|

市場調査レポート

商品コード

1636488

インドの電気自動車用バッテリー電解液:市場シェア分析、産業動向&統計、成長予測(2025~2030年)India Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの電気自動車用バッテリー電解液:市場シェア分析、産業動向&統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

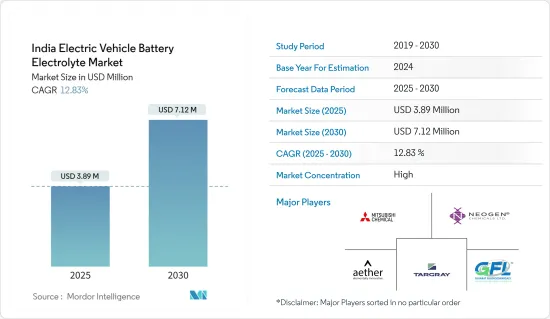

インドの電気自動車用バッテリー電解液市場規模は2025年に389万米ドルと推定され、予測期間(2025~2030年)のCAGRは12.83%で、2030年には712万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、電気自動車の普及拡大、政府施策、関連投資が市場を牽引するとみられます。

- 一方、原料の入手性と供給に関する課題は、市場にマイナスの影響を与えると予想されます。

- 電解質材料の継続的な研究開発は、市場に将来の成長機会をもたらすと予想されます。

- リチウムイオンバッテリータイプは、調査期間中、インドの電気自動車バッテリー電解液の最大市場になると予想されます。

インドの電気自動車用バッテリー電解液市場動向

リチウムイオンバッテリーが大きく成長

- リチウムイオンバッテリーは電気自動車(EV)革命の最前線にあります。優れたエネルギー密度と長寿命により、自動車産業がサステイナブルエネルギーソリューションにシフトする上で極めて重要な役割を担っています。

- 2023年4月、Neogen Chemicalsは日本のMU Ionic Solutions Corporationと提携し、製造能力を強化しました。この契約により、NeogenはMUIS独自の製造技術を活用できるようになりました。この戦略的な動きにより、Neogenはインドで年間3万MTの電解質溶液を生産できるようになり、国内のリチウムイオンバッテリーメーカーの需要増に直接対応できるようになりました。このような開発は、電気自動車用バッテリー電解液市場の成長を促進するものです。

- 同様に、2023年4月、Gujarat Fluorochemicals(GFL)は、インドにおけるバッテリーと電解槽の生産を対象に、3年間で6億米ドルの投資計画を発表しました。グジャラート州ダヘジにある同社の施設は、リチウムイオンバッテリーの重要な電解質塩である六フッ化リン酸リチウム(LiPF6)の生産から操業を開始します。年産1,800トンの生産能力からスタートするGFLは、リチウムイオンバッテリーの急増する需要に対応して規模を拡大する計画で、インドにおける電気自動車用電解液市場の拡大を裏付けています。

- 2023年12月、Ami Organicsは著名な世界的電解質企業と覚書を締結し、グジャラート州でのバッテリーセルと電解質の生産に道を開いた。インドの「メイク・イン・インディア」イニシアティブへのコミットメントを示すため、Ami Organicsは電解液専用生産施設に3,580万米ドルを投資します。

- ここ数年、リチウムイオンバッテリーの価格が急落し、関連部品の需要が高まっています。Bloomberg NEFの報告によると、2023年のリチウムイオンバッテリーの平均価格は139米ドル/KWhで、2014年以来5倍という驚異的な値下がりを示しています。この価格低下はリチウムイオンバッテリーの採用を加速させ、電解質市場の明るい未来を示唆しています。

- 前述のようなリチウムイオンバッテリーと電解液生産の動向を踏まえると、インドの電気自動車用バッテリー電解液市場は今後数年で大きく成長する可能性があります。

電気自動車の普及を促進する政府の奨励策

- 電気自動車(EV)は、運輸部門からの二酸化炭素排出を抑制する上で極めて重要な役割を果たしています。インド政府のFAMEインド計画は、電気自動車とハイブリッド車の採用を積極的に推進し、2030年までに全輸送手段の30%を電気自動車に移行することを目標としています。このような電気自動車導入の急増は、インドの電気自動車用バッテリー電解質市場に利益をもたらすと予想されています。

- これと並行して、インドの生産連動奨励金(PLI)制度は、30億9,000万米ドルの予算が承認され、国内の電気自動車製造を強化しています。PLI制度は、自動車メーカーに年間電気自動車販売額の13~15%の政府補助金を支給するものです。この優遇措置は、EV販売の拡大を目指すだけでなく、メーカーが新技術投資に伴うコストを軽減できるよう支援するものでもあります。その結果、このイニシアティブはインド全土で電気自動車用バッテリーの電解液の需要に拍車をかけています。

- さらに、Electric Mobility Promotion Scheme(EMPS)は、インドの電気自動車製造エコシステムを育成すると同時に、電気二輪車と電気三輪車の使用を奨励しています。EMPSでは、バッテリー容量1キロワット時あたり約60米ドルの補助金が交付されます。ただし、この補助金は工場出荷価格(税抜き車両価格)の15%または特定の上限(二輪車は約120米ドル、e-リキシャとe-カートは約300米ドル、e-自動二輪車は約600米ドル)に制限されています。このような取り組みにより、インドの電気自動車用バッテリーの電解質などの部品需要が高まると予想されます。

- 加えて、インドの電気自動車市場は近年一貫して上昇基調を示しています。国際エネルギー機関のデータによると、インドの電気自動車販売台数は2023年に8万2,000台に達し、前年比70%増という驚異的な伸びを示しました。このような勢いを考えると、インドにおける電気自動車の需要はさらに伸びることが予想され、電解液市場も活性化することが予想されます。

- こうした動向と市場開発を考慮すると、インドの電気自動車用バッテリー電解質市場展望は有望であると考えられます。

インドの電気自動車用バッテリー電解液産業概要

インドの電気自動車用バッテリー電解液市場は半固体化しています。主要企業(順不同)には、Neogen Chemicals、Gujarat Fluorochemicals、Mitsubishi Chemical Group Corporation、Targray Technology International Inc、Aether Industries Limitedなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車の導入を支援する政府の施策

- リチウムイオンバッテリーの価格低下

- 抑制要因

- 原料の入手可能性と供給の制限

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- バッテリータイプ

- 鉛蓄バッテリー

- リチウムイオンバッテリー

- その他

- 電解質タイプ

- 液体電解質

- ゲル電解質

- 固体電解質

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Ami Organics Electrolytes Private Ltd.

- Neogen Chemicals

- Gujarat Fluorochemicals

- 3M India

- BASF Shanshan Battery Materials Co.

- Targray Technology International Inc

- Aether Industries Limited

- Tatva Chintan Pharma Chem Limited

- Mitsubishi Chemical Group

- S K Industries

第7章 市場機会と今後の動向

- 電解質材料の研究開発

The India Electric Vehicle Battery Electrolyte Market size is estimated at USD 3.89 million in 2025, and is expected to reach USD 7.12 million by 2030, at a CAGR of 12.83% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the increasing adoption of electric vehicles, government policies, and associated investments in them are likely to drive the market.

- On the other hand, challenges associated with raw material availability and supply is expected to have a negative impact on the market.

- Continuous research and development in electrolyte materials is expected to provide future growth opportunities for the market.

- The lithium-ion battery type is expected to be the largest market for the India Electric Vehicle Battery Electrolyte during the study period.

India Electric Vehicle Battery Electrolyte Market Trends

Lithium-ion Battery to Grow Significantly

- Lithium-ion batteries are at the forefront of the electric vehicle (EV) revolution. Their superior energy density and extended life cycle make them pivotal to the automotive industry's shift toward sustainable energy solutions.

- In April 2023, Neogen Chemicals bolstered its manufacturing capabilities through a partnership with Japan's MU Ionic Solutions Corporation. The agreement allows Neogen to leverage MUIS's proprietary manufacturing technology. This strategic move positions Neogen to produce 30,000 MT annually of electrolyte solutions in India, directly addressing the rising demand from domestic lithium-ion cell manufacturers. Such developments are poised to fuel the growth of the electric vehicle battery electrolyte market.

- Similarly, in April 2023, Gujarat Fluorochemicals (GFL) announced a USD 600 million investment plan over three years, targeting battery and electrolyzer production in India. Their facility in Dahej, Gujarat, will commence operations with the production of Lithium hexafluorophosphate (LiPF6), a crucial electrolyte salt for lithium-ion batteries. Starting with a production capacity of 1800 tonnes per annum (tpa), GFL plans to scale up in response to the burgeoning demand for lithium-ion batteries, underscoring the expanding electric vehicle battery electrolyte market in India.

- In December 2023, Ami Organics entered into a Memorandum of Understanding with a prominent global electrolyte firm, paving the way for battery cell and electrolyte production in Gujarat. Demonstrating its commitment to India's "Make in India" initiative, Ami Organics is investing USD 35.8 million in a dedicated electrolyte production facility.

- Over the years, lithium-ion battery prices have plummeted, driving up demand for related components. Bloomberg NEF reports that the average lithium-ion battery price in 2023 was USD 139 USD/KWh, marking a staggering fivefold reduction since 2014. This price drop has accelerated the adoption of lithium-ion batteries, suggesting a bright future for the electrolyte market.

- Given the aforementioned trends in lithium-ion batteries and electrolyte production, the electric vehicle battery electrolyte market in India is poised for significant growth in the coming years.

Government Incentives to Raise Adoption of Electric Vehicles

- Electric vehicles (EVs) play a pivotal role in curbing carbon emissions from the transportation sector. The Indian government's FAME India scheme actively promotes the adoption of electric and hybrid vehicles, targeting a transition of 30% of total transportation to electric vehicles by 2030. This anticipated surge in electric vehicle adoption is poised to benefit India's electric vehicle battery electrolyte market.

- In a parallel effort, India's Production Linked Incentive (PLI) scheme, with an approved budget of USD 3.09 billion, has bolstered domestic electric vehicle manufacturing. The PLI scheme offers automakers a government grant ranging from 13-15% of their annual electric vehicle sales value. This incentive not only aims to amplify EV sales but also assists manufacturers in mitigating the costs associated with new technology investments. Consequently, this initiative has spurred demand for electrolytes in electric vehicle batteries across India.

- Furthermore, the Electric Mobility Promotion Scheme (EMPS) champions the use of electric two-wheelers and three-wheelers while simultaneously nurturing India's electric vehicle manufacturing ecosystem. Under the EMPS, a subsidy of approximately USD 60 is granted for each kilowatt hour of battery capacity. However, this subsidy is limited to 15% of the ex-factory cost (the vehicle's price at the factory gate before taxes) or specific caps: around USD 120 for two-wheelers, USD 300 for e-rickshaws and e-carts, and USD 600 for e-autos, whichever is lower for each category. Such initiatives are anticipated to elevate the demand for components like electrolytes in India's electric vehicle batteries.

- Additionally, India's electric vehicle market has shown a consistent upward trajectory in recent years. Data from the International Energy Agency reveals that electric car sales in India reached 82,000 units in 2023, marking a staggering 70% surge from the prior year. Given this momentum, the demand for electric vehicles in India is poised for further growth, which in turn is set to invigorate the electrolyte market.

- In light of these trends and developments, the outlook for India's Electric Vehicle Battery electrolyte Market appears promising.

India Electric Vehicle Battery Electrolyte Industry Overview

The India electric vehicle battery electrolyte market is semi-consolidated. Some of the major players (not in particular order) include Neogen Chemicals, Gujarat Fluorochemicals, Mitsubishi Chemical Group, Targray Technology International Inc, and Aether Industries Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government policies supporting adoption of electric vehicles

- 4.5.1.2 Declining Lithium-ion Battery Prices

- 4.5.2 Restraints

- 4.5.2.1 Limited avalibility and supply of raw materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lead Acid Batteries

- 5.1.2 Lithium-ion Batteries

- 5.1.3 Other Battery Types

- 5.2 Electrolyte Type

- 5.2.1 Liquid Electrolyte

- 5.2.2 Gel Electrolyte

- 5.2.3 Solid Electrolyte

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Ami Organics Electrolytes Private Ltd.

- 6.3.2 Neogen Chemicals

- 6.3.3 Gujarat Fluorochemicals

- 6.3.4 3M India

- 6.3.5 BASF Shanshan Battery Materials Co.

- 6.3.6 Targray Technology International Inc

- 6.3.7 Aether Industries Limited

- 6.3.8 Tatva Chintan Pharma Chem Limited

- 6.3.9 Mitsubishi Chemical Group

- 6.3.10 S K Industries

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Research & Development in electrolyte material