|

市場調査レポート

商品コード

1637858

アジア太平洋地域のデータセンター冷却:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)APAC Data Center Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域のデータセンター冷却:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

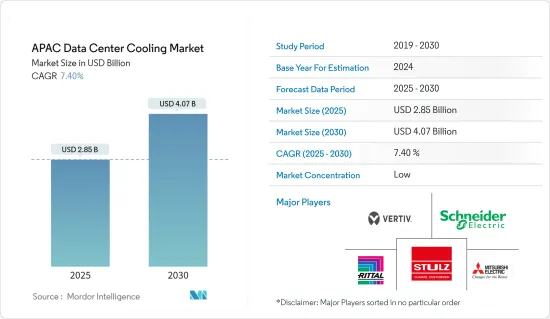

アジア太平洋地域のデータセンター冷却市場規模は、2025年に28億5,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは7.4%で、2030年には40億7,000万米ドルに達すると予測されます。

アジア太平洋地域(アジア太平洋地域)における人工知能(AI)およびメディア・アプリケーションによる膨大な計算要件に起因するインターネット利用およびデータセンター数の急増により、データセンター冷却市場は大規模な成長を遂げています。

国際エネルギー機関(IEA)によると、デジタルサービスへのニーズは継続的に高まっています。2010年以降、世界のインターネット・ユーザー人口はほぼ倍増し、世界のウェブ・トラフィックは20倍に増加しました。一方、エネルギー効率の大幅な向上により、データセンターとデータ・トランスミッション・システムによるエネルギー需要の増加は抑制されており、それぞれ世界の電力使用量の1~1.5%を占めています。2050年までのネット・ゼロ・シナリオを達成するために、今後10年間でエネルギー需要と排出量を大幅に削減するには、エネルギー効率、研究開発、電力供給とサプライチェーンの脱炭素化に関する政府と企業の多大な努力が必要です。

アジア太平洋地域の新興諸国におけるITインフラの開発が市場を促進しています。2022年10月に発表されたIEAのデータによると、アジアにおけるデータセンターのエネルギー需要は2019年の66TWhから2022年には72TWhに増加しました。

アジア太平洋地域地域の企業は、従来のエアコンの代わりに自由空冷システムを使用するグリーンデータセンターを設置することで、この問題に取り組もうとしています。情報の管理、保存、配信にグリーン・データセンターを導入する傾向が強まっており、多くのソフトウェア・ビジネスがエネルギー消費量と総エネルギー・コストの削減に貢献しています。

しかし、アジア太平洋地域における適応性の要求や停電は、市場成長の課題となっています。一般的なデータセンター冷却システムは、あらかじめ設計され、標準化され、モジュール化されていなければならないです。また、アジア太平洋地域のデータセンターの要件に適合する柔軟性と拡張性が求められます。ハイエンドでカスタマイズされた冷却システムにはあまりコストをかけず、コスト削減を目指す企業にとって、これは今日の課題となっています。

市場のプレーヤーは、より良い製品を顧客に提供するため、冷却液プロバイダーと協力しています。例えば、2023年8月、シンガポールのSK Enmoveは、デルおよび液浸冷却のエキスパートであるGRCと提携し、冷却液の提供を開始しました。この潤滑会社は液浸冷却に進出しています。デルのキットを収納し、サーバー・メーカーが供給・サポートするGRCの浴槽に充填する誘電冷却剤を提供します。SK Enmove社は、高品質の潤滑油ベースオイルをベースにした特殊な冷却液を開発し、デルとGRC社は、液浸冷却用に設計されたサーバー設計と浴槽を製造します。

アジア太平洋地域のデータセンター冷却市場動向

情報技術産業が最も高い成長を遂げる

情報技術(IT)産業は、様々な産業において変革的な進歩をもたらしてきました。IT技術革新によって著しい成長を遂げた分野の1つが、研究市場です。

さらに、アジア太平洋地域はこの分野で著しい成長を遂げています。テクノロジーとデジタルトランスフォーメーションの盛んな需要拠点として、IT部門は課題に立ち上がり、調査市場の開拓を新たな高みへと押し上げています。

SaaSプロバイダーの拡大によりクラウドストレージ・プロバイダーの容量拡大が可能になったため、クラウドストレージの利用は年々拡大しており、データセンター冷却システムの需要が高まる可能性が高いです。マイクロソフト、AWS、グーグルなどのクラウドストレージ企業は、より効率的なクラウドワークフローを実現するため、ストレージ容量を拡大しています。これらの企業は、ハイパースケール取引に投資しています。

データ駆動型技術、クラウド・コンピューティング、人工知能、(IoT)が進化を続ける中、データセンターの需要は急増しています。企業はデジタル・フットプリントを拡大し、より大規模なデータセンターや、さまざまな地域に分散した複数の小規模な施設を必要としています。この成長により、こうした広大なインフラの冷却ニーズを管理する上で新たな課題が浮上しています。

中国が大きな市場シェアを獲得する見込み

データセンター冷却は、アジア太平洋地域のデータセンター・インフラの成長、デジタル・サービスの導入拡大、クラウド・コンピューティングの台頭により、急速に拡大している市場です。データセンターのニーズは大幅に増加しており、その有効性と最大稼働時間が重視されています。

中国は、データセンターの建設で世界の競合他社を追い越すべく力を入れています。5G、ウェアラブル技術、モノのインターネット(IoT)、人工知能の利用は、データ・サービスの安定性と信頼性を保証するために大規模な組織がデータ・センターの規模を拡大しようとしているため、処理能力に対する需要が急増しています。

アクセラレーター・プロセッサーは、人工知能やそれに匹敵するワークロードが多くの中国産業で一般的になるにつれて、エンタープライズ・データセンターに参入しています。待ち時間の影響を受けやすいサービスはすべて、情報を迅速に処理するためにアクセラレーター・システムを使用するゼロ・レイテンシー・テクノロジーを求めています。こうしたハードウェア・アクセラレーターの冷却要件は相当なもので、200Wからそれ以上の幅があります。強力なサーバーと組み合わせると、1台のマシンの冷却要件は1kW近くになることもあります。この地域のデータセンターでは、液浸冷却技術の使用が増加しています。

マイクロソフト・アジュールとアマゾン・ウェブ・サービスは、大規模な世界・クラウド・データセンター・ネットワークを構築しています。中国最大のeコマース企業のクラウド・コンピューティング部門であるアリババ・グループは、こうした進歩に対抗するため、サーバーのマザーボードを液体冷却液に浸すデータセンター冷却ソリューションを採用しています。この技術では、液体が空気よりも効果的に熱を運ぶことを利用しています。液浸冷却ソリューションのエネルギー効率向上により、データセンターの運営費は20%減少しました。

アジア太平洋地域のデータセンター冷却産業の概要

アジア太平洋地域のデータセンター冷却市場は細分化されており、技術によってもたらされる利点や、データセンターに効率化規制を課すことによる政府からの援助が、データセンター冷却市場の成長に直接貢献すると予想されています。既存市場では大手企業の存在感が強く、市場への浸透が進んでいます。技術革新への注目が高まるにつれ、新技術への需要が高まり、それがさらなる開発のための投資を促進しています。主要企業は、Vertiv Co.、Schneider Electric SE、STULZ GMBHなどです。

2024年5月、リタールは複数のハイパースケーラーと共同でモジュール式冷却システムを開発しました。このソリューションは、直接水冷により1MWを超える冷却能力を誇る。AIアプリケーションの高電力密度に対応するよう特別に調整されています。

バーティブは2024年4月、AIに取り組む企業向けに特化した高密度データセンター・インフラストラクチャ・ソリューションの最新ラインアップを発表しました。Vertiv 360AIシリーズは、AI主導のデータセンターで増大する冷却と電力需要に対応するよう設計されています。

2024年3月、リタール・プライベート・リミテッドはインドのバンガロール製造工場に、冷却ユニットと液体冷却パッケージ(LCP)ソリューションに特化した新しいインテグレーションセンターを開設しました。この戦略的な動きにより、リタールの生産能力が強化され、産業用冷却ソリューションの需要拡大に対応できる体制が整いました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要(対象範囲:データセンター冷却に関連する現在の地域動向の詳細な分析を含みます。)

- 冷却に関する主要コストの考察

- DCクーリングに注目したDC運用に関連する主要コスト諸経費の分析

- データセンター冷却における主な技術革新と発展

- データセンターで採用されている主なエネルギー効率化手法

第5章 市場力学

- 市場促進要因(エネルギー消費重視の高まり、グリーンソリューションへの移行などの主要要因を、今後5~7年間の相対的影響に基づいてマッピング)

- 市場力学(規制のダイナミックな性質、顧客ニーズの進化などの主要因を、今後5~7年間の相対的影響に基づいてマッピング)

- 市場機会

- 封じ込め付きレイズドフロアと封じ込めなしレイズドフロアの比較

- 産業エコシステム分析

第6章 地域別データセンターのフットプリントの現状分析

- データセンターのIT負荷容量と面積フットプリントの地域分析(2017年~2030年の期間)

- アジア太平洋地域地域における確立されたDC市場と新興DCホットスポットの地域分析(主要な確立されたDC市場と新興DC市場にスポットを当ててカバレッジを含める予定です)

- DC冷却に関する規制枠組みの地域分析

第7章 データセンター冷却市場のセグメンテーション

- 冷却技術別(主要動向、2022~2029年の市場規模推計・予測、将来展望)

- エアベース冷却

- CRAH

- チラーとエコノマイザー

- 冷却塔(直接冷却、間接冷却、2段階冷却をカバー)

- その他

- 液体冷却

- 液浸冷却

- 直接チップ冷却

- リアドア式熱交換器

- エアベース冷却

- エンドユーザー業界別

- IT&テレコム

- 小売・消費財

- ヘルスケア

- メディア&エンターテインメント

- 連邦政府機関

- その他エンドユーザー

- 国別

- 中国

- インド

- 日本

- オーストラリア

- ニュージーランド

- シンガポール

- 韓国

- マレーシア

- インドネシア

- フィリピン

- 台湾

- 香港

- タイ

- ベトナム

第8章 競合情勢

- 企業プロファイル

- Vertiv Group Corp.

- Stulz GmbH

- Schneider Electric SE

- Rittal Gmbh & Co. KG

- Mitsubishi Electric Corporation

- Johnson Controls Inc.

- Munters Group

- Eaton Corporation plc

- Daikin Industries Limited

- Asetek A/S

第9章 投資分析

第10章 市場機会と今後の動向

The APAC Data Center Cooling Market size is estimated at USD 2.85 billion in 2025, and is expected to reach USD 4.07 billion by 2030, at a CAGR of 7.4% during the forecast period (2025-2030).

Due to the surge in Internet usage and the number of data centers due to enormous computational requirements by artificial intelligence (AI) and media applications in Asia-Pacific (APAC), the data center cooling market has had massive growth.

According to the International Energy Agency (IEA), the need for digital services is continuously increasing. Since 2010, the global population of internet users has nearly doubled, while global web traffic has increased 20-fold. On the other hand, significant advances in energy efficiency have helped to restrain the increase in energy demand from data centers and data transmission systems, each contributing to 1-1.5% of worldwide power use. Substantial government and business efforts on energy efficiency, research and development, and decarbonizing power supply and supply chains are required to cut energy demand and emissions significantly over the next decade to meet the Net Zero by 2050 Scenario.

Development in IT Infrastructure in emerging countries of APAC is propelling the market. The data center energy demand increased from 66 TWh in 2019 to 72 TWh in 2022 in Asia, according to IEA data released in October 2022.

Companies in the APAC region are trying to tackle this issue by setting up Green data centers that use Free air cooling systems instead of traditional Air conditioners. The increasing trends toward deploying green data centers for managing, storing, and distributing information have helped many software businesses decrease energy consumption and total energy costs.

However, adaptability demands and power outages in Asia-Pacific are a challenge to the growth of the market. A typical data center cooling system must be pre-engineered, standardized, and modular. It is expected to be flexible and scalable to match the data center's requirements in the region. This is challenging today, with firms looking to lower costs and not spend much on high-end customized cooling systems.

The players in the market are collaborating with cooling fluids providers to provide better products to their customers. For instance, in August 2023, Singapore's SK Enmove partnered with Dell and immersion cooling expert GRC to provide cooling fluids. The lubrication company is moving into immersion cooling. It will provide dielectric coolants to fill GRC's tubs, which will hold the Dell kit and be supplied and supported by the server maker. SK Enmove will develop specialized cooling fluids based on its high-quality lube base oil, while Dell and GRC will produce server designs and tubs designed for immersion cooling.

APAC Data Center Cooling Market Trends

Information Technology Industry to Witness Highest Growth

The Information Technology (IT) vertical has driven transformative advancements in various industries. One area that has witnessed remarkable growth due to IT innovation is the market studied.

Moreover, Asia-Pacific is experiencing significant growth in this segment. As a thriving demand hub for technology and digital transformation, the IT sector has risen to the challenge, propelling the development of the market studied to new heights.

Cloud storage use has expanded over the years as SaaS provider expansion has enabled cloud storage providers to expand their capacity, which is likely to raise demand for data center cooling systems. Cloud storage companies like Microsoft, AWS, and Google are expanding their storage capacity to enable more efficient cloud workflow. These firms are investing in hyperscale transactions.

As data-driven technologies, cloud computing, artificial intelligence, and (IoT) continue to evolve, the demand for data centers has skyrocketed. Companies are expanding their digital footprints, requiring larger data centers or multiple smaller facilities spread across various regions. This growth has introduced new challenges in managing the cooling needs of these sprawling infrastructures.

China is Expected to Witness Significant Market Share

Data center cooling is a market that is expanding quickly in Asia-Pacific due to the region's growing data center infrastructure, rising adoption of digital services, and the emergence of cloud computing. The need for data centers is increasing significantly and placing a greater emphasis on effectiveness and maximum uptime.

China is putting much effort toward overtaking its competitors globally in the construction of data centers. The use of 5G, wearable technology, the Internet of Things (IoT), and artificial intelligence generates a booming demand for processing capacity as larger organizations attempt to scale up their data centers to assure the stability and reliability of data services.

Accelerator processors are entering the enterprise data center as artificial intelligence and comparable workloads become commonplace in numerous Chinese industries. All latency-sensitive services demand zero-latency technologies that use accelerating systems to handle information rapidly. The cooling requirements for these hardware accelerators are considerable and range from 200 W to more. The cooling requirements of a single machine can be almost 1 kW when paired with a powerful server. In the region's data centers, this has increased the use of immersion cooling technologies.

Microsoft Azure and Amazon Web Services are constructing massive global cloud data center networks. Alibaba Group, the cloud computing division of China's largest e-commerce company, uses a data center cooling solution that submerges server motherboards in liquid coolant to compete with these advancements. This technique makes use of liquid's more effective ability to transport heat than air. The energy efficiency enhancements of the immersion cooling solution led to a 20% decrease in data center operating expenses.

APAC Data Center Cooling Industry Overview

The Asia-Pacific data center cooling market is fragmented as the advantages offered by the technology and aid from the government by imposing efficiency regulations on data centers are expected to help the growth of the data center cooling market directly. Market penetration is growing with a strong presence of major players in established markets. With the increasing focus on innovation, the demand for new technologies is growing, which, in turn, is driving investments for further developments. Key players are Vertiv Co., Schneider Electric SE, STULZ GMBH, etc.

In May 2024, Rittal developed a modular cooling system in collaboration with multiple hyperscalers. This solution boasts a cooling capacity exceeding 1 MW, achieved through direct water cooling. It's specifically tailored to cater to the high power densities of AI applications.

In April 2024, Vertiv unveiled its latest lineup of high-density data center infrastructure solutions tailored specifically for enterprises delving into AI. The Vertiv 360AI series is crafted to cater to AI-driven data centers' augmented cooling and power demands.

In March 2024, Rittal Private Limited marked the opening of its new Integration Centre, specifically tailored for Cooling Units and Liquid Cooling Package (LCP) solutions, at its Bangalore, India manufacturing plant. This strategic move bolsters the company's production capabilities and positions it to cater to the escalating demand for Industrial Cooling Solutions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview (Coverage: A detailed analysis of the current regional trends related to Data Center Cooling are included in this section)

- 4.2 Key cost considerations for Cooling

- 4.2.1 Analysis of the key cost overheads related to DC operations with an eye on DC Cooling

- 4.2.2 Key innovations and developments in Data Center Cooling

- 4.2.3 Key energy efficiency practices adopted in Data Centers

5 MARKET DYNAMICS

- 5.1 Market Drivers (Key factors such as the increased emphasis on energy consumption, move towards green solutions are mapped based on their relative impact over the next 5-7 years)

- 5.2 Market Challenges (Key factors such as the dynamic nature of regulations, evolving customer needs are mapped based on their relative impact over the next 5-7 years)

- 5.3 Market Opportunities

- 5.4 Comparison of raised floor with containment & raised floor without commitment

- 5.5 Industry Ecosystem Analysis

6 ANALYSIS OF THE CURRENT REGIONAL DATA CENTER FOOTPRINT

- 6.1 Regional Analysis of IT Load Capacity & Area Footprint of Data Centers (for the period of 2017-2030)

- 6.2 Regional Analysis of the Established DC Markets and Emerging DC Hotspots in APAC region (we will include coverage by highlighting major established and emerging DC markets)

- 6.3 Regional Analysis of Regulatory Framework On DC Cooling

7 DATA CENTER COOLING MARKET SEGMENTATION

- 7.1 By Cooling Technology (Key trends, market size estimates & projections for the period of 2022-2029 and future outlook)

- 7.1.1 Air-based Cooling

- 7.1.1.1 CRAH

- 7.1.1.2 Chiller and Economizer

- 7.1.1.3 Cooling Tower (covers direct, indirect & two-stage cooling)

- 7.1.1.4 Others

- 7.1.2 Liquid-based Cooling

- 7.1.2.1 Immersion Cooling

- 7.1.2.2 Direct-to-Chip Cooling

- 7.1.2.3 Rear-Door Heat Exchanger

- 7.1.1 Air-based Cooling

- 7.2 By End-user Vertical

- 7.2.1 IT & Telecom

- 7.2.2 Retail & Consumer Goods

- 7.2.3 Healthcare

- 7.2.4 Media & Entertainment

- 7.2.5 Federal & Institutional agencies

- 7.2.6 Other end-users

- 7.3 By Country

- 7.3.1 China

- 7.3.2 India

- 7.3.3 Japan

- 7.3.4 Australia

- 7.3.5 New Zealand

- 7.3.6 Singapore

- 7.3.7 South Korea

- 7.3.8 Malaysia

- 7.3.9 Indonesia

- 7.3.10 Philippines

- 7.3.11 Taiwan

- 7.3.12 Hong Kong

- 7.3.13 Thailand

- 7.3.14 Vietnam

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Vertiv Group Corp.

- 8.1.2 Stulz GmbH

- 8.1.3 Schneider Electric SE

- 8.1.4 Rittal Gmbh & Co. KG

- 8.1.5 Mitsubishi Electric Corporation

- 8.1.6 Johnson Controls Inc.

- 8.1.7 Munters Group

- 8.1.8 Eaton Corporation plc

- 8.1.9 Daikin Industries Limited

- 8.1.10 Asetek A/S