|

市場調査レポート

商品コード

1849844

欧州のグリーンデータセンター:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Europe Green Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のグリーンデータセンター:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月20日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

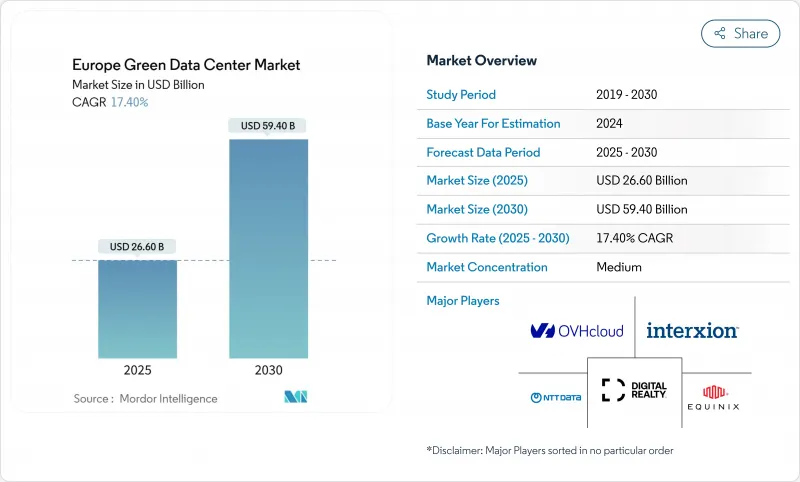

欧州のグリーンデータセンター市場は、2025年に266億米ドルを創出し、2030年にはCAGR 17.4%で成長し594億米ドルに達すると予測されます。

EUグリーン・ディールによる規制の強化、次世代AIインフラへの超大規模投資、企業全体のデジタル化により、容量の拡大と持続可能性の革新の両方を支える需要曲線が持続的に強化されています。エネルギー効率指令が500kW以上の施設にエネルギー測定基準を報告し、再生可能エネルギーの閾値を満たすことを義務付けているため、事業者は超効率的な電力と冷却技術に資本を誘導しています。北欧の電力購入契約(PPA)インセンティブは、低炭素電力を確保し、事業者が物理的最小値に近い電力使用効率(PUE)比を計上することを可能にする一方、FLAP-Dハブは、グリッドのバックログにもかかわらず、相互接続密度の点で依然として魅力的です。監視、ライフサイクル管理、コンプライアンス報告をバンドルするサービス・プロバイダーは、ハードウェア中心の同業他社よりも急速に拡大しており、単発の構築から継続的な最適化へのシフトを反映しています。調査範囲3の報告サポートを高密度の液体冷却と連携させることができるベンダーは、最も強力なアップサイドを獲得することになります。

欧州のグリーンデータセンター市場動向と洞察

クラウドとビッグデータのワークロード急増

AIおよび機械学習タスクは、2024年中に欧州のデータセンター電力の8%を消費し、2028年までに20%に達する可能性があるため、空気冷却の15~25倍の速さで熱を除去する液冷の急速な導入が促されています。マイクロソフトは、2026年までに2万台以上のGPUを収容するリーズのAIに特化したキャンパスに25億米ドルを計上し、ハイパースケーラが高密度ラックを中心とした施設アーキテクチャをどのように再構築するかを示しています。エッジでの小規模な推論ワークロードは、中央のトレーニングクラスタに接続された分散マイクロサイトを生み出し、再生可能エネルギー目標を維持しながら待ち時間を削減しています。現在、企業のクラウド戦略には定量的な持続可能性指標が含まれており、欧州の事業者の38%は、AIの成長と二酸化炭素削減の誓約のバランスを取るため、2024年に環境に優しい設備に投資しています。液体対応設計とラックレベルの熱再利用は、性能とコンプライアンスの両面でメリットをもたらし、近い将来の需要形成におけるドライバーの地位を強化します。

EUのグリーンディールと55歳適合義務

エネルギー効率指令は、500 kWを超えるデータセンターに対し、年間資源指標を公表し、2030年までにエネルギー消費量を11.7%削減することを義務付けています。ドイツのエネルギー効率化法では、2026年7月以降の新築のPUE上限を1.2とし、2027年までに再生可能電力100%を義務付ける。2024年9月に施行される汎EU的な持続可能性評価の枠組みは、事業者がパフォーマンスをベンチマークし、企業持続可能性報告指令に拘束される企業からの優先調達を確保することを可能にします。コンプライアンスへの支出は、製品のイノベーションを促進する:エクイニクスは、施設のPUEを下げながら近隣の家庭を暖める廃熱ネットワークを試験的に導入しています。透明性の高い指標を証明できる事業者は、企業のRFPで競争力を獲得し、自動モニタリングやライフサイクル炭素会計プラットフォームの採用を強化しています。

液冷とオンサイトREにかかる高いCAPEX

ダイレクト・ツー・チップおよび液浸システムは、ライフサイクルの節約にもかかわらず、空冷システムよりも20~40%コストが高く、低コストの資本を持たない事業者にとっては投資回収までの期間が長くなります。20kWを超えるAIラックは、これらのアップグレードの必要性を増大させるが、レトロフィット作業には、フロアプレートの再構成、電気系統の改造、スタッフの再教育が必要となります。太陽光発電やバッテリーのオンサイト設置は、6ヶ月の許認可期限に直面し、スケジュールを複雑にし、保有コストを上昇させる。大規模な多国籍企業は、持続可能性に関連したローンによって費用を軽減しているが、小規模なコロケーション・プレイヤーは、資金調達の革新やパートナーシップ・モデルによって先行投資負担が軽減されるまで、マージンが圧縮されるリスクがあります。

セグメント分析

ソリューションの売上は2024年に161億米ドルに達し、支出全体の60.54%に相当します。これは、事業者が効率的なパワートレイン、高密度サーバー、高度な冷却装置を調達し、指令主導のPUEベンチマークを満たすためです。欧州のグリーンデータセンターのサービス市場規模は105億米ドルを記録し、2030年までのCAGRは22.1%に達する見込みであり、これは炭素会計、ライフサイクルモニタリング、規制アドバイザリーに対する需要の急増を反映しています。専用のシステム統合手法により、液冷と空冷をレトロフィットのフットプリント内で整合させ、資源効率を高めながら移行時間を短縮します。データセンター・インフラ管理(DCIM)ソフトウェアによる継続的な監視は、EUグリーンディールの透明性監査の必須条件であるエネルギー報告を自動化します。スコープ3の追跡義務が深まるにつれて、サプライヤの監査や具体化炭素評価に焦点を当てた専門的なサービス・ポートフォリオがシェアを拡大し、ハードウェアの更新サイクルを補完するサービス主導の成熟段階が再確認されました。

ハイパースケーラは、2024年の売上高の35.2%を占め、CAGR24.4%で拡大します。これは、バランスシートの強みを活かして、再生可能契約を固定化し、大規模な液冷を試行するためです。ハイパースケールキャンパスに起因する欧州のグリーンデータセンター市場規模は2030年までに250億米ドルを超えると予測され、電力購入契約に組み込まれた持続可能性条項が長期的な競争力を支えます。コロケーション・プロバイダーは、再生可能クレジットや廃熱再利用スキームをバンドルすることで差別化を図り、中堅企業にアピールしています。企業のオンプレミス設置面積は縮小を続けているが、待ち時間の影響を受けやすいワークロードを抱える企業は、効率的な冷却装置を備えたエッジノードに依存するハイブリッドモデルを維持しています。エッジプロバイダーは、人口集中地区の近くに250kW-1MWのモジュールを配備し、再生空気エコノマイザーとモジュール式バッテリーストレージによって規制遵守を確保しています。大規模なハイパースケーラは、AWSがスウェーデンで低炭素鋼を採用し、体積排出量を最大70%削減するなど、建設段階での炭素削減を公表しており、小規模な競合他社はこれに匹敵するよう努力しています。

欧州のグリーンデータセンター市場セグメンテーションでは、業界をサービス(システムインテグレーション、監視サービス、プロフェッショナルサービス、その他サービス)、ソリューション(電源、サーバー、管理ソフトウェア、その他)、ユーザー(コロケーションプロバイダー、クラウドサービスプロバイダー、企業)、エンドユーザー業界(ヘルスケア、金融サービス、政府機関、その他)に分類。市場予測は金額(米ドル)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 主流のドライバー

- クラウドとビッグデータのワークロードの急増

- EUグリーンディールとFit-for-55の義務

- FLAP-Dハブにおけるハイパースケールとエッジの構築

- 注目されていないドライバー

- 超低PUEを実現する北欧のPPA

- 地域暖房廃熱補助金

- スコープ3重視のグリーンSLA需要

- 市場抑制要因

- 主流の制約

- 液体冷却とオンサイト再生可能エネルギーへの高額な設備投資

- 電力不足地域における送電網接続の遅延

- 目立たない拘束

- 炭素鋼とコンクリートの精査

- 持続可能なDCエンジニアリングの人材不足

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済動向の市場への影響の評価

第5章 市場規模と成長予測

- コンポーネント別

- サービス別

- システム統合

- 監視サービス

- プロフェッショナルサービス

- その他のサービス

- ソリューション別

- 電力

- 冷却

- サーバー

- ネットワーク機器

- 管理ソフトウェア

- その他の解決策

- サービス別

- データセンタータイプ別

- コロケーションプロバイダー

- ハイパースケーラー/クラウドサービスプロバイダー

- エンタープライズとエッジ

- ティアタイプ別

- ティア1とティア2

- ティア3

- ティア4

- 業界別

- ヘルスケア

- 金融サービス

- 政府

- 通信・IT

- 製造業

- メディアとエンターテイメント

- その他の業種

- 国別

- ドイツ

- 英国

- フランス

- オランダ

- アイルランド

- ノルウェー

- スウェーデン

- デンマーク

- スペイン

- イタリア

- ロシア

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Equinix Inc.

- Digital Realty Trust Inc.

- NTT Global Data Centers EMEA GmbH

- Schneider Electric SE

- Fujitsu Ltd.

- Cisco Systems Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Co.

- IBM Corporation

- Eaton Corporation plc

- Vertiv Holdings Co.

- OVH Groupe SAS

- Interxion Holding N.V.

- Vantage Data Centers LLC

- Bulk Infrastructure AS

- Green Mountain AS

- EcoDataCenter AB

- Stack Infrastructure Inc.

- Iron Mountain Inc.

- Deep Green Data Centres Ltd.

- Verne Global Ltd.