|

|

市場調査レポート

商品コード

1445555

日本の自動車保険: 市場シェア分析、業界動向と統計、成長予測(2024~2029)Japan Motor Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本の自動車保険: 市場シェア分析、業界動向と統計、成長予測(2024~2029) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

直接書込保険料額の観点から見た日本の自動車保険市場規模は、予測期間(2024年から2029年)中に3.41%のCAGRで、2024年の546億9,000万米ドルから2029年までに646億7,000万米ドルに成長すると予想されています。

車を購入する人が増え、人工知能(AI)を利用する企業が増えていることなどから、市場は今後数年間で成長すると予想されています。

COVID-19の世界的流行により、日本の自動車保険は自動車販売の低迷により深刻な影響を受けました。この分野はデジタル空間での地位を維持できますが、自動車保険事業全体に関する限り、依然として最も大きな影響を受けています。ロックダウンにより車両の売買ができなくなったため、パンデミックによる最悪の影響はディーラーやオフライン保険会社に及びました。

日本では、2021年度の強制自動車保険(CALI)の正味保険料は約63億米ドルでした。これはここ10年間で最低の金額でした。任意自動車保険の正味収入保険料は411億米ドル近くに達しました。自動車保険は、車の盗難や、鍵開け、悪天候、自然災害などの交通事故以外の事故によって引き起こされる損害や、静止物体との衝突によって引き起こされる損害に対して経済的保護を提供する場合があります。

日本の自動車保険市場動向

自動車の増加

2021年には、8,208万台の自動車が日本で使用されると予想され、登録台数の記録が続いています。この増加の主な要因は乗用車の登録台数でした。 2022年 3月31日の時点で、日本の路上を走っている乗用車の台数は約7,012万台で、2012年の約5,873万台から増加しています。自動二輪車や同様の車両を含む自動車の総使用台数は、2022年には7,840万台以上に達しました。

日本の人口は年々高齢化し、少子化が進んでいることは世界中の人々が知っていますが、それにもかかわらず、使用されている自動車の数は増加しています。これを正当化する1つの理由は、市場の需要側にあります。典型的な世帯人数は減少していますが、世帯数は増加し続けています。さらに、手頃な価格の小型軽量車の供給が日本市場に調整されています。

しかし、人口の変化により、登録がキャンセルされ、配布される車両の数が減り、遅かれ早かれ車両の数が減少する可能性があります。特に都市部では世帯が自分の車を購入する可能性が低いため、このプロセスは改善される可能性があります。それに代わるものとして、車両のシェア利用市場の拡大が見込まれています。

政府はテクノロジーイノベーションに注力

損害保険会社は、マーケティングや価格設定に使用するビッグデータを収集します。 AI(人工知能)を活用して保険金支払いやコールセンターなどの顧客サービス機能を評価するなど、業務の迅速化も進めています。デジタル流通チャネルの増加により、保険会社は保険契約へのアクセスが容易になりました。インシュアテック、メッセージングプラットフォーム、オンライン販売チャネルは、この国の保険情勢に貢献しています。

日本の保険会社は、さまざまな販売チャネルを通じて、さまざまな企業グループ、個人、その他の組織向けに設計された、複雑さのレベルが異なる多種多様な商品を提供しています。これにより、あらゆる最終用途顧客の新たな需要に応え、純売上を推進する方法が提供されます。

この国の地元市場関係者は、多様なセクター向けにパーソナライズされたプランをさらに展開し、より革新的なデジタル機能を開発することで、競争力をマーケティングすることに重点を置いています。

さらに、将来的には保険の販売・引受・保険金支払いの領域においてもAI(人工知能)が一次判断を行うことが期待されています。最近よく使われるようになった「フィンテック」という言葉は、保険業界でも使われています。保険業界では、保険商品を開発し、損害保険会社の業務革新を促進するための保険と情報技術の融合を指す「インシュアテック」という用語も採用されています。

日本の自動車保険業界の概要

日本の自動車保険市場の主要企業が調査の対象となっています。競合上位3社が市場シェアのほとんどを支配しているため、市場は統合されつつあります。市場は、モーターの売上高の増加、業界における人工知能(AI)の導入、その他の理由により、予測期間を通じて拡大すると予想されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の激しさ

- 自動車保険市場を形成するさまざまな規制動向に関する洞察

- 自動車保険市場における運営におけるテクノロジーとイノベーションの影響に関する洞察

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 保険適用範囲別

- 第三者賠償責任

- 総合

- 流通チャネル別

- エージェント

- ブローカー

- ダイレクト

- オンライン

- その他の流通チャネル

第6章 競合情勢

- Market Concentration and Overview

- 企業プロファイル

- Tokio Marine &Nichidio Fire Insurance Co. Ltd.

- Sompo Japan Insurance

- Mitsui Sumitomo Insurance Group

- Aioi Nissay Dowa Insurance Company, Limited

- Rakuten General Insurance Co., Ltd.

- AXA General Insurance Co. Ltd.

- Secom General Insurance Co., Ltd.

- Mitsui Direct General Insurance Co., Ltd.

- Zurich Insurance Company

- AIG General Insurance Company*

第7章 市場機会と将来の動向

第8章 免責事項と出版社について

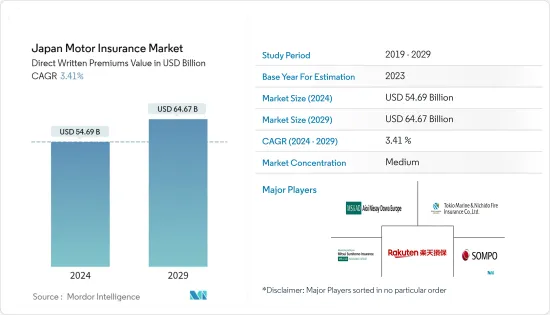

The Japan Motor Insurance Market size in terms of direct written premiums value is expected to grow from USD 54.69 billion in 2024 to USD 64.67 billion by 2029, at a CAGR of 3.41% during the forecast period (2024-2029).

The market is expected to grow over the next few years because more people are buying cars, more businesses are using artificial intelligence (AI), and other factors.

Due to the global outbreak of COVID-19, motor insurance in Japan was severely impacted due to the low sale of automobiles. Though the sector can hold itself in the digital space, it remains the most affected as far as the whole motor insurance business is concerned. The worst impact of the pandemic was on the dealers and offline insurers, as vehicles could not be bought or sold due to the lockdown.

In Japan, net premiums for mandatory auto insurance (CALI) were about USD 6.3 billion in the fiscal year 2021. This was the lowest amount in a decade. Net premiums written for voluntary car insurance reached nearly USD 41.1 billion. Motor insurance may provide financial protection against car theft and damage triggered by incidents other than traffic crashes, such as keying, bad weather, or natural disasters, as well as damage caused by colliding with stationary objects.

Japan Motor Insurance Market Trends

Increase in Motor Vehicles

In 2021, 82.08 million motor vehicles were anticipated to be in use in Japan, continuing the series of record registration numbers. The main driver of this increase was the number of passenger cars registered. As of March 31, 2022, approximately 70.12 million passenger cars were on Japan's streets, up from about 58.73 million in 2012. The total number of motor vehicles in use, including motorcycles and similar vehicles, reached over 78.4 million in 2022.

People all over the world know that Japan's population is getting older and smaller every year.Nevertheless, the number of vehicles in use is growing. One justification for this can be found on the demand side of the market. While the typical household size has decreased, the number of households has continued to grow. Furthermore, supply has adjusted to the Japanese market with affordable small and lightweight vehicles.

But the change in population is likely to cause the number of vehicles to go down sooner or later as registrations are canceled and fewer are given out. This process could be improved because households, especially in cities, are less likely to buy their own cars. As a substitute, the market for shared vehicle use is expected to increase.

Government Focus On Technology Innovations

Non-life insurance companies gather big data for use in marketing and pricing. They are also hastening their operations by using AI (artificial intelligence) to assess claims payment and customer service functions such as call centers. The rising number of digital distribution channels is encouraging insurers to offer easier access to insurance policies. Insurtech, messaging platforms, and online sales channels are conducive to the insurance landscape in the country.

Through different distribution channels, insurance companies in Japan provide a wide variety of products with differing levels of complexity that are designed for different groups of businesses, individuals, and other organizations. This will offer ways to meet the emerging demands of every end-use customer and propel net sales.

Local market players in the country are focusing on marketing their competitive edge by rolling out more plans personalized for diverse sectors and developing more innovative digital features.

Furthermore, AI (artificial intelligence) is expected to carry out primary judgment in the region of insurance sales, underwriting, and payment of claims in the future. The term "fintech," which has just come into common use, is also used in the insurance industry. The insurance industry has also adopted the term "Insurtech" to refer to the fusion of insurance and information technology for developing insurance products and encouraging innovation in non-life insurance companies' operations.

Japan Motor Insurance Industry Overview

The main companies in the Japanese motor insurance market are covered by the research. Because the top three competitors control most of the market share, the market is consolidating. The market is anticipated to expand throughout the forecast period as a result of rising motor sales, industry adoption of artificial intelligence (AI), and other reasons.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Insights on Various Regulatory Trends Shaping Motor Insurance Market

- 4.6 Insights on Impact of Technology and Innovation in Operation in the Motor Insurance Market

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Insurance Coverage

- 5.1.1 Third-party Liability

- 5.1.2 Comprehensive

- 5.2 By Distribution Channel

- 5.2.1 Agents

- 5.2.2 Brokers

- 5.2.3 Direct

- 5.2.4 Online

- 5.2.5 Other Distribution Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration and Overview

- 6.2 Company Profiles

- 6.2.1 Tokio Marine & Nichidio Fire Insurance Co. Ltd.

- 6.2.2 Sompo Japan Insurance

- 6.2.3 Mitsui Sumitomo Insurance Group

- 6.2.4 Aioi Nissay Dowa Insurance Company, Limited

- 6.2.5 Rakuten General Insurance Co., Ltd.

- 6.2.6 AXA General Insurance Co. Ltd.

- 6.2.7 Secom General Insurance Co., Ltd.

- 6.2.8 Mitsui Direct General Insurance Co., Ltd.

- 6.2.9 Zurich Insurance Company

- 6.2.10 AIG General Insurance Company*