|

市場調査レポート

商品コード

1689977

放送機器:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Broadcast Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 放送機器:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

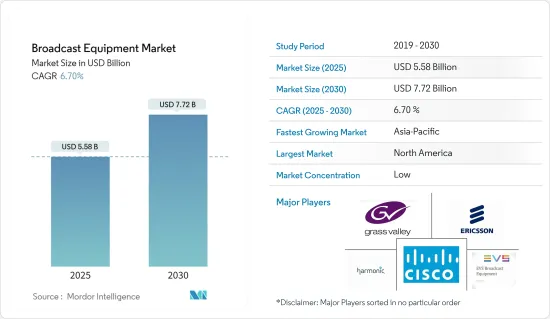

放送機器市場規模は2025年に55億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.7%で、2030年には77億2,000万米ドルに達すると予測されます。

電子的なマスコミュニケーションを通じて音声や映像のコンテンツを正確な視聴者に配信することは、放送として知られています。多くの人々に情報を広めることです。通常、放送はローカル・スポットネットワークシステムに限定されます。依然として人気の高い放送サービスは、最も直接的で信頼性の高い情報媒体を多くの視聴者に届けています。放送機器市場が拡大しているのは、スマート電子機器の利用が増え、3DやHDコンテンツへの需要が高まっているためです。

主要ハイライト

- 過去数十年にわたり、より高品質なオーディオとビデオに対する消費者の需要は、放送機器製品と技術を急速にアップグレードしてきました。コンテンツが4KやUHDフォーマットで制作されるようになり、視聴品質を高めるために同一のフォーマットで放送することがIPライブ制作技術につながりました。これは、柔軟で効率的なシステム制御が重視されるライブ制作には欠かせないです。

- 例えば、2023年11月、ArcGIS Motion Imagery Teamは、新しいArcGIS Video Serverのリリースを発表しました。ArcGIS Enterprise用のこの新しいサーバの役割は、ArcGIS全体で動画機能を拡大するように設計されています。最新のArcGIS Video Serverは、地理空間的と時間的コンテキストを持つサービスとして、動画のインデックス作成、公開、検索、ストリーミングを可能にします。

- 技術の進歩により、放送局はプレミアムユーザーにUHD出力を提供するようになり、市場の成長に拍車をかけています。さらに、デジタルチャネルの増加や、スポーツ中継では8K画質、ニュース中継では4K画質を特徴とする最先端放送機器の利用の増加が、市場成長の加速に寄与しています。8K協会によると、8Kテレビは今後ますます普及します。2023年には約214万台の8Kテレビが出荷され、前年の80万台から増加しました。2026年には、この数は440万台以上に達すると予測されています。

- スポーツ部門は世界中のテレビ視聴者にとって最大の市場であり、ビデオコンテンツを大規模に配信する方法が見つかっています。デバイスやフォーマットの増加は、サービスプロバイダ、コンテンツ所有者、放送局、権利者にいくつかの課題を提供しています。放送機器市場では、レンタルスポーツ放送機器セグメントも大きな収益源となっています。国際的なスポーツ大会の増加が放送機器のレンタル市場を牽引しています。

- さらに、技術の進化、高速インターネットインフラへの投資の増加、OTTサービスによるD2C提供への需要の高まりにより、市場は進化の機会を目の当たりにしています。国際電気通信連合によると、2023年時点で、小島嶼開発途上国(SIDS)では人口の67%がインターネットを利用しているのに対し、後発開発途上国(LDC)では35%であり、内陸の成長国に住む人々のインターネット普及率は39%でした。世界のオンラインアクセス率は67%でした。

- さらに、所得の増加、耐久消費財の購入の増加、高速で安価なインターネットの利用可能性の増加が、市場の成長にプラスの影響を与えると予想されます。IBEF, Indiaによると、2024年にはインドメディア市場の40%をテレビが占め、デジタル広告(12%)、印刷メディア(13%)、映画(9%)、OTTとゲーム産業(8%)がこれに続くと予測されています。2025年までには、インテリジェント・テレビの台数は4,000万台から5,000万台に達すると予想されています。

- デジタル音声・映像フォーマットの急速な開拓と、デジタル映像・音声を生成・保存するためのオープン、国内、または国際的な合意規範の必要性が、市場成長の課題となっています。デジタルオーディオやビデオのフォーマットや圧縮方法に関する規範は、デジタル技術の新しい進歩のたびに進化しています。

- COVID-19の大流行により、放送局はコンテンツの制作と配信に対するアプローチの見直しを余儀なくされ、その結果、人員配置、技術スタック、設備が変更されました。たとえばニュース放送は、いくつかの国の封鎖要件に適応し、世界中のいくつかの番組が民生用ビデオ技術を通じて専門家の意見を集めました。放送技術によって、パンデミック中の番組やコンサートも可能になりました。たとえば、レディー・ガガは100人のミュージシャンが居間や寝室、庭で演奏する8時間のイベントを企画しました。

放送機器市場の動向

エンコーダーが大きな成長を遂げる見込み

- エンコーダーは、オーディオ信号やビデオ信号をデジタル形式に変換してネットワーク経由でトランスミッションすることで、放送において重要な役割を果たしています。高画質コンテンツやストリーミングコンテンツの需要が高まるにつれ、放送局は高品質な映像を効率的に配信するための先進的エンコーダを必要としています。このため、視聴者の嗜好や技術標準の進化に合わせて放送局がインフラをアップグレードする際に、エンコーダを含む放送機器の需要が高まっている

- 2024年4月、ネット洞察は、エミー賞を受賞したインターネットメディアトランスポート製品Nimbra 400エンコーダーの機能を強化し、アップグレードされたNimbra 414で、より豊かでよりインタラクティブなイベント制作の成長に対応することを発表しました。Nimbra 414の最新バージョンは、チャネル密度を高め、UHDコンテンツをサポートすることで、Nimbra 414エンコーダー/デコーダー・ファミリーは、放送局が視聴者のエンゲージメントを高める、より没入感のある作品を提供するのに最適な位置づけとなっています。

- ビデオをエンコードする目的は、インターネットで伝送されるデジタルコピーを作成することです。放送局は、ストリームの目的や予算に応じて、ハードウェアエンコーダーかソフトウェアエンコーダーのどちらかを選択することができます。ほとんどのプロの放送局はハードウェアエンコーダを使用していますが、高価格帯のため、ほとんどの初級から中級の放送局はライブストリーミングエンコーダソフトウェアを使用しています。

- 例えば、2024年4月、米国のキャプション会社であるVerbit CompanyのVITACと放送ソリューションのプロバイダであるENCOは、放送事業者にハードウェアエンコーダとクラウドキャプションの選択肢を広げることを目的とした戦略的提携を発表しました。この提携により、放送事業者は、それぞれの要件に合わせた包括的なキャプションツールやサービスを利用できるようになります。

- さらに、ストリーミングプラットフォームの普及に伴い、高品質な映像コンテンツをインターネットで配信するための効率的なエンコーディング技術が必要とされています。例えば、2023年9月、北欧の有料テレビとストリーミングプラットフォームのAllenteは、新しいAllente StreamマルチスクリーンOTTサービスを開始しました。その結果、同事業者は3SS 3Ready製品プラットフォームをベースとしたAndroid TVや携帯電話、LGやSamsungのスマートTV、Apple TV、ウェブ、iOS向けの最新アプリを稼動させました。

- さらに、コンテンツがさまざまなプラットフォームやデバイスで配信されるため、放送局はアダプティブビットレート・ストリーミングやさまざまなコーデックやプロトコルとの互換性をサポートするエンコーダーを必要としています。さらに、ライブイベント、スポーツ、ニュース報道の人気により、ライブビデオストリームを効率的にエンコードしてリアルタイムで送信できるエンコーダが必要とされています。

- Meltwaterによると、近年、ライブストリーミングビデオコンテンツは、娯楽や業務目的でオンラインで消費される最も一般的なビデオコンテンツの1つになっています。2023年第3四半期には、ライブストリーミングは世界中のインターネットユーザーの約28%に視聴者リーチを記録しました。さらに2023年、Netflixは米国とカナダで8,013万人の有料ストリーミング加入者がいることを明らかにしました。

- エンコーダーの効果は著しく向上しており、HDTVのような最新のフォーマットやH.264のような圧縮規格の成功に重要な役割を果たしています。現在、放送環境におけるエンコーダーの需要は、貢献、一次配信、ホーム配信の3つの主要な領域に分類することができます。

アジア太平洋は大幅な成長が見込まれる

- アジア太平洋には、中国やインドなど人口密度の高い国々があります。アジア太平洋諸国では都市化とデジタル化が進み、テレビやデジタルメディアコンテンツにアクセスする人が増えているため、放送機器の需要が高まっています。Meltwaterによると、2023年第3四半期には、フィリピンの16~64歳のインターネットユーザーの約96%が毎月Netflixなどの定額制ビデオ・オン・デマンド(SVOD)サービスを利用していました。

- さらに、この地域ではOTT(オーバー・ザ・トップ)ストリーミングプラットフォームの人気が高まっており、高品質のストリーミングサービスをサポートする先進的放送機器のニーズが高まっています。例えば、2024年5月、Prasar Bharatiは8月に独自の家族向けOTTプラットフォームを開始する計画を発表しました。同政府の公共放送は、インドの社会と文化に焦点を当てたコンテンツをストリーミング配信します。当初、このプラットフォームは無料で公開されます。こうした市場の開拓は、同地域の市場成長をさらに推し進める可能性があります。

- アジア太平洋は、オリンピック、FIFAワールドカップ、地域大会などの主要スポーツイベントの開催地です。シームレスな中継とトランスミッションを確保するため、このようなイベント時には放送機器の需要が急増します。同時に、4K/UHD放送、仮想現実(VR)、拡張現実(AR)、没入型オーディオなどの放送技術の進歩が、この地域での先進的放送機器の採用を促進しています。

- GSMAの報告書によると、ブータン、イラン、バングラデシュ、ベトナムといった国々が、モバイルの普及を最も顕著に示しています。同地域におけるスマートデバイスの普及も、高解像度のオーディオとビデオの需要を促進している要因のひとつです。GSMAによると、アジア太平洋の住民の64%はすでにスマートフォンを所有しており、2025年には普及率が80%を超えると予想されています。

- さらに、Netflixは2023年3月、アジア太平洋のローカルコンテンツに約19億米ドルを投じる計画を発表しました。同社は2023年に前年比12%の収益成長を記録し、2022年の9%成長に対し40億米ドルを超えると予想されました。また、ITUによると、2023年時点でアジア太平洋の人口の66%がインターネットを利用していると報告されており、市場の成長をさらに促進しています。

- 現地ベンダーは、COVID-19パンデミックによってもたらされた機会を活用するために多額の投資を行りました。例えば、昨年3月、Signiant Inc.は、組み込みメディア処理ソフトウェアを提供するKynoの買収を発表しました。この買収は、SaaSプラットフォームSoftware-Defined Content Exchange(SDCX)の機能を拡大し、メディア資産とのエンゲージメントのためのツールを組み込むのに役立ちます。同プラットフォームは、全世界で約100万人のユーザーを抱え、5万社以上のあらゆる規模のメディアエンターテイメント企業を接続しています。

放送機器産業概要

放送機器市場における様々な企業間の競争は、価格、製品、市場シェア、競争の激しさによって決まる。主要市場参入企業には、Cisco Systems Inc.、Telefonaktiebolaget LM Ericsson、Harmonic Inc.、EVS Broadcast Equipment SA、Grass Valleyなどがあります。

- 2024年4月:ミッションクリティカルなリアルタイムビデオネットワーキングとビジュアルコラボレーションソリューションの世界的プロバイダであるHaivision Systemsは、HaivisionとSony Corporation(以下Sony)が、ハイビジョンの産業をリードするビデオエンコーダ、デコーダ、モバイルビデオトランスミッターとSonyのクラウドプロダクションプラットフォーム「Creators'Cloud for Enterprise」のテストに成功したと発表しました。

- 2024年2月:Sonyは、5Gネットワーク上での高速・低遅延な動画・静止画データ伝送を可能にする独自の専用ポータブルデータトランスミッター「PDT-FP1」の発売を発表しました。この無線通信機は、カメラに装着することで、ニュースやイベントの撮影、放送映像制作など、画像の取り込みから配信、放送、配信まで、スピードが求められる場面で活用されます。Wi-Fi接続が利用できない屋外や屋内環境で、5Gネットワークを介した高速、低遅延、安定したモバイルデータ通信を提供し、効率的でわかりやすいワークフローを実現します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

- 調査の枠組み

- 二次調査

- 一次調査

- データの三角測量と洞察の生成

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- バリューチェーン分析

- 主要マクロ経済動向の市場への影響

第5章 市場力学

- 市場の促進要因

- 複数フォーマット対応によるエンコーダー需要の拡大

- OTTサービスを通じたD2Cサービスの拡大

- SAASソリューションの採用増加

- 市場抑制要因

- 放送に使用されるメディアフォーマットとコーデックの標準化の欠如

第6章 市場セグメンテーション

- 技術別

- アナログ放送

- デジタル放送

- 製品別

- アンテナ

- スイッチ

- ビデオサーバー

- エンコーダ

- トランスミッター&リピータ

- その他

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Cisco Systems Inc.

- Telefonaktiebolaget LM Ericsson

- Evs Broadcast Equipment SA

- Grass Valley

- Harmonic Inc.

- Clyde Broadcast

- Sencore Inc.

- Eletec Broadcast Telecom Sarl

- AVL Technologies Inc.

- ETL Systems Ltd

第8章 投資分析

第9章 市場の将来

The Broadcast Equipment Market size is estimated at USD 5.58 billion in 2025, and is expected to reach USD 7.72 billion by 2030, at a CAGR of 6.7% during the forecast period (2025-2030).

The distribution of audio and video content to a precise audience via electronic mass communication is known as broadcasting. It is a spread of information to a large group of people. Typically, broadcasting is limited to a local spot network system. Broadcasting services, which remain popular, deliver a large audience with the most direct and reliable information mediums. The broadcast equipment market is expanding because of the increased use of smart electronic devices and improved demand for 3D and HD content.

Key Highlights

- Over the last few decades, consumers' demand for better-quality audio and video has rapidly upgraded broadcast equipment products and technology. With content being produced in 4K and UHD formats, broadcasting in the identical format for enhanced viewing quality has resulted in IP live-production technology. This is essential for live production, where a premium is placed on flexible and efficient system control.

- For instance, in November 2023, the ArcGIS Motion Imagery Team announced the release of the new ArcGIS Video Server. This new server role for ArcGIS Enterprise is designed to expand video capabilities across ArcGIS. The latest ArcGIS Video Server allows indexing, publishing, searching, and streaming video as a service with geospatial and temporal context.

- Technological advancements are driving broadcasters to provide UHD output to their premium users, fueling market growth. Moreover, the rise in digital channels and the increasing utilization of cutting-edge broadcasting devices, featuring 8K video quality for sports coverage and 4K quality for news coverage, contribute to the acceleration of market growth. According to the 8K Association, 8K TVs will become increasingly popular in the coming years. Around 2.14 million 8K TV sets were shipped in 2023, up from 800 thousand in the previous year. By 2026, this number is predicted to reach over 4.4 million units.

- The sports section is the biggest market for TV viewers worldwide, and it is finding ways to deliver video content at scale. The increasing number of devices and formats offer several challenges for service providers, content owners, broadcasters, and rights holders. The rental sports broadcast equipment sector is also a significant revenue generator in the broadcast equipment market. The increasing number of international sports tournaments is driving the rental market for broadcast equipment.

- Furthermore, the market is witnessing opportunities for evolution due to evolving technology, increased investments in high-speed internet infrastructure, and growing demand for D2C offerings via OTT services. According to the International Telecommunication Union, as of 2023, 67% of the population in small island developing states (SIDS) used the internet, compared to 35% of the population in least developed countries (LDCs), while the internet penetration rate for those living in landlocked growing counties was at 39%. The global online access rate was 67%.

- Moreover, the rising income, increasing purchases of consumer durables, and the increasing availability of fast and cheap internet are expected to impact the market's growth positively. As per IBEF, India, television is projected to constitute 40% of the Indian media market in 2024, trailed by digital advertising (12%), print media (13%), cinema (9%), and the OTT and gaming industries (8%). By 2025, it is anticipated that the number of linked intelligent televisions will reach around 40 to 50 million.

- The rapidly developing nature of digital audio and video formats and the need for open, domestic, or international agreement norms for generating and preserving digital video and audio are challenging the market's growth. Norms for digital audio and video formats and compression methods are evolving with every new advancement in digital technology.

- The COVID-19 pandemic forced broadcasters to rethink their approach to producing and delivering content - resulting in changes to staffing, technology stacks, and facilities. News broadcasting, for instance, adapted to the lockdown requirements of several nations, with several programs worldwide gathering experts' input through consumer video technology. Broadcasting technologies also enabled programs and concerts during the pandemic. For instance, Lady Gaga organized an eight-hour event involving 100 musicians playing from their living rooms, bedrooms, and gardens.

Broadcast Equipment Market Trends

Encoders are Expected to Witness Significant Growth

- Encoders play a crucial role in broadcasting by converting audio and video signals into digital format for transmission over networks. As demand for high-definition and streaming content grows, broadcasters need advanced encoders to deliver high-quality video efficiently. This drives the demand for broadcast equipment, including encoders, as broadcasters upgrade their infrastructure to meet evolving viewer preferences and technological standards.

- In April 2024, Net Insight announced a boost to the capability of its Emmy Award-winning internet media transport offering, the Nimbra 400 encoders, to meet the growth in more prosperous and more interactive events production with the upgraded Nimbra 414. The latest version of the Nimbra 414 increases channel density and support for UHD content, making the Nimbra 414 encoder/decoder family now ideally placed to help broadcasters deliver more immersive productions that enhance viewer engagement.

- The purpose of encoding a video is to create a digital copy transmitted over the internet. Broadcasters can choose between a hardware or software encoder, depending on the purpose of the stream and the budget. Most professional broadcasters use hardware encoders, but due to the high price point, most beginner-level to mid-experienced broadcasters go with live streaming encoder software.

- For instance, in April 2024, VITAC, a Verbit Company, a US-based captioning company, and ENCO, a provider of broadcasting solutions, announced a strategic partnership aimed at providing broadcasters with expanded choice for hardware encoders and cloud captioning. Through this alliance, broadcasters will access a comprehensive suite of captioning tools and services tailored to meet their specific requirements.

- Furthermore, the increasing popularity of streaming platforms necessitates efficient encoding technologies to deliver high-quality video content over the internet. For instance, in September 2023, Nordic PayTV and streaming platform Allente launched its new Allente Stream multiscreen OTT offering. As a result, the operator has gone live with the latest apps for Android TV and mobiles, LG and Samsung Smart TVs, Apple TV, web, and iOS, based on the 3SS 3Ready product platform.

- Moreover, with content being distributed across different platforms and devices, broadcasters need encoders that support adaptive bitrate streaming and compatibility with different codecs and protocols. Further, the popularity of live events, sports, and news coverage needs encoders that can efficiently encode and transmit live video streams in real time.

- According to Meltwater, in recent years, live-streaming video content has become one of the most popular types of video content consumed online for entertainment and operational purposes. During the third quarter of 2023, live streaming registered an audience reach of almost 28% among internet users worldwide. In addition, in 2023, Netflix revealed that it had 80.13 million paying streaming subscribers in the United States and Canada.

- The effectiveness of encoders has significantly improved, and they play a significant role in the success of modern formats, like HDTV, and compression standards, like H.264. Currently, the demand for encoders in broadcast settings can be categorized into three key domains: contribution, primary distribution, and home distribution.

Asia-Pacific is Expected to Witness Significant Growth Rate

- Asia-Pacific is home to some densely populated countries such as China and India. Increasing urbanization and digitization across Asia-Pacific countries fuel the demand for broadcast equipment as more people access television and digital media content. According to Meltwater, in the third quarter of 2023, about 96% of internet users aged between 16 and 64 years in the Philippines used a subscription video-on-demand (SVOD) service, such as Netflix, each month.

- Further, over-the-top (OTT) streaming platforms are gaining popularity in the region, creating a need for advanced broadcast equipment to support high-quality streaming services. For instance, in May 2024, Prasar Bharati has announced its plans to start its own OTT platform for families in August. The government's public service broadcaster will stream content that will be focused on Indian society and culture. Initially, the platform will be available for free to the public. Such developments may further propel the market's growth in the region.

- Asia-Pacific is home to major sporting events like the Olympics, FIFA World Cup, and regional tournaments. The demand for broadcast equipment surges during such events to ensure seamless coverage and transmission. At the same time, advancements in broadcasting technologies, such as 4K/UHD broadcasting, virtual reality (VR), augmented reality (AR), and immersive audio, are driving the adoption of advanced broadcast equipment in the region.

- Countries such as Bhutan, Iran, Bangladesh, and Vietnam are demonstrating the most significant mobile penetration advances, according to a GSMA report. The implementation of smart devices in the region is another factor fueling the demand for high-definition audio and videos. As per GSMA, 64% of the residents in APAC already possess smartphones, and the adoption is expected to cross 80% in 2025.

- Furthermore, in March 2023, Netflix announced plans to spend approximately USD 1.9 billion on local content in Asia-Pacific. The company was expected to register revenue growth of 12% Y-o-Y in 2023 and exceed USD 4 billion compared to 9% growth in 2022. In addition, according to ITU, 66% of the population in Asia-Pacific reported using the Internet as of 2023, further propelling the market's growth.

- Local vendors invested heavily to capitalize on the opportunities brought by the COVID-19 pandemic. For instance, in March last year, Signiant Inc. announced the acquisition of Kyno, which provides embedded media processing software. The acquisition helps Signiant Inc. extend the functionality of the Software-Defined Content Exchange (SDCX) SaaS platform, incorporating tools for engagement with media assets. With almost 1 million users globally, the platform connects more than 50,000 media and entertainment companies of all sizes.

Broadcast Equipment Industry Overview

The competitive rivalry between various firms in the broadcast equipment market depends on price, product, or market share, along with the intensity with which they compete. Some major market players include Cisco Systems Inc., Telefonaktiebolaget LM Ericsson, Harmonic Inc., EVS Broadcast Equipment SA, and Grass Valley.

- April 2024: Haivision Systems, a global provider of mission-critical, real-time video networking and visual collaboration solutions, announced that Haivision and Sony Corporation (Sony) had successfully tested Haivision's industry-leading video encoders, decoders, and mobile video transmitters with Sony's cloud production platform, Creators' Cloud for Enterprise.

- February 2024: Sony announced the launch of a unique dedicated portable data transmitter, the PDT-FP1, that allows high-speed, low-latency video and still image data transport over 5G networks. When attached to a camera, this wireless communication device will be used when speed is required, from image capture to delivery, broadcasting, and distribution, such as news or events photography and broadcast video production. It provides high-speed, low-latency, and stable mobile data communication over 5G networks in outdoor or indoor environments where a Wi-Fi connection is unavailable, enabling efficient and straightforward workflows.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Value Chain Analysis

- 4.4 Impact of Key Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Encoders due to Support for Multiple Formats

- 5.1.2 Growing D2C Offerings through OTT Services

- 5.1.3 Increased Adoption of SAAS Solutions

- 5.2 Market Restraint

- 5.2.1 Lack of Standardization of Media Formats and Codecs Used for Broadcasting

6 MARKET SEGMENTATION

- 6.1 By Technology

- 6.1.1 Analog Broadcasting

- 6.1.2 Digital Broadcasting

- 6.2 By Product

- 6.2.1 Dish Antennas

- 6.2.2 Switches

- 6.2.3 Video Servers

- 6.2.4 Encoders

- 6.2.5 Transmitters and Repeaters

- 6.2.6 Other Products

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc.

- 7.1.2 Telefonaktiebolaget LM Ericsson

- 7.1.3 Evs Broadcast Equipment SA

- 7.1.4 Grass Valley

- 7.1.5 Harmonic Inc.

- 7.1.6 Clyde Broadcast

- 7.1.7 Sencore Inc.

- 7.1.8 Eletec Broadcast Telecom Sarl

- 7.1.9 AVL Technologies Inc.

- 7.1.10 ETL Systems Ltd