|

市場調査レポート

商品コード

1693450

野菜種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Vegetable Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 野菜種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 805 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

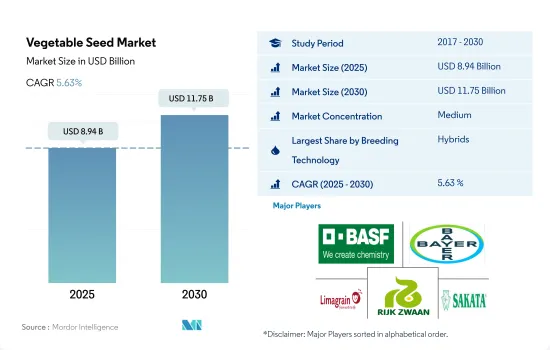

野菜種子市場規模は2025年に89億4,000万米ドルと予測され、2030年には117億5,000万米ドルに達し、予測期間(2025-2030年)のCAGRは5.63%で成長すると予測されています。

ハイブリッド品種は、高収量、害虫抵抗性、早生、均一なサイズの農産物などの形質により、野菜種子市場を独占しています。

- 世界全体では、ハイブリッド品種が2022年の野菜種子市場で80.6%のシェアを占め、一方、開放受粉野菜種子のシェアは19.4%でした。野菜生産を増強するニーズの増加と新たな害虫の出現が、世界のハイブリッド野菜種子市場を牽引しています。

- 2022年には、ウリ科植物と分類されていない野菜がハイブリッドの採用率が高い主要作物であり、世界のハイブリッド野菜種子市場のそれぞれ25.8%と22.9%を占める。トマト、キュウリ&ガーキン、カボチャ&スカッシュは、最も重要な3つの野菜作物であり、2022年の世界のハイブリッド野菜種子市場でそれぞれ13.0%、12.2%、9.7%のシェアを占めました。

- アジア太平洋は野菜の栽培にハイブリッドを使用する世界の主要地域で、2022年の世界のハイブリッド野菜種子市場の36.5%を占めました。中国とインドがこの地域の主要国で、2022年のアジア太平洋ハイブリッド野菜市場の約56.3%を占めています。

- 2022年には、非分類野菜とソラマメが、金額ベースでそれぞれ露地受粉野菜種子市場の約30.1%と25%を占める。世界全体では、トマト(14.9%)、カボチャとスカッシュ(6.5%)、キュウリとガーキン(6.3%)、レタス(6.1%)、サツマイモやキャッサバなどのその他の根菜類が、2022年の世界の露地受粉品種市場で大きなシェアを占めています。

- アジア太平洋は2022年の世界のOPV野菜種子市場の44.5%を占め、次いでアフリカが18.5%、欧州が15.2%でした。ハイブリッド種の投入コストが高く、開放受粉品種の価格が手ごろであることが、野菜栽培におけるOPVの利用を促進する要因となっています。

2022年の野菜種子の世界市場はアジア太平洋が独占

- 2022年、世界の野菜種子市場は76億8,000万米ドルと評価されました。アジア太平洋は世界最大の野菜生産国です。2022年には世界の野菜種子市場の30.2%を占めました。中国とインドがこの地域最大の野菜種子ユーザーであり、アジア太平洋の野菜種子市場のそれぞれ39%と19.8%を占めています。

- アジア太平洋地域のトマト種子市場は世界最大で、金額ベースでは世界のトマト種子市場の36.5%を占めており、ウリ科植物種子部門では世界第2位の地域で、世界のウリ科植物種子市場の35.6%を占めています。アジア太平洋におけるトマトの総栽培面積は、2022年には260万haでした。

- 欧州は世界第2位の野菜種子消費国です。2022年の世界の野菜種子市場における同地域のシェアは27.8%でした。主な栽培野菜はトマト、カボチャ&スカッシュ、タマネギ、レタスです。

- 北米は世界第3位の野菜種子消費国です。2022年には世界の野菜種子市場の22.8%を占めました。この地域ではウリ科の種子が27.9%のシェアで生産され、次いでアブラナ(22.4%)、分類されていない野菜(21.9%)、根と球根(13.8%)となっています。北米はキュウリ・ガーキンの主要シェアを占め、世界のキュウリ・ガーキン種子市場全体の28.6%を占めました。2022年の世界のキュウリ・ガーキン種子市場では、米国だけが19.6%のシェアを占めていました。

- アフリカでは、主な生育野菜科はナス科作物で、2022年には世界の分類不能野菜種子市場の20.2%、アフリカ野菜種子市場の50.6%を占める。

- 健康的な食生活の重要性に対する意識の高まりとハイブリッド種子の利用増加により、野菜の需要が急増しています。

世界の野菜種子市場動向

アジア太平洋とアフリカは、良好な農業気候条件のため、野菜の栽培面積が最も大きいです。

- 2022年の野菜栽培面積は世界の総栽培面積の約7.9%を占めました。地域間で野菜の需要が増加しており、これが世界の野菜栽培を促進する主な要因となっています。野菜栽培面積が最も大きいのはアジア太平洋で、2022年には世界の野菜栽培面積の約45.4%を占める。インドと中国は、アジア太平洋地域だけでなく世界でも有数の生産国です。野菜の輸出ポテンシャルの高さが、この地域の栽培面積を押し上げています。

- アフリカの野菜栽培面積は第2位で、2022年には約5,130万ヘクタールとなります。根菜類と球根類はこの地域で栽培されている主要な野菜作物であり、2022年のアフリカの野菜栽培面積の84.9%という大きなシェアを占めています。これは、この地域の多様な農業気候帯が、根菜・球根栽培に好条件を提供しているためです。

- 2022年には、欧州ではほぼ1,140万haで野菜が栽培されました。ロシア、ウクライナ、トルコ、フランス、スペイン、ドイツが欧州における野菜の主要栽培面積を占めており、2022年には同地域の野菜栽培面積の約69.6%を占める。消費量の増加と加工産業からの需要が、予測期間中の作付面積を押し上げると予想されます。

- 2022年には、南米ではほぼ530万haで野菜が栽培されています。ブラジルは主要な野菜生産国です。南米の野菜栽培面積の27.8%を占め、2022年には240万ヘクタールとなります。野菜需要の拡大が栽培面積を押し上げると予測されています。様々な産業や消費者における野菜需要の拡大が、予測期間中の作付面積を牽引すると予測されています。

黒腐病抵抗性キャベツ種子とカボチャ用優良品質形質への高い需要が種子市場を押し上げる

- キャベツは最も広く栽培されている野菜のひとつです。その品種は、頭の大きさ、葉の色の均一性、様々な条件への適応性、早熟性、耐病性などの特徴を持ち、主に生産者に好まれています。キャベツでは、黒腐病はXanthomonas campestris pv. campestris(XCC)によって引き起こされる主要な病害であり、作物の収量に約50%の影響を与えます。黒腐病に抵抗できる品種に対する需要は高いです。そのため、ほとんどの企業は、収量性の高いキャベツのブロック腐敗耐性品種の開発に注力しています。例えば、バイエルAG、BASF SE、サカタのタネ、シンジェンタ・グループなどの大手企業は、黒腐病、うどんこ病、べと病、その他の葉の病気などの病気に抵抗性があり、生産性が高い形質を持つ種子を提供しています。これらの種子品種は、作物の損失を防ぐことができるため、高い需要を目の当たりにしています。

- 世界的には、カボチャとスカッシュは広く栽培されている主要なウリ科植物です。カボチャとスカッシュの人気の高い特徴は、形、大きさ、色の良さ、貯蔵期間の長さ、耐病性、特にジェミニンウイルスに対する耐性、異なる気候や土壌タイプへの適応性の広さなどの品質特性です。今後、ベト病耐性やウイルス耐性、均一性、色、風味を備えた新品種の開発が各社で進められているため、耐病性や品質属性の形質がより広く利用できるようになると予想されます。例えば、2021年、エンザザーデンはオレンジサマーやバターナッツといったカボチャ種子の新品種を発売しました。

- さまざまな病気の流行、気象条件の変化、サイズや色などの高品質属性が、予測期間中に新しい種子品種の需要を増加させています。

野菜種子産業の概要

野菜種子市場は適度に統合されており、上位5社で40.55%を占めています。この市場の主要企業は以下の通りです。 BASF SE, Bayer AG, Groupe Limagrain, Rijk Zwaan Zaadteelt en Zaadhandel BV and Sakata Seeds Corporation(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 栽培面積

- 野菜

- 最も人気のある品種

- キャベツ、カボチャ、スカッシュ

- トマト、キュウリ

- 育種技術

- 野菜

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- 雑種

- 開放受粉品種とハイブリッド派生品種

- 栽培メカニズム

- 露地栽培

- 保護栽培

- 作物ファミリー

- アブラナ科

- キャベツ

- ニンジン

- カリフラワー&ブロッコリー

- その他のアブラナ

- ウリ科

- キュウリ・ガーキン

- カボチャ・スカッシュ

- その他ウリ科

- 根菜・球根

- ニンニク

- タマネギ

- ジャガイモ

- その他の根菜類

- ナス科

- 唐辛子

- ナス科

- トマト

- その他ナス科

- 分類されていない野菜

- アスパラガス

- レタス

- オクラ

- エンドウ豆

- ほうれん草

- その他分類されていない野菜

- アブラナ科

- 産地

- アフリカ

- 育種技術別

- 栽培メカニズム別

- 作物別

- 国別

- エジプト

- エチオピア

- ガーナ

- ケニア

- ナイジェリア

- 南アフリカ

- タンザニア

- その他のアフリカ

- アジア太平洋

- 育種技術別

- 栽培メカニズム別

- 作物別

- 国別

- オーストラリア

- バングラデシュ

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他アジア太平洋地域

- 欧州

- 育種技術別

- 栽培メカニズム別

- 作物別

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ポーランド

- ルーマニア

- ロシア

- スペイン

- トルコ

- ウクライナ

- 英国

- その他欧州

- 中東

- 育種技術別

- 栽培メカニズム別

- 作物別

- 国別

- イラン

- サウジアラビア

- その他中東

- 北米

- 育種技術別

- 栽培メカニズム別

- 作物別

- 国別

- カナダ

- メキシコ

- 米国

- 北米その他

- 南米

- 育種技術別

- 栽培メカニズム別

- 作物別

- 国別

- アルゼンチン

- ブラジル

- その他南米地域

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- BASF SE

- Bayer AG

- Bejo Zaden BV

- East-West Seed

- Enza Zaden

- Groupe Limagrain

- Rijk Zwaan Zaadteelt en Zaadhandel BV

- Sakata Seeds Corporation

- Takii and Co.,Ltd.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92512

The Vegetable Seed Market size is estimated at 8.94 billion USD in 2025, and is expected to reach 11.75 billion USD by 2030, growing at a CAGR of 5.63% during the forecast period (2025-2030).

Hybrids dominated the vegetable seed market due to their traits such as high yield, pest resistance, early bearing and uniform size of produce

- Globally, hybrid varieties dominated the vegetable seed market with a share of 80.6% in 2022, whereas open-pollinated vegetable seeds held a share of 19.4%. An increase in the need to boost vegetable production and the emergence of new pests are driving the global hybrid vegetable seed market.

- In 2022, cucurbits and unclassified vegetables are the major crops with higher adoption of hybrids, accounting for 25.8% and 22.9%, respectively, of the global hybrid vegetable seed market. Tomato, cucumber & gherkin, and pumpkin & squash were the three most significant vegetable crops, accounting for 13.0%, 12.2%, and 9.7% share of the global hybrid vegetable seed market, respectively, in 2022.

- Asia-Pacific was the major region in the world using hybrids in the cultivation of vegetables, accounting for 36.5% of the global hybrid vegetable seed market in 2022. China and India are the leading countries in the region, holding together about 56.3% of the Asia-Pacific hybrid vegetable market in 2022.

- In 2022, unclassified vegetables and solanaceous accounted for about 30.1% and 25%, respectively, of the open-pollinated vegetable seeds market in terms of value. Globally, tomato (14.9%), pumpkin & squash (6.5%), cucumber & gherkin (6.3%), lettuce (6.1%), and other roots such as sweet potato and cassava accounted major share in the global open-pollinated varieties market in 2022.

- Asia-Pacific was the largest region in the world under the open-pollinated varieties, accounting for 44.5% of the global OPV vegetable seed market in 2022, followed by Africa and Europe, which accounted for 18.5% and 15.2%, respectively. Higher input costs for hybrids and the high affordability of open-pollinated varieties are the factors driving the usage of OPV in vegetable cultivation.

Asia-Pacific dominated the global vegetable seed market in 2022

- In 2022, the global vegetable seed market was valued at USD 7.68 billion. Asia-Pacific is the largest vegetable producer in the world. It held 30.2% of the global vegetable seed market in 2022. China and India are the largest vegetable seeds users in the region, accounting for 39% and 19.8%, respectively, of the Asia-Pacific vegetable seeds market.

- Asia-Pacific has the largest tomato seed market in the world, with 36.5% of the global tomato seed market in terms of value, and the second largest region in the cucurbits seed segment, accounting for 35.6% of the global cucurbits seed market. The total acreage of tomatoes in Asia-Pacific was 2.6 million ha in 2022.

- Europe is the second-largest vegetable seed consumer in the world. The region's share in the respective global vegetable seed market was 27.8% in 2022. The major vegetables grown were tomato, pumpkin & squash, onion, and lettuce.

- North America is the third largest vegetable seed consumer in the world. It accounted for 22.8% of the global vegetable seed market in 2022. Cucurbit seeds were produced in the region with a share of 27.9%, followed by brassicas (22.4%), unclassified vegetables (21.9%), and roots & bulbs (13.8%). North America held the major share of the cucumber & gherkin, accounting for 28.6% of the total global cucumber and gherkin seed market. The United States alone held a 19.6% share in the global cucumber & gherkin seed market in 2022.

- In Africa, the major growing vegetable family is Solanaceae crops, accounting for 20.2% of the global unclassified vegetable seed market and 50.6% of the African vegetable seed market in 2022.

- The demand for vegetables is growing rapidly due to growing awareness of the importance of eating a healthy diet and increasing usage of hybrid seeds.

Global Vegetable Seed Market Trends

Asia-Pacific and Africa held the most significant areas under vegetable cultivation due to the favorable agroclimatic conditions

- The vegetable cultivation area accounted for about 7.9% of the total global cultivation area in 2022. There is an increasing demand for vegetables across regions, which is the major factor driving vegetable cultivation worldwide. Asia-Pacific held the largest acreage under vegetable cultivation, which accounted for about 45.4% of the global vegetable acreage in 2022. India and China are the leading producers not only in Asia-Pacific but also in the world. The high export potential of vegetables drives their cultivation area in the region.

- Africa held the second-largest area under vegetable cultivation, with about 51.3 million hectares in 2022. Roots and bulbs are major vegetable crops growing in the region, and they accounted for the major share of 84.9% of the African vegetable acreage in 2022. This is because the region's diverse agro-climatic zones provide favorable conditions for root & bulb cultivation.

- In 2022, vegetables were grown on almost 11.4 million ha in Europe. Russia, Ukraine, Turkey, France, Spain, and Germany cover the major area under vegetables in Europe, covering around 69.6% of the region's vegetable acreage in 2022. The growing consumption and demand from the processing industry are anticipated to drive the acreage during the forecast period.

- In 2022, vegetables were grown on almost 5.3 million ha in South America. Brazil is the major vegetable producer. It accounted for 27.8% of the South American vegetable cultivated area, with 2.4 million hectares in 2022. The growing demand for vegetables is projected to drive the acreage. The growing demand for vegetables across various industries and consumers is anticipated to drive the acreage during the forecast period.

High demand for cabbage seeds with black rot resistance and good quality traits for pumpkin are boosting the seed market

- Cabbage is one of the most widely cultivated vegetables. Its varieties, with characteristics such as uniformity in head size, foliage color, adaptability to various conditions, early maturity, and disease tolerance, are mainly preferred by growers. In cabbage, black rot is the major disease caused by the Xanthomonas campestris pv. campestris (XCC), and it affects crop yield by about 50%. There is a high demand for varieties that can resist black rot. Therefore, most companies focus on developing block rot-resistant varieties of cabbages with higher yield potential. For instance, major players such as Bayer AG, BASF SE, Sakata Seeds Corporation, and Syngenta Group are providing seeds with traits that are resistant to diseases, such as black rot, powdery mildew, downy mildew, and other leaf diseases, along with higher productivity. These seed varieties are witnessing high demand as they can prevent crop losses.

- Globally, pumpkin and squash are the major cucurbits widely grown. The popular traits of pumpkin and squash are quality attributes such as good shape, size, and color, longer storage life, disease resistance, especially against the geminin virus, and wider adaptability to different climatic and soil types. It is expected that in the future, the diseases resistant and quality attribute traits will be more widely available as companies are developing new varieties with mildew tolerance and virus resistance, as well as uniformity, color, and flavor. For instance, in 2021, Enza Zaden launched new pumpkin seed varieties such as Orange Summer and Butternut.

- The prevalence of different diseases, changes in weather conditions, and high-quality attributes such as size and color are increasing the demand for new seed varieties during the forecast period.

Vegetable Seed Industry Overview

The Vegetable Seed Market is moderately consolidated, with the top five companies occupying 40.55%. The major players in this market are BASF SE, Bayer AG, Groupe Limagrain, Rijk Zwaan Zaadteelt en Zaadhandel BV and Sakata Seeds Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Vegetables

- 4.2 Most Popular Traits

- 4.2.1 Cabbage, Pumpkin & Squash

- 4.2.2 Tomato & Cucumber

- 4.3 Breeding Techniques

- 4.3.1 Vegetables

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.2 Cultivation Mechanism

- 5.2.1 Open Field

- 5.2.2 Protected Cultivation

- 5.3 Crop Family

- 5.3.1 Brassicas

- 5.3.1.1 Cabbage

- 5.3.1.2 Carrot

- 5.3.1.3 Cauliflower & Broccoli

- 5.3.1.4 Other Brassicas

- 5.3.2 Cucurbits

- 5.3.2.1 Cucumber & Gherkin

- 5.3.2.2 Pumpkin & Squash

- 5.3.2.3 Other Cucurbits

- 5.3.3 Roots & Bulbs

- 5.3.3.1 Garlic

- 5.3.3.2 Onion

- 5.3.3.3 Potato

- 5.3.3.4 Other Roots & Bulbs

- 5.3.4 Solanaceae

- 5.3.4.1 Chilli

- 5.3.4.2 Eggplant

- 5.3.4.3 Tomato

- 5.3.4.4 Other Solanaceae

- 5.3.5 Unclassified Vegetables

- 5.3.5.1 Asparagus

- 5.3.5.2 Lettuce

- 5.3.5.3 Okra

- 5.3.5.4 Peas

- 5.3.5.5 Spinach

- 5.3.5.6 Other Unclassified Vegetables

- 5.3.1 Brassicas

- 5.4 Region

- 5.4.1 Africa

- 5.4.1.1 By Breeding Technology

- 5.4.1.2 By Cultivation Mechanism

- 5.4.1.3 By Crop

- 5.4.1.4 By Country

- 5.4.1.4.1 Egypt

- 5.4.1.4.2 Ethiopia

- 5.4.1.4.3 Ghana

- 5.4.1.4.4 Kenya

- 5.4.1.4.5 Nigeria

- 5.4.1.4.6 South Africa

- 5.4.1.4.7 Tanzania

- 5.4.1.4.8 Rest of Africa

- 5.4.2 Asia-Pacific

- 5.4.2.1 By Breeding Technology

- 5.4.2.2 By Cultivation Mechanism

- 5.4.2.3 By Crop

- 5.4.2.4 By Country

- 5.4.2.4.1 Australia

- 5.4.2.4.2 Bangladesh

- 5.4.2.4.3 China

- 5.4.2.4.4 India

- 5.4.2.4.5 Indonesia

- 5.4.2.4.6 Japan

- 5.4.2.4.7 Myanmar

- 5.4.2.4.8 Pakistan

- 5.4.2.4.9 Philippines

- 5.4.2.4.10 Thailand

- 5.4.2.4.11 Vietnam

- 5.4.2.4.12 Rest of Asia-Pacific

- 5.4.3 Europe

- 5.4.3.1 By Breeding Technology

- 5.4.3.2 By Cultivation Mechanism

- 5.4.3.3 By Crop

- 5.4.3.4 By Country

- 5.4.3.4.1 France

- 5.4.3.4.2 Germany

- 5.4.3.4.3 Italy

- 5.4.3.4.4 Netherlands

- 5.4.3.4.5 Poland

- 5.4.3.4.6 Romania

- 5.4.3.4.7 Russia

- 5.4.3.4.8 Spain

- 5.4.3.4.9 Turkey

- 5.4.3.4.10 Ukraine

- 5.4.3.4.11 United Kingdom

- 5.4.3.4.12 Rest of Europe

- 5.4.4 Middle East

- 5.4.4.1 By Breeding Technology

- 5.4.4.2 By Cultivation Mechanism

- 5.4.4.3 By Crop

- 5.4.4.4 By Country

- 5.4.4.4.1 Iran

- 5.4.4.4.2 Saudi Arabia

- 5.4.4.4.3 Rest of Middle East

- 5.4.5 North America

- 5.4.5.1 By Breeding Technology

- 5.4.5.2 By Cultivation Mechanism

- 5.4.5.3 By Crop

- 5.4.5.4 By Country

- 5.4.5.4.1 Canada

- 5.4.5.4.2 Mexico

- 5.4.5.4.3 United States

- 5.4.5.4.4 Rest of North America

- 5.4.6 South America

- 5.4.6.1 By Breeding Technology

- 5.4.6.2 By Cultivation Mechanism

- 5.4.6.3 By Crop

- 5.4.6.4 By Country

- 5.4.6.4.1 Argentina

- 5.4.6.4.2 Brazil

- 5.4.6.4.3 Rest of South America

- 5.4.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Bejo Zaden BV

- 6.4.5 East-West Seed

- 6.4.6 Enza Zaden

- 6.4.7 Groupe Limagrain

- 6.4.8 Rijk Zwaan Zaadteelt en Zaadhandel BV

- 6.4.9 Sakata Seeds Corporation

- 6.4.10 Takii and Co.,Ltd.

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms