南米の揚水蓄電:市場シェア分析、産業動向、成長予測(2025~2030年)

South America Pumped Hydro Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636165

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

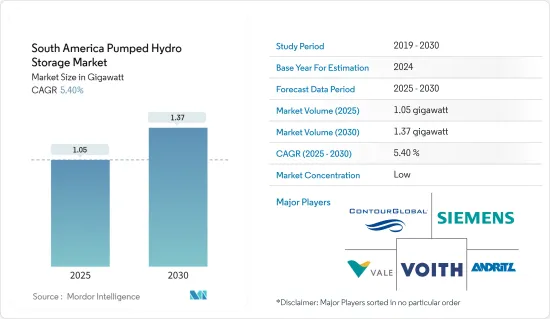

南米の揚水蓄電の市場規模は2025年に1.05ギガワットと推定され、予測期間(2025-2030年)のCAGRは5.4%で、2030年には1.37ギガワットに達すると予測されます。

主なハイライト

- 長期的には、再生可能エネルギー統合に向けた政府目標の増加と水力発電の潜在力が、予測期間中のポンプ式水力発電市場の成長を牽引するとみられます。

- 一方、他のエネルギー貯蔵技術の浸透は、予測期間中の南米のポンプ式水力貯蔵市場の成長を妨げると予想されます。

- とはいえ、技術的進歩の増加は、予測期間中、南米のポンプ式水力貯留市場に有利な成長機会を生み出す可能性が高いです。

- アルゼンチンは、人口が多く、電力需要が増加し、停電の回数が多いため、予測期間中にポンプ式水力貯留の必要性が高まると予想され、市場を独占すると見られています。

南米の揚水蓄電市場動向

クローズドループが市場を独占する見込み

- クローズドループポンプ水力貯蔵システムは、南米市場で顕著な成長を遂げると予測されます。主な促進要因の一つは、南米が豊富な水資源を誇ることから、水力発電を中心とした再生可能エネルギー源を重視する傾向が強まっていることです。閉回路設計を特徴とするクローズド・ループ・システムは、エネルギーを利用・貯蔵する効率的な手段を提供し、持続可能なエネルギー慣行に対する南米大陸のコミットメントによく合致しています。

- 国際再生可能エネルギー機関(International Renewable Energy Agency)によると、水力発電の導入はここ数年、この地域で大幅に増加しています。2016年から2023年にかけて、容量増の成長率は約10%を記録しており、水力発電の採用が増加していることを示しています。

- さらに、クローズドループポンプ水力貯水池固有の柔軟性は、再生可能エネルギー発電に伴う間欠性を管理するための信頼できるソリューションとして位置づけられています。南米諸国が風力や太陽光といった多様な再生可能エネルギー源をエネルギー・ポートフォリオに統合し続ける中、適切なエネルギー貯蔵の必要性が最も重要になっています。クローズド・ループ・システムは、需要の少ない時間帯に余剰エネルギーを貯蔵し、需要のピーク時にそれを放出する能力により、送電網の安定性と信頼性に大きく貢献します。

- 規制状況もまた、南米におけるクローズドループポンプ水力発電の成長を促進する上で重要な役割を果たしています。この地域の各国政府は、エネルギー安全保障と持続可能性の目標達成におけるエネルギー貯蔵ソリューションの重要性を認識しつつあります。クローズドループポンプ水力貯蔵プロジェクトの促進を目的とした支援政策とインセンティブは、投資に資する環境を作り出し、市場の拡大を促進しています。

- 例えば、2023年5月、Engie Brasil Energia社は、424MWのJaguara水力発電所の近代化をアンドリッツに発注しました。リファイナのグランデ川に位置するこの水力発電所は、1971年から稼働しています。このプロジェクトは、資産寿命の延長と性能向上を目的としています。近代化プロジェクトは2028年末までに完了する予定です。

- さらに、閉ループ式ポンプ水力貯蔵システムの拡張性は、地域の進化するエネルギー要件に合致しています。これらのシステムはモジュール式であるため、柔軟に容量を追加することができ、利害関係者はエネルギー需要の変化に対応することができます。この拡張性の要素は、南米の多様なエネルギー需要と国境を越えたエネルギー取引の可能性という文脈において、特に重要です。

- 従って、上記の点から、予測期間中はクローズドループ・セグメントが市場を独占すると予想されます。

アルゼンチンが市場を独占する見込み

- 水力発電を含む再生可能エネルギー源への注目の高まりは、ポンプ式水力貯留の特性とシームレスに整合しています。アルゼンチンは、エネルギーミックスの多様化を図り、従来の化石燃料への依存度を下げようとしており、ポンプ式水力発電の汎用性と信頼性は、持続可能で回復力のあるエネルギーインフラを確保する上で極めて重要な要素となっています。

- アルゼンチンの豊富な水力発電の潜在力は、ポンプ式水力貯蔵庫の成長見通しをさらに強固なものにしています。広大な水資源を自由に利用できるアルゼンチンは、ポンプ式水力貯蔵プロジェクトの開発にとって理想的な環境を有しています。これらのプロジェクトは、既存の水力発電インフラを活用し、エネルギー貯蔵に貢献するだけでなく、国の水力発電資源の全体的な効率と生産性を高めることができます。

- さらに、アルゼンチンはポンプ式水力発電の設置容量でトップの国です。国際再生可能エネルギー機関(International Renewable Energy Agency)によると、2023年現在、アルゼンチンのポンプ式水力貯留容量は約974MWで、設置容量約750MWのポンプ式水力貯留プロジェクトが2件、さらに224MWのポンプ式水力貯留プロジェクトが1件あります。

- アルゼンチンにおけるポンプ式水力発電の軌跡を形成する上で、進化する規制状況と再生可能エネルギー構想に対する政府の支援が重要な役割を果たしています。持続可能なエネルギーの普及に向けた政府の取り組みは、エネルギー貯蔵ソリューションの促進を目的としたインセンティブや政策と相まって、ポンプ式水力発電プロジェクトの成長を促す環境を作り出しています。このような支援は、国内での投資を誘致し、そのようなプロジェクトの実施を推進する上で重要な役割を果たしています。

- 例えば、2023年9月、アルゼンチンのコルドバ州は、750MW揚水蓄電所の改修を目的とした1億米ドルの契約の入札プロセスを開始しました。その目的は、現在指定容量の約半分で稼働しているリオ・グランデ施設を活性化させ、潜在的な生産能力を完全に回復させることです。コルドバの公営エネルギー会社であるEpecが入札プロセスの指揮を執り、発電所の運営を監督しています。提案されている改修工事は、リオ・グランデ発電所の寿命を最低でも40年延ばすことを目的に、5年間を予定しています。

- さらに、送電網の安定性と信頼性に対するニーズが高まっていることも、アルゼンチンにおける揚水蓄電の採用に説得力を与えています。アルゼンチンがエネルギー需要のシフトを経験し、断続的な再生可能エネルギー源をより多く取り入れるようになるにつれ、送電網の安定化力として機能する揚水蓄電の価値はますます高まっています。低需要時に余剰エネルギーを貯蔵し、ピーク時にそれを放出するこの技術の能力は、柔軟で弾力的なエネルギーシステムに対する国の要求に合致しています。

- 従って、上記の点から、同国は予測期間中に大きな成長を遂げることが予想されます。

南米の揚水蓄電産業概要

南米の揚水蓄電市場は半分断されています。同市場の主要企業(順不同)には、Voith GmbH &Co KGaA、ContourGlobal PLC、Andritz AG、Vale S.A.、Siemens AGなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 揚水蓄電の設置容量と2029年までの予測

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 再生可能エネルギー統合への注目の高まり

- 大きな水力発電の可能性

- 抑制要因

- 他のエネルギー貯蔵技術との競合

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 投資分析

第5章 市場セグメンテーション

- タイプ別

- オープンループ

- クローズドループ

- 地域別

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Voith GmbH & Co KGaA

- Norte Energia SA

- ContourGlobal PLC

- Centrais Eletricas Brasileiras SA

- Andritz AG

- Vale SA

- Siemens AG

- Mitsubishi Heavy Industries Ltd

- General Electric Company

- Iberdrola SA

- Market Ranking/Share(%)Analysis

- List of Other Prominent Companies

第7章 市場機会と今後の動向

- 技術の進歩

目次

Product Code: 50002222

The South America Pumped Hydro Storage Market size is estimated at 1.05 gigawatt in 2025, and is expected to reach 1.37 gigawatt by 2030, at a CAGR of 5.4% during the forecast period (2025-2030).

Key Highlights

- Over the long term, increasing government targets to integrate renewable energy coupled with significant hydropower potential is likely to drive the pump hydro storage market's growth during the forecast period.

- On the other hand, penetration of other energy storage techniques is expected to hamper the growth of the South American pump hydro storage market during the forecast period.

- Nevertheless, an increase in technological advancements is likely to create lucrative growth opportunities for the South American pump hydro storage market during the forecast period.

- Argentina is expected to dominate the market due to its large population, increasing electricity demand, and a higher number of power outages, which are expected to propel the need for pump hydro storage during the forecast period.

South America Pumped Hydro Storage Market Trends

Closed-loop is Expected to Dominate the Market

- The closed-loop pump hydro storage system is anticipated to experience notable growth in the South American market, driven by several strategic factors that underscore the region's evolving energy landscape. One of the key drivers is the increasing emphasis on renewable energy sources, mainly hydropower, as South America boasts abundant water resources. Closed-loop systems, characterized by their closed-circuit design, offer an efficient means of harnessing and storing energy, aligning well with the continent's commitment to sustainable energy practices.

- According to the International Renewable Energy Agency, hydropower installation has increased significantly in the region in the past few years. Between 2016 and 2023, the growth rate in capacity addition was recorded at around 10%, signifying the increasing adoption of hydropower, which in turn can drive the demand for pump storage.

- Furthermore, the inherent flexibility of closed-loop pump hydro storage positions it as a reliable solution for managing the intermittency associated with renewable energy generation. As South American countries continue to integrate diverse renewable sources like wind and solar into their energy portfolios, the need for adequate energy storage becomes paramount. Closed-loop systems contribute significantly to grid stability and reliability due to their ability to store excess energy during periods of low demand and release it during peak demand.

- The regulatory landscape also plays a crucial role in driving the growth of closed-loop pump hydro storage in South America. Governments across the region are increasingly recognizing the importance of energy storage solutions in achieving energy security and sustainability goals. Supportive policies and incentives aimed at promoting closed-loop pump hydro storage projects create a conducive environment for investments, driving the market's expansion.

- For instance, in May 2023, Engie Brasil Energia has awarded Andritz to modernize the 424 MW Jaguara hydropower plant. Located on the Grande River in Rifaina, the hydropower plant has been in operation since 1971. The project aims at the extension of asset lifetime and its performance improvement. The modernization project is expected to be completed by the end of 2028.

- Additionally, the scalability of closed-loop pump hydro storage systems aligns with the region's evolving energy requirements. The modular nature of these systems allows for flexible capacity additions, enabling stakeholders to adapt to changing energy demand dynamics. This scalability factor is particularly significant in the context of South America's diverse energy needs and the potential for cross-border energy trading.

- Therefore, as per the points mentioned above, the closed-loop segment is expected to dominate the market during the forecast period.

Argentina is Expected to Dominate the Market

- The increasing focus on renewable energy sources, including hydropower, aligns seamlessly with the attributes of pump hydro storage. As Argentina strives to diversify its energy mix and reduce dependency on traditional fossil fuels, the versatility and reliability of pump hydro storage emerge as pivotal components in ensuring a sustainable and resilient energy infrastructure.

- The abundant hydropower potential in Argentina further solidifies the growth prospects for pump hydro storage. With a vast array of water resources at its disposal, the country possesses an ideal environment for the development of pump hydro storage projects. These projects can leverage existing hydroelectric infrastructure, contributing not only to energy storage but also enhancing the overall efficiency and productivity of the nation's hydropower resources.

- Moreover, Argentina is the leading country in the installed capacity pump hydro storage. According to the International Renewable Energy Agency, as of 2023, the country had about 974 MW of pump hydro storage capacity, with two pump hydro storage projects of an installed capacity of about 750 MW and another capacity of 224 MW.

- The evolving regulatory landscape and government support for renewable energy initiatives play a crucial role in shaping the trajectory of pump hydro storage in Argentina. The government's commitment to fostering sustainable energy practices, coupled with incentives and policies aimed at promoting energy storage solutions, creates a conducive environment for the growth of pump hydro storage projects. This support is instrumental in attracting investments and driving the implementation of such projects within the country.

- For instance, in September 2023, the province of Cordoba in Argentina initiated a tender process for a USD 100 million contract aimed at refurbishing a 750 MW pumped storage hydropower plant. The goal is to revitalize the Rio Grande facility, currently operating at approximately half of its designated capacity, and restore its full production potential. Epec, the publicly owned energy company of Cordoba, is spearheading the tender process and overseeing the operation of the plant. The proposed refurbishment works are anticipated to span five years, with the objective of extending the lifespan of the Rio Grande plant by a minimum of 40 years.

- Moreover, the growing need for grid stability and reliability provides a compelling case for the adoption of pump hydro storage in Argentina. As the country experiences shifts in energy demand and incorporates a more significant share of intermittent renewable sources, the ability of pump hydro storage to act as a stabilizing force on the grid becomes increasingly valuable. The technology's capacity to store excess energy during periods of low demand and release it during peak demand aligns with the nation's requirements for a flexible and resilient energy system.

- Therefore, as per the points mentioned above, the country is expected to witness significant growth during the forecast period.

South America Pumped Hydro Storage Industry Overview

The South American pump hydro storage market is semi-fragmented. Some of the major players in the market (in no particular order) include Voith GmbH & Co KGaA, ContourGlobal PLC, Andritz AG, Vale S.A., and Siemens AG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Pumped Hydro Storage Installed Capacity and Forecast, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Emphasis on Renewable Energy Integration

- 4.5.1.2 Significant Hydropower Potential

- 4.5.2 Restraints

- 4.5.2.1 Competition From Other Energy Storage Technologies

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Open-loop

- 5.1.2 Closed-loop

- 5.2 By Geography

- 5.2.1 Brazil

- 5.2.2 Argentina

- 5.2.3 Colombia

- 5.2.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Voith GmbH & Co KGaA

- 6.3.2 Norte Energia SA

- 6.3.3 ContourGlobal PLC

- 6.3.4 Centrais Eletricas Brasileiras SA

- 6.3.5 Andritz AG

- 6.3.6 Vale SA

- 6.3.7 Siemens AG

- 6.3.8 Mitsubishi Heavy Industries Ltd

- 6.3.9 General Electric Company

- 6.3.10 Iberdrola SA

- 6.4 Market Ranking/Share (%) Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancement

南米の揚水蓄電:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日