|

市場調査レポート

商品コード

1690928

大豆殺菌剤種子処理:市場シェア分析、産業動向、成長予測(2025~2030年)Soybean Fungicide Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 大豆殺菌剤種子処理:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

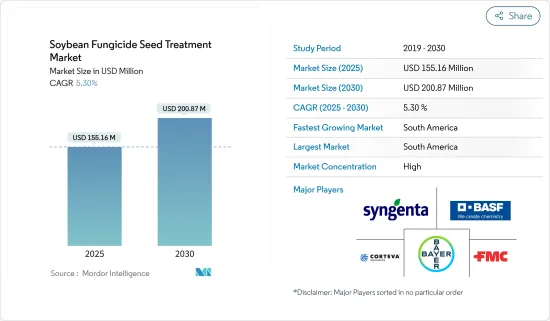

大豆殺菌剤種子処理市場規模は2025年に1億5,516万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.30%で、2030年には2億87万米ドルに達すると予測されます。

大豆殺菌剤種子処理市場は、農業従事者が健全な収量を維持するために作物を菌類病害から守ることに注力していることから拡大しています。大豆は、フィトフトラ、リゾクトニア、フザリウムなど、土壌や種子を媒介する病原菌による大きなリスクに直面しており、これらは発芽や植物の初期開発に影響を及ぼします。

世界の大豆消費量は、食品、家畜飼料、産業セクタ全体で増加し続けています。大豆は、豆腐、豆乳、代用肉など、植物性食品に不可欠なタンパク質と油脂を供給しており、健康や持続可能性への懸念から人気が高まっています。畜産業では、家禽、豚、牛の飼料として大豆ミールが使用されています。世界の畜牛頭数は、以前の15億5,770万頭から2023年には15億7,570万頭に達します。バイオ燃料産業も、バイオディーゼル生産に使用される大豆油を通じて需要を増加させています。人口の増加と食生活の嗜好の変化がこの消費の伸びを維持し、大豆殺菌剤処理市場をさらに牽引しています。

先進的な殺菌剤製剤は、複数の病原菌に対する保護を強化します。これらの処理は苗の活力を向上させ、均一な生育を確保し、環境ストレスへの耐性を強化します。産業は、従来の薬剤散布から標的を絞った種子処理に移行し、投入コストと散布の複雑さを軽減しながら、作物の生産性を最大化することに注力しています。

大豆殺菌剤種子処理剤市場は南米が大半を占め、中でもブラジルとアルゼンチンは大豆生産が盛んであるため、大きな貢献をしています。北米、特に米国は、真菌感染リスクを高める多湿条件により、大きな市場シェアを占めています。アジア太平洋市場は、特に中国とインドで大豆栽培と種子処理剤の導入が増加し、拡大しています。ITCの貿易マップによると、インドの大豆輸入量は48万9,500トンから72万4,900トンに増加しました。大豆殺菌剤種子処理剤の市場は、大豆需要の増加を背景に、予測期間中に拡大が見込まれます。

大豆殺菌種子処理剤市場の動向

生物学的種子処理への需要の急増

先進地域における環境問題への関心が生物学的種子処理剤への需要を高め、予測期間中の市場成長を牽引しています。化学企業は生物学的種子処理剤の提供を拡大することで対応しています。米国では、大手企業が生物学的処理と化学的処理を組み合わせた大豆種子を提供しています。FAOSTATによると、カナダの大豆収穫面積は2022年の211万ヘクタールから2023年には226万ヘクタールに増加します。

生物学的種子処理には、生きた微生物、発酵生成物、植物抽出物、植物ホルモン、化学化合物などの有効成分が組み込まれ、植物の開発に役立ちます。これらの処理は、植物の成長を促進し、ストレスを軽減し、植物の遺伝的ポテンシャルを最大化することによって収量を増加させる能力により人気を集めています。

米国の種子処理市場は、作物消費の増加と大豆の早期植え付けプラクティスにより拡大しています。FAOSTATによると、大豆生産量は2023年に1億1,330万トンに達します。湿った土壌での早植えは、種子や苗を昆虫、病気、害虫にさらすことが多く、保護と収量向上のために種子処理が必要となります。米国環境保護庁(EPA)は農作物や食品への化学農薬散布を監督しており、近年は多くの企業がEPA登録を取得しています。

生物学的種子処理市場に参入する企業も増えています。2022年、BASF SEはカナダの大豆栽培用にVeltyma Fungicideを登録しました。この製品は、メフェントリフルコナゾール(Revysol)とピラクロストロビンの植物健康上の利点、メトコナゾールのフザリウム防除能力を組み合わせ、包括的な大豆病害管理を記載しています。

市場を独占する南米

南米は世界の大豆生産と輸出の大半を占めており、ブラジルとアルゼンチンが主要な貢献者です。FAOによると、世界最大の大豆生産国であるブラジルは、世界の大豆生産量の40%以上を占め、アルゼンチンは輸出上位国の地位を維持しています。この地域の広大な耕地、適切な気候、近代的な農法は、食用、飼料用、バイオ燃料用の大豆の世界の需要を満たす大規模生産を可能にしています。FAOSTATによると、大豆生産量は2022年の1億2,120万トンから2023年には1億5,210万トンに増加します。ブラジルの主要大豆生産州であるマトグロッソ州、パラナ州、リオグランデ・ド・スル州は、国内生産量の大部分を占めています。アルゼンチンのパンパ地方は、確立された農業インフラに支えられた主要な大豆栽培地です。

南米は世界の大豆輸出市場を独占しており、中国が主要輸入国です。ITC貿易マップによると、ブラジルの大豆輸出量は2022年の7,890万トンから2023年には1億190万トンに増加し、アジア、欧州、北米の主要市場に供給されます。アルゼンチンはブラジルより生産量が少ないにもかかわらず、ミールやオイルなどの大豆加工品の輸出に特化しています。ブラジルのサントス港やアルゼンチンのロサリオ港など、この地域の港湾インフラは、効率的な世界流通を促進しています。これらの輸出は、特に大豆の生産量が限られている地域で、世界の食料安全保障と畜産業を支えています。

南米では、サステイナブル農業のニーズと環境意識に後押しされ、バイオ種子処理殺菌剤の需要が増加しています。大豆農業従事者は、フィトフトラ根腐病、フザリウム萎凋病、リゾクトニア枯死病など、作物の収量に影響する真菌病と闘っています。従来の化学殺菌剤からバイオベースの種子処理剤への移行は、その環境面での利点と、種子の発芽や作物の初期開発に好影響を与えることから続いています。これらのバイオ殺菌剤は、天然微生物と植物抽出物を利用し、土壌条件を改善しながら真菌病原菌を防除するもので、世界の持続可能性への取り組みを支援しています。南米は、バイオ種子処理殺菌剤のようなサステイナブル農業プラクティスの採用が増加していることに加え、強力な生産・輸出能力によって市場での地位を維持しています。

大豆殺菌剤種子処理産業概要

大豆殺菌剤種子処理の世界市場は統合されており、Syngenta Group、BASF SE、Bayer Crop Science AG、Corteva Agriscience、FMC Corporationのような主要企業が存在します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- 大豆真菌病の発生率の増加

- 高品質な作物収量に対する需要の高まり

- 政府の支援と取り組み

- 市場抑制要因

- 化学種子処理殺菌剤の悪影響

- 農薬に対する厳しい規制

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ

- ケミカル

- ノンケミカル/バイオ

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他の北米地域

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- タイ

- ベトナム

- オーストラリア

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- アフリカ

- 南アフリカ

- その他のアフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Syngenta Group

- Bayer CropScience AG

- BASF SE

- UPL

- Corteva Agriscience

- Sumitomo Chemical Co. Ltd

- FMC Corporation

第7章 市場機会と今後の動向

The Soybean Fungicide Seed Treatment Market size is estimated at USD 155.16 million in 2025, and is expected to reach USD 200.87 million by 2030, at a CAGR of 5.30% during the forecast period (2025-2030).

The soybean fungicide seed treatment market is growing as farmers focus on protecting crops against fungal diseases to maintain healthy yields. Soybeans face significant risks from soil- and seed-borne pathogens including Phytophthora, Rhizoctonia, and Fusarium, which affect germination and early plant development.

Global soybean consumption continues to rise across food, animal feed, and industrial sectors. Soybeans provide essential protein and oil for plant-based foods, including tofu, soy milk, and meat alternatives, which are increasing in popularity due to health and sustainability concerns. The livestock industry depends on soybean meal for feeding poultry, swine, and cattle. The global cattle population reached 1,575.7 million in 2023, up from 1,557.7 million previously. The biofuel industry also increases demand through soybean oil used in biodiesel production. Population growth and changing dietary preferences sustain this consumption growth further driving the soybean fungicide treatment market.

Advanced fungicide formulations provide enhanced protection against multiple pathogens. These treatments improve seedling vigor, ensure uniform growth, and strengthen environmental stress resistance. The industry is moving from traditional chemical applications to targeted seed treatments, focusing on maximizing crop productivity while reducing input costs and application complexity.

South America dominates the soybean fungicide seed treatment market, with Brazil and Argentina as major contributors due to extensive soybean production. North America, particularly the United States, represents a significant market share due to humid conditions that increase fungal infection risks. The Asia-Pacific market is expanding through increased soybean cultivation and seed treatment adoption, particularly in China and India. India's soybean imports increased to 724.9 thousand metric tons from 489.5 thousand metric tons, according to the ITC trade map. The market for soybean fungicide seed treatments is anticipated to expand during the forecast period, driven by increasing soybean demand.

Soybean Fungicide Seed Treatment Market Trends

Rapidating Demand for Biological Seed Treatment

Environmental concerns in developed regions are increasing the demand for biological seed treatments, driving market growth during the forecast period. Chemical companies are responding by expanding their biological seed treatment offerings. In the United States, major companies are providing soybean seeds treated with biological and chemical combinations. According to FAOSTAT, Canada's soybean harvested area increased from 2.11 million hectares in 2022 to 2.26 million hectares in 2023.

Biological seed treatments incorporate active ingredients such as living microbes, fermentation products, plant extracts, phytohormones, and chemical compounds to benefit plant development. These treatments are gaining popularity due to their ability to enhance plant growth, reduce stress, and increase yield by maximizing plant genetic potential.

The United States seed treatment market is expanding due to increased crop consumption and early soybean planting practices. FAOSTAT reports soybean production reached 113.3 million metric tons in 2023. Early planting in moist soils often exposes seeds and seedlings to insects, diseases, and pests, necessitating seed treatment for protection and yield improvement. The US Environmental Protection Agency (EPA) oversees chemical pesticide application on crops and food products, with numerous companies securing EPA registration in recent years.

Companies are increasingly entering the biological seed treatment market. In 2022, BASF SE registered Veltyma Fungicide for Canadian soybean farming. This product combines mefentrifluconazole (Revysol) with pyraclostrobin's plant health benefits and metconazole's Fusarium control capabilities to provide comprehensive soybean disease management.

South America Dominates the Market

South America dominates global soybean production and export, with Brazil and Argentina as major contributors. Brazil, the world's largest soybean producer, accounts for over 40% of global soybean output, while Argentina maintains its position among top exporters according to FAO. The region's extensive arable land, suitable climate, and modern farming practices enable large-scale production to meet global demand for soybeans in food, animal feed, and biofuels. According to FAOSTAT, soybean production increased from 121.2 million metric tons in 2022 to 152.1 million metric tons in 2023. Brazil's main soybean-producing states - Mato Grosso, Parana, and Rio Grande do Sul - constitute a significant portion of national output. Argentina's Pampas region serves as a primary soybean cultivation area, supported by established agricultural infrastructure.

South America controls the global soybean export market, with China as the primary importer. Brazil's soybean exports increased from 78.9 million metric tons in 2022 to 101.9 million metric tons in 2023, according to the ITC Trade map, supplying key markets in Asia, Europe, and North America. Argentina, despite lower production volumes than Brazil, specializes in exporting processed soybean products, including meal and oil. The region's port infrastructure, including Brazil's Santos Port and Argentina's Rosario Port, facilitates efficient global distribution. These exports support worldwide food security and livestock industries, particularly in regions with limited soybean production.

South America experiences increasing demand for bio seed treatment fungicides, driven by sustainable agriculture needs and environmental awareness. Soybean farmers combat fungal diseases including Phytophthora root rot, Fusarium wilt, and Rhizoctonia damping-off, which affect crop yields. The transition from conventional chemical fungicides to bio-based seed treatments continues due to their environmental benefits and positive effects on seed germination and early crop development. These biofungicides utilize natural microbes and plant extracts to control fungal pathogens while improving soil conditions, supporting global sustainability initiatives. South America maintains its market position through strong production and export capabilities, combined with increasing adoption of sustainable farming practices like bio seed treatment fungicides.

Soybean Fungicide Seed Treatment Industry Overview

The global market for soybean fungicide seed treatment is consolidated, with major players such as Syngenta Group, BASF SE, Bayer Crop Science AG, Corteva Agriscience, and FMC Corporation among others. Syngenta International AG occupies the largest market share, followed by BASF SE and Bayer Crop Science AG. Major players in the market have extended their product portfolio and taken the approach of expansion and partnerships to broaden their business and strengthen their position in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidence of Soybean Fungal Diseases

- 4.2.2 Growing Demand for High-Quality Crop Yield

- 4.2.3 Government Support and Initiatives

- 4.3 Market Restraints

- 4.3.1 Adverse Effect of Chemical Seed Treatment Fungicides

- 4.3.2 Stringent Regulations on Agrochemicals

- 4.4 Porter's Five Force Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Chemical

- 5.1.2 Non-Chemical/Biological

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.1.4 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Spain

- 5.2.2.5 Italy

- 5.2.2.6 Russia

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Thailand

- 5.2.3.5 Vietnam

- 5.2.3.6 Australia

- 5.2.3.7 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Africa

- 5.2.5.1 South Africa

- 5.2.5.2 Rest of Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Syngenta Group

- 6.3.2 Bayer CropScience AG

- 6.3.3 BASF SE

- 6.3.4 UPL

- 6.3.5 Corteva Agriscience

- 6.3.6 Sumitomo Chemical Co. Ltd

- 6.3.7 FMC Corporation