米国の石油・ガス下流-市場シェア分析、産業動向、成長予測(2025年~2030年)

United States Oil And Gas Downstream - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 70 Pages

- 納期

- 2~3営業日

- 商品コード

- 1640411

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

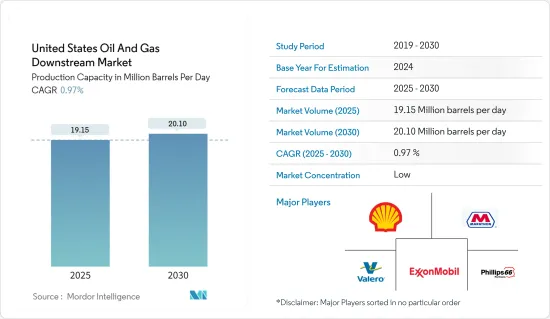

米国の石油・ガス下流市場規模は生産能力ベースで、予測期間(2025~2030年)のCAGR0.97%で、2025年の日量1,915万バレルから2030年には日量2,010万バレルに成長すると予測されます。

米国の石油・ガス下流市場は、予測期間中にCAGR 0.92%を記録すると予想されます。

主要ハイライト

- 中期的には、石油製品需要の増加、製油所への今後の投資といった要因が、予測期間中の米国の石油・ガス下流市場を牽引するとみられます。

- 一方、再生可能エネルギーのようなクリーンエネルギー技術の採用は、電力セクターに大きな影響を与え、石油・天然ガス産業に今後数年間の影響を与えると予想されます。

- 国際エネルギー機関(IEA)によれば、石油化学は2050年までに世界の石油需要の中で唯一成長するセグメントになると予想されています。さらに、米国では予測期間中にいくつかの石油化学プロジェクトが稼動すると予想されています。したがって、石油化学部門は、同国の下流企業にとって大きな成長機会となることが期待されます。

米国の石油・ガス下流市場動向

精製部門は緩やかな成長を記録

- 米国では最近、エネルギー需要が拡大しています。この需要の伸びは、先進国における人口の増加と生活水準の向上に起因しています。新エネルギーや再生可能エネルギーが国内で人気を集めている石油燃料は依然として世界的に主要なエネルギー源です。この動向は今後数十年間続くと予想され、石油産業のすべてのセクターに恩恵をもたらします。

- 産業活動の活発化と経済成長は、石油精製産業を支えると考えられます。マサチューセッツ州、コネティカット州、ミネソタ州などの先進国では、ディーゼルやその他の留分の需要が今後数年間堅調に推移すると予想されます。こうした需要の伸びは、これらの国々の製油所産業が好調であることに起因しています。

- 米国メキシコ湾岸地域では、予測期間中、下流事業への新たな投資の波が押し寄せると予想されます。さらに、米国のシェール生産量はシェール革命が始まって以来ほぼ倍増しており、今後もさらに増加すると予想されます。

- 2023年時点で、米国の精製能力は日量1,842万バレルに達しています。継続的な投資と高い競合により、米国の精製処理能力は2023年に2%の割合で増加します。

- 2023年現在、米国には操業可能な石油精製所が132カ所あります。米国で最も新しい製油所はテキサス州チャネルビューのTexas International Terminals製油所4万5,000b/cdで、2022年1月1日に操業可能となったが、実際には2022年2月に操業を開始しました。

- Element Fuels Holdingsは2024年6月、日量5万~5万5,000バレル規模の製油所建設を提案しました。同社は開発の初期段階で約12億米ドルの投資を見込んでいます。

- このようなプロジェクトとは別に、国内の石油需要は年々増加しています。例えば、2023年の石油需要は1%近く増加し、日量約2万360バレルとなりました。同様に、前年も石油需要の伸びが見られました。

- したがって、石油需要の増加は、精製部門への今後の投資とともに、予測期間には緩やかな成長が見込まれます。

石油製品需要の増加

- 石油には、ガソリン、ディーゼル燃料、ジェット燃料、未精製油などの石油精製製品や、燃料用エタノール、ガソリン用混合成分、その他の精製投入物などの液体が含まれます。

- 米国は消費する石油の大部分を生産しているが、増加する需要を満たすには依然として輸入に頼っています。他国からの輸入は、国内の石油需要を満たすのに役立っています。エネルギー情報庁によると、2023年に同国が輸入した原油と製品は日量852万6,000バレルで、前年比約2.3%増となりました。

- そのうち6,133万8,000バレルの石油製品が輸入されました。天然ガス液体が367万バレル、完成ガソリンが329万4,000バレル、残りは灯油、重油、軽油などです。

- 輸入に加えて、同国は石油製品の生産量を継続的に増やしています。2023年の石油製品生産量は、2022年の1,939万バレル/日から1,943万バレル/日に増加しました。さらに、今後数年間は、輸送や産業などのセグメントでの消費の増加により、石油製品の需要が増加する可能性が高いです。

- 2023年、米国では乗用車の販売台数が約9%増加します。2022年には285万台だった乗用車販売台数は、2023年には311万台に増加しました。人口と所得の増加に伴い、乗用車の販売台数は増加する可能性が高く、その結果、同国における石油製品の需要が増加します。

- さらに、航空と鉄道という2つの輸送産業があり、これらの拡大が石油製品の消費をさらに増加させる可能性があります。

- したがって、このようなシナリオは、今後数年間、米国の石油・ガス下流市場を牽引すると予想されます。

米国の石油・ガス下流産業概要

米国の石油・ガス下流市場は、Marathon Petroleum Corp.、Chevron Corporation、Valero Energy Corporation、Exxon Mobil Corporation、Phillips 66、Royal Dutch Shell PLCなど(順不同)多数の主要企業が参入しており、半分裂状態となっています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 市場の定義

- 調査の前提

- 調査の成果

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの精製能力(100万バレル/日)と予測

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 石油製品需要の増加

- 精製部門への今後の投資

- 抑制要因

- クリーンエネルギー技術の採用

- 促進要因

- PESTLE分析

- 投資分析

第5章 セクター別市場セグメンテーション

- 精製

- 石油化学

第6章 競争情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Marathon Petroleum Corp.

- Phillips 66

- Valero Energy Corporation

- Exxon Mobil Corporation

- Shell Plc

- Hunt Refining Company

- U.S. Oil & Refining Co.

- その他の著名な企業一覧

- 市場ランキング分析

第7章 市場機会と今後の動向

- 複数の産業における石油化学製品の需要

目次

The United States Oil And Gas Downstream Market size in terms of production capacity is expected to grow from 19.15 million barrels per day in 2025 to 20.10 million barrels per day by 2030, at a CAGR of 0.97% during the forecast period (2025-2030).

The United States oil and gas downstream market is expected to register a CAGR of 0.92% during the forecast period.

Key Highlights

- Over the medium term, factors such as increasing petroleum products demand, and upcoming investment in oil refineries are likely to drive the United States oil and gas downstream market during the forecast period.

- On the other hand, adopting clean energy technology, like renewables, is expected to significantly influence the power sector, thus impacting the oil and natural gas industry in the upcoming years.

- Nevertheless, according to the International Energy Agency, petrochemicals are expected to become the only growing segment of global oil demand by 2050. Moreover, several petrochemical projects are expected to come online in the United States during the forecast period. Hence, the petrochemical sector is expected to present a huge growth opportunity for the downstream players in the country.

US Downstream Oil and Gas Market Trends

Refining Sector to Register a Modest Growth

- The United States has been witnessing growing energy demand in recent days. This growth in demand can be attributed to the growing population and an improvement in living standards in the developed states. Even though new and renewable energy sources are gaining popularity around the country, petroleum fuel remains a major energy source globally. This trend is expected to continue for the next few decades and benefit all sectors of the petroleum industry.

- Increasing industrial activity and economic growth are likely to support the refining industry. In developed states such as Massachusetts, Connecticut, and Minnesota, the demand for diesel and other distillates is expected to be robust in the coming years. This demand growth can be attributed to the strong refinery industry in these countries.

- The United States Gulf Coast region is expected to witness a fresh wave of investment in the downstream business during the forecast period. In addition, the United States' shale production has almost doubled since the shale revolution started and is expected to increase further.

- As of 2023, the refining capacity of the United States stood at 18.42 million barrels per day. With continuous investments and high competition, the refining throughput of the United States increased at a rate of 2% in 2023.

- As of 2023, there were 132 operable petroleum refineries in the United States. The newest refinery in the United States is the Texas International Terminals 45,000 b/cd refinery in Channelview, Texas, which was operable on January 1, 2022, but actually started operating in February 2022.

- In the June 2024, Element Fuels Holdings proposed to build a refinery with a capacity of around 50,000 to 55,000 barrels per day. The company estimatewd to have an investment of around USD 1.2 billion in the initial phase of development.

- Apart from such projects, demand for oil in the country is increasing over the years. For instance, in 2023, the oil demand increased by nearly 1% to around 20.36 thousand barrels per day. Similarly, in the previous year, the country witnessed growth in oil demand.

- Hence, increased in oil demand, along with upcoming investment in the refining sector is expected to have a moderate growth in the forecast period.

Increasing Demand for Petroleum Products

- Petroleum includes refined petroleum products, such as gasoline, diesel fuel, jet fuel, unfinished oils, and other liquids, such as fuel ethanol, blending components for gasoline, and other refinery inputs.

- The United States produces a large share of the petroleum it consumes, but the country still relies on imports to meet the increasing demand. Imports from other countries help to meet the domestic demand for petroleum. According to the Energy Information Agency, in 2023, the country imported 8526 thousand barrels per day of crude oil and products, an increase of around 2.3% as compared to the previous year.

- Among all, 61338 thousand barrel of petrolume producst were imported. 3670 thousand barrels were natural gas liquids, 3294 thousand barrels were finished motor gasoline, and rest were kerosene, fuel oil, diesel fuel, etc.

- In addition to imports, the country is continously increasing its petroleum products output. In 2023, petroleum products output increased to 19.43 million barrels per day, from 19.39 million barrels per day in 2022. Further, in the upcoming years, the demand for petroleum products are likley to increase due to increasing consumption in sectors like transportation, and industries.

- In 2023, the United States witnessed increased in sales of passenger vahicles by around 9%. From 2.85 million in 2022, the passenger vehicle sales increased to 3.11 million in 2023. With increase in population, and income, sales of such vehicles are likley to increase, thus increasing demand for petroleum products in the country.

- In addition, aviation and railway are another two transportation industry, expantion of which is further likely to increase consumption of petrioleum products.

- Hence, such a scenario is expected to drive the United States oil and gas downstream market in the upcoming years.

US Downstream Oil and Gas Industry Overview

The market for United States oil and gas downstream market is semi-fragmented, with a number of key players, including (in no particular order) Marathon Petroleum Corp., Chevron Corporation, Valero Energy Corporation, Exxon Mobil Corporation, Phillips 66, and Royal Dutch Shell PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition

- 1.2 Study Assumptions

- 1.3 Study Deliverables

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Refining Capacity and Forecast in million barrels per day, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand for Petroleum Products

- 4.5.1.2 Upcoming Investment in the Refining Sector

- 4.5.2 Restraints

- 4.5.2.1 Adoption of Clean Energy Technology

- 4.5.1 Drivers

- 4.6 PESTLE Analysis

- 4.7 Investment Analysis

5 MARKET SEGMENTATION BY SECTOR

- 5.1 Refining

- 5.2 Petrochemical

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Marathon Petroleum Corp.

- 6.3.2 Phillips 66

- 6.3.3 Valero Energy Corporation

- 6.3.4 Exxon Mobil Corporation

- 6.3.5 Shell Plc

- 6.3.6 Hunt Refining Company

- 6.3.7 U.S. Oil & Refining Co.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Demand for Petrochemical in Several Industries

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 70 Pages

- 納期

- 2~3営業日