|

市場調査レポート

商品コード

1636478

ASEAN各国の電気自動車用バッテリー電解液:市場シェア分析、産業動向、成長予測(2025年~2030年)ASEAN Countries Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ASEAN各国の電気自動車用バッテリー電解液:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

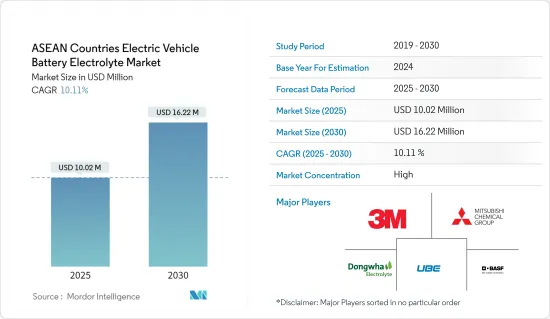

ASEAN諸国の電気自動車用バッテリー電解液市場規模は、2025年に1,002万米ドルと推定され、予測期間(2025~2030年)のCAGRは10.11%で、2030年には1,622万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、電気自動車(EV)の急速な普及と政府の支援策に後押しされ、市場は成長します。

- 逆に、サプライチェーンの混乱が成長の課題となる可能性もあります。

- しかし、電解質配合の進歩は近い将来、市場に有利な機会をもたらします。

- 同地域では、シンガポールが際立っており、同国のEVエコシステムを強化するための協調的な取り組みにより、顕著な成長が見込まれています。

ASEAN諸国の電気自動車用バッテリー電解液市場動向

リチウムイオンバッテリーセグメントが市場を独占

- リチウムイオンバッテリーセグメントは、電気自動車の急速な普及とバッテリー技術の革新に後押しされ、ASEAN地域の電気自動車(EV)用バッテリー電解液市場の極めて重要なコンポーネントとなっています。

- 地域政府が環境に優しい輸送手段を支持し、EVに対する消費者の嗜好が高まる中、効率的で高性能なバッテリーへの需要が高まっています。電解質は、バッテリーの性能を高め、安全性を確保し、寿命を延ばす上で重要な役割を果たしています。

- リチウムイオンバッテリーセグメント拡大の主要原動力は、バッテリーコストの顕著な低下です。例えば、2023年のリチウムイオンバッテリーの平均価格は1キロワット時(kWh)当たり約139米ドルまで下落し、2013年以来82%以上の著しい下落を示しました。予測によると、2025年には113米ドル/kWhを下回り、2030年には80米ドル/kWhに達する可能性があります。

- このようなバッテリー価格の下落傾向は、消費者にとって電気自動車の購入しやすさを向上させるだけでなく、メーカーが先進的なバッテリー技術や高級電解質に取り組むきっかけとなり、市場の需要を増幅させる。

- さらに、持続可能性はリチウムイオンバッテリーセグメントで極めて重要な力として浮上しています。環境意識の高まりに伴い、メーカーはサステイナブル材料から作られた環境に優しい電解質ソリューションに軸足を移しつつあります。このグリーンシフトは、消費者の嗜好と共鳴するだけでなく、バッテリー生産における環境フットプリントを抑制することを目的とした規制上の義務とも一致しています。

- 2024年7月、LG Energy SolutionとHyundai Motor Corpは、インドネシアに容量10GWhのEVバッテリー製造施設を開設しました。2024年10月、インドネシアは世界のEVハブになるという野心をさらに強め、中国のContemporary Amperex Technology(CATL)との合弁事業を発表し、東南アジアでのリチウムイオンバッテリー生産に向けて12億米ドルを拠出しました。

- 結論として、投資の増加と価格の下落に後押しされ、リチウムイオン技術の採用がこの地域で加速し、今後数年間で市場が大幅に成長する道が開かれます。

重要な役割を果たすと期待されるシンガポール

- シンガポールは、ASEANにおけるEV充電インフラの最先端を走っており、1,800カ所以上の公共充電ポイントが利用可能です。シンガポール政府は、2030年末までにさらに6万カ所の充電ポイントを設置する計画です。

- 2021~2025年にかけて、シンガポール政府はEV普及を促進するために2,200万米ドルを計上しました。このイニシアチブは、私有地の充電器の数を増やし、充電インフラ全体を強化することを目的としています。同時に、シンガポールは自国をEVセグメントの極めて重要な研究開発拠点と位置づけ、多国籍企業や新興企業の投資を誘致し、現地のEVエコシステムを育成しています。

- 公害の抑制に取り組むシンガポール政府は、電動モビリティを支持しています。この推進により、EVの販売台数が増加すると予想されます。特に、シンガポールは2040年までに内燃機関からよりクリーンなエネルギー自動車への移行を目指しています。その牽引役となるのが、シンガポールの2040年グリーンエネルギー自動車目標に向けた取り組みの舵取りを行う、新設の国民生用電子機器気自動車センター(NEVC)です。このシフトは、近い将来、バッテリー材料、特に電解質の需要を高めることになります。

- 陸運庁の報告によると、シンガポールでのEV販売は増加傾向にあります。2024年1月から7月の間に、シンガポールでは6,019台のバッテリー電気自動車が登録されました。これは、2023年の同時期の登録台数1,892台から32.4%増と大きく伸びています。

- EV市場の急成長は、ゼロエミッションによる大気環境の改善や温室効果ガスの抑制といった環境への恩恵だけでなく、気候変動との世界の闘いにおいても重要な役割を果たしています。

- 消費者の嗜好と規制のサポートが一致していることから、シンガポールにおける電気自動車用バッテリー電解液の需要は、当分の間増加すると考えられます。

ASEAN諸国の電気自動車用バッテリー電解液質産業概要

ASEAN諸国の電気自動車用バッテリー電解液市場は半固体化しています。主要参入企業としては、Mitsubishi Chemical Group Corporation、3M、Dongwha Eletrolyte、BASF SE、UBE Corp.などが挙げられます(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車(EV)普及率の上昇

- 政府の支援策

- 抑制要因

- サプライチェーンの混乱

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- バッテリータイプ

- リチウムイオンバッテリー

- 鉛蓄バッテリー

- その他

- 電解質タイプ

- 液体電解質

- ゲル電解質

- 固体電解質

- 地域

- マレーシア

- タイ

- インドネシア

- シンガポール

- その他のASEAN諸国

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Mitsubishi Chemical Group

- 3M

- Dongwha Eletrolyte

- UBE Corp.

- BASF SE

- Hitachi, Ltd.

- Cabot Corporation

- Umicore N.V

- 市場ランキング/シェア分析

- その他の著名な企業一覧

第7章 市場機会と今後の動向

- 電解質配合の革新

目次

Product Code: 50003746

The ASEAN Countries Electric Vehicle Battery Electrolyte Market size is estimated at USD 10.02 million in 2025, and is expected to reach USD 16.22 million by 2030, at a CAGR of 10.11% during the forecast period (2025-2030).

Key Highlights

- In the medium term, the market is poised for growth, fueled by the surging adoption of electric vehicles (EVs) and supportive government initiatives.

- Conversely, disruptions in the supply chain may pose challenges to this growth.

- However, advancements in electrolyte formulations present lucrative opportunities for the market in the near future.

- Within the region, Singapore stands out, anticipating notable growth, thanks to its concerted efforts to bolster the country's EV ecosystem.

ASEAN Countries Electric Vehicle Battery Electrolyte Market Trends

Lithium-Ion Batteries Segment to Dominate the Market

- The lithium-ion battery segment stands as a pivotal component of the electric vehicle (EV) battery electrolyte market in the ASEAN region, propelled by the swift uptake of electric vehicles and innovations in battery technology.

- With regional governments championing greener transportation and a growing consumer preference for EVs, the appetite for efficient, high-performance batteries is on the rise. Electrolytes play a vital role in boosting battery performance, ensuring safety, and extending longevity.

- A key driver behind the lithium-ion battery segment's expansion is the notable drop in battery costs. For example, in 2023, the average price of lithium-ion batteries dipped to approximately USD 139 per kilowatt-hour (kWh), marking a remarkable decline of over 82% since 2013. Forecasts suggest prices might slide below USD 113/kWh by 2025 and could touch USD 80/kWh by 2030.

- This downward trajectory in battery prices not only enhances the affordability of electric vehicles for consumers but also spurs manufacturers to delve into advanced battery technologies and premium electrolytes, amplifying market demand.

- Moreover, sustainability is emerging as a pivotal force in the lithium-ion battery segment. With a surge in environmental consciousness, manufacturers are pivoting towards eco-friendly electrolyte solutions crafted from sustainable materials. This green shift not only resonates with consumer preferences but also dovetails with regulatory mandates aimed at curbing the environmental footprint of battery production.

- In July 2024, LG Energy Solution and Hyundai Motor Corp inaugurated a 10 GWh capacity EV battery manufacturing facility in Indonesia. Furthering its ambition to be a global EV hub, Indonesia, in October 2024, unveiled a joint venture with China's Contemporary Amperex Technology Co Ltd (CATL), committing a substantial USD 1.2 billion towards lithium-ion battery production in the Southeast Asian landscape.

- In conclusion, driven by increasing investments and declining prices, the adoption of lithium-ion technology is set to accelerate in the region, paving the way for substantial market growth in the years ahead.

Singapore Expected to Play a Key Role

- Singapore has been at the forefront of EV charging infrastructure in ASEAN, with more than 1,800 public charging points available. The Government of Singapore plans to install 60,000 more charging points by the end of 2030.

- From 2021 to 2025, the Singapore government has earmarked USD 22 million to boost EV adoption. This initiative aims to bolster the number of chargers on private properties, enhancing the overall charging infrastructure. Concurrently, Singapore has positioned itself as a pivotal R&D hub for the EV sector, attracting investments from multinationals and startups alike, thereby nurturing a robust local EV ecosystem.

- With a commitment to curbing pollution, the Singapore government is championing electric mobility. This push is anticipated to drive up EV sales. Notably, Singapore aims to transition from internal combustion engines to cleaner-energy vehicles by 2040. Leading this charge is the newly established National Electric Vehicle Centre (NEVC), steering efforts towards Singapore's 2040 green energy vehicle goal. This shift is poised to elevate the demand for battery materials, particularly electrolytes, in the near future.

- As reported by the Land Transport Authority, EV sales in Singapore are on the rise. Between January-July 2024, the country registered 6,019 battery electric vehicles. This marks a significant jump from 1,892 registrations during the same period in 2023, representing an 32.4% increase.

- The swift growth of the EV market not only benefits the environment-due to zero emissions improving air quality and curbing greenhouse gases-but also plays a vital role in the global fight against climate change.

- Given the alignment of consumer preferences and regulatory support, the demand for electric vehicle battery electrolytes in Singapore is set to rise in the foreseeable future.

ASEAN Countries Electric Vehicle Battery Electrolyte Industry Overview

The ASEAN Countries' electric vehicle battery electrolyte market is semi-consolidated. Some of the major players include (not in particular order) Mitsubishi Chemical Group, 3M, Dongwha Eletrolyte, BASF SE, and UBE Corp. among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Electric Vehicle (EV) Adoption

- 4.5.1.2 Supportive Government Initiatives

- 4.5.2 Restraints

- 4.5.2.1 Supply Chain Disruptions

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Force Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-Ion Batteries

- 5.1.2 Lead-Acid Batteries

- 5.1.3 Others

- 5.2 Electrolyte Type

- 5.2.1 Liquid Electrolyte

- 5.2.2 Gel Electrolyte

- 5.2.3 Solid Electrolyte

- 5.3 Geography

- 5.3.1 Malaysia

- 5.3.2 Thailand

- 5.3.3 Indonesia

- 5.3.4 Singapore

- 5.3.5 Rest of ASEAN Countries

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Mitsubishi Chemical Group

- 6.3.2 3M

- 6.3.3 Dongwha Eletrolyte

- 6.3.4 UBE Corp.

- 6.3.5 BASF SE

- 6.3.6 Hitachi, Ltd.

- 6.3.7 Cabot Corporation

- 6.3.8 Umicore N.V

- 6.4 Market Ranking/Share Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovations in Electrolyte Formulations