|

|

市場調査レポート

商品コード

1692519

世界の半導体デバイス-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Global Semiconductor Device - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界の半導体デバイス-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

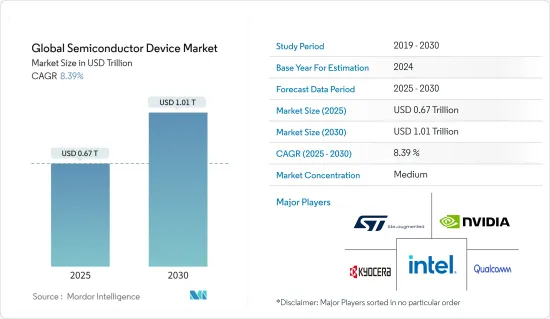

世界の半導体デバイス市場規模は、2025年に6,700億米ドルと推定され、予測期間(2025~2030年)のCAGRは8.39%で、2030年には1兆100億米ドルに達すると予測されます。

出荷量では、2025年の8,800億個から2030年には1兆2,300億個に成長し、予測期間(2025~2030年)のCAGRは7.02%と予測されます。

半導体デバイスは通常、半導体製造または集積回路(IC)製造と呼ばれる複雑なプロセスを経て製造されます。このプロセスでは、半導体材料を精密に操作して、特定の電気的挙動を持つコンポーネントを作成します。

半導体デバイスは現代のエレクトロニクスの基幹であり、スマートフォンやコンピューターから医療機器や再生可能エネルギーシステムまで、あらゆるものに電力を供給しています。半導体デバイスの主要利点のひとつは、小型でコンパクトであることです。

大きくてかさばる部品を必要とする旧来の真空管技術とは異なり、半導体デバイスは極めて小さなサイズで製造できます。この小型化によって、スマートフォン、フィットネストラッカー、スマートウォッチなど、軽量で持ち運びが容易なポータブルウェアラブルエレクトロニクスの開発が可能になりました。

半導体デバイス市場は、AIやIoTのような先端技術の採用増加により、近年著しい変貌を遂げています。これらの先端技術は、医療から自動車に至るまで様々な産業に革命的な変化の道を開き、半導体デバイス市場に新たな道を開いた。

データ消費の爆発的な伸びは、5Gの主要市場の促進要因の1つです。コネクテッドデバイス、スマートフォン、IoTアプリケーションの普及により、人々は毎日膨大な量のデータを生成しています。5Gの高い帯域幅と容量は、このデータ消費の急増をサポートし、ユーザーのシームレスな接続を可能にします。

さらに、半導体のサプライチェーンは、設計、製造、テスト、流通を含む相互接続された段階の複雑なネットワークです。プロセスはチップの設計から始まり、ウエハー製造、組立、テストと続きます。最後に、チップは様々な電子機器に使用される相手先商標製品メーカー(OEM)に供給されます。リモートワーク、eコマース、5Gの採用といった動向に後押しされた電子機器需要の急増は、半導体メーカーの供給能力を上回っています。この需要増はサプライチェーン全体を緊張させ、供給不足を招いています。

COVID-19の発生による重大な後遺症の一つは、データ利用の増加です。さらに、リモートワーク環境の増加により、データ生成量が増大する新たな機会がもたらされました。さまざまなデータセンターベンダーは、データに対する飽くなきニーズに合わせて、常に新しいデータセンターに投資しています。全米ソフトウェアサービス企業協会(NASSCOM)によると、インドのデータセンター市場への投資額は2025年に約46億米ドルに達すると予想されています。

半導体デバイス市場動向

通信産業が最大のエンドユーザーに

- 半導体は、イーサネットコントローラ、アダプタ、スイッチなど、有線通信において極めて重要な役割を果たしています。これらの半導体は、VoIP(Voice over Internet Protocol)のサポートに不可欠なPoE(Power over Ethernet)インターフェースコントローラや電力線トランシーバを備えています。

- ワイヤレス通信では、半導体はマイクロ波、赤外線、衛星、放送無線、モバイル通信システム、Wi-Fi、BluetoothやZigbeeなどの技術に使用されています。システムオンチップ(SoC)やフィールド・プログラマブル・ゲート・アレイ(FPGA)デバイスは、特に5Gをはじめとする無線通信システムの進化を牽引しています。一方、低消費電力マイクロコントローラ(MCU)は、Bluetoothの機能強化に極めて重要です。ワイヤレスセンサネットワークは、環境・構造モニタリングから資産追跡まで、多様なセグメントで応用されています。

- 無線通信に電力を供給する半導体市場は、5Gの導入が進むにつれて大きく変化しています。GSMAによると、2025年には韓国と日本の総接続数に占める5Gモバイル接続の割合はそれぞれ73%と68%になると予想されています。さらに、GCC諸国では2030年までにモバイル接続の95%が5Gとなり、アジアでは93%が5Gとなります。5Gスマートフォンとネットワークの普及が進むことで、新たな市場機会が生まれます。

- 5Gamericas.orgによると、2023年、世界の第5世代(5G)契約数は推定19億に達し、2028年には80億に急増すると予測されています。5G技術は、その前の世代と比較して、より速いダウンロード速度と大幅に低い待ち時間を誇っています。

著しい成長を遂げる中国

- 長年にわたり、中国の半導体産業は急速に拡大し、世界最大のチップ消費国のひとつとなりました。中国は、強固な国内サプライチェーンを開発することで、半導体部品の輸入依存度を下げることを目指しています。

- 例えば、2024年5月、中国は国内半導体産業を拡大するため、政府が支援する投資ファンドの第3期を設立しました。この動きは、米国の制裁を踏まえて自給自足を達成しようという中国の決意を浮き彫りにしています。

- ファンドの登録資本金は3,440億人民元(475億米ドル)です。中国集積回路産業投資ファンドは、国内トップ2のチップ鋳造会社であるセミコンダクタ・マニュファクチャリングインターナショナル・コーポレーションと華虹半導体、少数の中小企業に資金を提供しています。

- さらに、コンシューマーエレクトロニクス産業の急成長、国内製造を促進し外国技術への依存を減らすという政府の取り組みが、半導体生産設備への投資増につながったこと、人工知能やモノのインターネットなどの新興技術の台頭、電気自動車の需要増などが挙げられます。

- 中国の堅調な通信産業も、市場を大きく促進する要因となっています。例えば、中国国家統計局によると、2023年3月、中国の通信産業からの累積収入は約1,510億人民元(207億9,000万米ドル)でした。同月の前年比成長率は約4.8%でした。

半導体デバイス産業概要

半導体デバイス市場は半固定的です。統合の進展、技術の進歩、地政学的シナリオによって変動しています。鋳造メーカーとIDMの垂直統合が進んでいることに加え、市場競争も激化しています。参入企業には、Intel Corporation、Nvidia Corporation、京セラ株式会社、Qualcomm Incorporated、STMicroelectronics NVなどがあります。

2024年3月-Amazon Web ServicesとNvidiaは、Gen AIイノベーションを推進するための協業の延長を発表。顧客が先進的生成人工知能の能力を引き出すことを支援するため、BlackwellはNVIDIA GB200 Grace BlackwellスーパーチップとB100 TensorコアGPUを提供し、最も安全で先進的インフラ、ソフトウェア、サービスを提供するための両社の長年の戦略的協業を拡大します。

2024年2月-Intelコーポレーションは、AI時代に合わせたサステイナブルシステム鋳造工場であるIntel Foundryを発表。また、2020年代に向けてリーダーシップを確固たるものにするための拡大プロセスロードマップも明らかにしました。同社は、シノプシス、ケイデンス、Siemens、アンシスなどの主要パートナーが、先進的なツールと設計フローを通じてIntelファウンドリーの顧客のチップ設計を迅速化することを目指し、強力な顧客支援とエコシステムのサポートを強調しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 技術動向

- 産業のバリューチェーン/サプライチェーン分析

- COVID-19後遺症とその他のマクロ経済要因が市場に与える影響

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場の促進要因

- IoTやAIなどの技術の採用拡大

- 5Gの普及と5Gスマートフォンの需要増加

- 市場課題

- 半導体チップ不足をもたらすサプライチェーンの混乱

第6章 市場セグメンテーション

- デバイスタイプ別

- ディスクリート半導体

- オプトエレクトロニクス

- センサ

- 集積回路

- アナログ

- ロジック

- メモリー

- マイクロ

- マイクロプロセッサ(MPU)

- マイクロコントローラ(MCU)

- デジタルシグナルプロセッサ

- 産業別

- オートモーティブ

- 通信(有線と無線)

- コンシューマー

- 産業用

- コンピューティング/データストレージ

- 官公庁(航空宇宙・防衛)

- 地域別

- 米国

- 欧州

- 日本

- 中国

- 韓国

- 台湾

- その他

第7章 半導体ファウンドリーの展望

- ファウンドリー事業の売上高と鋳造メーカーの市場シェア

- 半導体売上高-IDM vsファブレス

- ファブ所在地による2021年12月末までのウエハー生産能力

- 半導体企業上位5社のウエハー生産能力とノード技術別ウエハー生産能力の推移

第8章 競合情勢

- 企業プロファイル

- Intel Corporation

- Nvidia Corporation

- Kyocera Corporation

- Qualcomm Incorporated

- STMicroelectronics NV

- Micron Technology Inc.

- Advanced Micro Devices Inc.

- NXP Semiconductors NV

- Toshiba Corporation

- Texas Instruments Inc

- Analog Devices Inc.

- SK Hynix Inc.

- Samsung Electronics Co. Ltd

- Fujitsu Semiconductor Ltd

- Rohm Co. Ltd

- Infineon Technologies AG

- Renesas Electronics Corporation

- Wolfspeed Inc.

- Broadcom Inc.

- ON Semiconductor Corporation

第9章 市場の将来展望

The Global Semiconductor Device Market size is estimated at USD 0.67 trillion in 2025, and is expected to reach USD 1.01 trillion by 2030, at a CAGR of 8.39% during the forecast period (2025-2030). In terms of shipment volume, the market is expected to grow from 0.88 trillion units in 2025 to 1.23 trillion units by 2030, at a CAGR of 7.02% during the forecast period (2025-2030).

Semiconductor devices are typically manufactured through a complex process called semiconductor fabrication or integrated circuit (IC) manufacturing. This process involves precise manipulation of the semiconductor material to create components with specific electrical behavior.

Semiconductor devices are the backbone of modern electronics, powering everything from smartphones & computers to medical devices and renewable energy systems. One of the primary advantages of semiconductor devices is their small size and compactness.

Unlike older vacuum tube technology, which requires large and bulky components, semiconductor devices can be manufactured in extremely small sizes. This miniaturization has allowed for the development of portable and wearable electronics that are lightweight and easy to carry, such as smartphones, fitness trackers, and smartwatches.

The semiconductor devices market has witnessed a significant transformation in recent years due to the increasing adoption of advanced technologies like AI and IoT. These advanced technologies have paved the way for revolutionary changes in various industries, ranging from healthcare to automotive, and have opened up new avenues for the semiconductor devices market.

The explosive growth of data consumption is one of the primary market drivers of 5G. With the proliferation of connected devices, smartphones, and IoT applications, people generate an enormous amount of data daily. 5G's higher bandwidth and capacity will support this surge in data consumption, enabling seamless connectivity for users.

Moreover, the semiconductor supply chain is a complex network of interconnected stages involving design, manufacturing, testing, and distribution. The process begins with chip design, followed by wafer fabrication, assembly, and testing. Finally, the chips are distributed to original equipment manufacturers (OEMs) who use them in various electronic devices. The surge in demand for electronic devices, driven by trends like remote working, e-commerce, and 5G adoption, has outpaced the supply capacity of semiconductor manufacturers. This increased demand has strained the entire supply chain, leading to shortages.

One of the significant aftereffects of the outbreak of COVID-19 is the increased usage of data. Moreover, it presented new opportunities for growing data generation due to increased remote working environments; various data center vendors consistently invest in new data centers in line with the insatiable need for data. According to the National Association of Software and Service Companies (NASSCOM), India's data center market investment is anticipated to reach approximately USD 4.6 billion in 2025.

Semiconductor Device Market Trends

Communication Industry to be the Largest End User

- Semiconductors play a pivotal role in wired communications, encompassing ethernet controllers, adapters, and switches. They feature Power over Ethernet (PoE) interface controllers, crucial for supporting Voice over Internet Protocol (VoIP), alongside powerline transceivers.

- In wireless communication, semiconductors are used in microwave, infrared, satellite, broadcast radio, mobile communications systems, Wi-Fi, and technologies such as Bluetooth and Zigbee. System-on-chip (SoC) and field-programmable gate array (FPGA) devices drive the evolution of wireless communication systems, notably 5G. Meanwhile, low-energy microcontrollers (MCUs) are pivotal in enhancing Bluetooth functionalities. Wireless sensor networks find applications in diverse fields, from environmental and structural monitoring to asset tracking.

- The market for semiconductors that power wireless communication is undergoing significant change with the increasing implementation of 5G. According to the GSMA, in 2025, the share of 5G mobile connections of total connections in South Korea and Japan are anticipated to account for 73% and 68%, respectively. Further, 95% of mobile connections will be 5G by 2030 in GCC states and 93% in Asia. The increasing adoption of 5G smartphones and networks creates new market opportunities.

- According to 5Gamericas.org, in 2023, the global count of fifth-generation (5G) subscriptions hit an estimated 1.9 billion, projected to soar to 8 billion by 2028. Compared to its predecessors, 5G technology boasts faster download speeds and significantly lower latency.

China to Witness Significant Growth

- Over the years, China's semiconductor industry has rapidly expanded and become one of the largest consumers of chips in the world. China aims to reduce its dependence on imported semiconductor components by developing a robust domestic supply chain.

- For instance, in May 2024, China established the third phase of a government-supported investment fund to expand its domestic semiconductor industry, which is the most significant phase to date. This move highlights China's determination to achieve self-sufficiency in light of US sanctions.

- The fund has a total registered capital of CNY 344 billion (USD 47.5 billion). The China Integrated Circuit Industry Investment Fund offers funding to the country's top two chip foundries, Semiconductor Manufacturing International Corporation and Hua Hong Semiconductor, and a few smaller companies.

- Moreover, the rapid growth of the consumer electronics industry, the government's efforts to promote domestic manufacturing and reduce reliance on foreign technology, which have led to increased investment in semiconductor production facilities, the rise of emerging technologies, such as artificial intelligence and internet of things, and the increasing demand for electric vehicles.

- The robust telecom industry in China is also a significant market driver. For instance, according to the National Bureau of Statistics of China, in March 2023, China generated a cumulative revenue of about CNY 151 billion (20.79 USD Billion) from its telecommunications industry. It had a year-on-year growth rate of approximately 4.8% that month.

Semiconductor Device Industry Overview

The semiconductor device market is semi-consolidated. It fluctuates with growing consolidation, technological advancement, and geopolitical scenarios. In addition to this increasing vertical integration of Foundries and IDMs, intense competition in the market studied is expected to rise, considering their ability to invest, which results from their revenues. Some players include Intel Corporation, Nvidia Corporation, Kyocera Corporation, Qualcomm Incorporated, and STMicroelectronics NV.

March 2024 - Amazon Web Services and Nvidia announced the extension of their collaboration to advance Gen AI innovation. To help customers unlock advanced generative artificial intelligence capabilities, Blackwell will offer the NVIDIA GB200 Grace Blackwell super chip and B100 Tensor core GPUs, which will extend the long-standing strategic collaboration between the two companies to deliver the most secure and advanced infrastructure, software, and services.

February 2024 - Intel Corporation unveiled Intel Foundry, a sustainable systems foundry tailored for the AI era. They also revealed an extended process roadmap to solidify their leadership well into the 2020s. The company emphasized strong customer backing and ecosystem support, with key partners like Synopsys, Cadence, Siemens, and Ansys, all geared to expedite chip design for Intel Foundry's clientele through advanced tools and design flows.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Trends

- 4.3 Industry Value Chain/Supply Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of Technologies like IoT and AI

- 5.1.2 Increased Deployment of 5G and Rising Demand for 5G Smartphones

- 5.2 Market Challenges

- 5.2.1 Supply Chain Disruptions Resulting in Semiconductor Chip Shortage

6 MARKET SEGMENTATION

- 6.1 By Device Type

- 6.1.1 Discrete Semiconductors

- 6.1.2 Optoelectronics

- 6.1.3 Sensors

- 6.1.4 Integrated Circuits

- 6.1.4.1 Analog

- 6.1.4.2 Logic

- 6.1.4.3 Memory

- 6.1.4.4 Micro

- 6.1.4.4.1 Microprocessors (MPU)

- 6.1.4.4.2 Microcontrollers (MCU)

- 6.1.4.4.3 Digital Signal Processors

- 6.2 By End-user Vertical

- 6.2.1 Automotive

- 6.2.2 Communication (Wired and Wireless)

- 6.2.3 Consumer

- 6.2.4 Industrial

- 6.2.5 Computing/Data Storage

- 6.2.6 Government (Aerospace and Defense)

- 6.3 By Geography

- 6.3.1 United States

- 6.3.2 Europe

- 6.3.3 Japan

- 6.3.4 China

- 6.3.5 Korea

- 6.3.6 Taiwan

- 6.3.7 Rest of the World

7 SEMICONDUCTOR FOUNDRY LANDSCAPE

- 7.1 Foundry Business Revenue and Market Shares by Foundries

- 7.2 Semiconductor Sales - IDM vs Fabless

- 7.3 Wafer Capacity By End of December 2021 Based on Fab Location

- 7.4 Wafer Capacity By Top 5 Semiconductor Companies and an Indication of Wafer Capacity by Node Technology

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Intel Corporation

- 8.1.2 Nvidia Corporation

- 8.1.3 Kyocera Corporation

- 8.1.4 Qualcomm Incorporated

- 8.1.5 STMicroelectronics NV

- 8.1.6 Micron Technology Inc.

- 8.1.7 Advanced Micro Devices Inc.

- 8.1.8 NXP Semiconductors NV

- 8.1.9 Toshiba Corporation

- 8.1.10 Texas Instruments Inc

- 8.1.11 Analog Devices Inc.

- 8.1.12 SK Hynix Inc.

- 8.1.13 Samsung Electronics Co. Ltd

- 8.1.14 Fujitsu Semiconductor Ltd

- 8.1.15 Rohm Co. Ltd

- 8.1.16 Infineon Technologies AG

- 8.1.17 Renesas Electronics Corporation

- 8.1.18 Wolfspeed Inc.

- 8.1.19 Broadcom Inc.

- 8.1.20 ON Semiconductor Corporation