|

市場調査レポート

商品コード

1549808

中東データセンター建設:市場シェア分析、産業動向、成長予測(2024年~2029年)Middle East Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東データセンター建設:市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

中東のデータセンター建設市場規模は2024年に42億米ドルと推定され、2030年には159億米ドルに達すると予測され、予測期間中(2024~2030年)のCAGRは24.85%で成長する見込みです。

今後数年間、中東地域はデータセンター市場への投資を拡大すると予想されます。同地域におけるデータセンターの拡大を促進している要因はいくつかあります。同地域の政府によるスマートシティの野望は、近代的コミュニティの構築方法の転換を促しています。デジタル技術に支えられた未来の都市は、大量のデータを生成すると予想されています。データの取得、保存、処理を最適化することが重要です。

主要ハイライト

- 同地域の今後のIT負荷容量は2030年までに3,530MWに達すると予想され、予測期間中のデータセンター・ラックの需要にプラスの影響を与えると予測されます。

- 2030年までに同地域の床面積は1,260万平方フィート増加すると予測されます。

- 同地域のラック設置総数は2029年までに38万個に達する見込みです。サウジアラビアが最大数のラックを設置する見込みです。

- 中東を結ぶ海底ケーブルシステムは29近くあり、その多くが建設中です。2025年にサービスを開始すると推定されている海底ケーブルのひとつが、インド・欧州・エクスプレス(IEX)で、サウジアラビアのNEOM、サウジアラビアのヤンブ、オマーンのサララを陸揚げ点とする全長9775キロメートルに及びます。

中東データセンター建設市場動向

ティア3が同地域の主要シェアを占める展望

- 中東のデータセンター市場のティア3セグメントは、ストリーミングサービス、オンラインゲーム、スマートホームオートメーションサービスなどのユーザーベースの増加により、予測期間中(2024~2030年)にCAGR 21.48%を記録すると予想されます。

- 中東には約90のティア3データセンター施設があります。これらの施設は主に、ドバイ、アブダビ、ジッダ、フルサン、リヤド、ヘルツリーヤ、ロシュ・ハアイン、テルアビブ、ブネイ・シオン、ドーハ、テヘラン、アンマン、アカバ、アル・アスカル、ハマラ、マスカット、バウシャールにあります。

- 2023年には、ティア3セグメントが市場の75%を占め、600MWを超えるIT負荷容量を誇っています。地域別では、アラブ首長国連邦が36%のシェアでトップ、次いでサウジアラビアが28.6%、イスラエルが25.4%で、他の国もこれに続いた。

- 施設数で見ると、中東のティア3セグメントの中規模データセンターの市場シェアは現在44.7%で、次いで大規模データセンターが34%、小規模データセンターが16%、メガデータセンターが3.2%となっています。

- 中東では、このような事例がティア3認定施設の需要を牽引すると予想されます。特にティア3セグメントからのこのような需要の急増により、データセンター建設サービスのニーズは今後数年間で高まると予想されます。

サウジアラビアが同地域の主要シェアを占める展望

- サウジアラビアのデータセンター市場は、2023年に258MWのIT負荷容量で主要シェアを占めました。サウジアラビアのデータセンターインフラ整備は、国の経済基盤を拡大することを目的とした政府の「ビジョン2030」構想に後押しされて急ピッチで進められています。

- アジア、アフリカ、欧州の交差点に位置するサウジアラビアは、その戦略的立地を活かしてデータセンター市場を強化しています。紅海とアラビア湾には海底ケーブルが大量に流入し、同地域の接続性をさらに高めています。2,000年代初頭に台頭したデータセンター産業は、主に電気通信と銀行・金融セクターを対象としていました。長年にわたり、国内外からの投資が急増し、このセクターの成長に拍車がかかり、ティア3とティア4認定データセンターの開発が促進されました。

- 生産効率の向上、顧客体験の向上、通信サービスの改善、国のビジョン2030に沿ったインダストリー4.0を目的としたモノのインターネット(IoT)の採用が増加し、ICT市場の成長を牽引しています。国内のベンダーによるIoTに特化した合弁事業は、IoTソリューションとインフラに対する需要をさらに生み出しています。2022年3月、サウジ・テレコム・カンパニー(STC)は公共投資基金(PIF)と1億3,100万米ドルの提携を結び、5GとNarrowBand-IoT接続インフラを拡大するため、IoTに特化した新たなジョイントベンチャー(JV)を設立しました。

- NEOM、Red Sea、Qiddiya、Waad Alshamal、SPARKを含む現在進行中のスマートシティプロジェクトや、2030年までに最も接続されデジタル化された国家を発展させるイニシアティブが、IoT技術の採用をさらに促進する要因となっています。このようなIoTの採用拡大により、ICTベンダーは、予知保全、資産追跡、車両管理、倉庫最適化などの向けのIoTソリューションを開発し、提供する機会を得られると期待されています。

- 2023年8月、サウジアラビアはサウジアラビア中央銀行の主導でシームレス・サウジアラビア2023会議を開催すると発表しました。この会議のテーマは「サウジアラビア全土における決済、フィンテック、バンキングの未来」で、金融セクターのデジタル変革というサウジ・ビジョン2030の目標達成に向けた中央銀行の取り組みが、この会議で確固たるものとなりました。データストレージ需要の急増は、同地域におけるデータセンターの必要性を高め、データセンター建設企業の今後数年間の展望を強化する構えです。

中東データセンター建設産業概要

中東のデータセンター建設市場はかなり細分化されており、Lael O'Rourke、McLaren Construction Group PLC、Turner &Townsend、James L Williams Middle East、Alfanar Groupといった大手企業が存在します。

2023年10月、インドのデータセンター企業CtrlS Datacentersが20億米ドルの野心的な投資計画を発表しました。この投資は今後6年間で展開される予定で、アジアと中東全域でのプレゼンス強化を目的としています。同社の戦略には、AIとクラウドに対応したハイパースケールデータセンターの容量350MWの追加を目標とした大幅な拡大が含まれています。この拡大は、新規施設と、現在234MWの容量を誇る既存施設の増強の両方で実施されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

- 調査の枠組み

- 2次調査

- 1次調査

- データの三角測量と洞察の生成

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 市場力学

- 市場促進要因

- モノのインターネット(IoT)機器の成長、クラウド導入、人工知能(AI)がデータセンター建設需要を牽引

- 政府によるデジタルプログラム導入の推進がデータセンター需要を牽引

- 市場抑制要因

- データセンターの高い消費電力と排出貢献

- 市場促進要因

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 中東の主要データセンター建設統計

- 中東のデータセンター数(2022年と2023年)

- 中東のデータセンター建設中容量(MW)(2024~2029年)

- 中東データセンター建設の平均CAPEXとOPEX

- 中東のデータセンター電力吸収量(MW)(特定都市、2022年と2023年)

- 中東におけるデータセンターインフラへのCAPEX支出上位国

第5章 市場セグメンテーション

- 市場セグメンテーション:インフラ別

- 市場セグメンテーション:電気インフラ別

- 配電ソリューション

- PDU-ベーシック&スマート-メータード&スイッチドソリューション

- 転送スイッチ

- 静的

- 自動(ATS)

- 開閉装置

- 低圧

- 高圧

- パワーパネルとコンポーネント

- その他の配電ソリューション

- 電源バックアップソリューション

- UPS

- 発電機

- サービス-設計&コンサルティング、インテグレーション、サポート&メンテナンス

- 市場セグメンテーション-機械インフラ別

- 冷却システム

- 液浸冷却

- ダイレクト・ツー・チップ冷却

- リアドア熱交換器

- インローとインラック冷却

- ラック

- その他の機械インフラ

- 一般構造

- 市場セグメンテーション:電気インフラ別

- 市場セグメンテーション-ティアタイプ別

- ティア1と2

- ティア3

- ティア4

- 市場セグメンテーション:エンドユーザー別

- 銀行、金融サービス、保険

- IT・通信

- 政府と防衛

- 医療

- その他

- 市場セグメンテーション-国別

- アラブ首長国連邦

- サウジアラビア

- イスラエル

- カタール

- オマーン

第6章 競合情勢

- 企業プロファイル

- Laing O Rourke

- McLaren Construction Group PLC

- Turner & Townsend

- James L Williams Middle East

- Alfanar Group

- Saudi Technical Contracting Co.(Saudi Technical Limited)

- SALFO SA

- ICS ARABIA

- OCS Infortech LLC

- Absal Paul Contracting

第7章 投資分析

第8章 市場機会と今後の動向

第9章 出版社について

- 対象産業

- 産業クライアント一覧

- 当社のカスタマイズ調査能力

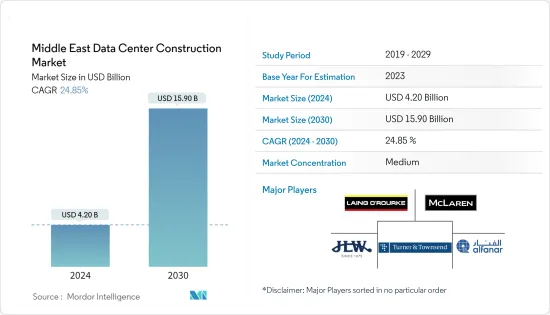

The Middle East Data Center Construction Market size is estimated at USD 4.20 billion in 2024, and is expected to reach USD 15.90 billion by 2030, growing at a CAGR of 24.85% during the forecast period (2024-2030).

In the coming years, the Middle East region is expected to increase its investment in the data center market. Several factors are facilitating the expansion of data centers in the area. The smart city ambitions of the governments in the region are driving a shift in how modern communities are built. Cities of the future, supported by digital technologies, are expected to generate massive amounts of data. It is critical to optimize data capture, storage, and processing.

Key Highlights

- The upcoming IT load capacity in the region is expected to reach 3,530 MW by 2030, which is projected to positively impact the demand for data center racks during the forecast period.

- The region's construction of raised floor area is expected to increase by 12.6 million sq. ft by 2030.

- The region's total number of racks to be installed is expected to reach 380k units by 2029. Saudi Arabia is expected to house the maximum number of racks.

- There are close to 29 submarine cable systems connecting the Middle East, and many are under construction. One such submarine cable that is estimated to start service in 2025 is India Europe Xpress (IEX), which stretches over 9,775 kilometers with a landing point in NEOM, Saudi Arabia, Yanbu, Saudi Arabia, and Salalah, Oman.

Middle East Data Center Construction Market Trends

Tier 3 Expected to Hold the Major Share in the Region

- The tier 3 segment of the data center market in the Middle East is expected to record a CAGR of 21.48% during the forecast period (2024-2030) due to the growing user base of streaming services, online gaming, smart home automation services, and other factors.

- There are around 90 tier 3 data center facilities in the Middle East. These facilities are mainly located in Dubai, Abu Dhabi, Jeddah, Fursan, Riyadh, Herzliya, Rosh HaAyin, Tel Aviv, Bnei Zion, Doha, Tehran, Amman, Aqaba, Al-Askar, Hamala, Muscat, and Bawshar.

- In 2023, the tier 3 segment dominated the market, claiming a substantial 75% share, boasting an IT load capacity exceeding 600 MW. Geographically, the United Arab Emirates led the pack with a 36% share, trailed by Saudi Arabia at 28.6% and Israel at 25.4%, with other countries following suit.

- In terms of the number of facilities, medium data centers in the tier 3 segment in the Middle East currently have a market share of 44.7%, followed by market shares of 34%, 16%, and 3.2% for large, small, and mega data centers, respectively.

- Such instances in the Middle East are expected to drive the demand for tier 3-certified facilities. This surge in demand, specifically from the tier 3 segment, is anticipated to bolster the need for data center construction services in the years ahead.

Saudi Arabia Expected to Hold Major Share in the Region

- The Saudi Arabian data center market held the major share in 2023, with an IT load capacity of 258 MW. Saudi Arabia's data center infrastructure development has surged, propelled by the government's 'Vision 2030' initiative, designed to broaden the nation's economic base.

- Positioned at the crossroads of Asia, Africa, and Europe, Saudi Arabia leveraged its strategic location to bolster its data center market. The Red Sea and Arabian Gulf witness a significant influx of subsea cables, further enhancing the region's connectivity. The data center industry, emerging in the early 2000s, primarily catered to the telecoms and banking & finance sectors. Over the years, a surge in both local and international investments has catalyzed the sector's growth, prompting the development of tier-3 and tier-4 certified data centers.

- The rising adoption of the Internet of Things (IoT) for higher production efficiency, better customer experience, improved communication services, and Industry 4.0, in line with the country's Vision 2030, is driving the ICT market's growth. The joint venture specializing in IoT by the vendors in the country is further creating demand for IoT solutions and infrastructure. In March 2022, Saudi Telecom Company (STC) formed a USD 131 million partnership with the Public Investment Fund (PIF) to establish a new joint venture (JV) specializing in IoT to expand its 5G and NarrowBand-IoT connection infrastructure.

- The ongoing smart city projects, including NEOM, Red Sea, Qiddiya, Waad Alshamal, and SPARK, and initiatives to develop the most connected and digitized nation by 2030 are the factors further fueling the adoption of IoT technology. This growing adoption of IoT is expected to provide opportunities for the ICT vendors to develop and cater IoT solutions for applications such as predictive maintenance, asset tracking, fleet management, and warehouse optimization.

- In August 2023, Saudi Arabia announced that it would host the Seamless Saudi Arabia 2023 Conference, steered by the Saudi Central Bank. The conference's theme was "The Future of Payments, Fintech and Banking across Saudi Arabia," and the meeting cemented the apex bank's efforts to achieve the Saudi Vision 2030 objective of digital transformation within the financial sector. The surge in data storage demand is poised to elevate the need for data centers in the region, thereby bolstering the prospects of data center construction firms in the coming years.

Middle East Data Center Construction Industry Overview

The Middle East data center construction market is fairly fragmented with the presence of significant players, such as Laing O'Rourke, McLaren Construction Group PLC, Turner & Townsend, James L Williams Middle East, and Alfanar Group.

In October 2023, CtrlS Datacenters, an Indian data center company, announced its ambitious investment plan of USD 2 billion. This investment, set to unfold over the next six years, is aimed at bolstering its presence across Asia and the Middle East. The company's strategy includes a significant expansion, with a target of adding 350 MW of AI and cloud-ready hyperscale data center capacity. This expansion will be implemented both in new facilities and as augmentations to its existing ones, which currently boast a capacity of 234 MW.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 The Growth of Internet of Things (IoT) Devices, Cloud adoption, and Artificial Intelligence (AI) Drives the Demand for Data Center Construction

- 4.2.1.2 The Government Push to Implement Digital Programs Driving the Demand for Data Centers

- 4.2.2 Market Restraints

- 4.2.2.1 High Power Consumption and Emission Contribution of Data Centers

- 4.2.1 Market Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Key Middle East Data Center Construction Statistics

- 4.4.1 Number of Data Centers in the Middle East, 2022 and 2023

- 4.4.2 Data Center Under Construction in the Middle East, in MW, 2024 - 2029

- 4.4.3 Average CAPEX and OPEX for the Middle East Data Center Construction

- 4.4.4 Data Center Power Capacity Absorption in MW, Selected Cities, Middle East, 2022 and 2023

- 4.4.5 The Top CAPEX Spenders on Data Center Infrastructure in the Middle East

5 MARKET SEGMENTATION

- 5.1 Market Segmentation - By Infrastructure

- 5.1.1 Market Segmentation - By Electrical Infrastructure

- 5.1.1.1 Power Distribution Solution

- 5.1.1.1.1 PDU - Basic & Smart - Metered & Switched Solutions

- 5.1.1.1.2 Transfer Switches

- 5.1.1.1.2.1 Static

- 5.1.1.1.2.2 Automatic (ATS)

- 5.1.1.1.3 Switchgear

- 5.1.1.1.3.1 Low-Voltage

- 5.1.1.1.3.2 Medium-Voltage

- 5.1.1.1.4 Power Panels and Components

- 5.1.1.1.5 Other Power Distribution Solutions

- 5.1.1.2 Power Backup Solutions

- 5.1.1.2.1 UPS

- 5.1.1.2.2 Generators

- 5.1.1.3 Service - Design & Consulting, Integration, Support & Maintenance

- 5.1.2 Market Segmentation - By Mechanical Infrastructure

- 5.1.2.1 Cooling Systems

- 5.1.2.1.1 Immersion Cooling

- 5.1.2.1.2 Direct-To-Chip Cooling

- 5.1.2.1.3 Rear Door Heat Exchanger

- 5.1.2.1.4 In-Row and In-Rack Cooling

- 5.1.2.2 Racks

- 5.1.2.3 Other Mechanical Infrastructure

- 5.1.3 General Construction

- 5.1.1 Market Segmentation - By Electrical Infrastructure

- 5.2 Market Segmentation - By Tier Type

- 5.2.1 Tier 1 and 2

- 5.2.2 Tier 3

- 5.2.3 Tier 4

- 5.3 Market Segmentation - By End User

- 5.3.1 Banking, Financial Services, and Insurance

- 5.3.2 IT and Telecommunications

- 5.3.3 Government and Defense

- 5.3.4 Healthcare

- 5.3.5 Other End Users

- 5.4 Market Segmentation - By Country

- 5.4.1 United Arab Emirates

- 5.4.2 Saudi Arabia

- 5.4.3 Israel

- 5.4.4 Qatar

- 5.4.5 Oman

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Laing O Rourke

- 6.1.2 McLaren Construction Group PLC

- 6.1.3 Turner & Townsend

- 6.1.4 James L Williams Middle East

- 6.1.5 Alfanar Group

- 6.1.6 Saudi Technical Contracting Co. (Saudi Technical Limited)

- 6.1.7 SALFO SA

- 6.1.8 ICS ARABIA

- 6.1.9 OCS Infortech LLC

- 6.1.10 Absal Paul Contracting

7 INVESTMENTS ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 ABOUT US

- 9.1 Industries Covered

- 9.2 Illustrative List of Clients in the Industry

- 9.3 Our Customized Research Capabilities