|

市場調査レポート

商品コード

1850042

北米のグリーンデータセンター:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)North America Green Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のグリーンデータセンター:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月23日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

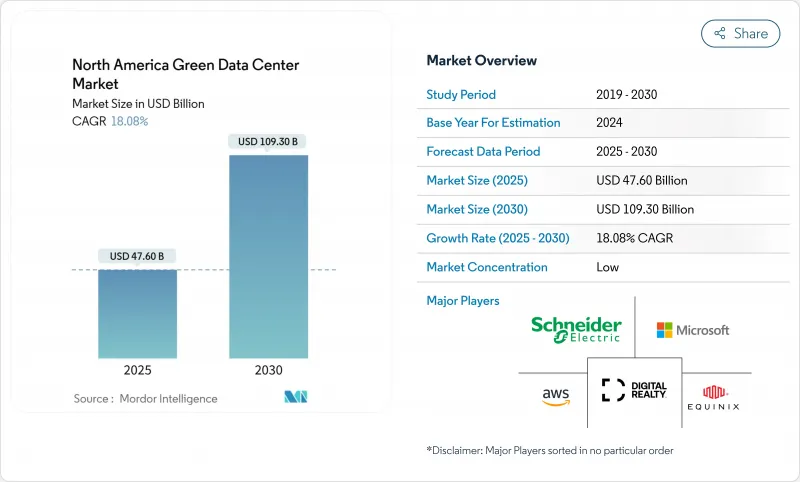

北米グリーンデータセンター市場規模は2025年に476億米ドルに達し、2030年には1,093億米ドルに達する勢いであり、CAGR18.08%で拡大しています。

2023年に176TWhの電力を消費するAIのワークロードの増加、再生可能な電力購入契約(PPA)の拡大、積極的なハイパースケール投資計画が、このエネルギー.govの進展を支えています。ハイパースケールのクラウドプラットフォームは数ギガワットのキャンパスを建設し続け、高密度の液体冷却とオンサイトのクリーンエネルギー発電の需要を押し上げています。コロケーション事業者は、企業のネット・ゼロ義務付けを満たすために競争しており、持続可能性の指標をサービスレベル契約に織り込んでいます。グリッド相互接続の遅れや熟練労働者の不足は依然として逆風だが、AIを活用した気流最適化の技術躍進と相まって、経営者レベルの政策支援が10年を通じて市場の勢いを維持します。

北米グリーンデータセンター市場動向と洞察

北米全域でハイパースケールの構築が急増

ハイパースケール事業者は、オンサイトの太陽光発電、天然ガスピーカープラント、原子力エネルギー割り当てを統合したギガワット規模のキャンパスに資本を注いでいます。アップルは、テキサス州、カリフォルニア州、ノースカロライナ州のAI対応施設に5,000億米ドルを投じ、マイクロソフトの800億米ドルの北米拡張計画に呼応しています。メタ社は、最大4GWのベースロード原子力発電容量に支えられたルイジアナ州の複合施設に100億米ドルを投入します。インフラストラクチャー・メイソン社は、10GWのクラスターをホストできるクリーン・エネルギー・パークを予測し、この地域を持続可能なハイパースケール開発の世界的基準として位置づけています。この軍拡競争が、北米グリーンデータセンター市場におけるハイパースケール容量のCAGR24.4%を裏付けています。

企業のネットゼロ義務化がコロケーションRFPを再形成

企業はコロケーションパートナーを選ぶ際、レイテンシーや価格よりも再生可能エネルギーとの整合性を重視するようになりました。アイアン・マウンテンは、2017年以降、データセンターの負荷の100%を自然エネルギーでまかない、北米初のBREEAM認定サイトを建設し、新たな調達ベンチマークを推進しています。マイクロソフトの2030年カーボン・マイナス誓約と2025年再生可能エネルギー100%適用要件は、サプライチェーンを通じて連鎖し、ベンダーに持続可能性に連動したローンや科学的根拠に基づく目標の採用を促しています。検証可能な炭素削減を実証するプロバイダーが優先入札権を獲得し、環境パフォーマンスが決定的な競争力に高まる。

持続可能な材料の先行投資プレミアム

低炭素コンクリート、大量木材、電気アーク炉鋼は、依然として2桁のプレミア価格で取引されています。マイクロソフトがクインシーで行った試験施工では、体積炭素を50%削減したが、数少ないサプライヤーからしか入手できない特注の混合材が必要でした。アマゾンは、数量割引を考慮した後でも、43の新しいセンターで低炭素鋼のための余分な設備投資を公表しました。長期的には、エネルギーとブランドの利点がこれらのコストを相殺する一方で、高価格帯の大都市圏の開発者は、グリーンボンドによる資金調達や税制優遇措置がなければ、プロジェクトの採算を取るのに苦労しています。

セグメント分析

ソリューションが引き続き北米グリーンデータセンター市場を独占し、2024年の売上高の63.1%を占めました。事業者は効率的な電力、液体冷却、AI対応管理プラットフォームに投資したためです。この優位性はスケールメリットをもたらすが、調達が標準化された利益率の低いハードウェアにシフトするにつれて成長は緩やかになります。対照的に、サービスはCAGR 22.1%で拡大すると予測されます。これは、ネットゼロのロードマップでは継続的な最適化、炭素会計、コンプライアンス監査が必要とされるためです。マネージド・サステナビリティ・サービスは、リアルタイムのエネルギー・ダッシュボードと、施設を科学的根拠に基づく目標(Science-Based Targets)に適合させるためのアドバイザリー・サポートをバンドルしています。

システム統合に割高な料金を支払っている事業者は、空冷ホールからダウンタイムなしの直接チップループへのシームレスなカットオーバーを期待しています。このような複雑な改修は、流体ネットワークの設計、リーク検出データの処理、および体積排出量の最小化が可能な専門企業に依存しています。その結果、機器の価格設定がデフレ圧力に直面しているにもかかわらず、キロワットあたりのサービス収益は上昇しており、グリーンデータセンター市場における長期的な構成比の底堅さを支えています。

ハイパースケーラは、AIのワークロード集約度と垂直統合されたクリーンエネルギー調達により、2024年の北米グリーンデータセンター市場規模の36.1%を獲得しました。2030年までのCAGRは24.4%であり、風力、太陽光、小型原子力、ガスなど、小規模な同業他社が太刀打ちできないような大規模な前倒し契約に基づいています。これらの企業は、電気室や液冷マニホールドのプレハブ化を進め、建設サイクルを短縮してAI製品の立ち上げに対応しています。

コロケーション・プロバイダーは、ハイパースケールの波及案件を獲得するためにキャンパスを再編成しています。新設のコロケーション・プロバイダーは、水なし冷却、持続可能性に関連したリース条項、主要なクラウド・オンランプへの直通ファイバーを備えた100MWのブロックを特徴としています。エッジサイトとエンタープライズサイトは小規模ながら、遠隔医療やゲームなど遅延の影響を受けやすいワークロードに重点を置いています。再生可能なマイクログリッドへの投資は、分散型サイトがいかに企業平均の炭素目標を上回ることができるかを示しており、北米グリーンデータセンター市場のアドレス可能なプールを広げています。

北米グリーンデータセンター市場レポートは、業界をサービス(システムインテグレーション、監視サービス、プロフェッショナルサービス、その他サービス)、ソリューション(電力、サーバー、管理ソフトウェア、その他)、ユーザー(コロケーションプロバイダー、クラウドサービスプロバイダー、企業)、エンドユーザー業界(ヘルスケア、金融サービス、政府、その他)に分類しています。市場予測は金額(米ドル)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 北米全域でハイパースケール施設の建設が急増

- 企業のネットゼロ義務化によりコロケーションRFPが再編される

- 公益事業レベルの再生可能エネルギーPPA価格の下落

- AIによる気流最適化で運用コストを削減

- モジュール式液体冷却レトロフィットの台頭

- データ資産における炭素クレジット収益化のパイロット

- 市場抑制要因

- 持続可能な材料の初期投資プレミアム

- 地域の電力網の混雑と相互接続キューのバックログ

- 低炭素コンクリートと鋼鉄の供給が限られている

- 高密度展開における熟練労働者の不足

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済動向の市場への影響の評価

第5章 市場規模と成長予測

- コンポーネント別

- サービス別

- システム統合

- 監視サービス

- プロフェッショナルサービス

- その他のサービス

- ソリューション別

- 電力

- 冷却

- サーバー

- ネットワーク機器

- 管理ソフトウェア

- その他のソリューション

- サービス別

- データセンタータイプ別

- コロケーションプロバイダー

- ハイパースケーラー/クラウドサービスプロバイダー

- エンタープライズとエッジ

- ティアタイプ別

- ティア1とティア2

- ティア3

- ティア4

- 業界別

- ヘルスケア

- 金融サービス

- 政府

- 通信・IT

- 製造業

- メディアとエンターテイメント

- その他の業界

- 国別

- 米国

- カナダ

- メキシコ

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Schneider Electric SE

- Vertiv Holdings Co

- Eaton Corporation plc

- Cisco Systems Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise

- Fujitsu Ltd

- IBM Corp.

- Hitachi Ltd

- Equinix Inc.

- Digital Realty Trust Inc.

- QTS Realty Trust LLC

- CyrusOne Inc.

- Switch Inc.

- Iron Mountain Data Centers

- Amazon Web Services

- Microsoft Corp.

- Google LLC

- Meta Platforms Inc.

- Rittal GmbH and Co. KG