|

市場調査レポート

商品コード

1636509

イタリアの電気自動車用バッテリー電解液:市場シェア分析、産業動向、成長予測(2025~2030年)Italy Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| イタリアの電気自動車用バッテリー電解液:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

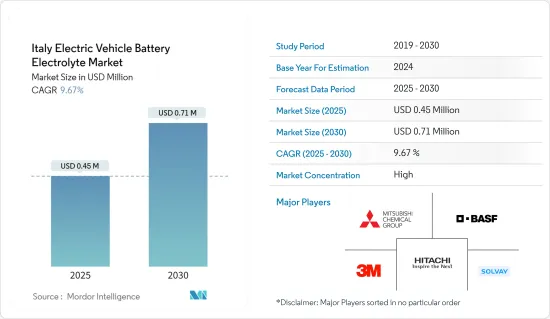

イタリアの電気自動車用バッテリー電解液市場規模は2025年に45万米ドルと推定され、予測期間(2025~2030年)のCAGRは9.67%で、2030年には71万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、電気自動車(EV)の需要拡大や政府の支援策などの要因が、予測期間中の市場を牽引すると予想されます。

- その一方で、サプライチェーンの問題が予測期間中の市場成長の妨げになると考えられます。

- 電解質材料の技術革新は今後数年間、市場に大きな機会をもたらすと期待されています。

イタリアの電気自動車用バッテリー電解質市場動向

電気自動車(EV)需要の拡大が市場を牽引

- イタリアの電気自動車(EV)市場は活況を呈しており、バッテリー電解液の需要を押し上げています。この動向は、近年のEV登録台数の大幅な増加によって裏付けられています。バッテリー電気自動車(BEV)の登録台数は、2017年のわずか2,000台から、2023年には6万6,000台へと急増しています。同様に、プラグインハイブリッド車(PHEV)の需要も2017年の2万9,000台から2023年には7万台に急増し、イタリアの消費者の間でEVが受け入れられつつあることを裏付けています。

- 2024年6月、イタリアはEV登録台数の顕著な急増を経験したが、これは主に、消費者の関心を効果的に刺激した新しいEcobonus奨励金の展開によるものです。6月だけで1万3,285台の完全電気自動車が新規登録され、2023年の同月から115.8%という驚異的な急上昇を記録しました。この増加により、電気自動車の市場シェアは8.3%に上昇し、前年の4.4%から大きく飛躍しました。2024年上半期の電気自動車登録台数は3万4,709台で、2023年の同時期から6.2%増加し、市場シェアは3.9%を維持しました。

- イタリア政府がEVの普及に力を入れていることは、さまざまな取り組みを通じて明らかです。例えば、2024年1月、政府は国産電気自動車(EV)の販売を強化するために9億3,000万ユーロを計上しました。このイニシアチブの主要目的は、低所得世帯に電気自動車を普及させることです。国産EVの購入を奨励することで、特に低所得世帯のEV販売台数の増加を見込んでいます。このような販売台数の増加は、電解質をはじめとするバッテリー部品の需要を押し上げると考えられます。

- イタリアは、財政的な優遇措置にとどまらず、2030年までに11万カ所の公共電気自動車充電ポイントを設置することを意欲的に目指しています。2023年8月現在、4万5,210カ所の充電ポイントがすでに稼働しており、その75%近くが急速充電器で、主に都市部やショッピングセンターに設置されています。

- ドイツやフランスを含む多くの欧州主要市場でEV市場の停滞が見られる中、イタリアの上昇基調は電動モビリティへの顕著なシフトを示しています。この動向は、EV販売が上昇を続ける中、バッテリー用電解液市場にとっても良い兆しです。

- まとめると、政府のインセンティブ、登録台数の急増、充電インフラの拡大が重なり、イタリアのEV用バッテリー電解質市場の成長にとって強固な環境が育まれています。

市場を独占するリチウムイオンバッテリーセグメント

- 電気自動車(EV)の普及拡大、サステイナブル輸送を求める政府の後押し、バッテリー開発における技術的進歩に後押しされ、リチウムイオンバッテリーセグメントが極めて重要な位置を占めています。高いエネルギー密度、軽量性、サイクル寿命の長さが評価され、リチウムイオンバッテリーはEVに選ばれています。EV市場の拡大に伴い、バッテリー効率、安全性、寿命を高める高性能電解液の需要が高まっている

- 現在、電気モビリティに軸足を移しているイタリアの堅調な自動車部門は、リチウムイオンバッテリー部門を強化しています。大手自動車メーカーがEV生産に投資を注ぎ込んでいるため、リチウムイオンバッテリーの製造は顕著に増加しています。この勢いを証明するように、Statevoltは2023年1月、イタリアにEV専用の45GWhリチウムイオンバッテリー施設を設立する計画を発表しました。この自動車シフトは、炭素排出を抑制しクリーンエネルギーを支持するイタリアの献身とシームレスに一致し、欧州連合(EU)の広範な野心と呼応しています。

- 電気自動車用バッテリー電解液市場は、リチウムイオンバッテリーの価格急落に大きく左右されます。2023年には、リチウムイオンバッテリーの平均価格は1キロワット時(kWh)当たり約139米ドルまで下落し、2013年以来82%以上の著しい下落を示しました。予測では、2025年までに113米ドル/kWh以下までさらに下落し、2030年には80米ドル/kWhを目指す可能性があります。

- バッテリーのコストが下がれば、電気自動車全体の価格もそれに追随し、消費者にとっての値ごろ感と入手しやすさが向上します。価格の低下により電気自動車需要の増加が予想されるため、最高級のバッテリー電解液に対するニーズが高まっている

- さらに、価格が低下するにつれて、メーカーはバッテリーの性能と安全性を強化する最先端の電解液配合に投資する傾向が強まっています。この動向を示すものとして、スタンFord大学の分校で先進的なバッテリー用電解質を専門とするFeon Energyは、革新的な電解質で2024年6月に610万米ドルのシード資金を獲得し、リチウム金属バッテリーのUN38.3認証を取得しました。このような進歩は、電解質セグメントの技術革新を促進し、バッテリー効率を高め、軽量化し、エネルギー密度を高める製品への道を開きます。

- このような力学を考えると、イタリアのリチウムイオンバッテリーセグメント、特に電気自動車用バッテリー電解液の領域は、技術革新とバッテリー価格の下落に後押しされ、電気自動車の普及を促進し、上昇基調にあります。

イタリアの電気自動車用バッテリー電解質産業概要

イタリアの電気自動車用バッテリー電解液市場は半固体化しています。主要参入企業には、Mitsubishi Chemical Group Corporation、3M、Hitachi、Solvay SA、BASF SEなどがあります(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車(EV)の需要拡大

- 政府の支援策

- 抑制要因

- サプライチェーンの課題

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- バッテリータイプ

- リチウムイオンバッテリー

- 鉛蓄バッテリー

- その他

- 電解質タイプ

- 液体電解質

- ゲル電解質

- 固体電解質

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Mitsubishi Chemical Group

- 3M

- Arkema

- Daikin Industries

- Dow Chemical Company

- BASF SE

- Solvay SA

- Asahi Kasei Corporation

- Hitachi, Ltd.

- Cabot Corporation

- 市場ランキング/シェア分析

- その他の著名な企業一覧

第7章 市場機会と今後の動向

- 電解質材料の革新

目次

Product Code: 50003839

The Italy Electric Vehicle Battery Electrolyte Market size is estimated at USD 0.45 million in 2025, and is expected to reach USD 0.71 million by 2030, at a CAGR of 9.67% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the growing demand for electric vehicle (EVs) and suppotive government initiatives are expected to drive the market during the forecast period.

- On the other hand, supply chain challanges are likely to hinder the market growth during the forecast period.

- Nevertheless, innovations in electrolyte materials are expected to provide significant opportunities for the market in the coming years.

Italy Electric Vehicle Battery Electrolyte Market Trends

Growing Demand for Electric Vehicles (EVs) to Drive the Market

- Italy's electric vehicle (EV) market is booming, driving up the demand for battery electrolytes. This trend is underscored by a significant uptick in EV registrations over recent years. Registrations for Battery Electric Vehicles (BEVs) surged from a mere 2,000 units in 2017 to an impressive 66,000 units in 2023. Likewise, Plug-in Hybrid Electric Vehicles (PHEVs) saw their demand leap from 29,000 units in 2017 to 70,000 units in 2023, underscoring the growing acceptance of EVs among Italian consumers.

- In June 2024, Italy experienced a notable spike in EV registrations, primarily due to the rollout of the new Ecobonus incentive, which has effectively piqued consumer interest. June alone witnessed the registration of 13,285 new fully electric vehicles, marking a staggering 115.8% jump from the same month in 2023. This upswing elevated the market share of electric vehicles to 8.3%, a significant leap from the previous year's 4.4%. In the first half of 2024, electric vehicle registrations totaled 34,709, reflecting a 6.2% growth from the same timeframe in 2023, and sustaining a market share of 3.9%.

- The Italian government's dedication to promoting EV adoption is evident through various initiatives. For example, in January 2024, the government earmarked 930 million euros to bolster the sales of locally produced electric vehicles (EVs). A primary objective of this initiative is to champion electromobility among lower-income households. By incentivizing the purchase of domestically produced EVs, especially for these families, the government anticipates a boost in overall EV sales. Such an uptick in sales is poised to drive up the demand for battery components, notably electrolytes.

- Beyond financial incentives, Italy is ambitiously aiming to set up 110,000 public electric vehicle charging points by 2030. As of August 2023, 45,210 charging points were already operational, with nearly 75% being fast chargers, predominantly situated in urban locales and shopping centers.

- While many major European markets, including Germany and France, saw stagnation in their EV markets, Italy's upward trajectory signals a pronounced shift towards electric mobility. This trend bodes well for the battery electrolyte market as EV sales continue their ascent.

- In summary, the confluence of government incentives, surging registrations, and an expanding charging infrastructure is cultivating a robust environment for the growth of Italy's EV battery electrolyte market, all fueled by the nation's escalating appetite for electric vehicles.

Lithium-Ion Batteries Segment to Dominate the Market

- Driven by the rising adoption of electric vehicles (EVs), government pushes for sustainable transportation, and technological strides in battery development, the lithium-ion battery segment is pivotal. Valued for their high energy density, lightweight nature, and extended cycle life, lithium-ion batteries are the preferred choice for EVs. As the EV market expands, there's a growing demand for high-performance electrolytes that boost battery efficiency, safety, and lifespan.

- Italy's robust automotive sector, now pivoting towards electric mobility, bolsters the lithium-ion battery segment. With major automakers pouring investments into EV production, lithium-ion battery manufacturing is witnessing a notable uptick. A testament to this momentum, Statevolt announced in January 2023 its plans to set up a 45 GWh lithium-ion battery facility in Italy, specifically for EVs. This automotive shift aligns seamlessly with Italy's dedication to curbing carbon emissions and championing clean energy, echoing the broader ambitions of the European Union.

- The electric vehicle battery electrolyte market is significantly swayed by the plummeting prices of lithium-ion batteries. In 2023, the average price of lithium-ion batteries dipped to approximately USD 139 per kilowatt-hour (kWh), showcasing a remarkable decline of over 82% since 2013. Forecasts suggest a further drop to below USD 113/kWh by 2025, with a potential target of USD 80/kWh by 2030.

- As battery costs decrease, the overall price of electric vehicles follows suit, enhancing their affordability and accessibility for consumers. This anticipated rise in EV demand, spurred by lower prices, underscores the growing need for top-tier battery electrolytes.

- Furthermore, as prices decline, manufacturers are more inclined to invest in cutting-edge electrolyte formulations that bolster battery performance and safety. Highlighting this trend, Feon Energy, a Stanford University offshoot specializing in advanced battery electrolytes, clinched USD 6.1 million in seed funding in June 2024 for its innovative electrolytes and achieved UN 38.3 certification for its lithium-metal batteries. Such advancements catalyze innovation in the electrolyte domain, paving the way for products that amplify battery efficiency, lighten weight, and boost energy density.

- Given these dynamics, Italy's lithium-ion battery segment, especially in the realm of electric vehicle battery electrolytes, is on an upward trajectory, buoyed by technological innovations and falling battery prices that facilitate the broader embrace of electric vehicles.

Italy Electric Vehicle Battery Electrolyte Industry Overview

The Italy electric vehicle battery electrolyte market is semi-consolidated. Some of the major players include (not in particular order) Mitsubishi Chemical Group, 3M, Hitachi Ltd., Solvay SA, and BASF SE, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Demand for Electric Vehicles (EVs)

- 4.5.1.2 Supportive Government Initiatives

- 4.5.2 Restraints

- 4.5.2.1 Supply Chain Challanges

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-Ion Batteries

- 5.1.2 Lead-Acid Batteries

- 5.1.3 Others

- 5.2 Electrolyte Type

- 5.2.1 Liquid Electrolyte

- 5.2.2 Gel Electrolyte

- 5.2.3 Solid Electrolyte

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Mitsubishi Chemical Group

- 6.3.2 3M

- 6.3.3 Arkema

- 6.3.4 Daikin Industries

- 6.3.5 Dow Chemical Company

- 6.3.6 BASF SE

- 6.3.7 Solvay SA

- 6.3.8 Asahi Kasei Corporation

- 6.3.9 Hitachi, Ltd.

- 6.3.10 Cabot Corporation

- 6.4 Market Ranking/Share Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovations in Electrolyte Materials