|

市場調査レポート

商品コード

1445816

日本のインスリン製剤・デリバリーデバイス市場:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Japan Insulin Drugs and Delivery Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本のインスリン製剤・デリバリーデバイス市場:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 70 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

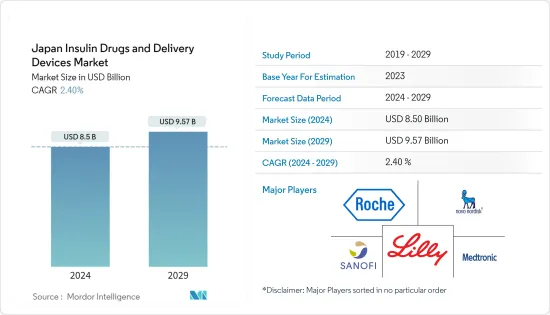

日本のインスリン製剤・デリバリーデバイス市場規模は、2024年に85億米ドルと推定され、2029年までに95億7,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に2.40%のCAGRで成長します。

COVID-19のパンデミック中の日本人の犠牲者の数は他国に比べて少なくなりましたが、これはおそらく遺伝的な違い、日本文化の側面、日本人では白人よりも凝固系の能力が弱いためと考えられます。病院の混雑を緩和するため、大阪府は患者を軽症、中等症、重症に分類し、さまざまな代替宿泊施設に割り当てました。患者は国家政府のガイドラインに従って病院で治療を受けました。中程度の患者、つまりコンピュータ断層撮影に特徴があるにもかかわらず、許容可能な酸素飽和レベルを持つ患者に重点を置いています。 1型糖尿病は免疫系の機能不全によって引き起こされますが、2型糖尿病は座りっぱなしのライフスタイルに関連しており、これが先天的なインスリン抵抗性の発症につながります。その結果、1型糖尿病はインスリン要求性として分類され、2型糖尿病はインスリン依存性として分類されます。日本は世界最大の高齢者人口を抱えているため、2型糖尿病の発症がより起こりやすくなっています。高齢化が進む日本では、糖尿病がより一般的になってきています。心血管疾患、腎臓障害、その他のさまざまな状態などの悪影響を回避するために、血糖値の監視と管理がより一般的になってきています。

前述の要因の結果、調査対象の市場は分析期間中に成長すると予想されます。

日本のインスリン製剤・デリバリーデバイス市場動向

日本の糖尿病と肥満人口の増加

日本では、病気になりやすい高齢者の増加に加え、運動不足や不規則な食生活による肥満の増加により、糖尿病患者が増加していると考えられています。もう一つの理由は、生活習慣病の予防を目的として2008年に導入されたメタボリックシンドローム検査の結果に基づいて医療機関を受診し、メタボリックシンドロームと診断される人が増えたことです。高齢化が進む日本では、糖尿病患者がさらに増加すると予想されています。糖尿病は世界の流行病として浮上しています。 IDF 2021データによると、日本には約1,100万人の糖尿病患者がいます。 1型糖尿病は免疫システムの機能不全によって引き起こされますが、2型糖尿病は座りっぱなしのライフスタイルに関連しており、固有のインスリン抵抗性を引き起こします。その結果、1型糖尿病はインスリン要求性として分類され、2型糖尿病はインスリン依存性として分類されます。日本は世界最大の高齢者人口を抱えているため、2型糖尿病の発症がより起こりやすくなっています。高齢化が進む日本では、糖尿病がより一般的になってきています。心血管疾患や腎臓障害などの悪影響を回避するために、血糖値の監視と管理が一般的になりつつあります。

以上のような要因により、市場はさらに拡大すると予想されます。

インスリンポンプセグメントは、予測期間中に最高の成長率を示すことが予想される

インスリンは、パッチに取り付けられたカニューレを介して皮下に送達されます。ポンプをAIDシステムとは独立して使用する場合、リモコンで基礎やボーラスなどの投与設定を調整できます。

予測的低血糖管理(PLGM)インスリンポンプが日本に導入されました。センサーは、低血糖値を検出または予測すると、インスリン投与を自動的に一時停止します。日本人の1型糖尿病患者におけるインスリンポンプ使用者数は約1万人と推定されており、日本ではまだインスリンポンプが浸透していないと考えられます。センサー拡張ポンプ療法を備えたMiniMed 620Gデバイス(メドトロニック、ノースリッジ、カリフォルニア州、米国)は、日本のポンプ使用者の数が少ないことを反映して2015年 2月に発売され、MiniMed 640Gデバイスはそれぞれの数年後の2018年 3月に発売されました。デバイスは欧州諸国で発売されました。 MiniMed 640Gデバイスの予測的低血糖管理(PLGM)コンポーネントは、センサーが低血糖値を検出した場合、または血糖値があらかじめ設定された低血糖制限値を20 mg/dL(1.1 mmol/L)上回ると予測される場合に、インスリン投与を自動的に一時停止します。 30分。

糖尿病は、厚生労働省(MHLW)によって優先ヘルスケアとして特定されています。 2型糖尿病の罹患率の高さは、重大な経済的負担と関連しています。糖尿病の費用は、高血圧や高脂血症などの併存疾患がある患者や合併症を発症した患者では増加します。合併症の数が増えると費用も増加します。日本では、医療保険制度が整備され、糖尿病の医療費は全額負担され、糖尿病患者は自由に医師の診察を受けることができます。また、自己注射によるインスリン療法も合法となり、健康保険が適用されます。このような利点により、日本市場でのこれらの製品の採用が促進されました。

日本のインスリン製剤・デリバリーデバイス業界の概要

日本のインスリン製剤・デリバリーデバイス市場は統合されており、主要なジェネリックプレーヤーはほとんどありません。最近、両社間で行われた合併と買収は、両社が市場での存在感を強化するのに役立ってきました。イーライリリーとベーリンガーインゲルハイムは、バサグラー(インスリングラルギン)の開発と商品化において提携関係を結んでいます。さらに、最近のプレーヤーは、企業が市場での存在感を強化するのに役立ちました。たとえば、ノボノルディスクはイプソメッドと協力して、より優れたインスリン療法ソリューションを提供しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替製品やサービスの脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 医薬品

- 基礎インスリンまたは長時間作用型インスリン

- ランタス(インスリングラルギン)

- レベミル(インスリンデテミル)

- トウジョ(インスリングラルギン)

- トレシーバ(インスリンデグルデク)

- バサグラー(インスリングラルギン)

- ボーラスまたは即効型インスリン

- NovoRapid/Novolog(インスリンアスパルト)

- ヒューマログ(インスリンリスプロ)

- アピドラ(インスリングルリシン)

- FIASP(インスリンアスパルト)

- Admelog(インスリンリスプロサノフィ)

- 従来型ヒトインスリン

- ノボリン/ミックスタード/アクタピッド/インシュラタード

- フムリン

- インスマン

- 混合インスリン

- NovoMix(二相性インスリンアスパルト)

- Ryzodeg(インスリンデグルデクおよびインスリンアスパルト)

- Xultophy(インスリンデグルデクおよびリラグルチド)

- Soliqua/Suliqua(インスリングラルギンおよびリキシセナチド)

- バイオシミラーインスリン

- インスリングラルギンバイオシミラー

- ヒトインスリンバイオシミラー

- 基礎インスリンまたは長時間作用型インスリン

- デバイス

- インスリンポンプ

- インスリンポンプデバイス

- インスリンポンプリザーバー

- インスリン注入セット

- インスリンペン

- 再利用可能ペンのカートリッジ

- 使い捨てインスリンペン

- インスリンシリンジ

- インスリンジェットインジェクター

- インスリンポンプ

第6章 市場指標

- 1型糖尿病の人口

- 2型糖尿病の人口

第7章 競合情勢

- 企業プロファイル

- Novo Nordisk

- Sanofi

- Eli Lilly

- Biocon

- Julphar

- Medtronic

- Ypsomed

- Becton Dickinson

- 企業シェア分析

第8章 市場機会と将来の動向

The Japan Insulin Drugs and Delivery Devices Market size is estimated at USD 8.5 billion in 2024, and is expected to reach USD 9.57 billion by 2029, growing at a CAGR of 2.40% during the forecast period (2024-2029).

The number of Japanese victims during the COVID-19 pandemic was lower than in other countries, possibly due to genetic differences, aspects of Japanese culture, and coagulation system characteristics that are less potent in Japanese than in Caucasians. To relieve overcrowding in hospitals, the prefectural government of Osaka classified patients as mild, moderate, or severe and assigned them to various alternative accommodations. Patients were cared for in hospitals in accordance with national government guidelines. Concentrating on moderate patients, that is, those with acceptable oxygen saturation levels despite the presence of characteristics on computed tomography. While Type 1 diabetes is caused by an immune system malfunction, Type 2 diabetes is associated with a sedentary lifestyle, which leads to the development of inherent insulin resistance. As a result, Type 1 diabetes can be classified as insulin-requiring, whereas Type 2 diabetes can be classified as insulin-dependent. Japan has one of the world's largest elderly populations, making it more vulnerable to the onset of type 2 diabetes. Diabetes is becoming more common in Japan as the country's population ages. Blood glucose monitoring and management are becoming more common in order to avoid negative consequences such as cardiovascular disease, kidney disorders, and a variety of other conditions.

As a result of the aforementioned factors, the studied market is expected to grow during the analysis period.

Japan Insulin Drugs And Delivery Devices Market Trends

Growing Diabetes and Obesity Population in Japan

Diabetes cases are thought to be increasing in Japan due to an increase in the number of older adults, who are more vulnerable to disease, as well as an increase in obesity due to a lack of exercise and irregular eating habits. Another reason is that more people have been diagnosed with the disease due to being referred to a medical facility based on the results of the metabolic syndrome examination, which was introduced in 2008 to prevent lifestyle-related diseases. Diabetes cases are expected to rise even further in Japan as the population ages. Diabetes has emerged as a global epidemic; according to IDF 2021 data, Japan has approximately 11 million diabetics. While an immune system malfunction causes Type 1 diabetes, Type 2 diabetes is associated with a sedentary lifestyle, leading to inherent insulin resistance. As a result, Type 1 diabetes can be classified as insulin-requiring, whereas Type 2 diabetes can be classified as insulin-dependent. Japan has one of the world's largest elderly populations, making it more vulnerable to the onset of type 2 diabetes. Diabetes is becoming more common in Japan as the country's population ages. Blood glucose monitoring and management are becoming more popular to avoid negative consequences such as cardiovascular disease, kidney disorders, etc.

Because of the factors above, the market is expected to expand further.

The Insulin Pumps Segment is Expected to Witness Highest Growth Rate Over the Forecast Period

Insulin is delivered subcutaneously via a cannula attached to a patch. When the pump is used independently of the AID system, a remote control can adjust administration settings such as basal and bolus.

A predictive low-glucose management (PLGM) insulin pump was introduced in Japan. The sensor automatically suspends insulin delivery when it detects or predicts low glucose levels. The number of insulin pump users among Japanese patients with type 1 diabetes mellitus is estimated to be around 10,000, implying that the insulin pump has not yet permeated Japan. The MiniMed 620G device (Medtronic, Northridge, CA, USA) with sensor-augmented pump therapy was launched in February 2015, reflecting the small number of pump users in Japan, and the MiniMed 640G device was launched in March 2018, several years after each device was launched in European countries. The MiniMed 640G device's predictive low-glucose management (PLGM) component automatically suspends insulin delivery when the sensor detects low glucose values or glucose values are predicted to rise to 20 mg/dL (1.1 mmol/L) above a preset low-glucose limit within 30 minutes.

Diabetes has been identified as a healthcare priority by the Ministry of Health, Labour, and Welfare (MHLW). The high prevalence of type 2 diabetes is associated with a significant economic burden. The costs of diabetes are increased in patients with co-morbidities such as hypertension and hyperlipidemia and in patients who develop complications. Costs increase with an increasing number of complications. Well-organized medical insurance systems cover all medical fees for diabetes mellitus, and people with diabetes can visit doctors freely in Japan. Also, insulin therapy by self-injection became legal and is covered by health insurance. Such advantages have helped the adoption of these products in the Japanese market.

Japan Insulin Drugs And Delivery Devices Industry Overview

Japan Insulin Drugs and Delivery Devices Market is consolidated, with few significant and generic players. Mergers and acquisitions that happened between the players in the recent past have helped the companies strengthen their market presence. Eli Lilly and Boehringer Ingelheim together have an alliance in developing and commercializing Basaglar (Insulin Glargine). Additionally, the players in the recent past helped the companies strengthen their market presence; for example, Novo Nordisk collaborated with Ypsomed to provide better insulin therapy solutions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Drug

- 5.1.1 Basal or Long-acting Insulins

- 5.1.1.1 Lantus (Insulin Glargine)

- 5.1.1.2 Levemir (Insulin Detemir)

- 5.1.1.3 Toujeo (Insulin Glargine)

- 5.1.1.4 Tresiba (Insulin Degludec)

- 5.1.1.5 Basaglar (Insulin Glargine)

- 5.1.2 Bolus or Fast-acting Insulins

- 5.1.2.1 NovoRapid/Novolog (Insulin aspart)

- 5.1.2.2 Humalog (Insulin lispro)

- 5.1.2.3 Apidra (Insulin glulisine)

- 5.1.2.4 FIASP (Insulin aspart)

- 5.1.2.5 Admelog (Insulin lispro Sanofi)

- 5.1.3 Traditional Human Insulins

- 5.1.3.1 Novolin/Mixtard/Actrapid/Insulatard

- 5.1.3.2 Humulin

- 5.1.3.3 Insuman

- 5.1.4 Combination Insulins

- 5.1.4.1 NovoMix (Biphasic Insulin aspart)

- 5.1.4.2 Ryzodeg (Insulin degludec and Insulin aspart)

- 5.1.4.3 Xultophy (Insulin degludec and Liraglutide)

- 5.1.4.4 Soliqua/Suliqua (Insulin glargine and Lixisenatide)

- 5.1.5 Biosimilar Insulins

- 5.1.5.1 Insulin Glargine Biosimilars

- 5.1.5.2 Human Insulin Biosimilars

- 5.1.1 Basal or Long-acting Insulins

- 5.2 Device

- 5.2.1 Insulin Pumps

- 5.2.1.1 Insulin Pump Devices

- 5.2.1.2 Insulin Pump Reservoirs

- 5.2.1.3 Insulin Infusion sets

- 5.2.2 Insulin Pens

- 5.2.2.1 Cartridges in reusable pens

- 5.2.2.2 Disposable insulin pens

- 5.2.3 Insulin Syringes

- 5.2.4 Insulin Jet Injectors

- 5.2.1 Insulin Pumps

6 MARKET INDICATORS

- 6.1 Type-1 Diabetes Population

- 6.2 Type-2 Diabetes Population

7 COMPETITIVE LANDSCAPE

- 7.1 COMPANY PROFILES

- 7.1.1 Novo Nordisk

- 7.1.2 Sanofi

- 7.1.3 Eli Lilly

- 7.1.4 Biocon

- 7.1.5 Julphar

- 7.1.6 Medtronic

- 7.1.7 Ypsomed

- 7.1.8 Becton Dickinson

- 7.2 COMPANY SHARE ANALYSIS