|

市場調査レポート

商品コード

1687467

段ボール包装:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Corrugated Board Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 段ボール包装:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

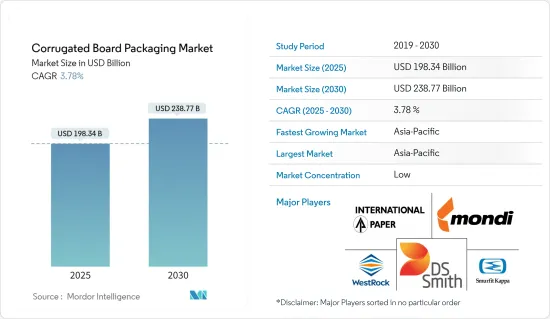

段ボール包装の市場規模は2025年に1,983億4,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは3.78%で、2030年には2,387億7,000万米ドルに達すると予測されています。

過酷な取り扱いに対する強固な保護機能を持つ段ボールは、選ばれるパッケージとして台頭してきました。その耐久性、多用途性、安定性により、段ボールは小売セクターの定番となっており、eコマースの世界の売上急増に伴い、その採用はますます強まっています。

主なハイライト

- 防湿性だけでなく、長時間の輸送にも耐える段ボール包装に注目する企業が増えています。この動向は、企業が二次包装や三次包装に段ボールを採用することで顕著になっています。需要の急増は、主にパンや肉製品のような加工食品や腐敗しやすい食品によってもたらされており、これらは使い捨ての包装を必要とします。さらに、人々のライフスタイルが忙しくなるにつれて、コンビニエンス・フードへの欲求が高まっています。

- パルプと紙から作られる段ボールは、プラスチック製のものよりもリサイクル性に優れています。フルーティング加工が施された段ボールは衝撃吸収材として機能し、外部からの衝撃から中身を守ります。段ボールは大きな圧力に耐えることができ、層状でさまざまな厚さのフルートが必要不可欠な緩衝材となります。eコマース部門は最近、段ボールの圧倒的な消費者として台頭してきました。アマゾンをはじめとする大手企業は、段ボールを一次包装に利用する一方、個々の商品にはプラスチックを使用しています。

- この市場にも課題と限界があります。段ボールにはプラスチックや木箱のような耐久性がないため、重量物や極端な圧力には適していないです。一般的に、長期的で再利用可能な投資というよりは、短期的な使用に適しています。

- 段ボールは汎用性があるため、箱などさまざまな形に成形することができます。持続可能性への関心が高まるにつれ、段ボールは徐々にフレキシブル・プラスチック袋に取って代わりつつあります。さらに、多様な印刷技術に対応しているため、企業にとっては魅力的なマーケティング・ツールであり、余分なマーケティング・コストをかけることなく、効果的にモバイル広告塔としての役割を果たします。

- 紙やリサイクル素材などの原材料の入手可能性や価格の変動は、生産や価格戦略に影響を与える可能性があります。紙パッケージング業界は、森林破壊に起因する課題、サプライチェーンの脆弱性、環境問題、規制上の課題、そして持続可能なイノベーションの緊急の推進に取り組んでいます。

段ボール包装市場の動向

加工食品セグメントが大きな市場シェアを占める見込み

- 段ボールは加工食品業界で人気のある包装の選択肢です。箱のサイズや形状には様々なものがあります。顧客はよく知られた容器で間食を楽しむことができます。段ボールで包装されたシリアル、クラッカー、その他のスナック菓子の消費は、数世代にわたっています。

- 段ボール包装は製品から湿気を遠ざけ、長時間の出荷に耐えることができるため、企業はこの包装をますます採用し、特に二次または三次包装において、より良い顧客成果を提供するようになっています。パン、肉製品、その他の生鮮品などの加工食品は、これらの包装材を一度だけ使用する必要があるため、需要が高まっています。

- 2023年9月にJamestown Containerが発表したところによると、段ボール食品包装は従来の素材に代わる環境に優しい素材と見なされるようになってきています。その汎用性は、生鮮食品、焼き菓子、冷凍・缶詰など様々な食品に及ぶ。段ボール包装の高いカスタマイズ性により、企業は独特で視覚的に魅力的なデザインを作ることができます。これには、ブランドロゴ、製品詳細、その他のブランディング要素を箱に直接印刷し、ブランド認知を高め、製品のプレゼンテーションを向上させることも含まれます。

- 段ボール包装は、多くの食品においてプラスチック包装に代わる有効な選択肢となりつつあります。高速インターネット・サービスへのアクセスが向上し、eリテールやeコマース・チャネルが台頭してきたため、顧客はさまざまな種類の加工食品をオンラインでより簡単に注文できるようになりました。加えて、手厚い節約と利便性が多くの消費者を引きつけており、予測期間を通じて同分野の成長に拍車をかけています。これには、チーズ、既製スープ、魚の缶詰などが含まれます。段ボール箱の包装は、リサイクル素材や堆肥化素材から、よりシンプルに作ることができます。

- ミレニアル世代をはじめとする消費者は、食品包装、生産、廃棄物が環境に与える影響についてより強く意識するようになっています。ストラ・エンソの調査によると、ミレニアル世代の59%が、バリューチェーン全体を通じて持続可能な包装であるべきだと考えています。持続可能な包装製品に対する需要は、加工食品包装の主要な促進要因であり、段ボール包装市場の成長にプラスの影響を与えています。

- ブラジルの紙パルプメーカーであるスザンヌ社と、欧州の重要なエンジニアリング、設計、アドバイザリーサービス会社であるAFRY社によると、紙と板紙の世界消費量は2022年には4億1,500万トンになると予想されています。消費量は今後10年間でさらに増加し、2032年には4億7,600万トンに達すると思われます。世界の紙・板紙生産の大半はパッケージングで消費されています。

アジア太平洋地域が大きなシェアを占める見込み

- アジア太平洋の段ボール包装市場は、都市化する人口と環境に優しい包装への意識の高まりによって成長します。主な業界動向としては、段ボール生産能力の増加や技術の進歩が挙げられます。しかし、厳しい規制や製品品質への懸念がこの成長を妨げる可能性があります。

- アジアの段ボール包装市場の成長加速は、持続可能な包装に対する需要の急増、eコマースセクターの活況、エレクトロニクスやパーソナルケア製品に対する需要の高まり、経済開拓に伴う一人当たり所得の上昇によって後押しされています。

- 一人当たり所得の上昇と人口動態の変化が中国の段ボール包装部門を形成し、新しい包装材料と包装プロセスを必要としています。アリババのようなeコマース大手が段ボール市場を牽引する態勢を整えています。国際貿易局は、中国が世界のeコマース市場を独占しており、取引総額の約50%を占めていると報告しています。オンライン小売取引は2024年までに3兆5,600億米ドルに達すると予測されており、このブームは持続可能なパッケージング・ソリューションへの需要を増幅させ、段ボールパッケージの売上を押し上げると思われます。

- インド、中国、日本などの国々では、飲食品、ITエレクトロニクス、家電製品など、段ボールに大きく依存している産業が消費アップグレードの動向を経験しています。このような主要エンドユーザー産業のシフトは、中・高級段ボール市場を押し上げると予想されます。

- さらに、段ボール包装市場の成長は、アジア太平洋諸国における原材料の入手可能性、使い捨てプラスチックを抑制する政府規制、およびこれらの国々における最終使用産業の増加によって拍車がかかっています。

段ボール包装業界の概要

段ボール包装市場は断片化されており、以下のような多数のプレーヤーが存在します。 Mondi Group, DS Smith PLC, WestRock Company, Smurfit Kappa Group, and more offering diverse solutions. These companies are innovating and rolling out eco-friendly packaging products to support sustainability. Additionally, they're unveiling tailored corrugated box designs catering to various end-user industries, seizing emerging opportunities. Furthermore, the market is seeing a flurry of partnerships and acquisitions as key players bolster their portfolios in the corrugated board packaging arena.

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- 環境に優しい素材の採用拡大と段ボールのデジタル印刷の進化

- eコマース分野からの旺盛な需要

- 市場抑制要因

- リターナブル包装と再利用可能包装の増加

第6章 市場セグメンテーション

- エンドユーザー産業別

- 加工食品

- 生鮮食品と青果物

- 飲料

- パーソナルケアとハウスホールドケア

- eコマース

- その他のエンドユーザー産業(電気・電子、ヘルスケア、工業、繊維、ガラス・セラミックス)

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ポーランド

- アジア

- 中国

- インド

- 日本

- 韓国

- インドネシア

- タイ

- オーストラリア・ニュージーランド

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- 北米

第7章 競合情勢

- 企業プロファイル

- International Paper Company

- Mondi Group

- DS Smith PLC

- WestRock Company

- Smurfit Kappa Group

- Stora Enso Oyj

- Sealed Air Corporation

- Asia Pulp & Paper(APP)Sinar Mas

- Napco National

- Georgia-Pacific LLC

- Nine Dragons Paper Holdings Limited

- Oji Holdings Corporation

第8章 投資分析

第9章 市場の将来展望

The Corrugated Board Packaging Market size is estimated at USD 198.34 billion in 2025, and is expected to reach USD 238.77 billion by 2030, at a CAGR of 3.78% during the forecast period (2025-2030).

With its robust protection against harsh handling, the corrugated board has emerged as the packaging of choice. Its durability, versatility, and stability make it a staple in the retail sector, and with the global surge in e-commerce sales, its adoption is only intensifying.

Key Highlights

- Businesses increasingly turn to corrugated board packaging, not only for its moisture protection but also for its resilience during extended transportation. This trend is significantly pronounced as companies adopt it for secondary and tertiary packaging. The surge in demand is primarily driven by processed and perishable foods, like bread and meat products, which necessitate single-use packaging. Additionally, as people's lifestyles grow busier, the appetite for convenience foods rises.

- Crafted from pulp and paper, corrugated boards boast a recyclability edge over their plastic counterparts. The fluting medium acts as a shock absorber, safeguarding contents from external impacts. These boards can endure significant pressure, and their layered and varied-thickness flutes provide essential cushioning. The e-commerce sector has recently emerged as a dominant consumer of corrugated boards. Major players, including Amazon, utilize these boards for primary packaging while reserving plastic for individual items.

- The market also has challenges and limitations. The corrugated board lacks the durability of plastic or wooden boxes, making them less suitable for heavy items or extreme pressures. Typically, it's favored for short-term use rather than as long-term, reusable investments.

- Their versatility allows corrugated boards to be molded into various shapes, including boxes. As sustainability concerns mount, they're gradually replacing flexible plastic bags. Furthermore, their compatibility with diverse printing techniques makes them an attractive marketing tool for companies, effectively serving as mobile billboards without incurring extra marketing costs.

- Variations in the availability and pricing of raw materials, such as paper and recycled content, can influence production and pricing strategies. The paper packaging industry grapples with challenges stemming from deforestation, encompassing supply chain vulnerabilities, environmental issues, regulatory challenges, and an urgent push for sustainable innovations.

Corrugated Board Packaging Market Trends

Processed Food Segment Expected to Occupy Significant Market Share

- The corrugated board is a popular packaging choice in the processed food industry. There are many different sizes and shapes of boxes. Customers are given a well-known container to enjoy their snacking in. The consumption of cereal, crackers, and other snack foods packaged in corrugated boards spans several generations.

- The corrugated board packaging keeps moisture away from products and can withstand long shipping times, companies are increasingly adopting this packaging to offer better customer outcomes, especially for secondary or tertiary packaging. Processed foods, such as bread, meat products, and other perishable items, need these packaging materials to be used just once, thus driving the demand.

- According to Jamestown Container in September 2023, corrugated food packaging is increasingly considered an eco-friendly alternative to conventional materials. Its versatility spans various food products, including fresh produce, baked goods, and frozen and canned items. The high customizability of corrugated packaging allows businesses to craft distinctive and visually appealing designs. This includes printing brand logos, product details, and other branding elements directly onto the boxes, enhancing brand recognition, and elevating product presentation.

- Corrugated board packaging is becoming a viable alternative to plastic packaging for many food products. Due to the rising accessibility of high-speed internet services and the rise of e-retail and e-commerce channels has been sparked, making it more straightforward for customers to order various kinds of processed food goods online. In addition, the generous savings and convenience it offers draw more consumers, adding to the segment's growth throughout the forecast period. These include cheese, ready-made soups, and canned fish, among others. Corrugated box packaging can be created more simply from recycled or composted materials.

- Consumers, such as millennials, are becoming more aware of the environmental impact of food packaging, production, and waste. According to a Stora Enso survey, 59% of millennials think packaging should be sustainable throughout the value chain. Demand for sustainable packaging products is a key driver in processed food packaging, positively impacting corrugated board packaging market growth.

- According to Suzanne, a Brazilian pulp and paper producer, and AFRY, a critical European engineering, design, and advisory services firm, the global consumption of paper and paperboard was expected to be 415 million tonnes in 2022. Consumption will rise further over the next decade, reaching 476 million tonnes by 2032. Packaging consumes the majority of worldwide paper and paperboard production.

Asia Pacific is Expected to Hold a Significant Share

- Asia Pacific's corrugated board packaging market is set to grow, driven by an urbanizing population and heightened awareness of eco-friendly packaging. Key industry trends include increased containerboard capacity and technological advancements. However, stringent regulations and product quality concerns could hinder this growth.

- Accelerated growth in Asia's corrugated board packaging market is fueled by a surge in demand for sustainable packaging, a booming e-commerce sector, heightened demand for electronics and personal care products, and rising per capita income amid economic development.

- Rising per capita income and shifting demographics shape China's corrugated board packaging sector, necessitating new packaging materials and processes. E-commerce giants like Alibaba are poised to drive the corrugated packaging market. The International Trade Administration reported that China dominates the global e-commerce landscape, accounting for about 50% of total transactions. With projections of online retail transactions hitting USD 3.56 trillion by 2024, this boom is set to amplify the demand for sustainable packaging solutions, bolstering sales of corrugated board packaging.

- In countries like India, China, and Japan, industries such as food and beverage, IT electronics, and home appliances, which heavily rely on corrugated boxes, are experiencing a trend of consumption upgrading. This shift in leading end-user industries is anticipated to boost the market for mid to high-end corrugated cartons.

- Additionally, the growth of the corrugated board packaging market is spurred by the availability of raw materials in Asia Pacific nations, government regulations curbing single-use plastics, and a rising number of end-use industries across these countries.

Corrugated Board Packaging Industry Overview

The corrugated board packaging market is fragmented, with numerous players such as Mondi Group, DS Smith PLC, WestRock Company, Smurfit Kappa Group, and more offering diverse solutions. These companies are innovating and rolling out eco-friendly packaging products to support sustainability. Additionally, they're unveiling tailored corrugated box designs catering to various end-user industries, seizing emerging opportunities. Furthermore, the market is seeing a flurry of partnerships and acquisitions as key players bolster their portfolios in the corrugated board packaging arena.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of Eco-friendly Materials and Evolution of Digital Print for Corrugated Boards

- 5.1.2 Strong Demand from the E-commerce Sector

- 5.2 Market Restraint

- 5.2.1 Increasing Usage of Returnable and Reusable Packaging

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 Processed Foods

- 6.1.2 Fresh Food and Produce

- 6.1.3 Beverages

- 6.1.4 Personal and Household Care

- 6.1.5 E-commerce

- 6.1.6 Other End-user Industries (Electrical & Electronics, Healthcare, Industrial, Textile, Glass & Ceramics)

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.2.4 Italy

- 6.2.2.5 Spain

- 6.2.2.6 Poland

- 6.2.3 Asia

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.3.4 South Korea

- 6.2.3.5 Indonesia

- 6.2.3.6 Thailand

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.5.1 Brazil

- 6.2.5.2 Argentina

- 6.2.5.3 Mexico

- 6.2.6 Middle East and Africa

- 6.2.6.1 Saudi Arabia

- 6.2.6.2 South Africa

- 6.2.6.3 United Arab Emirates

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 International Paper Company

- 7.1.2 Mondi Group

- 7.1.3 DS Smith PLC

- 7.1.4 WestRock Company

- 7.1.5 Smurfit Kappa Group

- 7.1.6 Stora Enso Oyj

- 7.1.7 Sealed Air Corporation

- 7.1.8 Asia Pulp & Paper (APP) Sinar Mas

- 7.1.9 Napco National

- 7.1.10 Georgia-Pacific LLC

- 7.1.11 Nine Dragons Paper Holdings Limited

- 7.1.12 Oji Holdings Corporation