モノカートンの世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)

Mono Cartons - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1549825

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

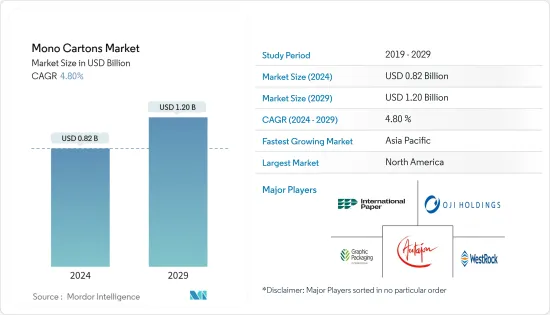

世界のモノカートンの市場規模は、2024年に8億2,000万米ドルと推定され、2029年には12億米ドルに達し、予測期間中(2024年~2029年)にCAGR4.80%で成長すると予測されています。

モノカートンは軽量で、審美的に魅力的な包装・ソリューションです。モノカートンは保護を提供する折り畳み式カートンの一種であり、様々なエンドユーザー用途の要件に基づいてカートンをカスタマイズすることができます。

主なハイライト

- モノカートンは製品をコンパクトに包装するために使用され、高度にカスタマイズ可能で、様々なエンドユーザー業界の多くの用途を容易にします。持続可能な包装に対する需要の増加が市場の成長を促進しています。コーティングおよび非コーティングのモノカートンは、複数のデザイン、形状、サイズで生産されており、魅力的なデザインへの需要が増加し、カートンの成長機会を生み出しています。

- モノカートンは保管や使用に便利です。これらのカートンは、その軽量構造によって包装の重量を減らすのに役立ち、包装された製品のセキュリティを確保するために適度な強度を提供します。また、折り畳み可能で、十分な保管と出荷のしやすさを提供します。生産、流通、消費において費用対効果が高いため、需要が高くなっています。

- 動きの速い消費財(FMCG)業界は、歯磨き粉、石鹸、ビスケット、フェイスクリームなどの小型製品の継続的な保管と出荷のため、モノカートンの消費に不可欠です。また、FMCG業界では、製品仕様がラベル付けされた印刷カートンを主要な包装材として使用しています。小売店の増加と発展途上国における個人の可処分所得の増加により、FMCG産業の成長は予測期間中にモノカートンの需要を促進すると予想されます。

- eコマース用モノカートンはeコマース用包装の代替品として注目されています。モノカートンは、より多くの個人がオンラインで購入し、製品が安全かつ良い状態で到着することを望んでいるため、重要な選択肢となっています。さらに、企業はモノカートンの大きな表面積をブランディングとマーケティングに利用することができ、露出を増やし、より強力なブランドアイデンティティを作ることができます。

- 市場は、プラスチックなどの代替包装材による課題を目の当たりにしています。持続可能な包装の人気が高まっているにもかかわらず、プラスチック包装は依然として市場の主要な成長要因のひとつです。多くの顧客はいまだにプラスチック包装の快適さとコストを支持しており、これがモノカートンの普及を困難にしています。消費者や企業にプラスチック包装をやめるよう説得するには、モノカートンを利用する環境上の利点に関する効果的な教育・啓蒙活動が必要です。

モノカートンの市場動向

飲食品業界は大きな成長が見込まれる

- 飲食品包装は食品業界にとって重要な部分であり、食品や飲料の安全性を確保するために不可欠です。食品を汚染や損傷から守り、賞味期限を延ばし、輸送や保管を容易にします。

- 食品包装に使用されるモノカートンは、1層の板紙から作られています。モノカートンはリサイクル可能で、耐久性があり、多目的に使用でき、生鮮食品、冷凍食品、スナック菓子、焼き菓子など様々な食品を包装することができます。モノカートン包装は、食品を新鮮に保ち、保護し、視覚的にアピールすることを保証します。

- カートンボードの需要は世界的に伸びています。Suzano Papel e Celuloseによると、カートンボードの消費量は2022年には5,400万トンで、2024年には5,600万トンに達すると予想されています。世界のカートン消費量の増加は、予測期間中の市場成長を促進すると予想されます。また、Frozen & Refrigerated BuyerとCirncaによると、2023年の米国における冷凍食品売上高はピザが15億6,404万米ドルでトップ、次いでアイスクリームが14億6,349万米ドルでした。

- カートン包装は製品から湿気を遠ざけ、長時間の出荷に耐えるため、主に二次包装や三次包装の手段として、消費者により良い結果を提供するために様々なブランドで採用されるようになってきています。パン、ケーキ、生鮮品などの加工食品は、このような包装材を使用する必要があり、需要を牽引しています。

- 様々な国で、加工食品、生鮮食品、食肉分野の消費増加が起きています。食品消費の伸びは、健康とウェルネスの動向と消費者の倫理的関心の高まりによって引き続き促進されています。さらに、予測期間中、人口増加が生鮮食品の需要を支える主要な原動力になると予想されます。有機的に生産された食品を求める動向は、近代的な食料品小売店におけるプレミアム価格帯の持続可能な生鮮食品の存在感を高めると予想されます。

アジア太平洋が最も速い成長を遂げる見込み

- アジア太平洋は、モノカートンを含む世界最大の紙器包装市場の一つであり、その大きな潜在的進化により需要が拡大する可能性が高いです。アジアの一部の新興国における需要は堅調であると予想されます。アジア太平洋は、中国、インドなどにおける惣菜需要の高まりにより、世界の紙器包装市場を独占しています。

- 消費者が環境に優しく持続可能な慣行への変化に注目する中、モノカートンの需要は、飲食品、ヘルスケア、パーソナルケア、小売など、いくつかの地域の産業で伸びています。持続可能な包装の選択に対する消費者の意識、原材料の入手可能性、紙の軽量でリサイクル可能な特性、森林減少のすべてが、この地域の紙器包装の需要に寄与しています。

- 2023年6月にPackmanチームが実施した調査では、インドのモノカートン企業グループの財務分析が示され、上位5社の売上高は20億インドルピーを超え、下位5社の売上高は4億5,000万インドルピーから9億インドルピーでした。多くの企業が食品、アルコール、医薬品を含む様々なFMCGセグメントにモノカートンを供給していました。

- 経済産業省(日本)と財団法人古紙再生促進センター(PRPC)によると、2023年の日本の紙生産量は約1,160万トン、板紙生産量は約1,040万トンでした。紙・板紙の生産量は約2,200万トンに増加しました。

- 2023年5月、Omya International AGは紙・板紙産業への投資を発表しました。中国とインドネシアの板紙工場に、粉砕炭酸カルシウムと沈殿炭酸カルシウムのオンサイトプラント7基を建設しました。中国の新プラントには、広西チワン族自治区、広東省、山東省に3つの粉砕炭酸カルシウム(GCC)プラント、山東省に2つの沈殿炭酸カルシウム(PCC)プラント、福建省にさらに1つのPCCプラントが含まれます。製紙に使用されるこれらの原料は、印刷適性、光沢、平滑性などの紙の特性を向上させます。この地域の製紙会社によるこのような拡張は、予測期間中の市場成長を促進すると予想されます。

モノカートン産業の概要

モノカートン市場は細分化されており、以下のような様々な企業が存在します。 Graphic Packaging International LLC, Oji Holdings Corporation, Westrock Company, and International Paper. The companies operating are focused on innovating new solutions through investments, collaborations, mergers and acquisitions, etc., to expand their business in the region.

- 2024年2月:王子ホールディングスと日本テトラパック株式会社は、アセプティック包装専用の日本初のリサイクルシステムを開発するために提携しました。このリサイクルシステムは、小売店や自治体の回収、包装メーカーからの古紙など、さまざまな供給源からアセプティックパック包装を回収します。

- 2023年9月:Graphic Packaging Internationalは2億6,250万米ドルでベルを買収しました。ベルはサウスダコタ州に2ヶ所、オハイオ州に1ヶ所の計3ヶ所のコンバーティング施設を運営しています。Graphicは以前、Bellの買収により2億米ドルの売上と1,000万米ドルの利益が追加されると見積もっていました。ベルはこれらの施設で年間9万5,000トンの板紙を消費し、紙器や関連製品に転換しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 持続可能な包装ソリューションへの需要

- 市場成長を牽引するeコマース

- 市場抑制要因

- 代替包装ソリューションとの競合

第6章 市場セグメンテーション

- コーティング別

- コート有り

- コート無し

- エンドユーザー産業別

- 飲食品

- 医薬品

- パーソナルケア

- エレクトロニクス

- その他エンドユーザー産業

- 地域別

- 北米

- 欧州

- アジア

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Graphic Packaging International LLC

- Oji Holdings Corporation

- Westrock Company

- International Paper Company

- Stora Enso

- Georgia-Pacific LLC

- Autajon Group

- Parksons Packaging Ltd

- Packman Packaging Private Limited

- Packtek

第8章 投資分析

第9章 市場機会と今後の動向

目次

The Mono Cartons Market size is estimated at USD 0.82 billion in 2024, and is expected to reach USD 1.20 billion by 2029, growing at a CAGR of 4.80% during the forecast period (2024-2029).

Mono cartons are lightweight, esthetically appealing packaging solutions. Mono cartons are a type of folding carton that provides protection, and the cartons can be customized based on the requirements of various end-user applications.

Key Highlights

- Mono cartons are used for compact packaging of products, are highly customizable, and facilitate many applications across various end-user industries. An increase in demand for sustainable packaging is driving the market growth. Coated and uncoated mono cartons are produced in multiple designs, shapes, and sizes, increasing the demand for appealing designs and creating growth opportunities for the cartons.

- Mono cartons facilitate convenience for their storage and usage. These cartons help reduce the weight of the package due to their lightweight structure and offer a reasonable amount of strength to ensure the security of the packaged products. It also comes foldable, providing ample storage and shipment easement. It is cost-effective in production, distribution, and consumption, thus, is in high demand.

- The fast-moving consumable goods (FMCG) industry is critical to the consumption of mono cartons due to the continuous storage and shipment of small-sized products such as toothpaste, soap, biscuits, and face cream. The FMCG industry also uses printed cartons labeled with product specifications as the primary packaging material. Due to the increasing number of retail stores, coupled with rising individual disposable income in developing countries, the growing FMCG industry is anticipated to fuel the demand for mono cartons over the forecast period.

- E-commerce mono cartons have emerged as a favored alternative for e-commerce packaging. Mono cartons are a significant choice as more individuals buy online and want their products to arrive securely and in shape. Furthermore, companies can use the large surface area of mono cartons for branding and marketing, increasing exposure and creating a stronger brand identity.

- The market witnesses challenges due to alternate packaging materials such as plastic. Despite the rising popularity of sustainable packaging, plastic packaging remains one of the market's leading growth drivers. Many customers still favor the comfort and cost of plastic packaging, which makes the widespread adoption of mono cartons difficult. Persuading consumers and businesses to abandon plastic packaging necessitates effective educational and awareness initiatives on the environmental benefits of utilizing mono cartons.

Mono Cartons Market Trends

The Food and Beverage Industry is Expected To Witness Significant Growth

- Food and beverage packaging is a critical part of the industry and essential in ensuring the food or beverage is safe. It protects food from contamination and damage, helps extend its shelf life, and makes it easier to transport and store.

- Mono cartons used for food packaging are made from a single layer of cardboard. Mono cartons are recyclable, durable, and versatile and can package various food products, including fresh and frozen food products, snacks, and baked goods. Mono-carton packaging guarantees the food stays fresh, protected, and visually appealing.

- The demand for carton boards globally is witnessing growth. According to Suzano Papel e Celulose, cartonboard consumption was 54 million tons in 2022 and is expected to reach 56 million tons by 2024. The increase in the worldwide consumption of cartons is expected to drive the market growth over the forecast period. Also, according to Frozen & Refrigerated Buyer and Cirnca, the frozen food sales in the United States in 2023 were topped by pizza at USD 1,564.04 million, followed by ice cream at USD 1,463.49 million.

- As carton packaging keeps moisture away from products and resists long shipping times, it is increasingly being adopted by various brands to offer better results to their consumers, mainly as a means to secondary or tertiary packaging. Processed foods, such as bread, cakes, and perishable items, need such packaging materials to be used, thereby driving the demand.

- Various countries are witnessing a rise in the consumption of processed food, fresh produce, and meat sectors. Food consumption growth continues to be fueled by health and wellness trends and the increase in consumers' ethical concerns. Additionally, population growth is expected to be the key driver behind the demand for fresh food during the forecast period. A trend for organically produced foods is expected to increase the presence of sustainable fresh food at premium price points in modern grocery retailers.

The Asia-Pacific Region is Expected to Witness the Fastest Growth

- The Asia-Pacific region is one of the largest global folding carton packaging markets, including mono cartons, and demand is likely to grow due to its significant potential evolution. Demand in some emerging Asian countries is anticipated to be strong. The Asia-Pacific region dominates the global folding carton packaging market due to the rising demand for ready-to-eat meals in China, India, etc.

- As consumers focus on changes to eco-friendly and sustainable practices, mono-carton demand is growing across several regional industries, including food and beverage, healthcare, personal care, retail, etc. Consumer awareness of sustainable packaging choices, raw material availability, paper's lightweight and recyclable characteristics, and deforestation have all contributed to the region's demand for folding carton packaging.

- A survey conducted by the Packman team in June 2023 showed a financial analysis of a group of Indian mono-carton companies; the top five companies had turnovers exceeding INR 200 crore, while the bottom five had turnovers ranging from INR 45 crore to INR 90 crore. Many companies supplied mono cartons for various FMCG segments, including food, alcohol, and pharma products.

- According to METI (Japan) and the Paper Recycling Promotion Center (PRPC), in 2023, the paper production volume in Japan amounted to approximately 11.6 million metric tons, and the production volume for paperboard stood at around 10.4 million metric tons. The paper and paperboard production volume increased to around 22 million metric tons.

- In May 2023, Omya International AG announced investments in its paper and board industry. The company invested in seven onsite plants for ground and precipitated calcium carbonate at paperboard mill locations in China and Indonesia. The new plants in China include three ground calcium carbonate (GCC) plants in Guangxi, Guangdong, and Shandong, two precipitated calcium carbonate (PCC) plants in Shandong, and one more PCC plant in Fujian. These raw materials used for paper manufacturing will improve the paper's properties, such as printability, gloss, smoothness, etc. Such expansions by paper manufacturing companies in the region are expected to drive the market growth over the forecast period.

Mono Cartons Industry Overview

The market is fragmented with the presence of various players such as Graphic Packaging International LLC, Oji Holdings Corporation, Westrock Company, and International Paper. The companies operating are focused on innovating new solutions through investments, collaborations, mergers and acquisitions, etc., to expand their business in the region.

- February 2024: Oji Holdings and Nihon Tetra Pak K.K. partnered to pioneer Japan's first recycling system specifically for aseptic carton packages, a significant step toward gaining a circular economy for paper resources in the country. The recycling system collects aseptic carton packages from various sources, including retail and municipal collections and waste paper from packaging manufacturers.

- September 2023: Graphic Packaging International acquired Bell Inc. for USD 262.5 million. Bell operates three converting facilities: two in South Dakota and one in Ohio. Graphic previously estimated the Bell acquisition would add USD 200 million in sales and yield USD 10 million. Bell consumes an estimated 95,000 tons of paperboard annually at those facilities to convert into folding cartons and related products.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for Sustainable Packaging Solutions

- 5.1.2 E-commerce to Drive the Market Growth

- 5.2 Market Restraints

- 5.2.1 Competition from Alternative Packaging Solutions

6 MARKET SEGMENTATION

- 6.1 By Coating

- 6.1.1 Coated

- 6.1.2 Uncoated

- 6.2 By End-User Industry

- 6.2.1 Food & Beverage

- 6.2.2 Pharmaceuticals

- 6.2.3 Personal Care & Comsetics

- 6.2.4 Electronics

- 6.2.5 Other End-User Industries

- 6.3 By Region

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Graphic Packaging International LLC

- 7.1.2 Oji Holdings Corporation

- 7.1.3 Westrock Company

- 7.1.4 International Paper Company

- 7.1.5 Stora Enso

- 7.1.6 Georgia-Pacific LLC

- 7.1.7 Autajon Group

- 7.1.8 Parksons Packaging Ltd

- 7.1.9 Packman Packaging Private Limited

- 7.1.10 Packtek

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日