冷凍食品包装:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Frozen Food Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1624595

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

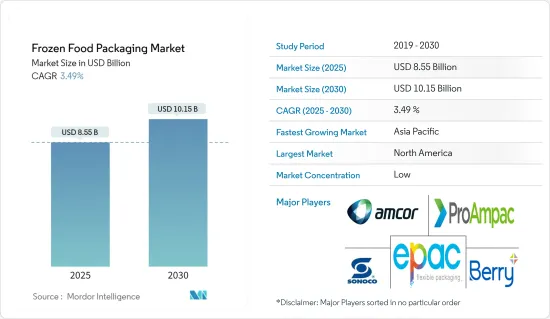

冷凍食品包装市場規模は2025年に85億5,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは3.49%で、2030年には101億5,000万米ドルに達すると予測されます。

冷凍食品包装は軽量で割れにくく、リシーラブルな機能を提供し、化石燃料の使用量を減らし、環境に優しい環境を作るために温室効果ガスの排出と水の使用量を削減することができます。

主なハイライト

- 市場の消費者は小売店、スーパーマーケット、ハイパーマーケットを好みます。組織化された小売店は、世界的に大きな存在感を示しており、市場のかなりの部分を占めています。組織化された小売チェーンの増加は、冷凍食品業界における食品包装ソリューションのニーズに直結しています。

- 肉、鶏肉、魚介類のような冷凍食品包装は、他の食品用途の中で最も速い成長を示しました。世界中の多くの大手食品包装会社は、非常に創造的で装飾的なパッケージを発売しています。

- 例えば、2023年8月、繊維ベースの製品メーカーであるAhlstrom社は、持続可能なパッケージング・プロバイダーであるThe Paper People社と提携し、冷凍食品用の持続可能なパッケージング・ソリューションを発表しました。両社が共同開発したこの完全な繊維ベースのパッケージは、主に冷凍食品パッケージ用の従来の化石資源由来のプラスチックやフィルムの代用として設計されています。このリサイクル可能な包装は、縦型フォームフィルシール、スタンドアップパウチ、SOSスタイルシステムなど、既存の包装設備で利用することができます。

- また、サビックは2023年5月、エスティコ・パッケージング・ソリューションズ社およびノルウェーのブランド・オーナーであるコールドウォーター・プローンズ社と共同で、冷凍エビ用の持続可能な新包装パウチを設計・製造しました。このパウチは、サビックPP(ポリプロピレン)クリスタルのサーキュラー認証ランダム・ポリマー・グレードを使用し、エスティコ・パッケージング・ソリューションズが提供する多層フィルムから作られており、海洋由来プラスチック含有率は約60%です。

- しかし、政府の包装に関する法規制が市場の成長を制限する可能性があります。米国では食品医薬品局(FDA)が食品に添加される物質の安全性を規制しています。全体として、冷凍食品包装には以下のような本質的特性が求められる:低温および高温に対する耐性、特定の機械的強度、食品に含まれる酸、油、その他の分解性化学物質に対する耐性、特定の衛生レベルと類似性。

冷凍食品包装市場の動向

肉と海産食品が市場の主要シェアを占める

- 冷凍食肉市場は、主に食の嗜好の変化により、今後数年間で大幅な成長が見込まれます。COVID-19の発生後、冷凍食肉と包装された調理済み食品の需要が急増しました。時間の経過とともに食肉産業は多様化し、現在では多数の加工企業が冷凍食肉製品や調理済み食品を提供しています。特筆すべきは、この分野が世界のほぼすべての地域で拡大していることです。

- 消費者は、より高い品質に対してプレミアムを支払うことを望むようになっています。消費者は一貫して、保存料を最小限に抑えた、あるいは全く使わない冷凍食肉製品の製造を優先するブランドを好みます。その結果、健康的な食事に対する消費者の嗜好の高まりが、「オーガニック」や防腐剤不使用として販売される冷凍肉・魚製品の需要を押し上げることになります。生鮮肉に比べて保存期間が長いなどの利点に惹かれて、多くの個人が安心して冷凍肉製品を購入するようになった。

- ニュージーランド統計局によると、ニュージーランドの2023年の冷凍鶏肉生産量は6万8,000トン強で、前年の約6万3,000トンから増加しました。この増加傾向は今後も続くと予想され、冷凍食品包装の需要をさらに押し上げると思われます。

- ノルウェーのリスク管理・保証会社であるデット・ノルスケ・ベリタス(DNV)の「水産物予測」によると、世界の一人当たり水産物需要は2050年まで着実に増加するといいます。市場の拡大に伴い、水産物の品質維持が最重要課題となっています。このため、微生物の繁殖を抑え、冷凍焼けを防ぎ、急速冷凍を容易にし、ドリップロスを最小限に抑えることで保存期間を延ばす包装ソリューションが必要となります。その結果、パッケージ化された水産物製品の消費の増加は、冷凍水産物包装の需要を押し上げています。

- 市場の主要企業は、一貫して新しい冷凍水産物製品を発表しており、それによってパッケージングベンダーの機会を拡大しています。例えば、2024年5月、Scott &Jon's社は冷凍エビ料理ラインを拡大し、新たに電子レンジで調理可能なサーモン丼を追加しました。これらの最新製品は、Scott &Jon'sが2023年に健康志向のエビ丼ラインをデビューさせたことに続くものです。

アジア太平洋地域が最速の成長を遂げる

- アジア太平洋地域では、人口の増加が食品需要の拡大を牽引しています。都市化と食中毒、浪費、腐敗に対する意識の高まりが、より高品質の製品に対する需要を促進しています。中国はアジア太平洋冷凍食品包装市場で大きなシェアを占めています。同国の膨大な人口と都市化が、冷凍食品に対する食欲の高まりに拍車をかけています。今日の消費者は利便性と品質の両方を優先しています。

- インドの冷凍食品分野は急速に拡大しています。各ブランドの冷凍食品は、時折パーティーで提供される軽食から、あらゆる年齢層が楽しむ常食アイテムへの移行に成功しています。調理済み食品(RTE)や簡便食品に対する需要の急増は、特に労働人口の増加の中で顕著です。この動向は、多忙な生活を送り、家族のために手早く栄養価の高い食事を求める現代の夫婦間でさらに顕著になっています。

- 地域全体で健康とフィットネスの動向が勢いを増す中、冷凍食品部門も取り残されてはいないです。包装はこの業界で極めて重要な役割を果たしています。食品メーカーは、製造から消費に至るまで製品が安全で汚染されていないことを保証することを最優先しており、この課題には堅牢な冷凍食品パッケージング・ソリューションが効果的に対処しています。

- 高品質で調理しやすいという人気の動向から、冷凍食品包装は日本の消費者に好まれています。さらに、日本の多国籍食品・バイオテクノロジー企業である味の素は、日本の家庭用冷凍食品の消費額が前年の486億円(3億3,000万米ドル)から2023年には603億円(4億1,000万米ドル)に増加すると報告しています。この急増は、この地域の冷凍食品包装オプション市場を押し上げる構えです。

- さらに、中国、日本、インド、その他のアジア諸国の冷凍食品包装市場の規模は、冷凍食肉や調理済み食肉製品の需要の増加により拡大しています。中国国家統計局によると、この業界ではここ数年で冷凍食品包装が30%近く増加したといいます。

冷凍食品包装業界の概要

The frozen food packaging market is fragmented and consists of several major players, such as Sonoco Products Company.ProAmpac LLC、Cascades Inc.などです。市場シェアの面では、現在市場を独占している大手企業は少数です。しかし、独創的で装飾的な包装パターンを持つ中堅・中小企業は、新規契約の獲得や新市場の開発によって市場での存在感を高めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 新興国における冷凍食品需要の拡大

- 組織化された小売店の増加

- 市場抑制要因

- 政府の規制と介入

第6章 市場セグメンテーション

- 食品タイプ別

- 果物・野菜

- 肉・海産物

- 冷凍デザートとアイスクリーム

- 焼き菓子

- 包装タイプ別

- 袋

- 箱

- チューブ・カップ

- トレー

- ラッパー

- パウチ

- その他の包装

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア

- 中国

- 日本

- インド

- 韓国

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- ProAmpac LLC

- Sonoco Products Company

- Amcor PLC

- Berry Plastics Group Inc.

- ePac Holdings, LLC

- Cascades Inc.

- Duropack Limited

- Smurfit Westrock plc

- Mondi Group

- American Packaging Corporation

- ThinkInk Packaging

第8章 投資分析

第9章 市場機会と今後の動向

目次

The Frozen Food Packaging Market size is estimated at USD 8.55 billion in 2025, and is expected to reach USD 10.15 billion by 2030, at a CAGR of 3.49% during the forecast period (2025-2030).

Frozen food packaging delivers lightweight, unbreakable, and resealable features, lowers fossil fuel usage, and can reduce greenhouse gas emissions and water usage to create an eco-friendly environment.

Key Highlights

- The market's consumers prefer retail stores, supermarkets, and hypermarkets. Organized retail stores are a substantial part of the market with a significant global presence. The increase in the organized retail chain is translating directly into the need for food packaging solutions in the frozen food industry.

- Packaging for frozen foods like meat, poultry, and seafood witnessed the fastest growth among other food applications. Many large food packaging companies across the globe are launching hugely creative and decorative packaging.

- For instance, in August 2023, fiber-based products manufacturer Ahlstrom teamed up with sustainable packaging provider The Paper People to launch a sustainable packaging solution for frozen food. Co-developed by the two companies, this fully fiber-based packaging is mainly designed to substitute traditional fossil-based plastic and films for frozen food packaging. The recyclable packaging can be utilized on existing packaging equipment, including vertical form-fill-seal, stand-up pouches, and SOS-style systems.

- Also, in May 2023, Sabic joined forces with Estiko Packaging Solutions and brand owner Coldwater Prawns of Norway to design and execute a sustainable new packaging pouch for frozen prawns. The pouch is made from a multilayer film offered by Estiko Packaging Solutions utilizing a circular-certified random polymer grade of Sabic PP (polypropylene) Qrystal with an ocean-bound plastic content of around 60%.

- However, the government packaging laws and regulations could limit the market growth. In the United States, the Food and Drug Administration (FDA) regulates the safety of substances added to food. Overall, frozen food packaging should have the following essential characteristics: Resistance to low and high temperatures, a particular mechanical strength, resistance to acid, oil, and other degrading chemicals in the food product, and a specific level of hygiene and similar.

Frozen Food Packaging Market Trends

Meat and Sea Food to Account for a Major Share in the Market

- The frozen meat market is poised for substantial growth in the coming years, primarily driven by shifting food preferences. Following the COVID-19 outbreak, demand surged for frozen meats and packaged, ready-to-eat foods. Over time, the meat industry has diversified, with numerous processing firms now offering frozen meat products and ready-to-eat items. Notably, this sector is witnessing expansion in nearly every region worldwide.

- Consumers are increasingly willing to pay a premium for higher quality. They consistently prefer brands that prioritize producing frozen meat items with minimal or no preservatives. As a result, the growing consumer preference for healthy eating is set to boost the demand for frozen meat and fish products marketed as "organic" and preservative-free.Many individuals now purchase frozen meat products with confidence, drawn by advantages like extended shelf life compared to fresh meat.

- Statistics New Zealand reported that New Zealand produced just over 68 thousand metric tons of frozen chicken meat in 2023, up from approximately 63 thousand metric tons the year before. This upward trend is anticipated to continue, further driving the demand for frozen food packaging.

- According to the "Seafood Forecast" by Det Norske Veritas (DNV), a Norwegian risk management and assurance firm, global per capita seafood demand is set to rise steadily until 2050. As markets expand, maintaining seafood quality becomes paramount. This necessitates packaging solutions that extend shelf life by curbing microbial growth, preventing freezer burn, facilitating rapid freezing, and minimizing drip loss. Consequently, the rising consumption of packaged seafood products is driving up the demand for frozen seafood packaging.

- Major players in the market are consistently launching new frozen seafood products, thereby expanding opportunities for packaging vendors. For example, in May 2024, Scott & Jon's expanded its frozen shrimp entree line to include new microwavable salmon bowls. These latest offerings come on the heels of Scott & Jon's 2023 debut of its health-focused shrimp bowl line.

Asia-Pacific to Witness the Fastest Growth

- In the Asia-Pacific region, a growing population is driving an increasing demand for food products. Urbanization and heightened awareness of foodborne illnesses, wastage, and spoilage are fueling demand for higher-quality offerings. China holds a significant share of the Asia-Pacific frozen food packaging market. The country's vast population and urbanization have spurred a rising appetite for frozen food items. Today's consumers prioritize both convenience and quality.

- India's frozen food segment is witnessing rapid expansion. Brands have successfully transitioned their offerings from being occasional party snacks to regular meal items enjoyed by all age groups. The surge in demand for ready-to-eat (RTE) and convenience foods is particularly pronounced among the growing working population. This trend is even more evident among modern couples, both of whom lead busy lives and seek quick, nutritious meals for their families.

- As the health and fitness trend gains momentum across the region, the frozen foods sector is not left behind. Packaging plays a pivotal role in this industry. Food manufacturers prioritize ensuring their products remain safe and contamination-free from production to consumption, a challenge effectively addressed by robust frozen food packaging solutions.

- Due to its high quality and popular easy-to-cook trends, frozen food packaging is preferred by Japanese consumers. Moreover, Ajinomoto, a Japanese multinational food and biotechnology corporation, reported that the consumption of home-use frozen meals in Japan rose to JPY 60.3 billion (USD 0.41 billion) in 2023, up from JPY 48.6 billion (USD 0.33 billion) the previous year. This surge is poised to boost the market for frozen food packaging options in the region.

- Additionally, the size of China, Japan, India and other Asian countries frozen food packaging market is expanding due to the rise in demand for frozen meat and ready-to-eat meal products. The National Bureau of Statistics of China states that the industry saw an increase in frozen food packaging of almost 30% in the last few years.

Frozen Food Packaging Industry Overview

The frozen food packaging market is fragmented and consists of several major players, such as Sonoco Products Company. ProAmpac LLC, Cascades Inc., and more. In terms of market share, few of the major players currently dominate the market. However, with creative and decorative packaging patterns, mid-size to smaller companies are increasing their market presence by securing new contracts and tapping new markets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Frozen Food Demand in Emerging Countries

- 5.1.2 Rising Number of Organized Retail Stores

- 5.2 Market Restraint

- 5.2.1 Government Regulations and Interventions

6 MARKET SEGMENTATION

- 6.1 By Type of Food

- 6.1.1 Fruits and Vegetables

- 6.1.2 Meat and Sea Food

- 6.1.3 Frozen Desserts and Ice Creams

- 6.1.4 Baked Foods

- 6.2 By Type of Packaging

- 6.2.1 Bags

- 6.2.2 Boxes

- 6.2.3 Tubs and Cups

- 6.2.4 Trays

- 6.2.5 Wrappers

- 6.2.6 Pouches

- 6.2.7 Other Types of Packaging

- 6.3 Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Spain

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ProAmpac LLC

- 7.1.2 Sonoco Products Company

- 7.1.3 Amcor PLC

- 7.1.4 Berry Plastics Group Inc.

- 7.1.5 ePac Holdings, LLC

- 7.1.6 Cascades Inc.

- 7.1.7 Duropack Limited

- 7.1.8 Smurfit Westrock plc

- 7.1.9 Mondi Group

- 7.1.10 American Packaging Corporation

- 7.1.11 ThinkInk Packaging

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日