|

市場調査レポート

商品コード

1549799

欧州半導体デバイス:市場シェア分析、産業動向、成長予測(2024年~2029年)Europe Semiconductor Device - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州半導体デバイス:市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 207 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

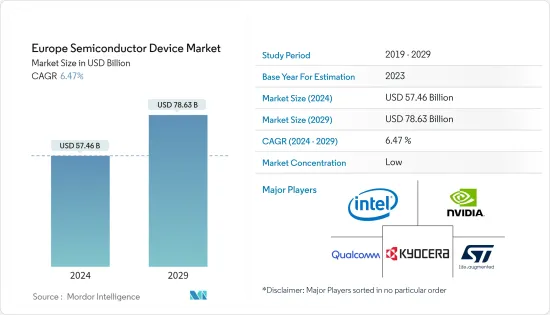

欧州半導体デバイス市場規模は、2024年に574億6,000万米ドルと推定、2029年には786億3,000万米ドルに達すると予測、予測期間(2024~2029)のCAGRは6.47%で成長します。

主要ハイライト

- 半導体デバイスは、スマートフォン、LEDテレビ、薄型モニターから民間航空宇宙や軍事システムの用途まで、幅広い電子機器において極めて重要な役割を果たしています。バイオメトリクスの進歩がこのセグメントをさらに強化します。欧州のスマートフォンやウェアラブルを含む最先端製品への意欲の高まりは、市場の軌道に顕著な影響を与えています。

- 予測期間中、欧州の半導体産業は力強い成長を遂げようとしています。この成長の原動力は、人工知能(AI)、自律走行、5G、モノのインターネットなどの最先端技術における半導体材料への需要の高まりです。この急成長は、産業企業間の競争の激化と研究開発への一貫した注力によってさらに加速しています。

- 例えば、自動車産業の自動化と電動化へのシフトは、半導体デバイスの需要を大幅に押し上げています。多様な機能を組み込んだこれらのデバイスは、インフォテインメントシステム、ナビゲーションコントロール、衝突検知メカニズムなどの自動車部品に不可欠です。このような先進的機能の統合は、自動車販売に直接影響を及ぼしています。

- インダストリー4.0、ウェアラブル、航空、医療、スマートホームなどの市場の出現とともに、データ集約的なIoTデバイスの採用が増加しており、半導体デバイスの需要をさらに押し上げています。

- 欧州の半導体市場は、政府の好意的な姿勢によって支えられています。特に、欧州委員会はチップ不足の懸念に対処するため、野心的な「チップス法」を制定しました。この計画は、欧州の半導体生産シェアを2030年までに倍増させることを目標としています。こうした構想は、今後数年間に大きな市場機会を生み出すことになります。

- しかし、この市場は、その進展を妨げる顕著な課題に取り組んでいます。特に、集積回路(IC)セグメントの複雑さが増していることが大きな障害となっています。最先端の半導体デバイスの製造と開発には、高額な価格がつきまとう。これは主に、複雑な製造プロセス、小型化の必要性、特殊な材料や装置の需要によるものです。その結果、こうした高い製造コストは半導体の価格設定に直接影響し、中小企業やコスト意識の高い消費者には手が届きにくいものとなっています。

- 半導体の供給危機は、当初はパンデミックに端を発し、予測不可能な地政学的緊張によってさらに悪化しました。半導体が経済成長と国民の幸福にとって極めて重要であることを認識した欧州委員会は、他の欧州諸国と共同で、野心的な構想を発表しました。このイニシアチブは、欧州大陸の技術的独立性を強化し、競合と回復力を高め、デジタルと環境に配慮した変革を支援するという包括的な目標を掲げて、欧州内での半導体生産を強化しようとしています。

欧州半導体デバイス市場動向

通信セグメントが最も急成長するエンドユーザーセグメント

- 半導体は通信システムにおいて極めて重要であり、トランジスタ、ダイオード、集積回路などの必須部品の生産を促進しています。これらの部品は、信号処理、増幅、変調に役立っています。有線通信機器にはイーサネット・コントローラ、アダプタ、スイッチがあり、ボイス・オーバー・インターネット・プロトコル(VoIP)用に作られたパワーオーバー・イーサネット(PoE)インターフェース・コントローラや電力線トランシーバもあります。従来、電話線の材料は導電性で知られる銅線が主流でした。産業は帯域幅を強化するため、光ファイバーに軸足を移しています。光ファイバー技術は、光検出器やLEDなど、さまざまな半導体から作られています。

- ワイヤレス通信では、半導体はマイクロ波、赤外線、衛星、放送ラジオ、モバイル通信システム、Wi-Fi、BluetoothやZigbeeなどの技術に使用されています。システムオン・チップ(SoC)やフィールド・プログラマブル・ゲート・アレイ(FPGA)デバイスは、特に5Gをはじめとする無線通信システムの進化を牽引しています。一方、低消費電力マイクロコントローラ(MCU)は、Bluetoothの機能強化に極めて重要です。

- ワイヤレスセンサ・ネットワークは、環境・構造モニタリングから資産追跡まで、多様なセグメントで応用されています。さらに、通信技術の急速な進歩により、ワイヤレス用途は拡大し、消費者の通信方法を再定義することで、現在と将来の市場成長を後押ししています。

- ETNOによると、FTTHへの累積投資額は2025年までに831億ユーロ(788億5,000万米ドル)に急増し、年間投資額は101億ユーロ(109億米ドル)に達すると予想されています。欧州全域で高速光ファイバーブロードバンドネットワークへのこのような投資が続いており、半導体デバイスの需要を牽引しています。これらのデバイスには、光トランシーバ、フォトニック集積回路、信号処理チップなどがあり、光ファイバー通信機器に不可欠です。

大きな成長が期待されるフランス

- フランス2030」計画は、特に半導体のようなセグメントで国の産業主権を強化するように設計されており、フランスの戦略的ビジョンの要となっています。フランス企業は、欧州のIPCEI ME/CTイニシアチブをはじめとする公的支援プログラムを活用し、生産・研究能力を強化しています。さらにフランスは、欧州全域で半導体生産を拡大するため、チップス法などのEUイニシアチブを活用しています。

- 半導体の研究開発を先導するため、フランス政府は、次世代技術に熱心な研究機関や大学に対する財政的支援を強化しています。

- 特に、フランスの著名な非営利半導体研究機関であるCEA-Letiは、理論研究と実用的な産業応用のギャップを埋める上で極めて重要な役割を果たしています。欧州には、ベルギーのIMEC、フィンランドのVTT技術研究センター、ドイツのフラウンホーファー協会、スペインのテクナリアなど、同様の組織が点在しています。CEA-Letiが、より大きな政府機関であるフランス代替エネルギー・原子力委員会(CEA)の傘下で運営されていることは注目に値します。

- 自動車産業はフランスにおける半導体需要の主要な牽引役です。より環境に優しい経済を目指すフランス政府の後押しとEUの厳しい排ガス規制により、自動車メーカーはEVやハイブリッド車への先進半導体技術の搭載を増やしています。OICAが発表したデータによると、フランスでは2023年に150万台の自動車が製造されました。これは、2019年に激減した後、2020年から継続的に増加しています。

- さらに、Avere Franceのデータによると、2023年にフランスで登録された電気自動車は32万8,512台でした。これは2022年の水準から大幅に増加し、2011年以来増加傾向にあります。2019~2020年にかけて、BEV登録台数は2倍以上に増加しました。

欧州半導体デバイス産業概要

欧州半導体デバイス市場はセグメント化されています。Intel Corporation、Nvidia Corporation、Kyocera Corporation、Qualcomm Technologies Inc.、STMicroelectronics NVといった市場の既存大手が存在し、鋳造メーカーとIDMの垂直統合が進むにつれて、市場は競争の激化に直面しています。ファウンドリとIDMの垂直統合が進むにつれ、同市場は競争の激化に直面しています。この競争は、各社が多額の投資を可能にする強固な収益源によって促進されています。

- 2024年2月-Intel Corporationは、AI時代に合わせたサステイナブルシステム鋳造工場であるIntel Foundryを発表しました。同社は、2030年代に向けてリーダーシップを確固たるものにすることを目指し、拡大プロセスのロードマップを明らかにしました。同社は、Synopsys、Cadence、Siemens、Ansysのような主要パートナーが、先進的なツールと設計フローを通じてIntelのファウンドリの顧客のチップ設計を迅速化することを目指し、強力な顧客支援とエコシステムのサポートを強調しています。

- 2024年1月-CES 2024で、Qualcomm Technologies Inc.とRobert Bosch GmbH社は、インフォテインメント機能とADAS(先進運転支援システム)機能を1つのシステムオンチップ(SoC)で実行できる初の中央車両コンピュータを発表しました。Qualcomm Technologies Inc.のデジタルコックピットとADASコンピュートプラットフォームのリーダーシップに基づいて構築されたFlex SoCは、混合クリティカルなワークロードをサポートするように設計されており、デジタルコックピット、ADAS、自動運転(AD)機能を1つのSoCで共同実装できます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 技術動向

- 産業バリューチェーン分析

- マクロ経済動向が市場に与える影響の評価

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- IoTやAIなどの技術の採用拡大

- 民生用電子機器製品に対する需要の高まり

- 市場課題

- 半導体製造市場における競争の激化

第6章 市場セグメンテーション

- デバイスタイプ別

- ディスクリート半導体

- オプトエレクトロニクス

- センサーとアクチュエータ

- 集積回路

- アナログ

- ロジック

- メモリー

- マイクロ

- マイクロプロセッサ(MPU)

- マイクロコントローラー(MCU)

- デジタルシグナル・プロセッサ

- 産業別

- オートモーティブ

- 通信(有線と無線)

- コンシューマー

- 産業用

- コンピューティング/データストレージ

- その他

- 国別

- ドイツ

- 英国

- フランス

第7章 競合情勢

- 企業プロファイル

- Intel Corporation

- Nvidia Corporation

- Kyocera Corporation

- Qualcomm Incorporated

- STMicroelectronics NV

- Advanced Micro Devices Inc.(Xilinx Inc.)

- NXP Semiconductors NV

- Toshiba Electronic Devices and Storage Corporation

- Samsung Electronics Co. Ltd

- ON Semiconductor Corporation

- Infineon Technologies AG

- Rohm Co. Ltd

- Analog Devices Inc.

- Texas Instrument Inc.

- Arm Holdings PLC

- Wolfspeed Inc.

- ams Osram AG

第8章 投資分析

第9章 市場の将来展望

The Europe Semiconductor Device Market size is estimated at USD 57.46 billion in 2024, and is expected to reach USD 78.63 billion by 2029, growing at a CAGR of 6.47% during the forecast period (2024-2029).

Key Highlights

- Semiconductor devices play a pivotal role in a wide array of electronic devices, spanning from smartphones, LED TVs, and flat-screen monitors to applications in civil aerospace and military systems. Advancements in biometrics are poised to further bolster this sector. Europe's increasing appetite for smartphones and cutting-edge products, including wearables, is notably influencing the market's trajectory.

- During the forecast period, the European semiconductor industry is poised for robust growth. This growth is driven by the escalating demand for semiconductor materials in cutting-edge technologies like artificial intelligence (AI), autonomous driving, 5G, and the Internet of Things. This surge is further fueled by heightened competition among industry players and a consistent focus on R&D.

- For instance, the automotive industry's shift toward automation and electrification is significantly boosting the demand for semiconductor devices. These devices, embedded with diverse functionalities, are integral to automotive components like infotainment systems, navigation controls, and collision detection mechanisms. The integration of such advanced features is directly influencing automobile sales.

- The rising adoption of data-intensive IoT devices, alongside the emergence of markets like Industry 4.0, wearables, aviation, healthcare, smart homes, and more, is further bolstering the demand for semiconductor devices.

- Europe's semiconductor market is bolstered by a favorable government stance. Notably, the European Commission, addressing chip shortage worries, initiated the ambitious 'Chips Act.' This plan aims to elevate Europe's semiconductor production share, targeting a doubling by 2030. These initiatives are poised to create significant market opportunities in the coming years.

- However, this market grapples with notable challenges that impede its progress. Notably, the integrated circuits (ICs) segment's rising complexity poses a substantial hurdle. The manufacturing and development of cutting-edge semiconductor devices come with a hefty price tag. This is primarily due to intricate manufacturing processes, the imperative of miniaturization, and the demand for specialized materials and equipment. Consequently, these high production costs directly influence semiconductor pricing, rendering them less accessible to smaller enterprises and cost-conscious consumers.

- The semiconductor supply crisis, initially sparked by the pandemic and further exacerbated by unpredictable geopolitical tensions, has prompted nations across the region to reassess their manufacturing strategies. Recognizing semiconductors as pivotal to economic growth and the well-being of their citizens, the European Commission, in collaboration with other European nations, has unveiled an ambitious initiative. This initiative seeks to ramp up semiconductor production within Europe, with the overarching goals of bolstering the continent's technological independence, enhancing its competitiveness and resilience, and supporting its digital and green transformations.

Europe Semiconductor Device Market Trends

Communication Sector to be the Fastest Growing End-user Vertical

- Semiconductors are pivotal in communication systems, facilitating the production of essential components such as transistors, diodes, and integrated circuits. These components are instrumental in signal processing, amplification, and modulation. Wired communication devices encompass Ethernet controllers, adapters, and switches, alongside Power over Ethernet (PoE) interface controllers tailored for Voice over Internet Protocol (VoIP) and powerline transceivers. Traditionally, copper, known for its electrical conductivity, dominated telephone line materials. The industry is pivoting toward fiber optics to bolster bandwidth. Fiber optic technology is crafted from various semiconductors, including photodetectors and LEDs.

- In wireless communication, semiconductors are used in microwave, infrared, satellite, broadcast radio, mobile communications systems, Wi-Fi, and technologies such as Bluetooth and Zigbee. System-on-chip (SoC) and field-programmable gate array (FPGA) devices drive the evolution of wireless communication systems, notably 5G. Meanwhile, low-energy microcontrollers (MCUs) are pivotal in enhancing Bluetooth functionalities.

- Wireless sensor networks find applications in diverse fields, from environmental and structural monitoring to asset tracking. Furthermore, with the rapid advancement of communication technologies, wireless applications are poised to expand and redefine how consumers communicate, bolstering market growth both presently and in the future.

- According to ETNO, the total cumulative investment in FTTH is expected to surge to EUR 83.1 billion (USD 78.85 billion) by 2025, with an annual investment of EUR 10.1 billion (USD 10.90 billion). Such ongoing investments in high-speed fiber optic broadband networks across Europe drive the demand for semiconductor devices. These devices include optical transceivers, photonic integrated circuits, and signal processing chips, which are crucial for fiber optic communication equipment.

France Expected to Witness Major Growth

- The "France 2030" plan, designed to bolster the nation's industrial sovereignty, particularly in sectors like semiconductors, is a cornerstone of France's strategic vision. French companies are tapping into public aid programs, notably the European IPCEI ME/CT initiative, to fortify their production and research capabilities. Moreover, France is leveraging EU initiatives, such as the Chips Act, to ramp up semiconductor production across Europe.

- In a bid to spearhead semiconductor R&D, the French Government has upped its financial backing for research institutions and universities with a keen eye on next-gen technologies.

- Notably, CEA-Leti, a prominent nonprofit semiconductor research entity in France, plays a pivotal role in bridging the gap between theoretical research and practical industry applications. Similar organizations dotting Europe include Belgium's IMEC, Finland's VTT Technical Research Center, Germany's Fraunhofer Society, and Spain's Tecnalia. It's worth noting that CEA-Leti operates under the umbrella of a larger governmental body, the French Alternative Energies and Atomic Energy Commission (CEA).

- The automotive sector is a major driver of the semiconductor demand in France. With the French Government's push for a greener economy and the EU's stringent emission regulations, automakers are increasingly integrating advanced semiconductor technologies into EVs and hybrid vehicles. According to data published by OICA, 1.5 million cars were manufactured in France in 2023. This marked a continuous increase since 2020, after a drastic fall in 2019.

- Moreover, as per Avere France data, 328,512 electric cars were registered in France in 2023. This represents a significant increase from the 2022 level and an upward trajectory since 2011. Between 2019 and 2020, BEV registrations more than doubled.

Europe Semiconductor Device Industry Overview

The European semiconductor device market is fragmented. Large market incumbents, such as Intel Corporation, Nvidia Corporation, Kyocera Corporation, Qualcomm Technologies Inc., and STMicroelectronics NV, are present, and as foundries and IDMs increasingly vertically integrate, the market faces heightened competition. This competition is fueled by their robust revenue streams, enabling them to make substantial investments.

- February 2024 - Intel Corporation unveiled Intel Foundry, a sustainable systems foundry tailored for the AI era. It revealed an extended process roadmap, aiming to solidify their leadership well into the 2030s. The company emphasized strong customer backing and ecosystem support, with key partners like Synopsys, Cadence, Siemens, and Ansys, all geared to expedite chip design for Intel Foundry's clientele through advanced tools and design flows.

- January 2024 - At CES 2024, Qualcomm Technologies Inc. and Robert Bosch GmbH introduced the first central vehicle computer capable of running infotainment and advanced driver assistance system (ADAS) functionalities on one single system-on-chip (SoC). Built on Qualcomm Technologies' leadership in digital cockpit and ADAS compute platforms, the Flex SoC is designed to support mixed-criticality workloads, allowing for digital cockpit, ADAS, and automated driving (AD) capabilities to be co-implemented on a single SoC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Trends

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of Macroeconomic Trends on the Market

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of Technologies like IoT and AI

- 5.1.2 Rising Demand for Consumer Electronics Goods

- 5.2 Market Challenges

- 5.2.1 High Competition in The Semiconductor Manufacturing Market

6 MARKET SEGMENTATION

- 6.1 By Device Type

- 6.1.1 Discrete Semiconductors

- 6.1.2 Optoelectronics

- 6.1.3 Sensors and Actuators

- 6.1.4 Integrated Circuits

- 6.1.4.1 Analog

- 6.1.4.2 Logic

- 6.1.4.3 Memory

- 6.1.5 Micro

- 6.1.5.1 Microprocessors (MPU)

- 6.1.5.2 Microcontrollers (MCU)

- 6.1.5.3 Digital Signal Processors

- 6.2 By End-user Vertical

- 6.2.1 Automotive

- 6.2.2 Communication (Wired and Wireless)

- 6.2.3 Consumer

- 6.2.4 Industrial

- 6.2.5 Computing/Data Storage

- 6.2.6 Other End Users

- 6.3 By Country

- 6.3.1 Germany

- 6.3.2 United Kingdom

- 6.3.3 France

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Intel Corporation

- 7.1.2 Nvidia Corporation

- 7.1.3 Kyocera Corporation

- 7.1.4 Qualcomm Incorporated

- 7.1.5 STMicroelectronics NV

- 7.1.6 Advanced Micro Devices Inc. (Xilinx Inc.)

- 7.1.7 NXP Semiconductors NV

- 7.1.8 Toshiba Electronic Devices and Storage Corporation

- 7.1.9 Samsung Electronics Co. Ltd

- 7.1.10 ON Semiconductor Corporation

- 7.1.11 Infineon Technologies AG

- 7.1.12 Rohm Co. Ltd

- 7.1.13 Analog Devices Inc.

- 7.1.14 Texas Instrument Inc.

- 7.1.15 Arm Holdings PLC

- 7.1.16 Wolfspeed Inc.

- 7.1.17 ams Osram AG