|

市場調査レポート

商品コード

1849935

中国のデータセンター冷却:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)China Data Center Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国のデータセンター冷却:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月25日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

概要

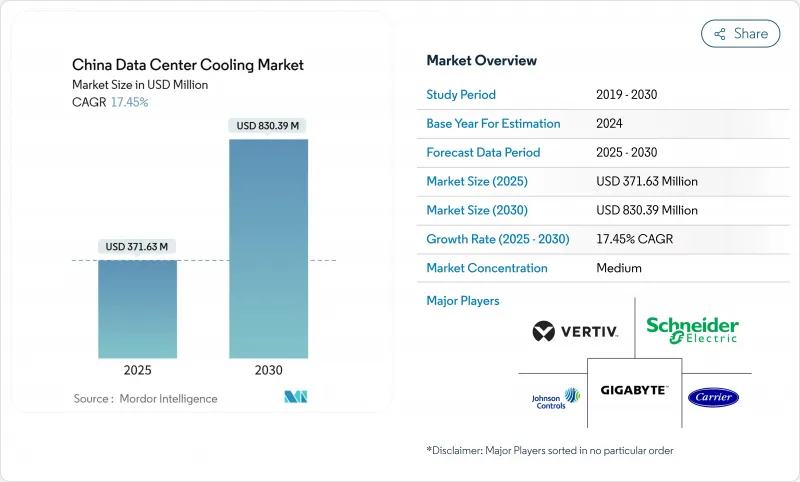

中国のデータセンター冷却市場の2025年の市場規模は3億7,163万米ドル、2030年には8億3,039万米ドルに達すると予測され、2025~2030年のCAGRは17.45%で推移します。

電力使用効率(PUE)上限の義務化、レガシーワークロードの6~8倍の熱を放散するAIサーバーラックの高密度化、政府のEastern Data and Western Computeプログラムなどが、液体ベース冷却への設備投資を加速する要因となっています。事業者は、ティア1都市でPUEを1.3未満に抑える技術を優先し、従来のエアシステムからダイレクト・ツー・チップ、液浸、リアドアの液体ソリューションへと軸足を移しています。同時に、水ストレス規制は、熱効率を最大化しながら消費量を最小化するクローズドループ設計を後押ししています。機器の販売が依然として支出の大半を占めているが、施設のオーナーが改修やグリーンフィールドでの液体導入に専門知識を求めているため、専門サービスに対する需要は急速に高まっています。

中国のデータセンター冷却市場動向と洞察

急増するハイパースケールとAI主導のラック密度

最新のAIキャビネットの消費電力は20~130kWであるのに対し、レガシー・サーバーは5~10kWであるため、空冷では不十分となり、液体技術の大量導入が進んでいます。ファーウェイの密閉型液冷キャビネットは、冷却電力を96%削減し、施設のPUEを1.1に下げ、ハイパースケールレベルでの実行可能性を証明しました。桂安、ウランカブ、蕪湖にある国家的フラッグシップのAIコンピュート・クラスターは現在、構築段階で液体ソリューションを指定しており、データセンター計画において熱設計をチップ性能と同等に位置づける構造的転換を強調しています。

政府による新設データセンターのPUE上限設定

北京の第14次5カ年計画では、2025年までにすべての新設データセンターがPUE1.5未満で運用されることを義務付けており、上海ではその基準が1.3に強化されています。2023年のグリーンデータセンター基準では、水消費比率と再生可能エネルギー調達にまで準拠が拡大され、液冷が効率目標を大規模に達成するための唯一の現実的なルートであることが確定しました。

電気料金の高騰がTCOの優位性を損なう

データセンターの電力使用量は、2025年の200TWhから2030年には400~600TWhに上昇すると予想されており、江蘇省と浙江省の関税は、レガシー機器の減価償却による節約分を帳消しにするほど運用コストを引き上げています。東部データ・西部コンピュート構想は、再生可能エネルギーが豊富な地方に負荷を移すことで負担を軽減するものだが、事業者は遅延やファイバーバックホールの制約を調整する必要があります。

セグメント分析

ハイパースケーラは2024年の売上高の46.5%を占め、中国のデータセンター冷却市場規模への寄与は2030年までCAGR 17.9%で拡大すると予測されます。これらの企業は、ラックあたり100kWを超えるAIクラスターを構築しており、サーマルヘッドルームとPUEコンプライアンスにおいてリキッドテクノロジーの採用は必須となっています。このような企業の規模は、ラックあたりの冷却コストも引き下げるため、企業やエッジ事業者が模倣するベンチマークとなっています。しかし、エッジサイトでは、スペースとメンテナンスの制限から、コンパクトなリアドア式熱交換器が好まれています。ハイパースケーラの波は、空気式システムが後付けのニッチを維持しているとはいえ、液体インフラが新規容量増設の大半を占めることを確実にしています。

コロケーション事業者は、専用リキッドゾーンをプレミアムサービスとしてバンドルし、密度をマージンと差別化された顧客体験の両方に変換することで、この軌道を反映しています。企業施設では、完全液浸の採用は遅れているが、既存のチラープラントを拡張するために、ダイレクト・トゥ・チップ・ループを試験的に導入しています。このような動きを総合すると、各オペレーターセグメントがAI対応のサーマルアーキテクチャに向けて前進する中、中国のデータセンター冷却市場は高成長路線を維持していることになります。

成熟した設計フレームワークと稼働時間と設備投資の競合バランスにより、2024年の支出額の67.1%をティア3サイトが占める。しかし、Tier 4の構築はCAGR 19.2%で成長しています。これは、AIトレーニングのワークロードが数分の予定外のダウンタイムも許されないためです。したがって、ティア4施設の中国のデータセンター冷却市場規模は、投資家がフォールトトレラントで、メンテナンス中でもラックを30℃以内に保つ同時メンテナンス可能な液体システムを優先するため、急速に拡大します。

Tier 1とTier 2のフットプリントは、電力と冷却のエンベロープがラックあたり15kW以下になるにつれて、着実に縮小しています。一方、Tier 3仕様は、デュアルループの液体インフラで改修されつつあるため、事業者はTier 4の予算を新たに確保することなく、新たな顧客の密度要件を満たすことができます。このティアの進化は、中国のデータセンター冷却市場において、AI中心の構築のベースラインとして液体技術を強化するものです。

中国のデータセンター冷却市場は、データセンタータイプ(ハイパースケーラ(所有およびリース)、エンタープライズおよびエッジ、コロケーション)、ティアタイプ(ティア1および2、ティア3、ティア4)、冷却技術(空気ベース冷却、液体ベース冷却)、コンポーネント(サービス、機器)で区分されます。市場予測は金額(米ドル)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ハイパースケールとAI主導のラック密度の急増

- 新築物件に対する政府義務付けのPUE上限

- コロケーションの急速な拡大(ラックシェア前年比51.7%増)

- 成熟した液体冷却サプライチェーンと現地OEMのスケールアップ

- 寒冷地のフリークーリングゾーンを活用した東部データおよび西部コンピューティングプログラム

- サーバー廃熱を地域暖房グリッドに収益化する

- 市場抑制要因

- 高額な電気料金がTCOの優位性を損なっている

- 水ストレスの増大による蒸発冷却許可の抑制

- 地方の電力割当上限がハイパースケールプロジェクトの遅延を招いている

- フッ素系冷媒への輸入依存が関税リスクに直面

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済要因の市場への影響

第5章 市場規模と成長予測

- データセンタータイプ別

- ハイパースケーラー(所有およびリース)

- エンタープライズとエッジ

- コロケーション

- ティアタイプ別

- ティア1とティア2

- ティア3

- ティア4

- 冷却技術別

- 空気冷却

- チラーとエコノマイザー(DXシステム)

- コンピュータルーム空調機

- 冷却塔(直接冷却、間接冷却、2段冷却に対応)

- その他

- 液体ベースの冷却

- 浸漬冷却

- チップへの直接冷却

- リアドア熱交換器

- 空気冷却

- コンポーネント別

- サービス別

- コンサルティングとトレーニング

- インストールと展開

- メンテナンスとサポート

- 機器別

- サービス別

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Schneider Electric SE

- Johnson Controls International plc

- GIGA-BYTE Technology Co. Ltd.

- Vertiv Group Corp.

- Carrier Global Corporation

- Rittal GmbH and Co. KG

- Munters Group AB

- Stulz GmbH

- Kstar Science and Technology Co. Ltd.

- Alfa Laval AB

- Huawei Technologies Co. Ltd.

- Hangzhou Envicool Technology Co. Ltd.

- Shenzhen Yimikang Technology Co. Ltd.

- Inspur Group Co. Ltd.

- Lenovo Group Ltd.

- CoolIT Systems Inc.

- Asetek A/S

- Sugon(Dawning Information Industry)

- Midea Group Co. Ltd.(Clivet Division)

- Iceotope Technologies Ltd.