|

市場調査レポート

商品コード

1636255

冷凍食品ロジスティクス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Frozen Food Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 冷凍食品ロジスティクス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

冷凍食品ロジスティクスの市場規模は2025年に309億4,000万米ドルと推定され、予測期間中(2025-2030年)のCAGRは11.28%で、2030年には527億9,000万米ドルに達すると予測されます。

主なハイライト

- 冷凍食品需要の急増と都市化の進展が主に冷凍食品ロジスティクス市場を牽引しています。

- 過去数年間、プレミアム冷凍食品業界は著しい成長を遂げてきました。一流の、便利で栄養価の高い食品を求める消費者の欲求の高まりが、主にこの急成長を後押ししています。この動向は、バランスの取れた食事とすぐに食べられる食事を求める健康志向の人々に特に顕著です。

- さらに消費者は、味と栄養価を効果的に保持する最新の冷凍技術によって可能になった製品の優れた品質をますます認めるようになっています。

- 特筆すべきは、都市部の富裕層が、こうした高級冷凍食品の売れ行きの先頭に立っていることです。これらの製品は、グルメなレシピ、責任ある原料調達、最先端の味を誇ることが多いです。

- この需要の急増は、家庭料理、料理実験、レストラン並みの食事への欲求へと消費者がシフトしていることを反映しています。これは、品質、味、栄養面で妥協を許さない、舌の肥えた食通向けの動向です。

- 2023年には、冷凍食品の小売売上高は7.9%急増し、742億米ドルに達しました。これは、最近の報告書で強調されているように、過去3年間で100億米ドルの顕著な増加を示しています。多くの食料品分野と同様、冷凍食品のドル建て金額の伸びは、主にインフレによる価格上昇に後押しされたものです。

- その結果、冷凍食品に対する消費者行動は変化しています。米国冷凍食品協会(AFFI)と食品産業協会(FMI)が共同で発行した「小売業における冷凍食品の力2023」レポートによると、消費者は冷凍食品に1個当たり平均4.99米ドルを支払っていることが明らかになった。これは2023年から13.5%の上昇を示し、過去3年間では29.6%の大幅な飛躍となった。

- 冷凍食品売上では、冷凍食品とデザートがリードしており、2023年にはそれぞれ266億米ドルと154億米ドルを稼ぎ出します。これらに続くのは果物/野菜、水産物、肉/鶏肉で、それぞれ同年に81億米ドル、70億米ドル、57億米ドルの売上高を誇る。

冷凍食品ロジスティクスの市場動向

業界を牽引する冷凍食品需要

近年、調理済み食品市場は、消費者の嗜好の変化に合わせた製品イノベーションの急増に牽引され、著しい進化を遂げています。この変化は、利便性と味覚の嗜好が最優先されるインドで特に顕著です。

消費者は、調理済み食品業界において、より健康的で自然な選択肢を求めるようになっています。そのため、クリーンなラベル、最小限の添加物、オーガニック原材料を使用した製品に対する需要が高まっています。さらに、植物性食品やヴィーガン食品に対する需要も高まっています。植物ベースの食生活を採用したり、肉の消費量を減らしたりする個人が増えるにつれ、植物ベースやビーガンに適した調理済み食品の需要が高まっています。

この業界の成長の鍵は、既存企業と新興企業の両方によるイノベーションへの揺るぎないコミットメントです。ニールセンの最近の調査では、特にインドにおいて、消費者がより健康的な調理済み食品を選ぶようになったことが強調されています。同調査によると、インドの消費者の72%が栄養バランスの取れた調理済み食品を積極的に求めており、健康志向の高まりがうかがえます。

これに応えるため、企業は技術と調理技術を駆使して、栄養ニーズを満たし、多様なインド人の味覚に対応する製品を作りつつあります。これには、グルテンフリー、オーガニック、郷土料理風のオプションのイントロダクションが含まれます。

調理済み食品ブランドと栄養研究機関や専門家との提携は、製品の提供を拡大し、消費者の認識を再構築して、調理済み食品をより健康的な食事の選択肢として位置付けています。

欧州が市場で突出した地位を占めています。

2023年には、ドイツの総冷凍食品販売量は404万3,000トンに達し、2022年の390万9,000トンから3.4%増加しました。この急増により、売上高は初めて400万トンの節目を超えました。

家庭外市場は6.5%の伸びを示し、2022年の193万5,000トンから2023年には206万1,000トンとなった。この成長により、市場は200万トンの大台を突破しました。

食品小売・家庭サービス業界では、2023年の冷凍食品販売量は198万2,000トンに達し、2022年の197万4,000トンから0.4%の小幅増となった。注目すべきは、この数字がCOVID-19パンデミック前の2019年のレベルである186万1,000トンを6.5%上回っていることです。

一人当たりの冷凍食品消費量は、2022年の47.7 kgから2023年には49.4 kgとなり、過去最高を記録しました。世帯レベルでは、消費量は3 kg増加し、2022年の96.4 kgから2023年には99.4 kgに達しました。

冷凍食品ロジスティクス業界の概要

冷凍食品ロジスティクス市場は、その性質上、断片化されています。Lineage Logistics、Americold Logistics、Swire Cold Storage、Nichirei Logistics、VersaCold Logistics Servicesといった大手企業がコールドチェーン物流業界をリードしています。

これらの主要企業は、冷凍食品業界特有のニーズに合わせて、温度管理された保管、輸送、流通などの一連のサービスを提供しています。これらの企業は、広範なネットワーク、最先端技術、冷凍品管理の専門的ノウハウを活用することで、市場での競合優位性を確固たるものにしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 現在の市場シナリオ

- 市場力学

- 促進要因

- 市場を牽引するeコマースの台頭

- 消費者のライフスタイルの変化が市場を牽引

- 抑制要因

- コールドチェーン物流の維持に伴う高い運営コスト

- 市場に影響を与える規制コンプライアンス

- 機会

- 市場を牽引する技術の進歩

- 促進要因

- バリューチェーン/サプライチェーン分析

- 政府の規制、貿易協定、イニシアチブ

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 地政学とパンデミックが市場に与える影響

第5章 市場セグメンテーション

- 製品別

- RTE

- RTC

- 製品タイプ別

- 冷凍果物・野菜

- 冷凍肉・魚

- 冷凍調理済みレディミール

- 冷凍デザート

- 冷凍スナック

- その他の製品タイプ

- 輸送別

- 道路

- 鉄道

- 海路

- 航空

- 地域別

- 北米

- 欧州

- アジア太平洋

- 南米

- 中東・アフリカ

第6章 競合情勢

- 市場集中の概要

- 企業プロファイル

- Lineage Logistics

- Americold Logistics

- Swire Cold Storage

- Nichirei Logistics

- VersaCold Logistics Services

- Burris Logistics

- Kloosterboer

- NewCold

- Interstate Cold Storage

- Preferred Freezer Services*

- その他の企業

第7章 市場の将来

第8章 付録

- マクロ経済指標

- 資本フローの洞察(運輸・倉庫部門への投資)

- eコマースと消費関連統計

- 対外貿易統計

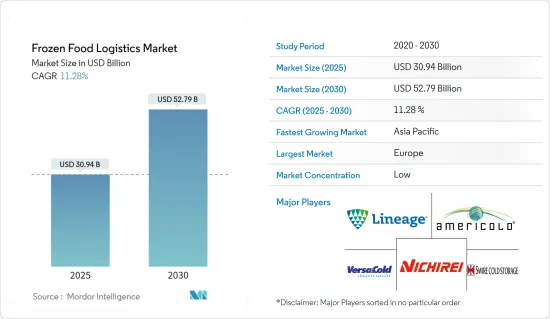

The Frozen Food Logistics Market size is estimated at USD 30.94 billion in 2025, and is expected to reach USD 52.79 billion by 2030, at a CAGR of 11.28% during the forecast period (2025-2030).

Key Highlights

- A surge in demand for frozen food products and growing urbanization mainly drive the frozen food logistics market.

- Over the past few years, the premium frozen food industry has witnessed remarkable growth. A heightened consumer appetite for top-tier, convenient, and nutritious food choices predominantly propels this upsurge. This trend is especially pronounced among health-conscious individuals seeking balanced diets and the swiftness of ready-to-eat meals.

- Moreover, consumers increasingly acknowledge the superior quality of products made possible by modern freezing technologies, which effectively retain taste and nutritional value.

- Notably, affluent urban households are spearheading the sales of these premium frozen offerings. These products often boast gourmet recipes, responsibly sourced ingredients, and cutting-edge flavors.

- This surge in demand mirrors a broader consumer shift toward home cooking, culinary experimentation, and a desire for restaurant-grade meals-all enjoyed from the comfort of their homes. It is a trend tailored for discerning food enthusiasts unwilling to compromise on quality, taste, or nutrition.

- In 2023, retail sales of frozen foods surged by 7.9%, hitting USD 74.2 billion. This marked a notable USD 10 billion increase over the last three years, as highlighted in a recent report. Like many grocery segments, the growth of frozen food's value in dollars was primarily fueled by inflation-driven price hikes.

- Consequently, consumer behavior toward frozen food is changing. The Power of Frozen in Retail 2023 report, a collaboration between the American Frozen Food Institute (AFFI) and the Food Industry Association (FMI), revealed that consumers shelled out an average of USD 4.99 per unit for frozen items. This represented a 13.5% uptick from 2023 and a substantial 29.6% leap in the last three years.

- Frozen meals and desserts are leading the pack in frozen food sales, raking in USD 26.6 billion and USD 15.4 billion, respectively, in 2023. These are followed by fruits/vegetables, seafood, and meat/poultry, each boasting sales figures of USD 8.1 billion, USD 7 billion, and USD 5.7 billion, respectively, in the same year.

Frozen Food Logistics Market Trends

Demand for Frozen Food Products Gaining Traction in the Industry

The ready-to-eat market has witnessed a significant evolution in recent years, driven by a surge in product innovation tailored to changing consumer preferences. This transformation is especially pronounced in India, where convenience and taste preferences are paramount.

Consumers are increasingly gravitating toward healthier, natural options in the ready-to-eat industry. This has increased demand for products with clean labels, minimal additives, and organic ingredients. Furthermore, there is a growing appetite for plant-based and vegan choices. As more individuals adopt plant-based diets or reduce meat consumption, the demand for plant-based or vegan-friendly ready-to-eat options is rising.

Key to the industry's growth is the unwavering commitment to innovation by both established players and startups. Recent research from Nielsen underscores a significant consumer pivot toward healthier ready-to-eat choices, particularly in India. The study indicates that 72% of Indian consumers actively seek nutritious, well-balanced, ready-to-eat meals, showcasing a heightened health consciousness.

In response, companies are harnessing technology and culinary skills to craft products that meet nutritional needs and cater to the diverse Indian palate. This includes the introduction of gluten-free, organic, and locally-inspired options.

Partnerships between ready-to-eat brands and nutrition institutes or experts are broadening product offerings and reshaping consumer perceptions, positioning ready-to-eat foods as a healthier meal choice.

Europe is Holding a Prominent Position in the Market

In 2023, Germany's total frozen food sales reached 4.043 million tonnes, marking a 3.4% increase from 3.909 million tonnes in 2022. This surge pushed sales past the 4-million-tonne milestone for the first time.

The out-of-home market saw a notable 6.5% uptick in sales, hitting 2.061 million tonnes in 2023, up from 1.935 million tonnes in 2022. This growth propelled the market past the 2-million-tonne threshold.

Within the food retail and home services industry, frozen food sales in 2023 reached 1.982 million tonnes, reflecting a modest 0.4% increase from 1.974 million tonnes in 2022. Notably, this figure stood 6.5% higher than the pre-COVID-19-pandemic levels in 2019, which were at 1.861 million tonnes.

Individually, per capita consumption of frozen food hit a record high of 49.4 kg in 2023, up from 47.7 kg in 2022. At the household level, consumption saw a 3 kg increase, reaching 99.4 kg in 2023, compared to 96.4 kg in 2022.

Frozen Food Logistics Industry Overview

The frozen food logistics market is fragmented in nature. Giants like Lineage Logistics, Americold Logistics, Swire Cold Storage, Nichirei Logistics, and VersaCold Logistics Services are leading the pack in the cold chain logistics industry.

These key players provide a suite of services, including temperature-controlled storage, transportation, and distribution, tailored to the specific needs of the frozen food industry. These companies have solidified their competitive edge in the market by leveraging expansive networks, cutting-edge technologies, and specialized know-how in frozen goods management.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Rise in E-Commerce Driving The Market

- 4.2.1.2 Changing Consumer Lifestyles Driving The Market

- 4.2.2 Restraints

- 4.2.2.1 High Operating Costs Associated With Maintaining Cold Chain Logistics

- 4.2.2.2 Regulatory Compliances Affecting The Market

- 4.2.3 Opportunities

- 4.2.3.1 Technological Advancements Driving The Market

- 4.2.1 Drivers

- 4.3 Value Chain/Supply Chain Analysis

- 4.4 Government Regulations, Trade Agreements, and Initiatives

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Impact of Geopolitics and Pandemics on the Market

5 MARKET SEGMENTATION

- 5.1 By Product

- 5.1.1 Ready-to-eat

- 5.1.2 Ready-to-cook

- 5.2 By Product Type

- 5.2.1 Frozen Fruits and Vegetables

- 5.2.2 Frozen Meat and Fish

- 5.2.3 Frozen-Cooked Ready Meals

- 5.2.4 Frozen Desserts

- 5.2.5 Frozen Snacks

- 5.2.6 Other Product Types

- 5.3 By Transportation

- 5.3.1 Roadways

- 5.3.2 Railways

- 5.3.3 Seaways

- 5.3.4 Airways

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Lineage Logistics

- 6.2.2 Americold Logistics

- 6.2.3 Swire Cold Storage

- 6.2.4 Nichirei Logistics

- 6.2.5 VersaCold Logistics Services

- 6.2.6 Burris Logistics

- 6.2.7 Kloosterboer

- 6.2.8 NewCold

- 6.2.9 Interstate Cold Storage

- 6.2.10 Preferred Freezer Services*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators

- 8.2 Insight Into Capital Flows (Investments In Transport and Storage Sector)

- 8.3 E-commerce and Consumer Spending-related Statistics

- 8.4 External Trade Statistics