ヘルスケア電子データ交換市場の機会、成長促進要因、業界動向分析、2025年~2034年の予測

Healthcare Electronic Data Interchange Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1665077

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

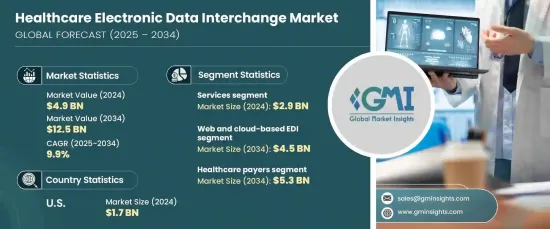

世界のヘルスケア電子データ交換市場は、2024年に49億米ドルと評価され、2025年から2034年にかけて9.9%のCAGRが予測され、著しい成長を遂げようとしています。

この市場拡大は、厳格な規制の義務化、シームレスな相互運用性への需要の高まり、ヘルスケアシステムにおける管理業務の合理化ニーズの高まりに後押しされ、自動化されたEDIソリューションの採用が増加していることが背景にあります。

ヘルスケア業界がデジタルトランスフォーメーションを取り入れる中、EDIプラットフォームは、支払者、プロバイダー、利害関係者間の安全で標準化された効率的なデータ交換に不可欠なツールとして台頭しています。これらのプラットフォームは、手作業による非効率なプロセスを排除し、進化する規制へのコンプライアンスを確保し、機密性の高い患者情報を保護します。さらに、クラウド・コンピューティングとAIを活用した分析の進歩により、洗練されたコスト効率の高いソリューションが導入され、あらゆる規模の組織にEDIシステムの魅力が広がっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 49億米ドル |

| 予測金額 | 125億米ドル |

| CAGR | 9.9% |

ヘルスケアEDIシステムの導入を加速させる上で、政府の規制と業界標準が極めて重要な役割を果たしています。規制の枠組みは、安全なデータ交換の必要性を強調し、医療機関にワークフローの近代化を促しています。自動化されたEDIソリューションは、ヘルスケア・エコシステム全体の効率的なコミュニケーションを促進しながら、プライバシーとセキュリティ標準へのシームレスなコンプライアンスを保証します。デジタル化の推進は、ヘルスケアプロバイダーがパフォーマンスの最適化とコスト削減のプレッシャーの高まりに取り組む中で特に重要であり、市場の拡大をさらに後押ししています。

コンポーネント別に見ると、ヘルスケアEDI市場はサービスとソリューションに区分され、サービスが収益をリードしています。サービスは2024年に29億米ドルに達し、業界のシステム統合、カスタマイズ、トレーニング、技術サポートへの依存を反映しています。組織がレガシーシステムから最新のEDIプラットフォームに移行する際、これらのサービスはスムーズで効率的な統合プロセスを保証します。専門サービスに対する需要の高まりは、相互運用性の達成と厳格なコンプライアンス要件の遵守にヘルスケア部門が注力していることを裏付けています。この動向は、オペレーショナル・エクセレンスを追求するヘルスケアプロバイダーの優先事項と一致し、勢いを増すと予想されます。

市場はまた、EDI付加価値ネットワーク(VAN)、ダイレクト(ポイント・ツー・ポイント)EDI、ウェブおよびクラウドベースEDI、モバイルEDIなど、導入タイプに基づいてセグメント化されます。このうち、ウェブおよびクラウドベースのEDIソリューションが2024年には優位を占めており、このセグメントは2034年までに45億米ドルを生み出すと予測されています。クラウドベースのソリューションは比類のない拡張性とコスト効率を提供するため、ヘルスケア組織は多額のハードウェア投資をすることなく業務を拡大することができます。これらのシステムは、オンプレミスのインフラを維持する負担なしに高度なツールへのアクセスを求める中小規模の医療機関にとって特に魅力的です。クラウドベースのEDIは、柔軟性、信頼性、手頃な価格により、市場成長の礎となっています。

北米は2024年にヘルスケアEDI市場の17億米ドルを占めたが、これは標準化されたトランザクションを義務付ける厳しい規制要件と米国の堅調な医療支出に後押しされたものです。業界がデータ主導のイノベーションを優先する中、デジタルインフラとAI主導のアナリティクスへの投資が引き続き先進的なEDIソリューションの採用を促進し、ヘルスケアデータ交換の世界情勢を再構築しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 規制支援とコンプライアンス要件

- 相互運用性に対する需要の高まり

- 技術の進歩

- コスト削減と効率化

- 業界の潜在的リスク&課題

- 高い導入コスト

- 促進要因

- 成長可能性分析

- 規制状況

- 米国

- 欧州

- 技術動向

- 今後の市場動向

- イノベーションの展望

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- サービス

- ソリューション

第6章 市場推計・予測:展開タイプ別、2021年~2034年

- 主要動向

- ウェブおよびクラウドベースのEDI

- EDI付加価値ネットワーク(VAN)

- ダイレクト(ポイント・ツー・ポイント)EDI

- モバイルEDI

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 医療費支払者

- 医療提供者

- 製薬・医療機器業界

- その他のエンドユーザー

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Boomi

- Cleo

- DataTrans Solutions

- Effective Data

- Epicor Software Corporation

- GE Healthcare

- MCKESSON CORPORATION

- NXGN Management

- OpenText

- Optum

- Oracle

- OSP

- SPS Commerce

- SSI Group

- TrueCommerce

目次

The Global Healthcare Electronic Data Interchange Market, valued at USD 4.9 billion in 2024, is set to experience remarkable growth with a projected CAGR of 9.9% between 2025 and 2034. This expansion is driven by the increasing adoption of automated EDI solutions, propelled by stringent regulatory mandates, growing demand for seamless interoperability, and the rising need to streamline administrative operations in healthcare systems.

As the healthcare industry embraces digital transformation, EDI platforms emerge as indispensable tools for secure, standardized, and efficient data exchange between payers, providers, and stakeholders. These platforms eliminate the inefficiencies of manual processes, ensuring compliance with evolving regulations and safeguarding sensitive patient information. Furthermore, advancements in cloud computing and AI-powered analytics have introduced sophisticated, cost-effective solutions, broadening the appeal of EDI systems to organizations of all sizes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.9 Billion |

| Forecast Value | $12.5 Billion |

| CAGR | 9.9% |

Government regulations and industry standards play a pivotal role in accelerating the adoption of healthcare EDI systems. Regulatory frameworks emphasize the necessity for secure data exchange, prompting healthcare organizations to modernize their workflows. Automated EDI solutions ensure seamless compliance with privacy and security standards while fostering efficient communication across the healthcare ecosystem. This push toward digitization is particularly significant as healthcare providers grapple with mounting pressures to optimize performance and reduce costs, further driving the market's expansion.

In terms of components, the healthcare EDI market is segmented into services and solutions, with services leading the charge in revenue generation. Services reached USD 2.9 billion in 2024, reflecting the industry's reliance on system integration, customization, training, and technical support. As organizations transition from legacy systems to modern EDI platforms, these services ensure a smooth and efficient integration process. The rising demand for professional services underscores the healthcare sector's focus on achieving interoperability and adhering to stringent compliance requirements. This trend is expected to gain momentum, aligning with healthcare providers' priorities for operational excellence.

The market also segments based on deployment type, including EDI value-added networks (VANs), direct (point-to-point) EDI, web and cloud-based EDI, and mobile EDI. Among these, web and cloud-based EDI solutions dominated in 2024, and this segment is forecasted to generate USD 4.5 billion by 2034. Cloud-based solutions offer unmatched scalability and cost-efficiency, allowing healthcare organizations to expand operations without heavy hardware investments. These systems are particularly attractive to small and medium-sized providers seeking access to advanced tools without the burden of maintaining on-premises infrastructure. The flexibility, reliability, and affordability of cloud-based EDI make it a cornerstone of the market's growth trajectory.

North America accounted for USD 1.7 billion of the healthcare EDI market in 2024, fueled by strict regulatory requirements mandating standardized transactions and robust healthcare spending in the United States. As the industry prioritizes data-driven innovations, investments in digital infrastructure and AI-driven analytics continue to drive the adoption of advanced EDI solutions, reshaping the global landscape of healthcare data exchange.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Regulatory support and compliance requirements

- 3.2.1.2 Rising demand for interoperability

- 3.2.1.3 Technological advancements

- 3.2.1.4 Cost reduction and efficiency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation cost

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Innovation landscape

- 3.8 Gap analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Component, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Services

- 5.3 Solutions

Chapter 6 Market Estimates and Forecast, By Deployment Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Web and cloud-based EDI

- 6.3 EDI value added network (VAN)

- 6.4 Direct (point-to-point) EDI

- 6.5 Mobile EDI

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Healthcare payers

- 7.3 Healthcare providers

- 7.4 Pharmaceutical and medical device industries

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Boomi

- 9.2 Cleo

- 9.3 DataTrans Solutions

- 9.4 Effective Data

- 9.5 Epicor Software Corporation

- 9.6 GE Healthcare

- 9.7 MCKESSON CORPORATION

- 9.8 NXGN Management

- 9.9 OpenText

- 9.10 Optum

- 9.11 Oracle

- 9.12 OSP

- 9.13 SPS Commerce

- 9.14 SSI Group

- 9.15 TrueCommerce

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日