|

|

市場調査レポート

商品コード

1435768

セラミック基板:市場シェア分析、産業動向、成長予測(2024~2029年)Ceramic Substrate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| セラミック基板:市場シェア分析、産業動向、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

セラミック基板市場規模は2024年に80億5,000万米ドルと推定され、2029年までに109億8,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に6.42%のCAGRで成長すると予想されます。

セラミック基板市場は、2020年に新型コロナウイルス感染症(COVID-19)によって悪影響を受けました。しかし、新型コロナウイルス感染症のパンデミック後、業界は急速に回復しており、今後数年間で上昇すると推定されており、これがセラミック基板市場の需要を刺激すると予想されています。

主なハイライト

- 調査対象の市場を牽引する主な要因は、金属よりもセラミック基板の需要が高まっていることと、エレクトロニクス用途でのセラミック基板の採用が増加していることです。

- セラミック基板の使用に伴うコストが高く、損傷しやすく、組み立てやテスト中に慎重な取り扱いが必要であるため、予測期間中にセラミック基板市場の抑制要因となることが予想されます。

- 医療業界や自動車業界の新たな用途からの需要の増加は、予測期間中のセラミック基板市場にとってチャンスです。

- アジア太平洋地域は最大の市場を表しており、中国、インド、日本などの国々からの消費の増加により、予測期間中に最も急成長する市場になると予想されています。

セラミック基板市場動向

半導体業界からの需要の増加

- セラミック基板は、製造における重要な役割を通じて、半導体産業の発展を可能にする重要な役割を果たしています。

- 半導体メーカーは、アルミナ、酸化ベリリウム、窒化アルミニウムなどのセラミック基板を使用します。これらの材料は、硬くて耐摩耗性があり、高温での強酸やアルカリに対する耐性、良好な熱伝導率、非常に高い体積抵抗率、非常に低い誘電率と損失正接などの特性により、半導体産業で使用されています。

- 世界の半導体産業は、自動運転や人工知能などの技術の需要により、近年順調に成長しています。

- 半導体産業協会(SIA)によると、2022年の世界の半導体売上高は5,740億米ドルに達し、2021年の5,559億米ドルと比較して3.3%増加しました。

- 世界半導体貿易統計(WSTS)によると、2022年にはすべての地理的地域で半導体貿易が2桁の成長を示しました。南北アメリカ地域は17.0%、欧州は12.6%、日本は10.0%増加しました。しかし、同年のアジア太平洋の成長率は2.0%減少しました。

- したがって、成長する半導体産業により、今後数年でセラミック基板の需要が高まることが予想されます。

アジア太平洋地域が市場を独占

- アジア太平洋地域は最大の市場を占めると予想されており、予測期間中にセラミック基板の最も急成長する地域でもあると予測されています。

- 中国は今後数年間でエレクトロニクスおよび半導体製品の最大の市場になると予想されています。産業科学技術国際戦略センター(ISTI)によると、人工知能用途向けの集積回路(IC)デバイスの需要の増加により、台湾の半導体産業の生産額は大幅に増加すると予想されています。

- 中国政府は、集積回路生産の自給率を2025年までに70%に引き上げる「中国製造2025」政策を導入しました。

- 半導体産業協会(SIA)によると、2022年の中国の売上高は1,804億米ドルで半導体市場を独占し、2021年と比較して6.2%減少しました。

- インド電子半導体協会によると、同国の半導体部品市場は2025年までに323億5,000万米ドルに達すると予想されており、 CAGRは10.1%です。さらに、政府が現在進めている「Make in India」構想により、同国の半導体産業への投資が期待されます。

- さらに、インド電子半導体協会(IESA)はシンガポール半導体産業協会(SSIA)と覚書を締結し、両国のエレクトロニクスおよび半導体産業間の貿易および技術協力を確立および発展させました。これにより、インドの半導体製造におけるセラミック基板の消費範囲がさらに拡大するさまざまな画期的な半導体製造技術の開発がもたらされることが期待されています。

- 現在、日本には約30社の半導体製造産業があり、さまざまな種類の半導体チップの製造に携わっています。日本の半導体サプライチェーンは、世界の半導体製造装置の3分の1と業界の材料の半分以上を提供しています。

- さらに、フィリピンや韓国などの国も、最近調査対象となっている市場の成長に貢献しています。

- 上記の要因により、予測期間中にアジア太平洋のセラミック基板市場の需要がさらに促進されると予想されます。

セラミック基板業界の概要

世界のセラミック基板市場は、市場における重要な競合他社の存在により部分的に統合されています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 金属よりもセラミック基板の需要の増加

- エレクトロニクス用途におけるセラミック基板の採用増加

- その他の促進要因

- 抑制要因

- セラミック基板の使用に伴う高コスト

- 損傷を受けやすく、組み立てやテスト時に慎重な取り扱いが必要

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 原材料分析

第5章 市場セグメンテーション(金額ベースの市場規模)

- タイプ

- アルミナ

- 窒化アルミニウム

- 窒化ケイ素

- 酸化ベリリウム

- その他

- エンドユーザー産業

- コンシューマーエレクトロニクス

- 航空宇宙・防衛

- 自動車

- 半導体

- 通信

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- CeramTec GmbH

- CoorsTek Inc.

- Corning Incorporated

- ICP TECHNOLOGY Co.,LTD

- KOA Speer Electronics INC.

- KYOCERA Corporation

- LEATEC Fine Ceramics Co,.Ltd.

- MARUWA Co., Ltd.

- NEOTech

- NIPPON CARBIDE INDUSTRIES CO., INC.

- Niterra Co., Ltd.

- Ortech Advanced Ceramics

- TOSHIBA MATERIALS Co. LTD.,

- TTM Technologies Inc.

- Yokowo co., ltd.

第7章 市場機会と今後の動向

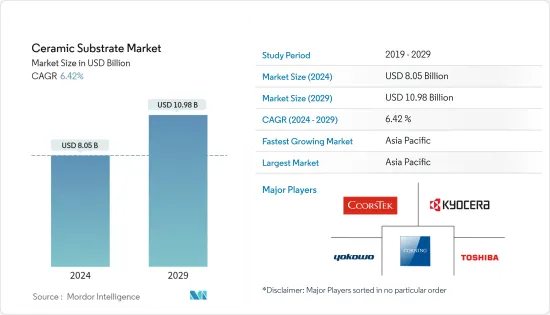

The Ceramic Substrate Market size is estimated at USD 8.05 billion in 2024, and is expected to reach USD 10.98 billion by 2029, growing at a CAGR of 6.42% during the forecast period (2024-2029).

The ceramic substrate market was negatively impacted by COVID-19 in 2020. However, post-COVID-19 pandemic, the industries are recovering fast and are estimated to rise in the coming years, which will stimulate the demand for the ceramic substrate market.

Key Highlights

- The major factor driving the market studied are the increasing demand for ceramic substrates over metal and the rise in the adoption of ceramic substrates in electronics applications.

- The high cost associated with the use of ceramic substrate and prone to damage and need careful handling during assembly and testing is expected to act as a restraint for the ceramic substrate market during the forecast period.

- Increasing demand from the medical industry and emerging applications in the automotive industry is an opportunity for ceramic substrate market during the forecast period.

- Asia-Pacific region represents the largest market and is also expected to be the fastest-growing market over the forecast period owing to the increasing consumption from countries such as China, India, and Japan.

Ceramic Substrate Market Trends

Increasing Demand from the Semiconductor Industry

- Ceramic substrate plays an important role in enabling developments in the semiconductor industry through their essential role in manufacturing.

- Semiconductor manufacturers use ceramic substrates such as alumina, beryllium oxide, and aluminum nitride. These materials are used in the semiconductor industry owing to their properties such as hard and resistant to wear, resistant to strong acid and alkali at high temperatures, good thermal conductivity, extremely high bulk resistivity, very low dielectric constant and loss tangent among others.

- The global semiconductor industry is growing at a healthy rate in recent times, owing to the demand for technologies such as autonomous driving, artificial intelligence, etc.

- According to the Semiconductor Industry Association (SIA), in 2022, the worldwide sales of semiconductors reached to USD 574 billion which was increase by 3.3% compared to 2021 at USD 555.9 billion.

- According to World Semiconductor Trade Statistics (WSTS), In 2022, all geographical regions exhibited double-digit growth in trade of semiconductors. The Americas region has increased by 17.0%, Europe by 12.6%, and Japan by 10.0%. However, The growth of Asia-Pacific has declined by 2.0% in the same year.

- Therefore, the growing semiconductor industry is expected to boost the demand for ceramic substrates incoming years.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to account for the largest market and is also forecasted to be the fastest-growing region for ceramic substrates during the forecast period.

- China is expected to become the largest market for electronics and semiconductor products over the coming years. According to the Industry, Science and Technology International Strategy Center (ISTI), the production value of Taiwan's semiconductor industry is anticipated to grow substantially, owing to the increasing demand for integrated circuit (IC) devices for artificial intelligence applications.

- The Chinese government has introduced the 'Made in China 2025' policy to increase the nation's self-sufficiency in integrated circuits production to 70% by 2025.

- According to Semiconductor Industry Association (SIA), in 2022, China dominated the semiconductor market with sales of USD 180.4 billion which declined as compared to 2021 by 6.2%.

- According to India Electronics and Semiconductor Association, the semiconductor component market in the country is expected to be worth USD 32.35 billion by 2025, displaying a CAGR of 10.1%. In addition, the ongoing Make in India initiative by the government is expected to result in investments in the semiconductor industry in the country.

- Additionally, India Electronics and Semiconductor Association (IESA) signed a MoU with Singapore Semiconductor Industry Association (SSIA) to establish and develop trade and technical cooperation between the electronics and semiconductor industries of both the countries. This is expected to result in development of various break-through semiconductor manufacturing technologies that would further increase the scope for the consumption of ceramic substrate in semiconductor manufacturing in India.

- Japan currently has about 30 semiconductor fabrication industries, which are involved in manufacturing of various types of semiconductor chips. Japan's semiconductor supply chain provides one third of the world's semiconductor manufacturing equipment and more than half of the industry's materials.

- Furthermore, countries such as Philippines and South Korea have also been contributing to the growth of the market studied lately.

- The above mentioned factors are expected to further drive the demand for ceramic substrate market in Asia-Pacific over the forecast period.

Ceramic Substrate Industry Overview

The Global Ceramic Substrate market is partially consolidated with the presence of significant competitors in the market. The major companies in the market are Corning Incorporated, CoorsTek Inc. TOSHIBA MATERIALS Co. LTD., KYOCERA Corporation, and Yokowo co., ltd. among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Ceramic Substrates Over Metal

- 4.1.2 Rise in the Adoption of Ceramic Substrates in Electronics Application

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost Associated with the Use of Ceramic Substrate

- 4.2.2 Prone to Damage and Need Careful Handling During Assembly and Testing

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porters Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Raw Material Analysis

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Alumina

- 5.1.2 Aluminum Nitride

- 5.1.3 Silicon Nitride

- 5.1.4 Beryllium Oxide

- 5.1.5 Others

- 5.2 End-user Industry

- 5.2.1 Consumer Electronics

- 5.2.2 Aerospace & Defense

- 5.2.3 Automotive

- 5.2.4 Semiconductor

- 5.2.5 Telecommunication

- 5.2.6 Others

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 CeramTec GmbH

- 6.4.2 CoorsTek Inc.

- 6.4.3 Corning Incorporated

- 6.4.4 ICP TECHNOLOGY Co.,LTD

- 6.4.5 KOA Speer Electronics INC.

- 6.4.6 KYOCERA Corporation

- 6.4.7 LEATEC Fine Ceramics Co,.Ltd.

- 6.4.8 MARUWA Co., Ltd.

- 6.4.9 NEOTech

- 6.4.10 NIPPON CARBIDE INDUSTRIES CO.,INC.

- 6.4.11 Niterra Co., Ltd.

- 6.4.12 Ortech Advanced Ceramics

- 6.4.13 TOSHIBA MATERIALS Co. LTD.,

- 6.4.14 TTM Technologies Inc.

- 6.4.15 Yokowo co., ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand From Medical Industry

- 7.2 Emerging Applications in Automotive Industry