|

市場調査レポート

商品コード

1636489

中国のEVバッテリー電解液:市場シェア分析、産業動向・統計、成長予測(2025~2030年)China Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国のEVバッテリー電解液:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

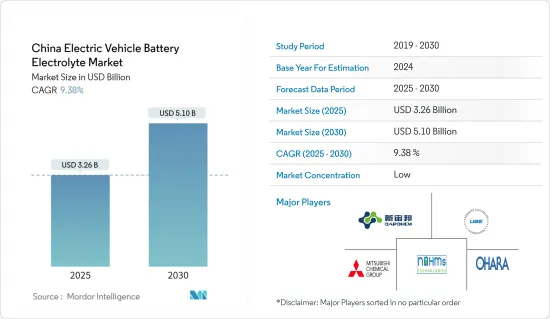

中国の電気自動車用バッテリー電解液市場規模は2025年に32億6,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは9.38%で、2030年には51億米ドルに達すると予測されます。

主なハイライト

- 長期的には、中国におけるBEV、PHEV、HEVを含む電気自動車の利用増加と、電気自動車の利用を促進するための有利な政府補助金(i.e.免税政策)が市場の成長を促進すると予測されます。

- 逆に、電池製造のための原料埋蔵量の不足は、電気自動車用電池電解質市場にマイナスの影響を与えると予想されます。

- とはいえ、中国の電池試験所(i.e. China Automotive Battery Research Institute、SGS China)で進行中の電解質材料の調査と進歩は、市場成長の機会を提供する可能性があります。

中国の電気自動車用バッテリー電解液市場動向

リチウムイオン電池が市場を独占する見込み

- リチウムイオン電池は寿命が長いため、電気自動車(EV)の電源として使用されており、電池交換の頻度が少なくなっています。リチウムイオンバッテリーは、鉛やカドミウムのような有害物質を含まないため、他のバッテリーと違って環境に優しく、クリーンで安全です。さらに、これらの電池は、素早い加速と高速走行が要求されるEVに不可欠な、強力な出力を提供します。

- 2023年6月、中国のバッテリー・メーカーであるゴティオン・ハイテックは、電気自動車用に1回の充電で621マイルという驚異的な航続距離を誇るリチウム・マンガン・鉄・リン酸塩(LMFP)バッテリーを発表しました。従来、この航続距離は主に高価なニッケル・コバルト電池で達成されていました。ゴティオンは、同社のLMFP電池が240Wh/kgに達し、キロワット時当たり米ドルベースで標準的なLFP電池より5%低い価格になると予想しています。

- 2023年現在、中国はバッテリー電気自動車(BEV)の分野で圧倒的な地位を占めており、販売台数は約540万台に達します。正極と負極の間で正リチウムイオンを運搬する電解液は極めて重要な役割を担っているため、EVへのリチウムイオン電池の採用が進むにつれ、浸透電解液の需要が高まることが予想されます。

- 2024年7月、中国の研究チームは、低密度と負極適合性を特徴とする、費用対効果の高い硫化物固体電解質を開発し、固体電池技術を飛躍的に発展させました。これらの全固体電池は、現在リチウムイオン電池が直面している容量と安全性の課題に対処する態勢を整えています。

- 予測によると、2025年までに中国の電池メーカーは4,800ギガワット時(GWh)という驚異的な電池を生産することになります。充放電プロセスにおけるバッテリー電解液の重要な役割を考えると、このバッテリー生産の急増は、バッテリー電解液材料の需要を国全体で増幅させることになります。

- その結果、電気自動車へのリチウムイオン電池の採用が増加し、その価格が急落していることから、リチウムイオン電池分野は今後数年間で大きく成長する見込みです。

電気自動車の採用増加が市場を牽引する見込み

- 中国はプラグイン・ハイブリッド電気自動車(EV)の主要市場であり、さまざまな用途の電池を大量生産していることで世界的に認知されています。政府が排ガスフリーの交通機関に向けて強力に推進していることから、中国は今後数年間も支配的な地位を維持するとみられます。

- プラグイン・ハイブリッド車は今後10年間で普及する見通しで、海外の自動車メーカーは中国ブランドに専門知識を求めるようになっています。特に、中国の大手自動車メーカーであるBYDは、2008年に世界初のプラグイン・ハイブリッド・モデルであるF3DMセダンを発表して話題となった。

- 重要な動きとして、中国政府は2024年5月、電気自動車(EV)用の次世代バッテリー技術の開拓に約8億4,500万米ドルを投資する計画を発表しました。CATL(世界最大の電池メーカー)やBYD、吉利汽車などの大手自動車メーカーを含む6社が、全固体電池(ASSB)を発展させるために政府の支援を受けることになった。

- 中国汽車工業協会(CAAM)が2023年8月に報告したように、中国では905万台の乗用車用電気自動車が販売され、その内訳はバッテリーのみの電気自動車(BEV)が626万台、プラグインハイブリッド車(PHEV)が279万台となっています。2023年には、プラグイン電気自動車(BEVとPHEVの両方)が中国の自動車総販売台数の37%を占め、市場シェアはBEVが25%、PHEVが12%です。

- 2024年6月、中国工業情報化部はバッテリー部門に対する新たな指針を発表しました。この指針は、電気自動車用リチウムイオン電池の品質と技術革新を高めることを目的としており、企業に対し、単に生産能力を拡大することから、特に電池電解質溶液の技術革新を強化することに軸足を移すよう促しています。

- 2030年までに、中国では5,000万台の電気自動車が普及すると予想されており、電気自動車充電のための年間電力需要は200TWhに達します。この急増する需要は、中国国内における電気自動車用バッテリー電解液の進歩の可能性を強調しています。

- EVの急速な普及と現在進行中の技術的進歩を考えると、中国は当分の間、市場の優位性を維持する態勢を整えています。

中国の電気自動車用バッテリー電解液産業概要

中国の電気自動車用バッテリー電解液市場は半分裂状態です。市場に参入している主要企業(順不同)には、Advanced Electrolyte Technologies LLC、三菱ケミカルホールディングス、Shenzhen Capchem Technology、Nohms Technologies Inc.、大原鉄工所などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- BEV、PHEV、HEVを含む電気自動車の利用増加

- 電気自動車の利用を促進する有利な政府政策

- 抑制要因

- 電池材料のサプライチェーン格差

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- 電池タイプ

- リチウムイオン電池

- 鉛蓄電池

- その他の電池タイプ

- 電解液タイプ

- 液体電解液

- ゲル電解液

- 固体電解液

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Advanced Electrolyte Technologies LLC

- Mitsubishi Chemical Holdings

- Shenzhen Capchem Technology Co., Ltd

- Nohms Technologies Inc

- Ohara Corporation

- BASF SE

- LG Chem Ltd

- Targray Industries Inc.

- SGS China

- Ningbo Shanshan Co., LTD

- 市場ランキング/シェア(%)分析

- その他の主要プレーヤーのリスト

第7章 市場機会と今後の動向

- 先進電解液材料の研究開発

The China Electric Vehicle Battery Electrolyte Market size is estimated at USD 3.26 billion in 2025, and is expected to reach USD 5.10 billion by 2030, at a CAGR of 9.38% during the forecast period (2025-2030).

Key Highlights

- Over the long term, the increasing usage of electric vehicles, including BEVs, PHEVs, and HEVs, and favorable government subsidies (i.e. tax exemption policy) to promote the usage of electric vehicles in the China are expected to drive the market's growth.

- Conversely, the lack of raw material reserves for battery manufacturing is expected to negatively impact the electric vehicle battery electrolyte market.

- Nevertheless, the ongoing research and advancement in electrolyte material in Chinese battery testing labs i.e, China Automotive Battery Research Institute Co., Ltd., SGS China may offer opportunities for market growth.

China Electric Vehicle Battery Electrolyte Market Trends

Lithium-ion Battery is Expected to Dominate the Market

- Lithium-ion batteries, favored for their extended lifespan, are the go-to power source for electric vehicles (EVs), leading to less frequent battery replacements. Unlike some other battery types, lithium-ion variants are deemed environmentally friendly, as they steer clear of toxic materials such as lead or cadmium, making them a cleaner and safer option. Furthermore, these batteries deliver a robust power output, essential for EVs that demand swift acceleration and high speeds.

- In June 2023, Gotion High-Tech, a Chinese battery manufacturer, introduced a lithium-manganese-iron-phosphate (LMFP) battery, boasting an impressive range of 621 miles per charge for electric vehicles. Previously, this range was predominantly achieved by pricier nickel-cobalt batteries. Gotion anticipates its LMFP battery will reach 240 Wh/kg and be priced 5% lower than the standard LFP battery on a USD per kilowatt-hour basis.

- As of 2023, China stands as a dominant player in the battery electric vehicle (BEV) arena, with sales hitting approximately 5.4 million units. The rising adoption of lithium-ion batteries in EVs is set to boost the demand for penetration electrolyte solutions, given the electrolyte's pivotal role in ferrying positive lithium ions between the cathode and anode.

- In July 2024, a team of Chinese researchers made strides in solid-state battery technology by crafting a cost-effective sulfide solid electrolyte, characterized by its low density and stellar anode compatibility. These all-solid-state batteries are poised to address the capacity and safety challenges currently faced by lithium-ion batteries.

- Forecasts suggest that by 2025, Chinese battery manufacturers will churn out a staggering 4,800 giga-watt hours (GWh) of batteries. Given the critical role of battery electrolytes in the charging and discharging process, this surge in battery production is set to amplify the demand for battery electrolyte materials throughout the nation.

- Consequently, with the rising adoption of lithium-ion batteries in electric vehicles and their plummeting prices, the lithium-ion battery segment is poised for substantial growth in the coming years.

Increasing Adoption of Electric Vehicles is expected to Drive the Market

- China stands as the leading market for plug-in hybrid electric vehicles (EVs) in the region and is globally recognized for its mass production of batteries across various applications. With the government's strong push towards emission-free transportation, China is set to uphold its dominant position in the coming years.

- Plug-in hybrid vehicles are poised to gain traction in the next decade, leading foreign carmakers to seek expertise from Chinese brands. Notably, BYD, a prominent Chinese player, made headlines in 2008 by launching the world's inaugural plug-in hybrid model, the F3DM sedan.

- In a significant move, the Chinese government, in May 2024, unveiled plans to invest approximately USD 845 million into pioneering next-generation battery technologies for electric vehicles (EVs). Six companies, including CATL (the globe's largest battery manufacturer) and major automakers like BYD and Geely, have been greenlit for government backing to advance all-solid-state batteries (ASSBs).

- As reported by the China Association of Automobile Manufacturers (CAAM) in August 2023, China has seen sales of 9.05 million passenger electric vehicles, breaking down to 6.26 million battery-only EVs (BEVs) and 2.79 million plug-in hybrid electric vehicles (PHEVs). In 2023, plug-in electric vehicles (both BEVs and PHEVs) accounted for 37% of China's total automotive sales, with market shares of 25% for BEVs and 12% for PHEVs.

- In June 2024, China's Ministry of Industry and Information Technology rolled out fresh directives for the battery sector. These guidelines aim to elevate the quality and innovation of lithium-ion batteries for electric vehicles, urging firms to pivot from merely expanding production capacity to enhancing technological innovations, especially in battery electrolyte solutions.

- Looking ahead, by 2030, China anticipates hosting 50 million electric vehicles, translating to a staggering annual electricity demand of 200 TWh for EV charging. This burgeoning demand underscores the potential for advancements in electric vehicle battery electrolytes within the nation.

- Given the surging adoption of EVs and ongoing technological strides, China is poised to retain its market dominance in the foreseeable future.

China Electric Vehicle Battery Electrolyte Industry Overview

The China Electric Vehicle Battery Electrolyte Market is semi-fragmented. Some of the major companies operating in the market (in no particular order) include Advanced Electrolyte Technologies LLC, Mitsubishi Chemical Holdings, Shenzhen Capchem Technology Co., Ltd, Nohms Technologies Inc., and Ohara Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Increasing Usage of Electric Vehicles, including BEVs, PHEVs, and HEVs

- 4.5.1.2 Favorable government policies to promote the usage of electric vehicles

- 4.5.2 Restraints

- 4.5.2.1 The Supply chain gap in battery materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-Ion Batteries

- 5.1.2 Lead-Acid Batteries

- 5.1.3 Other type of Batteries

- 5.2 Electrolyte Type

- 5.2.1 Liquid Electrolyte

- 5.2.2 Gel Electrolyte

- 5.2.3 Solid Electrolyte

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Advanced Electrolyte Technologies LLC

- 6.3.2 Mitsubishi Chemical Holdings

- 6.3.3 Shenzhen Capchem Technology Co., Ltd

- 6.3.4 Nohms Technologies Inc

- 6.3.5 Ohara Corporation

- 6.3.6 BASF SE

- 6.3.7 LG Chem Ltd

- 6.3.8 Targray Industries Inc.

- 6.3.9 SGS China

- 6.3.10 Ningbo Shanshan Co., LTD

- 6.4 Market Ranking/Share (%) Analysis

- 6.5 List of Other Prominent Players

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 R&D for advanced electrolyte material