|

|

市場調査レポート

商品コード

1640415

データセンター冷却:市場シェア分析、産業動向と統計、成長予測(2025年~2031年)Data Center Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2031) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| データセンター冷却:市場シェア分析、産業動向と統計、成長予測(2025年~2031年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

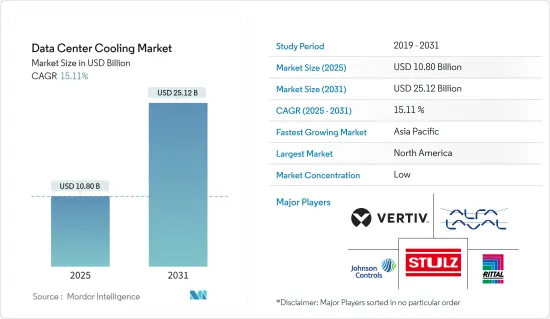

データセンター冷却の市場規模は2025年に108億米ドルと推定され、予測期間(2025-2031年)のCAGRは15.11%で、2031年には251億2,000万米ドルに達すると予測されます。

主なハイライト

- AIやメディアアプリケーションの計算ニーズが高いため、データセンターの導入が世界的に進んでいます。これらのデータセンターは大量の電力を消費し、大量の熱を発生させるため、さまざまな効率的な冷却システムの必要性がさらに高まっています。

- データセンター冷却市場は、デジタル化の進展によりコンピュータの性能が向上し、より多くの集積小型チップが必要となるため、大幅な成長が見込まれています。データセンターの設計と冷却の必要性は、主にAIワークロード用の強力なコンピュータ・ハードウェアの影響を受けています。メーカーは、人工知能や高性能コンピューティングのワークロードのパフォーマンスを最適化するために、大型シリコンチップを導入しています。人工知能と高性能コンピューティング環境における強力なGPUの使用は、データセンターの冷却技術の必要性を裏付けています。

- OTTやストリーミング・サービスの利用拡大がデータの増加につながり、市場開拓を促進しています。また、Disney+Hotstar、Hulu、Netflixなどのオンライン・ストリーミング・サービスからのデータ増加が、データセンター冷却システムの需要を促進すると予想されます。

- 市場プレーヤーは、世界な事業展開とサービス提供の拡大に注力することで、消費者基盤の増強に取り組んでいます。例えば、2024年3月に、インテリジェント電力管理会社のイートンは、機械学習、エッジコンピューティング、AIの増加する要件を迅速に満たそうとしている組織のための革新的なモジュール式データセンター・ソリューションの北米での発売を宣言しました。イートンのSmartRackモジュラー・データセンターは主にITラックと冷却とサービス・エンクロージャを組み合わせて,最大150kWの機器負荷がある重要なIT機器のための性能最適化されたデータセンター・ソリューションを構築します。

- 同市場の成長は、さまざまな適応性への要求の高まりと世界の電力不足によって阻害されると予想されます。また、時代遅れのインフラや最適化されていないレイアウトなど、非効率な冷却システム設計の使用は、エネルギー効率の低下や運用コストの増加につながり、エネルギー価格の上昇は冷却費用を法外なものにする可能性があるため、予測期間中の市場成長を抑制する要因の1つとなっています。

データセンター冷却市場の動向

IT・通信セグメントが最も高い成長を遂げる見込み

- 情報技術によって生成されるデータの急激な増加により、効率的なデータセンターが必要とされ、高度な冷却ソリューションへの需要が高まっています。増大するワークロードとストレージ需要に対応するためにデータセンターが拡張されるにつれ、発生する熱は重大な懸念事項となり、効果的な冷却ソリューションへの需要を生み出しています。

- クラウドストレージの採用は年々増加しています。より効率的な作業プロセスを提供するため、マイクロソフト、AWS、グーグルなどのクラウド・ストレージ・プロバイダーは、クラウドに保存する容量を拡大しています。これらの企業は、ハイパースケール・トランザクションに投資を行っています。その結果、SaaS(Software-as-a-Service)の拡大により、クラウドストレージ・プロバイダーの容量増強が可能になり、データセンター冷却システムの需要は拡大すると予想されます。

- 液浸冷却には、単相または二相のソリューションがあります。単相液浸冷却では、サーバーを密閉シャーシに収納し、ラックマウントまたはスタンドアロン形式で設計を構成できます。一方、二相液浸冷却は、サーバーを液体に浸しますが、冷却プロセス中に液体が変化します。液体が温まり結露すると、水回路と熱交換器が熱を奪います。2P液浸冷却では、サーバーを収納した金属製の保持タンク内の誘電冷却液が、安全な冷却システムで沸騰・凝縮し、熱伝達効率が飛躍的に向上します。

- 2023年5月、KTクラウドはスイスの液冷ソリューション・プロバイダーであるImmersion 4社と、KTクラウドのデータセンターに次世代液浸冷却技術を導入する契約を締結しました。液浸冷却は、電気が流れない誘電体溶液に情報通信技術機器を浸すことで熱を除去します。これにより、空冷システムで起こりうるデータセンターのサーバールーム温度の不均衡やファンの騒音が解消されます。

アジア太平洋地域が著しい成長を遂げる見込み

- アジア太平洋地域は、主にネットワークインフラの急速な開発により、予測期間中に最も速い成長率を記録すると予測されています。同地域ではデータ生成の需要が増加しており、特にインドや中国のような国々では政府の政策によりエネルギー効率の高いインフラ整備が進められています。また、AIを活用した冷却管理や液冷システムなどの技術の進歩が状況を変え、この地域でのさらなる採用を促進しています。

- 中国と日本は、IoT、ML、AIなどの領域における継続的な技術革新と開発に基づいて、市場の成長機会を大きく促進すると期待される最も重要な国の1つです。さらに、これらの国々ではデータセンターの数が急速に増加しており、地域全体でより環境に配慮したインフラを推進する政府の政策が、これらのデータセンター内でより優れた、より効果的な冷却ソリューションの必要性を促進しています。

- 例えば、2024年4月、アジアで高性能データセンターを運営・開発するGDSと、アジア太平洋地域の不動産市場やその他の参入障壁の高い世界市場に特化したプライベート・エクイティ・ファンド運用会社であるGaw Capital Partnersは、日本の東京に40メガワット(MW)のデータセンター・キャンパスを建設する戦略的パートナーシップを締結しました。

- アジア太平洋地域のデータセンター冷却市場は、主にデータ消費とクラウドサービスの急激な成長によって活性化しています。企業がデジタルインフラを拡大するにつれ、最適な動作温度を維持するための効率的な冷却システムへの需要が高まっています。また、エネルギー効率と環境の持続可能性に関する厳しい規制が、革新的な冷却技術の採用を後押ししています。新興国はITインフラに多額の投資を行っており、信頼性と拡張性の高い冷却ソリューションへのニーズが市場の成長をさらに後押ししています。

- 2023年12月、オーストラリアのクラウドサービスプロバイダーであるResetData社は、先駆的な液冷データセンター・サーバー技術の試験・シミュレーションラボを開設しました。これは、液冷環境でワークロードを試行できるアジア太平洋で最初の施設の1つでした。この一歩により、地元企業はAIや機械学習などの過酷なアプリケーションに不可欠な、よりエコロジカルで高性能なIaaS(Infrastructure-as-a-Service)を利用できるようになった。

データセンター冷却業界の概要

データセンター冷却市場は、主要な業界プレーヤー間の統合度が低いです。注目すべき市場リーダーには、Stulz GmbH、Alfa Laval AB、Schneider Electric SE、Johnson Controls Inc.、Vertiv Group Corp.、Asetek A/Sが含まれます。大きな市場シェアを誇るこれらの業界大手は、この地域全体で顧客基盤の拡大に積極的に取り組んでいます。彼らの成長戦略は主に、市場シェアと全体的な収益性を高めることを目的とした戦略的な共同作業にかかっています。さらに、Schneider Electric SE、Johnson Controls Inc.、Mitsubishi Electric Europe BVなどの企業は、液体および空気ベースの冷却製品を提供しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 冷却に関する主要コストの考察

- DC冷却を視野に入れたDC運用に関連する主要コストオーバーヘッドの分析

- 設計の複雑さ、PUE、利点、欠点、自然気象条件の利用範囲などの主要要因に基づく、各冷却技術に関連するコストと運用上の考慮事項の比較研究

- データセンター冷却における主な革新と発展

- データセンターで採用されている主なエネルギー効率化手法

第5章 市場力学

- 市場促進要因

- 世界のAIとHPCワークロードの急速なデジタル化と普及

- グリーンデータセンターの出現

- 市場の課題

- コスト、適応要件、停電

- 世界のサプライチェーンの混乱

- 市場機会

- デジタル経済の成長と主要地域における政府支援の増加

- 業界エコシステム分析

第6章 世界のデータセンターの現状分析

- データセンターのIT負荷容量と面積フットプリントの分析(2017~2030年の期間)

- 世界における現在のDCホットスポットと将来の拡張展望の分析

- 主要地域における主要データセンター建設業者と運営業者の分析

第7章 インドネシアデータセンター市場のセグメンテーション

- 冷却技術別

- 空冷

- チラーとエコノマイザー

- CRAH

- 冷却塔(直接冷却、間接冷却、二段階冷却をカバー)

- その他の空冷技術

- 液体ベース冷却

- 液浸冷却

- チップ間直接冷却

- リアドア式熱交換器

- 空冷

- タイプ別

- ハイパースケーラー(所有およびリース)

- エンタープライズ(オンプレミス)

- コロケーション

- 業界別

- ITおよび電気通信

- 小売・消費財

- ヘルスケア

- メディア・エンターテイメント

- 連邦政府機関

- その他エンドユーザー業界別

- 地域別

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域

第8章 競合情勢

- 企業プロファイル

- Vertiv Co.

- Stulz GmbH

- Schneider Electric SE

- Rittal GmbH & Co. KG

- Alfa Laval Corporate AB

- Fujitsu General Limited

- Johnson Controls Inc.

- Hitachi Ltd

- CoolIT Systems Inc.

- Liquid Stack Inc.

- Asetek Inc. A/S

- Asperitas

- Chilldyne Inc.

- Fujitsu Ltd

- Mikros Technologies

- KAORI HEAT TREATMENT Co. Ltd

- Lenovo Group Limited

第9章 投資分析

第10章 市場機会と今後の動向

第11章 出版社について

The Data Center Cooling Market size is estimated at USD 10.80 billion in 2025, and is expected to reach USD 25.12 billion by 2031, at a CAGR of 15.11% during the forecast period (2025-2031).

Key Highlights

- Due to the high computational needs of AI and media applications, data centers are being increasingly deployed worldwide. These data centers consume a massive amount of power, generating a significant amount of heat, further creating the need for various efficient cooling systems.

- The data center cooling market is expected to show substantial growth due to increased digitization, leading to greater computer performance and requiring a larger number of integrated small chips. The design of data centers and the need to cool them are mainly influenced by powerful computer hardware for AI workloads. Manufacturers are introducing large silicon chips to optimize the performance of artificial intelligence and high-performance computing workloads. The use of powerful GPUs in artificial intelligence and high-performance computing environments supports the need for data center cooling technologies.

- The increasing use of OTT and streaming services has led to a growth in data, fostering market development. Also, the increasing data from online streaming services such as Disney+ Hotstar, Hulu, and Netflix is expected to drive the demand for data center cooling systems.

- Market players are taking action to augment their consumer base by focusing on expanding their global footprint and service offerings. For instance, in March 2024, the intelligent power management company Eaton declared the North American launch of an innovative modular data center solution for organizations that are seeking to rapidly fulfill the increasing requirements for machine learning, edge computing, and AI. Eaton's SmartRack modular data centers primarily combine IT racks and cooling and service enclosures to build a performance-optimized data center solution for critical IT equipment with up to 150 kW of equipment load.

- The market's growth is expected to be hampered by the rising need for various adaptability requirements and power shortages worldwide. Also, the use of inefficient cooling system designs, such as outdated infrastructure or poorly optimized layouts, leading to energy inefficiencies and increased operational costs, and rising energy prices, which might make the cooling expenses prohibitive, are some of the factors that can restrain the market's growth during the forecast period.

Data Center Cooling Market Trends

The IT and Telecom Segment is Expected to Witness the Highest Growth

- The exponential growth of data generated by information technology significantly necessitates efficient data centers, driving demand for advanced cooling solutions. As data centers expand to accommodate increasing workloads and storage demands, the heat generated becomes a significant matter of concern, creating demand for effective cooling solutions.

- The adoption of cloud storage has been increasing over the years. To provide more efficient work processes, cloud storage providers such as Microsoft, AWS, and Google are expanding their capacity to store in the cloud. These companies make their investments in hyperscale transactions. As a result, the demand for data center cooling systems is expected to grow due to the expansion of Software-as-a-Service, enabling cloud storage providers to augment their capacity.

- Immersion cooling can be executed in a single-phase or two-phase solution. Single-phase immersion cooling encapsulates the server in a sealed chassis, and the design can be configured in a rackmount or standalone format. However, two-phase immersion cooling locations the server in the liquid, but the liquid transitions during the cooling process. As the fluid warms up and turns to condensation, the water circuit and heat exchanger withdraw the heat. In 2P immersion cooling, dielectric cooling fluid inside a metal holding tank contained with servers is boiled and condensed in a secured cooling system, exponentially growing heat transfer efficiency.

- In May 2023, KT Cloud signed a deal with Immersion 4, a Swiss provider of liquid cooling solutions, to install next-generation immersion cooling technology at KT Cloud data centers. Immersion cooling removes heat by immersing information and communications technology equipment in a dielectric solution where electricity does not flow. This eliminates the imbalance in server room temperatures and fan noise at data centers that can occur with an air-cooling system.

Asia-Pacific is Expected to Register Significant Growth

- Asia-Pacific is estimated to witness the fastest growth rate during the forecast period, mainly due to the rapid development of the network infrastructure. The demand for data generation is increasing in the region, and government policies are promoting more energy-efficient infrastructure, especially in countries like India and China. Also, advancements in technologies such as AI-driven cooling management and liquid cooling systems are reshaping the landscape, driving further adoption in the region.

- China and Japan are among the most important countries that are expected to fuel the market's growth opportunities, significantly based on their ongoing innovations and developments in domains like IoT, ML, and AI. Moreover, the rapidly growing number of data centers in these countries and the government policies to promote more environmentally sound infrastructure across the region are driving the need for better and more effective cooling solutions within these data centers.

- For instance, in April 2024, GDS, an operator and developer of high-performance data centers in Asia, and Gaw Capital Partners, a private equity fund management firm especially focusing on the real estate markets in Asia-Pacific and other high barrier-to-entry markets worldwide, signed a strategic partnership to build a 40 megawatts (MW) data center campus in Tokyo, Japan.

- The Asia-Pacific data center cooling market is primarily fueled by the exponential growth of data consumption and cloud services. As businesses expand their digital infrastructure, the demand for efficient cooling systems to maintain optimal operating temperatures increases. Additionally, stringent regulations regarding energy efficiency and environmental sustainability encourage the adoption of innovative cooling technologies. With emerging economies investing heavily in IT infrastructure, the need for reliable and scalable cooling solutions further fuels market growth.

- In December 2023, the Australian cloud service provider ResetData launched a test and simulation lab for its pioneering liquid-cooled data center server technology. This was one of the first facilities in Asia-Pacific capable of trialing workloads in a liquid-cooled environment. This step empowered local businesses to utilize a more ecological and high-performance Infrastructure-as-a-Service (IaaS) that is essential for strenuous applications like AI and machine learning.

Data Center Cooling Industry Overview

The data center cooling market exhibits a low level of consolidation among key industry players. Notable market leaders include Stulz GmbH, Alfa Laval AB, Schneider Electric SE, Johnson Controls Inc., Vertiv Group Corp., and Asetek A/S. These industry giants, boasting significant market shares, are actively engaged in expanding their customer base throughout the region. Their growth strategies primarily hinge on strategic collaborative efforts aimed at enhancing market share and overall profitability. Moreover, companies such as Schneider Electric SE, Johnson Controls Inc., and Mitsubishi Electric Europe BV offer both liquid and air-based cooling products.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Key Cost Considerations for Cooling

- 4.2.1 Analysis of the Key Cost Overheads Related to DC Operations with an Eye on DC Cooling

- 4.2.2 Comparative Study of the Cost and Operational Considerations Related to Each Cooling Technology Based on Key Factors Such as Design Complexity, PUE, Advantages, Drawbacks, and Extent of Utilization of Natural Weather Conditions

- 4.2.3 Key Innovations and Developments in Data Center Cooling

- 4.2.4 Key Energy Efficiency Practices Adopted in Data Centers

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid Digitization and Adoption of AI and HPC Workload Around the Globe

- 5.1.2 Emergence of Green Data Centers

- 5.2 Market Challenges

- 5.2.1 Costs, Adaptability Requirements, and Power Outages

- 5.2.2 Supply Chain Disruption Globally

- 5.3 Market Opportunities

- 5.3.1 The Growth of the Digital Economy and Increasing Government's Support across Major Regions

- 5.4 Industry Ecosystem Analysis

6 ANALYSIS OF THE CURRENT DATA CENTER FOOTPRINT IN GLOBAL

- 6.1 Analysis of IT Load Capacity and Area Footprint of Data Centers (For the Period of 2017-2030)

- 6.2 Analysis of the Current DC Hotspots and Scope for Future Expansion Globally

- 6.3 Analysis of Major Data Center Contractors and Operators Across Major Regions

7 INDONESIA DATA CENTER MARKET SEGMENTATION

- 7.1 By Cooling Technology

- 7.1.1 Air-based Cooling

- 7.1.1.1 Chiller and Economizer

- 7.1.1.2 CRAH

- 7.1.1.3 Cooling Tower (Covers Direct, Indirect, and Two-stage Cooling)

- 7.1.1.4 Other Air-based Cooling Technologies

- 7.1.2 Liquid-based Cooling

- 7.1.2.1 Immersion Cooling

- 7.1.2.2 Direct-to-chip Cooling

- 7.1.2.3 Rear-door Heat Exchanger

- 7.1.1 Air-based Cooling

- 7.2 By Type

- 7.2.1 Hyperscalers (Owned and Leased)

- 7.2.2 Enterprise (On-premise)

- 7.2.3 Colocation

- 7.3 By End-user Vertical

- 7.3.1 IT and Telecom

- 7.3.2 Retail and Consumer Goods

- 7.3.3 Healthcare

- 7.3.4 Media and Entertainment

- 7.3.5 Federal and Institutional Agencies

- 7.3.6 Other End-user Verticals

- 7.4 By Region

- 7.4.1 North America

- 7.4.2 Europe

- 7.4.3 Asia-Pacific

- 7.4.4 Rest of the World

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Vertiv Co.

- 8.1.2 Stulz GmbH

- 8.1.3 Schneider Electric SE

- 8.1.4 Rittal GmbH & Co. KG

- 8.1.5 Alfa Laval Corporate AB

- 8.1.6 Fujitsu General Limited

- 8.1.7 Johnson Controls Inc.

- 8.1.8 Hitachi Ltd

- 8.1.9 CoolIT Systems Inc.

- 8.1.10 Liquid Stack Inc.

- 8.1.11 Asetek Inc. A/S

- 8.1.12 Asperitas

- 8.1.13 Chilldyne Inc.

- 8.1.14 Fujitsu Ltd

- 8.1.15 Mikros Technologies

- 8.1.16 KAORI HEAT TREATMENT Co. Ltd

- 8.1.17 Lenovo Group Limited