アジア太平洋の揚水発電:市場シェア分析、産業動向、成長予測(2025年~2030年)

Asia-Pacific Pumped Hydro Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644920

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

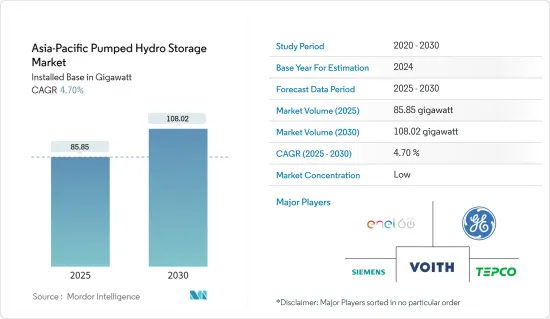

アジア太平洋の揚水発電市場は、2025年の85.85ギガワットから2030年には108.02ギガワットに拡大し、予測期間(2025~2030年)のCAGRは4.7%になると予測されます。

主要ハイライト

- 中期的には、再生可能エネルギー導入の増加や政府の支援施策などの要因により、アジア太平洋の揚水発電市場は成長すると予測されます。

- その一方で、他のエネルギー貯蔵技術との競合が同地域の揚水発電市場の成長を脅かすと予想されます。

- 揚水発電技術の技術的進歩の高まりは、予測期間中に市場に大きな機会をもたらすと期待されています。

- 中国は、揚水発電容量を増加させるための政府の取り組みにより、今後数年間で最大の市場シェアを獲得すると予測されます。それにもかかわらず、揚水発電技術における技術進歩の成長は、予測期間中に市場に大きな機会を創出すると期待されます。

- 中国は、揚水発電容量を増加させるための政府の取り組みにより、今後数年間で最大の市場シェアを獲得すると予測されています。

アジア太平洋の揚水発電市場動向

クローズドループセグメントが大きな成長を遂げる見込み

- クローズドループシステムでは、揚水発電所は、一方または両方のリザーバーが人工的に建設され、どちらにも自然水の流入がないように作られます。閉ループ揚水発電は、高い柔軟性、信頼性、高出力を記載しています。クローズドループ揚水発電システムは、既存の河川システムに接続されないため、オープンループ揚水発電システムに比べて環境への影響が少ないです。さらに、送電網のサポートが必要な場所に設置することもできます。

- 国際再生可能エネルギー機関(International Renewable Energy Agency)によると、アジアにおける純粋な揚水発電の設備容量は、2022年には80,988MWとなり、世界の全地域の中で最高となりました。同地域における閉ループ揚水発電所に対する需要の高まりにより、容量は過去5年間で一貫して増加しています。

- 例えば、2023年5月、Rewa Ultra Mega Solar Ltd(RUMSL)は、マディヤ・プラデーシュ州の合計13.8GWの揚水発電(PHS)プロジェクトの場所を割り当てるための提案依頼書(RFP)プロセスを開始しました。この提案には、開発事業者が600MWから2GWのPHS容量を設置できる合計12の場所が含まれています。

- オーストラリアの調査チームは、閉ループ揚水発電所は、揚水発電所の立地に適した場所を見つけるという問題を克服し、水資源への環境影響がないなどの利点があるため、近い将来、開ループPSH発電所を凌駕する可能性があると結論づけた。

- さらに、クローズドループ揚水発電は、高い柔軟性、信頼性、出力を記載しています。また、既存の河川システムや水流に干渉しないため、運転免許や許可を確実に取得できることも選ばれる大きな要因です。

- このような要因が、予測期間中の閉ループ揚水発電市場の勢いを目に見える形にする道を開いています。

中国が市場を独占する見込み

- 中国は、2022年時点で約3,677万kWの再生可能水力発電容量を持ち、世界の水力発電市場をリードしています。水力発電は総発電量の約16%を占めています。同国はまた、特に新しい施策やプロジェクト目標を掲げて、揚水発電の開発に熱心に取り組んでいます。

- 2022年、同国の純粋な揚水発電設備容量は約4,579万kWで、アジア諸国の中で最も高いです。政府と民間団体の努力により、この技術は中国でさらに開花することになります。

- 例えば、2022年6月、Power Construction Corporation of Chinaは、2025年までに200基の揚水発電所を設置し、新たに2700万kWの揚水発電容量を追加するための作業を開始したと発表しました。これにより、中国の設備容量は約10%、世界のエネルギー貯蔵容量は約170%増加する見込みです。

- さらに2022年1月、中国は河北省で世界最大の揚水発電所を稼働させました。この360万kWの揚水発電施設は、1基30万kWの12基の可逆式ポンプ発電セットで構成され、蓄電による発電能力は66億kWhです。

- 2023年11月、State Grid Corporation of Chinaは中国北西部の新疆ウイグル自治区に福康揚水発電所を完成させました。このプロジェクトは、総発電容量120万kWの30万kWタービン3基を備えています。この種の発電所は中国北西部では初めてです。

- このような開発は、近い将来、同国の揚水発電市場を牽引すると予測されています。

アジア太平洋の揚水発電産業概要

アジア太平洋の揚水発電市場はセグメント化されています。主要企業(順不同)には、Enel SpA、General Electric Company、Siemens AG、Voith GmBH & Co.KGAa、東京電力などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2028年までの設置容量と予測(単位:GW)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 再生可能エネルギーの統合

- 政府の支援施策と施策

- 抑制要因

- その他のエネルギー貯蔵技術との競合

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- オープンループ

- クローズドループ

- 2028年までの市場規模・需要予測(地域別)

- 中国

- 韓国

- インド

- 日本

- その他のアジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Enel SpA

- General Electric Company

- Siemens AG

- Voith GmBH & Co. KGaA

- Tokyo Electric & Power Company

- Stantec

- Black & Veatch Holding Company

- Andritz AG

第7章 市場機会と今後の動向

- 技術的進歩の増加

目次

Product Code: 93141

The Asia-Pacific Pumped Hydro Storage Market size in terms of installed base is expected to grow from 85.85 gigawatt in 2025 to 108.02 gigawatt by 2030, at a CAGR of 4.7% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as increasing adoption of renewable energy coupled with supportive government policies are projected to thrive in the Asia-Pacific pumped hydro storage market.

- On the other hand, the competition from other energy storage technologies is expected to threaten the growth of the pumped hydro storage market in the region.

- Nevertheless, the growing technological advancements in pumped hydro storage technology are expected to create significant opportunities for the market during the forecasted period.

- China is predicted to capture the largest market share in the coming years due to government initiatives to increase the pumped hydro storage capacity.Nevertheless, the growing technological advancements in pumped hydro storage technology are expected to create significant opportunities for the market during the forecasted period.

- China is predicted to capture the largest market share in the coming years due to government initiatives to increase the pumped hydro storage capacity.

Asia-Pacific Pumped Hydro Storage Market Trends

Closed-loop Segment is Expected to Witness Significant Growth

- In closed-loop systems, pumped hydro storage plants are created so that one or both the reservoirs are artificially built, and no natural water inflow is involved with either of them. Closed-loop pumped hydro storage offers high flexibility, reliability, and high-power output. Since the closed-loop pumped-hydro systems are not connected to existing river systems, their impact on the environment is less compared to open-loop pumped hydro storage systems. Moreover, they can be positioned where support for the grid is required.

- According to the International Renewable Energy Agency, the capacity of installed pure pumped hydro storage in Asia was recorded at 80,988 MW in 2022, the highest among all the regions across the world. The capacity grew consistently in the last five years due to the growing demand for closed-loop pumped hydro storage plants in the region.

- For instance, in May 2023, Rewa Ultra Mega Solar Ltd (RUMSL) initiated a Request for Proposal (RFP) process to allocate locations for a combined 13.8 GW of pumped hydro storage (PHS) projects in Madhya Pradesh. The offering includes a total of 12 sites where developers can establish PHS capacities ranging from 600 MW to 2 GW.

- A research team from Australia has concluded through a research study that the closed-loop pumped hydro storage plants may overshadow the open-loop PSH plants in the near future due to the benefits they provide, like overcoming the problem of finding suitable sites for pumped hydro storage plant location, and no environmental effects on water resources.

- Furthermore, closed-loop pumped hydro storage offers high flexibility, reliability, and power output. The other major factor for their preference is the certainty of gaining an operating license or permit since they do not interfere with the existing river systems or any water streams.

- Such factors pave the way for an explicitly visible momentum for the closed-loop pumped hydro storage market during the forecast period.

China is Expected to Dominate the Market

- China led the global hydropower market with around 36.77 GW of renewable hydropower capacity as of 2022. Hydro sources constitute about 16% of the total electricity generation mix. The country is also strenuously working on a lucid pumped hydro storage development, particularly with new policies and project goals.

- In 2022, the country's pure pumped hydro storage installed capacity was around 45.79 GW, the highest among all the Asian countries. The technology is set to bloom even more in China due to the efforts made by the government and private entities.

- For example, in June 2022, the Power Construction Corporation of China announced that it had started working on the new 270 GW of pumped hydro storage capacity to be added to the country's electricity mix, with the installation of 200 pumped hydro storage plants by 2025. It is expected to raise China's installed capacity by around 10% and the world's energy storage capacity by about 170%.

- Furthermore, in January 2022, the country commissioned the world's largest pumped hydro storage plant in China's Hebei province. The 3.6 GW pumped hydro storage facility consists of 12 reversible pumps generating sets with 300 MW each and possesses a power generation capacity from storage of 6.6 billion kWh.

- In November 2023, the State Grid Corporation of China inaugurated the Fukang pumped-storage power station in northwest China's Xinjiang region. The project features three 300 MW turbines with a total capacity of 1.2 GW. The facility is the first of its kind in northwestern China.

- Such developments are projected to drive the pumped hydro storage market in the country in the near future.

Asia-Pacific Pumped Hydro Storage Industry Overview

The Asia-Pacific pumped hydro storage market is fragmented. Some of the key players (in no particular order) include Enel SpA, General Electric Company, Siemens AG, Voith GmBH & Co. KGAa, and Tokyo Electric & Power Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Installed Capacity and Forecast in GW, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Renewable Energy Integration

- 4.5.1.2 Supportive Government Policies and Regulations

- 4.5.2 Restraints

- 4.5.2.1 Competition with Other Energy Storage Technologies

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Open Loop

- 5.1.2 Closed Loop

- 5.2 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.2.1 China

- 5.2.2 South Korea

- 5.2.3 India

- 5.2.4 Japan

- 5.2.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Enel SpA

- 6.3.2 General Electric Company

- 6.3.3 Siemens AG

- 6.3.4 Voith GmBH & Co. KGaA

- 6.3.5 Tokyo Electric & Power Company

- 6.3.6 Stantec

- 6.3.7 Black & Veatch Holding Company

- 6.3.8 Andritz AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Technological Advancements

アジア太平洋の揚水発電:市場シェア分析、産業動向、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日