石油・ガス下流- 市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Oil & Gas Downstream - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1630327

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

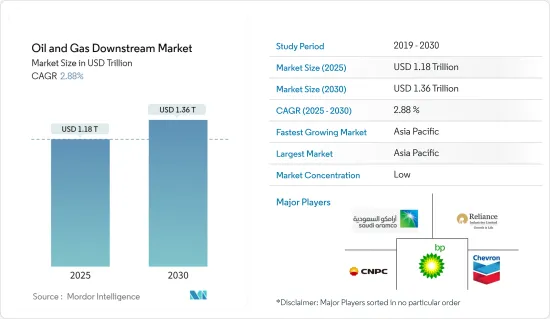

石油・ガス下流市場規模は2025年に1兆1,800億米ドルと推定・予測され、予測期間中(2025~2030年)のCAGRは2.88%で、2030年には1兆3,600億米ドルに達すると予測されます。

主要ハイライト

- 中期的には、アジア太平洋と中東全域での精製能力の増加や新興諸国での工業化の進展といった要因が、予測期間中の石油・ガス下流市場を牽引すると予想されます。

- 先進国と新興経済諸国における低燃費車のシェア拡大や電気自動車の普及拡大は、予測期間中の市場開拓の妨げになると予想されます。

- 精製・石油化学部門のデジタル化と近代化により、精製コストとプロセスロスの削減が期待されます。このことは、予測期間中、市場に機会をもたらすと予想されます。

- 石油・ガス下流市場はアジア太平洋が支配的で、需要の大半は中国、東南アジア、インドからもたらされています。

石油・ガス下流市場の動向

製油所セグメントが市場を独占する見込み

- 製油所は、原油を加工してガソリン、ディーゼル、ジェット燃料、暖房油、石油化学製品などの精製製品に変換する産業施設です。製油所は石油・ガス産業の下流部門において、エネルギーや化学製品の需要を満たす精製製品を供給する重要な役割を担っています。

- 製油所は、石油生産地、主要航路、主要需要地の近くに戦略的に配置されています。北米、欧州、アジア太平洋、中東・アフリカなどの地域に重要な精製拠点が存在します。

- さらに、各国は処理能力を高めるために製油所の強化に力を入れています。例えば、Energy Institute Statistical Review of World Energyによると、2023年にはアジア太平洋が世界の精製能力の36.2%近くを占めるのに対し、北米は21.2%です。

- 複数の企業が既存の製油所に投資し、精製能力を増強しています。例えば、タイ石油公社は2023年3月、シラチャ製油所の精製能力を現在の280kb/dから400kb/d増強する計画を発表しました。このプロジェクトは2025年までに約5億米ドルで完成する予定です。

- また、複数の企業が世界各地で製油所の建設に投資しています。例えば、2023年4月、インド大使は最近、インドの援助を受けて建設中のモンゴル初の石油精製所が2025年までに完成する見込みであることを発表しました。このプロジェクトは12億米ドルのインドのソフトローンで資金を調達しており、モンゴル製油所の第一段階は2023年末までに完成する予定です。製油所の処理能力は年間約150万トンとなります。

- さらに2023年3月、タイ・オイルは事業成長のために2023~2025年の間に10億米ドルを資本投資する計画を発表しました。その中には、製油所の能力を拡大し、クリーン燃料プロジェクト(CFP)戦略の一環としてより付加価値の高い燃料製品に移行するための5億米ドルが含まれています。同事業は、シラチャ(タイ)の製油所能力を従来の280kb/dから400kb/dに拡大し、燃料油をディーゼルやジェット燃料などの高付加価値製品に改良する予定です。

- 多くの国の政府も、製油所の新設にいくつかのイニシアチブを取りました。例えば、インド政府は2023年2月、HPPCLラジャスタン製油所(HRRL)プロジェクトを2024年1月までに完成させ、2024年までに完全稼働させる予定であると発表しました。エネルギー相によると、政府はナレンドラ・モディ首相に2024年1月の製油所開所を要請する予定です。

- したがって、既存の製油所の精製能力を高め、新たな製油所を設立することが、石油・ガス下流部門の成長を世界的に確認することになると予想されます。

アジア太平洋が市場を独占する見込み

- アジア太平洋の石油・ガス下流市場は、同地域の新興経済国におけるエネルギー需要の増加に牽引され、力強い成長を遂げています。人口増加と工業化に伴い、中国やインドのような国々ではエネルギー消費が急増し、精製能力の拡大、既存精製所の近代化、石油化学コンビナートの開発など、川下セグメントへの投資が活発化しています。

- 世界エネルギー統計によると、2023年にはアジア太平洋の石油精製能力は日量3,740万バレルに達します。2023年時点で、インドは世界の石油精製能力のほぼ4.9%を占めています。石油精製製品に対する需要の高まりは、川下企業に新規プロジェクトへの投資や既存施設の拡大を促しています。

- 例えば2023年9月、インド首相はBharat Petroleum Corp Ltd(BPCL)の製油所拡大とBinaにおけるグリーンフィールド石油化学プロジェクトの礎石を据えました。この拡大プロジェクトにより、BPCLの精製能力は780万トン/年から1,100万トン/年に増加する見込みです。また、220万トン/年以上の石油化学製品を生産する製造コンプレックスも建設されます。このプロジェクトの費用は59億米ドルです。

- 2023年時点で、中国は世界の石油精製能力の17.9%を占めています。予測期間中、同国の石油化学・精製部門はプラスに転じると予想されます。

- 2023年3月、Saudi Aramcoと中国のパートナーは、同国の石油化学と燃料の需要増に対応するため、2026年に中国北東部の石油化学・製油所プロジェクトの全運転開始を目指すと発表しました。遼寧省磐津市でのプロジェクトは100億米ドルを要する見込みで、Aramcoにとって中国で2番目の大規模な石油精製・石油化学投資となります。

- さらに2023年3月には、韓国を拠点とするロッテグループの子会社であるロッテケミカル・インドネシアが、インドネシアのバンテン州に石油化学コンプレックスを建設するための資金調達に成功しました。LINEと呼ばれるこのプロジェクトは、PT Lotte Chemical Indonesiaにとって総額39億米ドルの重要な投資です。2025年の完成時には、LINE石油化学コンプレックスは年間100万トンのエチレンと52万トンのプロピレンの製造能力を持つことになります。

- 石油・ガス川下市場は、石油精製・石油化学部門への投資の増加と、各国の既存川下インフラの拡大により、予測期間中、この地域が支配的な地位を占めると予想されます。

石油・ガス下流産業概要

石油・ガス下流市場は適度にセグメント化されています。同市場の主要企業には、Reliance Industry Limited、BP PLC、Saudi Aramco、China National Petroleum Corporation、Chevron Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 石油・ガス生産シナリオ(2013~2029年)

- 石油・ガス消費シナリオ(2013~2029)

- 製油所の処理能力(2013~2029年)

- 主要プロジェクト情報

- 既存プロジェクト

- 進行中のプロジェクト

- 今後のプロジェクト

- 原油価格動向分析(2013~2023年)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- ドライバー

- アジア太平洋と中東における精製能力の増加

- 新興諸国における工業化の進展

- 抑制要因

- 電気自動車の普及拡大

- ドライバー

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- タイプ

- 製油所

- 石油化学プラント

- 市場分析:地域別(2029年までの市場規模と需要予測)

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- フランス

- イタリア

- ドイツ

- 英国

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- インドネシア

- 日本

- 韓国

- マレーシア

- タイ

- ベトナム

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Reliance Industries Ltd

- Royal Dutch Shell PLC

- The Dow Chemical Company

- BP PLC

- Saudi Aramco

- Indian Oil Corporation Limited

- China National Petroleum Corporation

- Total SA

- Chevron Corporation

- List of Other Prominent Companies

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 精製・石油化学セクターのデジタル化と近代化

目次

Product Code: 68192

The Oil & Gas Downstream Market size is estimated at USD 1.18 trillion in 2025, and is expected to reach USD 1.36 trillion by 2030, at a CAGR of 2.88% during the forecast period (2025-2030).

Key Highlights

- In the medium term, factors such as increasing refining capacity across Asia-Pacific and the Middle East and rising industrialization in developing countries are expected to drive the oil and gas downstream market during the forecast period.

- The growing share of fuel-efficient vehicles and increasing penetration of electric vehicles in developed and emerging economies are expected to hinder the market's growth during the forecast period.

- Nevertheless, digitalization and modernization of the refining and petrochemical sectors are expected to reduce refining costs and process losses. This, in turn, is expected to create an opportunity for the market during the forecast period.

- Asia-Pacific has dominated the oil and gas downstream market, with the majority of the demand coming from China, Southeast Asia, and India.

Oil & Gas Downstream Market Trends

The Refineries Segment is Expected to Dominate the Market

- Refineries are industrial facilities where crude oil is processed and converted into refined products such as gasoline, diesel, jet fuel, heating oil, and petrochemicals. Refineries play a critical role in the downstream sector of the oil and gas industry by supplying refined products to meet energy and chemical demands.

- Refineries are located strategically near oil production regions, major shipping routes, and key demand centers. Significant refining hubs exist in regions such as North America, Europe, Asia-Pacific, and the Middle East and Africa.

- Further, countries are focused on enhancing their refineries to increase the throughput. For instance, according to the Energy Institute Statistical Review of World Energy, in 2023, Asia-Pacific holds nearly 36.2% of the global refining capacity, whereas North America has 21.2%.

- Several companies are investing in the existing refineries to increase their refining capacity. For instance, in March 2023, Thai Oil Public Company Limited announced that it plans to increase the refining capacity in the Sriracha refinery by 400 kb/d from the current 280 kb/d. The project is expected to be completed by 2025 at approximately USD 500 million.

- Several companies are also investing in the construction of refineries in many regions across the world. For instance, in April 2023, the Indian Ambassador recently announced that Mongolia's first oil refinery, which is being built with Indian assistance, is expected to be completed by 2025. The project is being funded through a USD 1.2 billion Indian soft loan, and the first stage of the Mongol Oil Refinery is set to be completed by the end of 2023. The refinery will have approximately 1.5 million metric tons of processing capacity annually.

- Further, in March 2023, Thai Oil announced plans to invest USD 1 billion in the capital between 2023 and 2025 to grow its business, including USD 500 million to expand its refinery capacity and transition to higher added-value fuel products as part of its Clean Fuel Project (CFP) strategy. The business intends to expand its oil refinery capacity in Sriracha (Thailand) to 400 kb/d, up from 280 kb/d, and upgrade fuel oil to higher-value products such as diesel and jet fuel.

- Governments in many countries also took several initiatives to establish new refineries. For instance, in February 2023, the Government of India announced that the HPPCL Rajasthan Refinery (HRRL) project is anticipated to be completed by January 2024 and be completely operational by 2024. According to the energy minister, the government will ask Prime Minister Narendra Modi to open the refinery in January 2024.

- Hence, increasing the refining capacity of the existing refineries and establishing new refineries are expected to witness the growth of the oil and gas downstream sector globally.

Asia-Pacific is Expected to Dominate the Market

- The Asia-Pacific oil and gas downstream market is witnessing robust growth driven by increasing energy demand in the region's emerging economies. With a growing population and industrialization, countries like China and India are experiencing a surge in energy consumption, boosting investments in downstream activities, including refining capacity expansion, modernization of existing refineries, and the development of petrochemical complexes are key trends in this market.

- According to a Statistical Review of World Energy data, in 2023, Asia-Pacific's oil refining capacity reached 37.4 million barrels per day. As of 2023, India accounted for almost 4.9% of global oil refinery capacity. The increasing demand for refined petroleum products has driven downstream companies to invest in new projects and expand existing facilities.

- For instance, in September 2023, the prime minister of India laid the foundation stone for Bharat Petroleum Corp Ltd's (BPCL) refinery expansion and greenfield petrochemical project in Bina. The expansion project is expected to increase BPCL's refinery capacity to 11m tonnes/year from 7.8m tonnes/year. A manufacturing complex will also be built to produce more than 2.2m tonnes/year of petrochemical products. The cost of this project is USD 5.9 billion.

- As of 2023, China accounted for 17.9% of global oil refining capacity. The country's petrochemical and refinery sector is expected to be positive during the forecast period.

- In March 2023, Saudi Aramco and its Chinese partners announced that they aim to start entire operations at a petrochemical and refinery project in northeast China in 2026 to meet the country's increasing demand for petrochemicals and fuel. The project in Liaoning province's city of Panjin, expected to cost USD 10 billion, will be Aramco's second significant refining-petrochemical investment in China.

- Further, in March 2023, Lotte Chemical Indonesia, a South Korea-based Lotte Group subsidiary, successfully secured financing for constructing a petrochemical complex in Banten Province, Indonesia. The project, known as the LINE, is a significant investment for PT Lotte Chemical Indonesia, with a total cost of USD 3.9 billion. Upon completion in 2025, the LINE petrochemical complex will have the capacity to manufacture 1 million tons of Ethylene and 520,000 tons of Propylene annually.

- Hence, the region is expected to dominate the oil and gas downstream market during the forecast period owing to the increasing investment in the refining and petrochemical sector and the expansion of existing downstream infrastructure in respective countries.

Oil & Gas Downstream Industry Overview

The oil and gas downstream market is moderately fragmented. Some of the key players in the market are Reliance Industry Limited, BP PLC, Saudi Aramco, China National Petroleum Corporation, and Chevron Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Oil and Gas Production Scenario (2013 - 2029)

- 4.4 Oil and Gas Consumption Scenario (2013 - 2029)

- 4.5 Refinery Throughput Capacity (2013 - 2029)

- 4.6 Key Projects Information

- 4.6.1 Existing Projects

- 4.6.2 Projects in Pipeline

- 4.6.3 Upcoming Projects

- 4.7 Crude Oil Price Trend Analysis (2013 - 2023)

- 4.8 Recent Trends and Developments

- 4.9 Government Policies and Regulations

- 4.10 Market Dynamics

- 4.10.1 Drivers

- 4.10.1.1 Increasing Refining Capacity across Asia-Pacific and the Middle East

- 4.10.1.2 Rising Industrialization in Developing Countries

- 4.10.2 Restraints

- 4.10.2.1 Increasing Penetration of Electric Vehicles

- 4.10.1 Drivers

- 4.11 Supply Chain Analysis

- 4.12 Porter's Five Forces Analysis

- 4.12.1 Bargaining Power of Suppliers

- 4.12.2 Bargaining Power of Consumers

- 4.12.3 Threat of New Entrants

- 4.12.4 Threat of Substitutes Products and Services

- 4.12.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Refineries

- 5.1.2 Petrochemical Plants

- 5.2 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2029 (for regions only)})

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 France

- 5.2.2.2 Italy

- 5.2.2.3 Germany

- 5.2.2.4 United Kingdom

- 5.2.2.5 Spain

- 5.2.2.6 Nordic Countries

- 5.2.2.7 Turkey

- 5.2.2.8 Russia

- 5.2.2.9 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Indonesia

- 5.2.3.4 Japan

- 5.2.3.5 South Korea

- 5.2.3.6 Malaysia

- 5.2.3.7 Thailand

- 5.2.3.8 Vietnam

- 5.2.3.9 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Nigeria

- 5.2.5.5 Qatar

- 5.2.5.6 Egypt

- 5.2.5.7 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Reliance Industries Ltd

- 6.3.2 Royal Dutch Shell PLC

- 6.3.3 The Dow Chemical Company

- 6.3.4 BP PLC

- 6.3.5 Saudi Aramco

- 6.3.6 Indian Oil Corporation Limited

- 6.3.7 China National Petroleum Corporation

- 6.3.8 Total SA

- 6.3.9 Chevron Corporation

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Digitalization and Modernization of the Refining and Petrochemical Sector

石油・ガス下流- 市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日