States every year, helped support nearly USD 80 billion worth of crops grown by the American farmers.

As the population continues to grow, there is a greater need to enhance agricultural productivity and ensure food security. Seed treatments play a crucial role in achieving these objectives. By treating seeds, farmers can protect them from various diseases, pests, and environmental stresses, which can hinder crop growth and reduce yields. Seed treatments provide an early line of defense and protect seeds and young seedlings during critical stages of growth.

US Seed Treatment Market Trends

Increase in Cost of High-quality Seeds

High costs associated with hybrids and genetically modified seeds are among the major factors driving the growth of the seed treatment market. Seed treatment is being increasingly considered by farmers as a mode to protect investments made on good-quality seeds, due to an increase in regulatory issues relating to fumigation, as well as the foliar application of pesticides. The cost of seeds is expected to increase, owing to an increase in the demand for high-quality seeds with desirable agronomic traits. Both companies and farmers are ready to spend on seed-treatment solutions, in order to save high-quality seeds. Since most of the GM seeds are costly and treated with chemical treatments, there is an increase in the area under GM crops, which is positively affecting the market growth.

Increasing Usage of Treated Seeds

The demand for higher yield due to the rapid increase in the consumption of crops has increased the demand for the seed treatment market in the United States. Increasing farm size and decreasing crop rotation are the major factors that lead to an increase in the demand for seed-treatment products. Corn is one of the major crops grown in the United States, with around 33.1 million hectares harvested in 2018. In the United States, around 90% of the corn seeds are treated with seed treatment, and there is a significant percentage of growth in seed treatment.

US Seed Treatment Industry Overview

The most widely adopted strategies by major market players include new product launches (which is being adopted 41% times of all other strategies market share), followed by acquisitions (over 20% of the time). R&D expansion and partnerships or joint ventures are some of the other important strategies, followed by major companies in the market. Strategic partnership licensing and distribution agreements to address broad-acre opportunities are being used by top players, who are expanding their sales teams for larger geographic coverage, with researches on understanding the significance of seed treatment in agriculture.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Insecticides

- 5.1.2 Fungicides

- 5.1.3 Nematicides

- 5.2 Crop Type

- 5.2.1 Grains and Cereals

- 5.2.2 Oilseeds and Pulses

- 5.2.3 Fruits and Vegetables

- 5.2.4 Commercial crops

- 5.2.5 Turf and Ornamentals

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Syngenta International AG

- 6.3.2 Bayer CropScience AG

- 6.3.3 BASF SE

- 6.3.4 Corteva Agriscience

- 6.3.5 Adama Agricultural Solutions Ltd

- 6.3.6 Germains Seed Technology

- 6.3.7 UPL Limited

- 6.3.8 Incotec Group BV