|

市場調査レポート

商品コード

1629763

欧州の冷凍食品包装:市場シェア分析、産業動向、成長予測(2025~2030年)Europe Frozen Food Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の冷凍食品包装:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

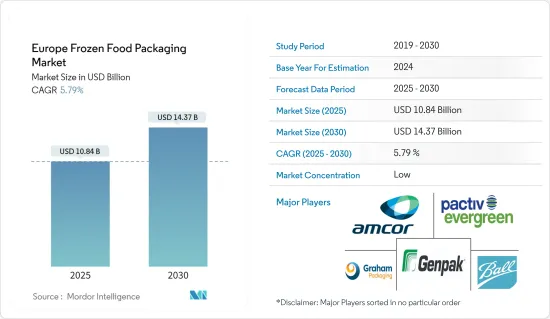

欧州の冷凍食品包装市場規模は2025年に108億4,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.79%で、2030年には143億7,000万米ドルに達すると予測されています。

都市化の急速な進展とペースの速いライフスタイルにより、消費者の嗜好は、従来の家庭料理よりも調理に時間がかからない冷凍食品にシフトしています。

主なハイライト

- 食品の品質に対する消費者の期待の高まりが冷凍食品包装の需要を促進しています。また、製品の品質に対する消費者の評価も市場成長を促進する要因です。さらに、経済やライフスタイルの変化に伴い、欧州では冷凍食品包装の需要が増加しています。同市場は予測期間中、高成長が見込まれています。

- 新しい包装技術も最近開発され、冷凍食品の包装をより実用的で安全なものにしています。こうした技術には、インテリジェント・パッケージング、アクティブ・パッケージング、エンジニアリング・サイエンスなどがあります。環境汚染を減らし、政府の規制を遵守するため、企業はリサイクル、再生、再利用が可能な生分解性包装材料を採用することで、環境に優しい包装に注力しています。

- さらに、利便性は冷凍食品消費の世界の増加を促す主な要因のひとつです。その結果、大手企業は消費者の地域的嗜好に応えるため、新しいタイプや原材料を導入しています。コンビニエンス製品に対する消費者の嗜好の高まりは、ゼロから調理するのに比べて調理が簡単で時間が節約できるため、冷凍製品の需要増加を後押ししています。

- さらに、労働人口の多忙なライフスタイルの増加により冷凍スナック食品市場は急速に拡大しており、これが冷凍スナック市場を押し上げ、冷凍食品パッケージ市場の需要を促進しています。

- しかし、欧州市場は、欧州委員会などの機関による食品包装の種類や接触材料に関する厳しい規制のため、今後も高い規制が続くと予想されます。冷凍食品包装には、汚染、水分の侵入、温度変動を防止してサプライチェーン全体で食品の品質と安全性を維持するための堅牢なソリューションが必要です。

欧州の冷凍食品包装市場の動向

プラスチックが大きな市場シェアを占める

- 欧州では、利便性、保存性、費用対効果に後押しされ、冷凍食品セクターにおけるプラスチック包装の需要の急増が顕著です。プラスチック包装は、消費者がすぐに食べられる食事や冷凍スナックに引き寄せられる中で際立っています。その密閉性は、冷凍食品に不可欠な製品の保存期間を大幅に延長します。湿気、冷凍焼け、酸化を防ぐことは、味、食感、栄養価を保つ上で最も重要です。欧州では、フレキシブルなプラスチックフィルム、袋、パウチが人気を博しており、軽量で使い勝手が良く、食品の品質保持を実現しています。

- 消費者のライフスタイルの変化が、欧州の冷凍食品市場の成長をさらに後押ししています。現代生活の喧騒に伴い、多くの欧州人は利便性と保存期間の延長を求めて冷凍食品に引き寄せられつつあります。1回分ずつのプラスチック包装の台頭は、ポーションコントロールに対応し、食品廃棄を最小限に抑え、欧州の消費者の環境意識の高まりと一致しています。さらに、欧州ではeコマースやオンライン食料品ショッピングのシーンが急増しており、輸送中の冷凍製品の完全性を保証する、堅牢で耐久性のあるパッケージへの需要が高まっています。

- しかし、プラスチックの利点がより顕著になるにつれて、環境への懸念がますます欧州の需要状況を形作っています。これを受けて、多くの欧州諸国がプラスチック廃棄物を抑制し、持続可能な包装を支持するための規制を展開しています。EUの持続可能性に関する誓約は、単なるコミットメントではなく、パッケージング領域におけるイノベーションに拍車をかける触媒となっています。その結果、リサイクル可能なプラスチック、生分解性プラスチック、さらには植物由来のプラスチックといった進歩が生まれました。消費者の環境意識が高まる中、メーカーは代替素材を模索しています。その目的は?冷凍食品包装においてプラスチックが提供する本質的な機能性と品質を維持しつつ、規制上の義務や消費者の要望を満たすことです。

- 欧州のミレニアル世代は、冷凍食品包装の需要を牽引し、一人前や持ち帰り用のオプションを好みます。ミレニアル世代は利便性、ポーションコントロール、クイックミールを重視するため、プラスチック包装が不可欠となっています。シングルサーブ容器やフレキシブルパウチは、食品の鮮度と安全性を保ちながらこうしたニーズを満たし、冷凍食品包装のプラスチック需要を煽っています。

- ドイツ冷凍食品協会(German Frozen Food Institute)によると、ドイツの冷凍食品消費量は増加しており、小売売上高は2020年の101億7,000万米ドルから2023年には125億9,000万米ドルに増加します。この動向は、冷凍食品が多忙な消費者の主食となっている欧州全体のシフトを反映しています。売上の増加はプラスチック包装の需要を直接後押しし、プラスチック包装は品質の保持と賞味期限の延長に不可欠です。

- 冷凍食品の需要が拡大するにつれて、メーカーは多層フィルム、トレイ、パウチなどのプラスチック・ソリューションを、その汎用性と費用対効果の高さから頼りにしています。リサイクル可能で持続可能なパッケージングにおけるイノベーションも、環境責任を重視する欧州の動きに対応するために生まれてきています。

袋包装タイプが市場成長を牽引

- 気密性シーリングの需要が高まっている背景には、アロマを含む製品の品質を長期間保持する高いバリア性を備えた袋のニーズがあります。さらに、ジッパー付き袋は、再密封や再閉が可能な包装への需要によって、調査対象市場ではますます一般的になってきています。スペースを取らない包装形態のため、企業は袋を選択し、調査対象市場における同セグメントの成長を後押ししています。さらに、プラスチック袋が提供する柔軟性、耐引裂性、透明性、防湿性などの特性は、市場の成長をさらに加速させると予想されます。

- さらに、同業他社は再生プラスチックを50%使用した新しい高級スナック菓子の包装の発売にも力を入れています。例えば、2024年3月、INEOSは、ペプシコが英国とアイルランドでSunbitesスナック・ブランドに導入した、リサイクル・プラスチックを50%使用した新しい高級スナック包装の発売で極めて重要な役割を果たしました。先進のリサイクルプロセスで製造されたこのパッケージは、食品接触パッケージに関するEUの厳しい規制基準を満たしています。

- このマイルストーンを達成するために、フレキシブル食品包装のサプライチェーン全体で様々なパートナーが協力しました。GreenDot社は、消費者向けのプラスチック包装廃棄物を提供し、Plastic Energy社の技術によってTACOILに変換されました。INEOSはこの熱分解油を利用して再生プロピレンとバージン品質の再生ポリプロピレン樹脂を製造しました。IRPLASTはこの樹脂を使用して50%リサイクル原料を使用した包装用フィルムを製造し、AmcorはPepsiCoのためにこれらのフィルムを印刷しました。このパートナーシップは、2030年までにパッケージから化石由来のプラスチックを排除するというペプシコのコミットメントに沿ったものです。

- さらに、オンライン食料品ショッピングの増加により、輸送中に冷凍製品の鮮度を維持する袋などのパッケージング・ソリューションに対する需要が高まっています。便利な食事作りを好む消費者の嗜好は、惣菜、野菜、果物、デザートを含む冷凍食品の需要増加を牽引しています。

- 袋の形式は冷凍スナックの正確な分量管理を可能にし、消費管理を容易にし、食品廃棄を最小限にします。カナダ農業食糧省によると、2023年の英国のスナック菓子小売売上高は143億7,290万米ドルで第1位、次いでフランス、イタリア、その他欧州各国の順となっています。

欧州の冷凍食品包装業界の概要

利便性と多用途性から冷凍食品を好む消費者の増加がこの地域の市場成長を促進しています。革新的な包装形態と包装材料も消費者の経験を向上させ、廃棄物を最小限に抑えるのに役立っています。

欧州の冷凍食品包装市場は断片化されており、Genpack LLC、Graham Packaging Company、Ball Corporation、Pactiv LLC、Amcor Groupなど複数の大手企業で構成されています。同地域の企業は、冷凍食品用の持続可能な包装材料の発売にも注力しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 世界の冷凍食品包装市場の概要

第5章 市場力学

- 市場促進要因

- 消費者によるコンビニエンス包装への需要の高まり

- 欧州における可処分所得の増加と消費者行動の変化

- 市場抑制要因

- 政府の規制と介入による市場の制限

第6章 市場セグメンテーション

- 材料タイプ別

- ガラス

- 紙

- 金属

- プラスチック

- その他

- 製品タイプ別

- 袋

- 箱

- タブとカップ

- トレー

- パウチ

- その他の製品タイプ

- 食品タイプ別

- レディメイドミール

- 野菜・果物

- 肉類

- 海産物

- 焼き菓子

- その他食品

- 国別

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

第7章 競合情勢

- 企業プロファイル

- Pactiv LLC

- Amcor Group

- Genpak LLC

- Graham Packaging Company, Inc.

- Ball Corporation Inc

- Crown Holdings

- Tetra Pak International

- Placon Corporation

- Toyo Seikan Group Holdings, Ltd.

- WestRock Company

- Sealed Air Corporation

- Berry Global Inc.

第8章 投資分析

第9章 市場の将来

The Europe Frozen Food Packaging Market size is estimated at USD 10.84 billion in 2025, and is expected to reach USD 14.37 billion by 2030, at a CAGR of 5.79% during the forecast period (2025-2030).

The rapid growth of urbanization and fast-paced lifestyles have shifted consumers' preferences toward frozen food products, which require less time for cooking than traditional home-cooked meals.

Key Highlights

- The rise in consumer expectations related to food quality has propelled the demand for frozen food packaging. Also, consumer appreciation of the product quality is another factor driving the market growth. Additionally, with changes in the economy and lifestyles, there is an increased demand for frozen food packaging in Europe. The market is expected to grow lucratively during the forecast period.

- New packaging technologies have also developed recently, making packaging for frozen food products more practical and secure. These technologies include intelligent packaging, active packaging, and engineering science. To reduce environmental pollution and comply with government regulations, companies focus on eco-friendly packaging by employing biodegradable packaging materials that can be recycled, regenerated, and reused.

- Furthermore, convenience is one of the primary factors driving the global increase in frozen food consumption. As a result, leading players are introducing new types and ingredients to cater to consumers' regional tastes. The growing consumer preference for convenience products fuels the increasing demand for frozen products due to their ease of preparation and time savings compared to cooking from scratch.

- Moreover, the frozen snacks food market is expanding rapidly due to the increasing volume of the hectic lifestyle of the working population, which is boosting the frozen snacks market and propelling the demand for the frozen food packaging market.

- However, the European market is anticipated to remain highly regulated, owing to stringent regulations regarding food packaging types and contact materials by agencies such as the European Commission. Frozen food packaging requires robust solutions to maintain food quality and safety across the supply chain by preventing contamination, moisture intrusion, and temperature fluctuations.

Europe Frozen Food Packaging Market Trends

Plastic to Hold Significant Market Share

- In Europe, a surge in demand for plastic packaging in the frozen food sector is evident, spurred by convenience, preservation, and cost-effectiveness. Plastic packaging stands out as consumers gravitate towards ready-to-eat meals and frozen snacks. Its airtight seal capability significantly extends product shelf life, a vital feature in frozen food. Safeguarding against moisture, freezer burn, and oxidation is paramount to preserving taste, texture, and nutritional value. In Europe, flexible plastic films, bags, and pouches have gained traction, offering food quality preservation while being lightweight and user-friendly.

- Changing consumer lifestyles have further propelled the growth of Europe's frozen food market. With the hustle and bustle of modern life, many Europeans are gravitating towards frozen foods for convenience and extended shelf life. The rise of single-serve plastic packaging caters to portion control and minimizes food waste, aligning with the heightened environmental awareness among European consumers. Moreover, the burgeoning e-commerce and online grocery shopping scene in Europe amplifies the demand for robust, durable packaging, ensuring the integrity of frozen products during transit.

- Yet, as the advantages of plastic become more pronounced, environmental concerns increasingly shape Europe's demand landscape. In response, numerous European nations are rolling out regulations to curb plastic waste and champion sustainable packaging. The EU's sustainability pledge is not just a commitment but a catalyst, spurring innovations in the packaging domain. This has birthed advancements like recyclable, biodegradable, and even plant-based plastics. With a growing environmental consciousness among consumers, manufacturers are searching for alternative materials. Their goal? To align with regulatory mandates and consumer desires, all while preserving the essential functionality and quality plastic offers in frozen food packaging.

- Europe's Millennials drive demand for frozen food packaging, favoring single-serving and on-the-go options. They value convenience, portion control, and quick meals, making plastic packaging essential. Single-serve containers and flexible pouches meet these needs while keeping food fresh and secure, fueling demand for plastic in frozen food packaging.

- According to the German Frozen Food Institute, Germany's frozen food consumption is rising, with retail revenue growing from USD 10.17 billion in 2020 to USD 12.59 billion in 2023. This trend reflects a broader European shift, where frozen foods are staples for busy consumers. Increased sales directly boost demand for plastic packaging, which is crucial for preserving quality and extending shelf life.

- As frozen food demand grows, manufacturers rely on plastic solutions like multi-layer films, trays, and pouches for their versatility and cost-effectiveness. Innovations in recyclable and sustainable packaging are also emerging to address Europe's focus on environmental responsibility.

Bags Packaging Type to Drive the Market Growth

- The rising demand for airtight sealing is driven by the need for bags with high barrier properties, which retain product quality, including aroma, for a prolonged period. Furthermore, zippered bags are becoming more and more common in the market under study, driven by the demand for packaging that can be resealed and reclosed. Due to space-saving packaging formats, businesses choose bags, boosting the segment's growth in the market under study. Moreover, properties such as flexibility, tear-resistance, transparency, and moisture protection offered by plastic bags are expected to accelerate the market's growth further.

- Additionally, in line with the same players are focusing on launching new, premium-quality snack packaging containing 50% recycled plastic. For instance, in March 2024, INEOS played a pivotal role in launching new, premium quality snack packaging containing 50% recycled plastic, which PepsiCo introduced for their Sunbites snack brand in the UK and Ireland. This packaging, made through advanced recycling processes, meets strict EU regulatory standards for food contact packaging.

- Various partners collaborated across the flexible food packaging supply chain to achieve this milestone. GreenDot provided post-consumer plastic packaging waste, which was converted into TACOIL by Plastic Energy's technology. INEOS utilized this pyrolysis oil to produce recycled propylene and virgin-quality recycled polypropylene resin. IRPLAST used this resin to create packaging films with 50% recycled materials, while Amcor printed these films for PepsiCo. This partnership aligns with PepsiCo's commitment to eliminating fossil-based plastic in its packaging by 2030.

- Moreover, the growth in online grocery shopping has increased demand for packaging solutions such as bags that maintain frozen product freshness during transportation. Consumer preference for convenient meal preparation has driven increased demand for frozen foods, including ready meals, vegetables, fruits, and desserts.

- The bag format enables precise portion control for frozen snacks, facilitating consumption management and minimizing food waste. According to Agriculture and Agri-Food Canada, the retail sales of snacks in the United Kingdom in 2023 took first position with USD 14,372.9 million sales, followed by France, Italy, and many other countries across Europe.

Europe Frozen Food Packaging Industry Overview

Rising consumer preference for frozen foods due to their convenience and versatility is driving the market growth in the region. Innovative packaging formats and materials are also helping to improve consumer experience and minimize waste.

The European frozen Food packaging market is fragmented and consists of several major players, such as Genpack LLC, Graham Packaging Company, Ball Corporation, Pactiv LLC, and Amcor Group. Players in the region are also focusing on launching sustainable packaging materials for frozen food.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Overview of the Global Frozen Food Packaging Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Convenience Packaging by Consumers

- 5.1.2 Increase in Disposable Income and Changing Consumer Behavior in Europe

- 5.2 Market Restraint

- 5.2.1 Government Regulations and Interventions limit the Market

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Glass

- 6.1.2 Paper

- 6.1.3 Metal

- 6.1.4 Plastic

- 6.1.5 Others Material Type

- 6.2 By Product Type

- 6.2.1 Bags

- 6.2.2 Boxes

- 6.2.3 Tubs and Cups

- 6.2.4 Trays

- 6.2.5 Pouches

- 6.2.6 Other Product Types

- 6.3 By Type of Food

- 6.3.1 Readymade Meals

- 6.3.2 Fruits and Vegetables

- 6.3.3 Meat

- 6.3.4 Sea Food

- 6.3.5 Baked Goods

- 6.3.6 Others Food Types

- 6.4 By Country

- 6.4.1 United Kingdom

- 6.4.2 Germany

- 6.4.3 France

- 6.4.4 Spain

- 6.4.5 Italy

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Pactiv LLC

- 7.1.2 Amcor Group

- 7.1.3 Genpak LLC

- 7.1.4 Graham Packaging Company, Inc.

- 7.1.5 Ball Corporation Inc

- 7.1.6 Crown Holdings

- 7.1.7 Tetra Pak International

- 7.1.8 Placon Corporation

- 7.1.9 Toyo Seikan Group Holdings, Ltd.

- 7.1.10 WestRock Company

- 7.1.11 Sealed Air Corporation

- 7.1.12 Berry Global Inc.