|

市場調査レポート

商品コード

1443987

カカオ豆のバリューチェーン分析: 市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Cocoa Beans Value Chain Analysis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| カカオ豆のバリューチェーン分析: 市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 80 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

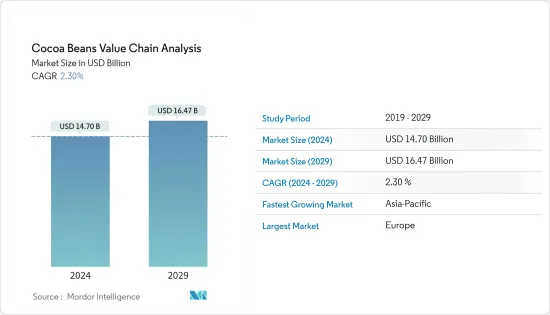

カカオ豆市場規模は2024年に147億米ドルと推定・予測され、2029年には164億7,000万米ドルに達し、予測期間中(2024-2029年)にCAGR 2.30%で成長すると予測されます。

主なハイライト

- 中間体としてのカカオ豆の需要は、中国やインドなどの新興国におけるチョコレート産業として増加すると予測されます。この製品は、機能性食品・飲食品、菓子類、医薬品、化粧品などの産業で応用されています。ミルクチョコレート、ブラウニー、ダークチョコレートなど、チョコレートのバリエーションに対する需要が高まっています。

- FAO(国連食糧農業機関)によると、2020年のカカオ豆生産量はコートジボワール、ガーナ、インドネシア、ナイジェリア、エクアドルが最も多く、220万トン、次いで80万トン、73万9,400トン、34万100トン、32万7,900トンとなっています。

- 小規模業者は農家を1軒1軒訪問し、カカオ豆を直接買い付ける。第二段階では、小規模バイヤーは卸売業者に豆を販売し、卸売業者は輸出業者に豆を再販します。もう一方の極端な例では、カカオ豆は農民協同組合によって輸出業者に直接販売されるか、あるいは現在でも協同組合によって輸出されています。

- カカオセクターは大きく成長しているが、カカオ供給側の様々な重要なリスクが、産業の潜在的な拡大を制限する可能性があります。バリューチェーン全体における価格変動と所得格差は、カカオセクターの根強い課題です。これらの課題は、政府、基準設定機関、開発機関、非公開会社を含む業界参加者が協調して取り組み、カカオ需要の継続的成長がバリューチェーン全体で公平に共有されるようにすることで対処できます。

カカオ・バリューチェーンの市場動向

利害関係者の経済向上のための持続可能な調達

カカオ豆生産は、多くの社会的・環境的持続可能性リスクに直面しています。その中には、強制労働や児童労働、不利な労働条件、土地の権利をめぐる紛争、保護林でのカカオ栽培などがあり、これらに対処しなければなりません。また、貧困、児童労働、森林破壊、土壌汚染など、人権や環境問題の複雑さが、主に小農であるカカオ農家の間で指摘されています。そのため、業界関係者は責任ある、あるいは持続可能なカカオ調達方針に重点を移し、カカオ農家を支援する活動を行うようになりました。

これには、カカオ豆の生産性と品質の向上、農業支援と教育による農家の生活水準の向上が含まれます。UTZ認証、レインフォレスト・アライアンス、フェアトレード、オーガニックはカカオセクターの主要な自主持続可能性基準(VSS)です。コートジボワール、UTZ、レインフォレスト・アライアンス、オーガニック認証は、数量、日付、売り手・買い手の情報をチェックするために、CCCのプラットフォームSYDOREに依存しています。

多くの著名な企業は、品質基準を備えた持続可能なカカオ豆の調達を達成し、健康的なカカオ豆製品の提供に活用されることを目標としています。例えば、Ferrero は2021年4月、カカオ農家の生活環境の改善と持続可能な慣行の育成を支援するため、サプライチェーン全体で完全な持続可能なカカオ豆調達を達成しました。Ferrero は、主要な認証機関や、レインフォレスト・アライアンス(UTZ)、フェアトレード、ココア・ホライズンズなどの独自に管理された基準を通じて、持続可能なカカオを調達しています。これにより、Ferrero は自社のさまざまな強みから最適な利益を得ることができ、包括的なカカオ・サステナビリティ戦略を充実させています。

世界のカカオ豆バリューチェーンにおける集中度

生産面では、コートジボワールとガーナが市場を独占しており、合わせて生産量の60%以上を占めています。これらの国々でサプライチェーンが混乱すれば、大規模なカカオ不足につながる可能性があります。カカオ市場の複雑さは、企業が資源にアクセスしやすく、規模の経済を達成しやすいという特徴があります。このため、業界では垂直的・水平的統合が進んでいます。その結果、限られた数の大手商社や加工会社が、世界および国内のカカオ市場で大きなシェアを占めています。

欧州のチョコレート・メーカーは、カカオ豆を自社で加工するか、欧州の加工業者からカカオの半製品を購入する傾向があり、カカオの半製品の輸出業者の競争は激しいです。Barry Callebaut、Cargill、ADM Cemoi、ECOM/Dutch Cocoa、Olam、Nederland SA、Crown Holland(有機のみ)といった多国籍企業が欧州に拠点を置き、欧州の食品・菓子類業界にココア半製品全般を供給しています。例えば、Barry Callebautは2022年10月、消費者の嗜好の変化に対応するため、カカオ豆の栽培、発酵、焙煎を再設計し、第2世代のチョコレート・カテゴリーを立ち上げました。さらに2021年4月、Mondelez InternationalとOlum Food Ingredients(OFI)はインドネシアで2,000ヘクタールのカカオ栽培モジュールと提携し、世界最大の持続可能な商業カカオ農場を創設しました。

これらは、最終的にチェーン全体のコスト効率を高め、最終的にチェーン全体の様々な利害関係者に還元されます。過去数年間のカカオ加工業の統合は、主に商品価格の高騰によって推進されてきました。業界はまた、持続可能な豆の調達からカカオベースの製品の生産まで活動を拡大し、垂直統合も進んでいます。

ココア・バリューチェーン業界の概要

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 サプライチェーン分析

- サプライチェーンの構造

- サプライチェーンの利害関係者

- サプライチェーン構造の問題点

第5章 バリューチェーン分析

- バリューチェーンの構造

- バリューチェーンにおける価格マークアップ

- バリューチェーンの利害関係者

- バリューチェーン構造の問題点

第6章 市場機会と今後の動向

The Cocoa Beans Market size is estimated at USD 14.70 billion in 2024, and is expected to reach USD 16.47 billion by 2029, growing at a CAGR of 2.30% during the forecast period (2024-2029).

Key Highlights

- The demand for cocoa beans as intermediates is predicted to rise as the chocolate industry in emerging economies, such as China and India. The product finds application in industries such as functional food and beverage, confectionery, pharmaceuticals, and cosmetics. There has been a rising demand for chocolate variants, such as milk chocolate, brownies, and dark chocolate.

- According to the Food and Agriculture Organization (FAO), in the year 2020, Cote d'Ivoire, Ghana, Indonesia, Nigeria, and Ecuador were the critical producer of cocoa beans volumed at 2,200.0 thousand metric tons, followed by 800.0 thousand metric tons, 739.4 thousand metric ton, 340.1 thousand metric ton, and 327.9 thousand metric ton.

- Small traders buy cocoa beans directly from farmers, visiting them one by one. In the second stage, small buyers sell the beans to wholesalers, who will re-sell them to exporters. At the other extreme of the spectrum, cocoa beans are sold directly to exporters by farmers' cooperatives or even now exported by the cooperative.

- Although the cocoa sector is growing significantly, various vital risks on the cocoa supply side can limit the potential expansion of the industry. Price volatility and income disparity across the value chain remain a persistent challenge in the sector. These challenges can be addressed by coordinated efforts between industry participants, including governments, standard-setting bodies, development organizations, and private companies, to ensure that the continued growth in cocoa demand is equitably shared across the value chain.

Cocoa Value Chain Market Trends

Sustainable Sourcing to Improve Economies for Stakeholders

Cocoa bean production faces many social and environmental sustainability risks. These include forced and child labor, unfavorable labor conditions, conflict over land rights, and the growing of cocoa in protected forests, which must be addressed. Also, the complexity of human rights and environmental issues, including poverty, child labor, forest destruction, and soil contamination, have been identified among cocoa farmers, who are primarily smallholders. Therefore, industry participants shifted their focus towards responsible or sustainable cocoa sourcing policy to undertake activities to support cacao farmers.

This includes enhancing the productivity and quality of cacao beans and improving farmers' living standards by providing farming support and education. UTZ Certified, Rainforest Alliance, Fairtrade, and Organic are the cocoa sector's primary Voluntary sustainability standards (VSS). Cote d'Ivoire, UTZ, Rainforest Alliance, and organic certifications rely on the CCC platform SYDORE to check volumes, dates, and seller/buyer information.

Many prominent players are targeted to achieve sustainable cocoa bean sourcing with quality standards and being utilized in delivering healthy cocoa bean products. For instance, in April 2021, Ferrero reached fully sustainable cocoa bean sourcing across its supply chain to help improve cocoa farmers' living conditions and foster sustainable practices. Ferrero sources sustainable cocoa through leading certification bodies and other independently managed standards such as Rainforest Alliance (UTZ), Fairtrade, and Cocoa Horizons. This ensures the company can optimally benefit from its different strengths, enriching its overarching cocoa sustainability strategy.

Concentration in the Global Cocoa Beans Value Chain

On the production side, the Ivory Coast and Ghana dominate the market together, accounting for more than 60% of the production. Any supply chain disruptions in these countries could lead to major cocoa shortages. The complexity of the cocoa market is characterized by corporations' ease of access to resources and achieving economies of scale. This has led to increased vertical and horizontal integration in the industry. As a result, a limited number of large trading and processing companies control a significant share of global and local cocoa markets.

Chocolate manufacturers in Europe tend to either process cocoa beans themselves or purchase semi-finished cocoa products from European processors, making competition for exporters of semi-finished cocoa products fierce. Multinationals such as Barry Callebaut, Cargill, ADM Cemoi, ECOM/Dutch Cocoa, Olam, Nederland SA, and Crown Holland (only organic) are based in Europe and supply the whole range of semi-finished cocoa products to the European food and confectionery industry. For instance, in October 2022, Barry Callebaut launched the second generation of the chocolate category by redesigning the farming, fermentation, and roasting of cocoa beans to address the changing consumer preferences. Further, in April 2021, Mondelez International and Olum Food Ingredients (OFI) has collabortaed in Indonesia with 2,000 hectare cocoa farming module to create the world's single largest sustainable commercial cocoa farm.

These ultimately increase the cost efficiency along the chain, which will finally be passed on to various stakeholders across the chain. Consolidations in cocoa processing over the past few years have been driven primarily by the boom in commodity prices. The industry has also well integrated vertically, expanding activities from sustainable sourcing beans to producing cocoa-based products.

Cocoa Value Chain Industry Overview

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 Supply Chain Analysis

- 4.1 Supply Chain Structure

- 4.2 Stakeholders in the Supply Chain

- 4.3 Issues with Supply Chain Structure

5 Value Chain Analysis

- 5.1 Value Chain Structure

- 5.2 Price Markups in the Value Chain

- 5.3 Stakeholders in the Value Chain

- 5.4 Issues with Value Chain Structure