|

|

市場調査レポート

商品コード

1322926

サワードウの世界市場:タイプ別(タイプI、タイプII、タイプIII)、用途別(パン・バンズ、クッキー、ケーキ、ピザ)、原材料別(小麦、大麦、オーツ麦)、地域別(北米、欧州、アジア太平洋、南米、その他の地域)-2028年までの予測Sourdough Market by Type (Type I, Type II and Type III), Application (Bread & Buns, Cookies, Cakes, Pizza), Ingredients (Wheat, Barley, and Oats), and Region (North America, Europe, APAC, South America, RoW) - Global Forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| サワードウの世界市場:タイプ別(タイプI、タイプII、タイプIII)、用途別(パン・バンズ、クッキー、ケーキ、ピザ)、原材料別(小麦、大麦、オーツ麦)、地域別(北米、欧州、アジア太平洋、南米、その他の地域)-2028年までの予測 |

|

出版日: 2023年07月24日

発行: MarketsandMarkets

ページ情報: 英文 227 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

サワードウの市場規模は2023年に23億米ドルと推計され、2028年には35億米ドルに達すると予測されており、CAGRは9.0%と見込まれています。

クリーンラベルと天然素材への動向が、サワードウ製品の需要をさらに増大させています。職人的な企業と商業的な企業の両方を含むベーカリー業界の拡大は、サワードウ製品の導入と販売促進によって市場成長に貢献しています。様々な小売チャネルでサワードウ製品が入手可能になることで、入手しやすさと市場拡大が促進されます。さらに、サワードウの風味、食感、用途の多様性は製品の革新を可能にし、より幅広い消費者層にアピールします。全体として、サワードウ市場の成長予測は、消費者の嗜好の進化、健康志向、クリーン・ラベル・トレンド、ベーカリー業界の拡大が原動力となっています。

タイプIIIのサワードウは、他のタイプに比べて複雑さと風味が強化されており、独特の味覚体験のために果物や蜂蜜のような材料を取り入れています。消費者が高級で職人的なサワードウ製品をますます求めるようになっているため、タイプIIIは多様で贅沢な風味を求める消費者の需要に応えています。その他の特典として、このセグメントは、特殊でニッチなベーカリー製品への関心の高まりや、ナチュラルでクリーンラベルな製品への動向から利益を得ています。タイプIIIのサワードウは、天然香料と天然原材料を使用し、健康志向の消費者にアピールしています。全体として、タイプIIIの成長は、その複雑さ、プレミアムなポジショニング、冒険好きな消費者へのアピール、現在の市場動向との整合性によって促進されています。

パンとバンズは世界中で消費される主食であり、安定した高い需要基盤を提供しています。職人的なパンや特殊なパンの人気の高まりは、ピリッとした風味、改善された食感、保存期間の延長といったサワードウのユニークな品質と一致しています。この分野の多様性はカスタマイズを可能にし、サイズ、形状、風味の面で多様な消費者の嗜好に応えます。業務用ベーカリー、小売店、食品施設を通じてパンとバンズが広く入手可能であることが、このセグメントの優位性をさらに高めています。全体として、パン・饅頭分野は、その普遍的な魅力、職人技を駆使したパンに対する消費者の関心の高まり、これらの製品へのアクセスにおける利便性から利益を得ており、予測期間における最大市場シェアにつながっています。

酵素を多く含むなど大麦特有の特性は、サワードウ製品の食感や風味の向上に寄与しています。より健康的で代替穀物に対する消費者の関心の高まりが、大麦ベースのサワードウ製品の需要を牽引しています。大麦はその栄養価の高さで知られ、クリーンラベルや天然素材の動向に合致しています。その汎用性により、市場内での革新と製品の差別化が可能になります。健康志向の消費者が栄養価が高く健康的な選択肢を求める中、大麦分野は大きな成長が見込まれます。大麦は、その用途が認知され親しまれていることから、透明性と加工度の低い原材料を優先する消費者にアピールします。全体として、大麦ベースのサワードウ製品に対する需要の高まりとその有利な特性は、サワードウ市場において大麦部門を最も高いCAGRに位置づけています。

アジア太平洋は、都市化と可処分所得の増加と相まって、大規模かつ急速に拡大する人口を抱え、より健康的で多様な食品オプションへの需要を牽引しています。アジアにおける豊かな食文化遺産と発酵食品に対する文化的親和性は、サワードウ製品の自然市場に貢献しています。加えて、世界の食生活動向と世界化の影響により、サワードウを含む職人的な自然派パンの受容と需要が拡大しています。消費者の健康志向の高まりと、サワードウ発酵に伴う潜在的な健康効果が、さらに成長を後押ししています。ベーカリー産業の拡大、技術の進歩、研究開発への投資もアジア太平洋地域におけるサワードウ市場の急成長に寄与しています。

当レポートでは、世界のサワードウ市場について調査し、市場の概要とともに、タイプ別、用途別、原材料別、地域別動向、および市場に参入する企業のプロファイルなどを提供しています。

>目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

第6章 業界の動向

- イントロダクション

- バリューチェーン分析

- 顧客のビジネスに影響を与える動向/混乱

- 関税と規制状況

- 規制の枠組み

- 北米

- 欧州連合

- アジア太平洋

- 南米

- 特許分析

- 貿易分析

- 価格分析

- エコシステム分析

- 技術分析

- ポーターのファイブフォース分析

- 主要な利害関係者と購入基準

- 2023年~2024年の主要な会議とイベント

第7章 サワードウ市場、原材料別

- イントロダクション

- 小麦

- 大麦

- オーツ麦

第8章 サワードウ市場、タイプ別

- イントロダクション

- タイプI

- タイプⅡ

- タイプⅢ

第9章 サワードウ市場、用途別

- イントロダクション

- パン・バンズ

- クッキー

- ケーキ

- ピザ

- その他

第10章 サワードウ市場、地域別

- イントロダクション

- 北米

- 欧州

- アジア太平洋

- 南米

- その他の地域

第11章 競合情勢

- 概要

- 主要企業の過去の収益分析

- 主要プレーヤーが採用した戦略

- 主要な市場参入企業の世界スナップショット

- 市場シェア分析

- 主要企業の企業評価マトリックス、2022年

- スタートアップ/中小企業の企業評価マトリックス、2022年

- 競合シナリオ

第12章 企業プロファイル

- 主要参入企業

- PURATOS

- IREKS GMBH

- LALLEMAND INC.

- LESAFFRE

- GOODMILLS

- GOLD COAST BAKING COMPANY

- BOUDIN BAKERY

- PHILIBERT SAVOURS

- ERNST BOCKER GMBH & CO. KG

- BAKE WITH BROLITE

- SEMIFREDDI'S

- KING ARTHUR BAKING COMPANY, INC.

- DR. SUWELACK

- CULTURES FOR HEALTH

- LA BREA BAKERY

- スタートアップ/中小企業

- ITALMILL

- POILANE

- THE ACME BREAD COMPANY

- THE SOURDOUGH COMPANY

- THEOBROMA

第13章 隣接市場および関連市場

第14章 付録

According to MarketsandMarkets, the Sourdough market size is estimated to be valued at USD 2.3 billion in 2023 and is projected to reach USD 3.5 billion by 2028, recording a CAGR of 9.0 % in terms of value. The trend towards clean labels and natural ingredients further amplifies the demand for sourdough products. The expanding bakery industry, including both artisanal and commercial players, contributes to market growth by introducing and promoting sourdough offerings. The availability of sourdough products across various retail channels enhances accessibility and market expansion. Additionally, the versatility of sourdough in terms of flavors, textures, and applications enables product innovation and appeals to a wider consumer base. Overall, the projected growth of the sourdough market is driven by evolving consumer preferences, health consciousness, the clean label trend, and the expanding bakery industry. due to which it is preferred by most sourdough manufacturers.

"By type, Type III segment is expected to grow at the highest growth rate during the forecast period."

Type III sourdough offers enhanced complexity and flavor compared to other types, incorporating ingredients like fruits or honey for a distinctive taste experience. As consumers increasingly seek premium and artisanal sourdough products, the Type III segment meets their demand for diverse and indulgent flavors. Additionally, the segment benefits from the growing interest in specialty and niche bakery items, as well as the trend toward natural and clean-label products. With its natural flavorings and ingredients, Type III sourdough appeals to health-conscious consumers. Overall, the Type III segment's growth is fueled by its complexity, premium positioning, appeal to adventurous consumers, and alignment with current market trends.

"By application, the Bread and Buns segment is the largest segment during the forecast period."

Bread and buns are stapled food items consumed worldwide, providing a consistent and high-demand base. The increasing popularity of artisanal and specialty bread aligns with the unique qualities of sourdough, such as its tangy flavor, improved texture, and extended shelf life. The segment's versatility allows for customization and caters to diverse consumer preferences in terms of size, shape, and flavor. The widespread availability of bread and buns through commercial bakeries, retail outlets, and food establishments further contributes to their dominant position. Overall, the bread and buns segment benefits from its universal appeal, increasing consumer interest in artisanal bread, and convenience in accessing these products, leading to its largest market share in the forecast period.

"By Ingredients, the Barley segment is projected to grow at the highest CAGR in the Sourdough markets."

Barley's unique characteristics, such as its high enzyme content, contribute to improved texture and flavor development in sourdough products. The increasing consumer interest in healthier and alternative grains drives the demand for barley-based sourdough products. Barley is known for its nutritional benefits and aligns with the clean label and natural ingredient trends. Its versatility allows for innovation and product differentiation within the market. As health-conscious consumers seek nutritious and wholesome options, the barley segment is expected to experience significant growth. With its recognized and familiar usage, barley appeals to consumers who prioritize transparency and minimally processed ingredients. Overall, the growing demand for barley-based sourdough products and its favorable properties position the barley segment for the highest CAGR in the sourdough market.

"Asia Pacific market is estimated to be the fastest-growing region in the Sourdough market."

Asia Pacific is having a large and rapidly expanding population, coupled with increasing urbanization and disposable incomes, which drive the demand for healthier and diverse food options. The rich culinary heritage and cultural affinity for fermented foods in Asia contribute to the natural market for sourdough products. Additionally, the influence of Western dietary trends and globalization has led to a greater acceptance and demand for artisanal and natural bread, including sourdough. Rising health consciousness among consumers and the potential health benefits associated with sourdough fermentation further fuel the growth. The expanding bakery industry, technological advancements, and investments in research and development also contribute to the rapid growth of the sourdough market in the Asia Pacific region.

Breakdown of Primaries:

In-depth interviews were conducted with various key industry participants, subject-matter experts, C-level executives of key market players, and industry consultants, among other experts, to obtain and verify critical qualitative and quantitative information, as well as to assess future market prospects. The distribution of primary interviews is as follows:

By Company Type: Tier 1- 30%, Tier 2- 45%, Tier 3- 25%

By Designation: CXOs- 25%, Managers- 50%, Executives- 25%

By Region: North America- 25%, Europe- 25%, Asia Pacific- 40%, and RoW - 10%

Key players in this market are Puratos (Belgium), IREKS GMBH (Germany), Lallemand Inc. (Canada), Lesaffre (France), Gold Coast Baking Company (US), and others.

Research Coverage:

This research report categorizes the Sourdough market by Type (Type I, Type II and Type III), by Application (Bread & Buns, Cookies, Cakes, Pizza, and Others), by Ingredients (Wheat, Barley, and Oats), and by Region (North America, Europe, Asia Pacific, South America, and RoW). The report's scope covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the Sourdough market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions, new product launches, mergers & acquisitions, partnerships, agreements, and other recent developments in the Sourdough market. Competitive analysis of coming startups in the Sourdough market is covered in this report.

Reasons to buy this report:

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall Sourdough market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market's pulse and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key driver (Health & wellness consciousness among consumers), restraint (Limites shelf-life and product consistency), opportunity (Innovation and product diversification), and challenges (Quality and consistency control) influencing the growth of the Sourdough market

- Product Development/Innovation: Detailed insights on coming technologies, R&D activities, and product launches in the Sourdough market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the Sourdough market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the Sourdough market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Puratos, IREKS GMBH, Lallemand Inc., and others in the Sourdough market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- 1.3.3 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- TABLE 1 USD EXCHANGE RATES, 2019-2022

- 1.6 UNITS CONSIDERED

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

- 1.8.1 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- 2.1.2.3 Breakdown of primary interviews

- FIGURE 2 BREAKDOWN OF PRIMARY INTERVIEWS: BY VALUE CHAIN, DESIGNATION, AND REGION

- 2.2 FACTOR ANALYSIS

- 2.2.1 INTRODUCTION

- 2.2.2 DEMAND-SIDE ANALYSIS

- FIGURE 3 KEY ECONOMIES BASED ON GROSS DOMESTIC PRODUCT, 2019-2021 (USD TRILLION)

- 2.2.3 SUPPLY-SIDE ANALYSIS

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 APPROACH ONE (BASED ON APPLICATION, BY REGION)

- 2.3.2 APPROACH TWO (BASED ON GLOBAL MARKET)

- 2.4 DATA TRIANGULATION

- FIGURE 4 DATA TRIANGULATION AND MARKET BREAKDOWN

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 LIMITATIONS AND RISK ASSESSMENT

- 2.7 RECESSION IMPACT ANALYSIS

- 2.7.1 RECESSION MACROINDICATORS

- FIGURE 5 RECESSION MACROINDICATORS

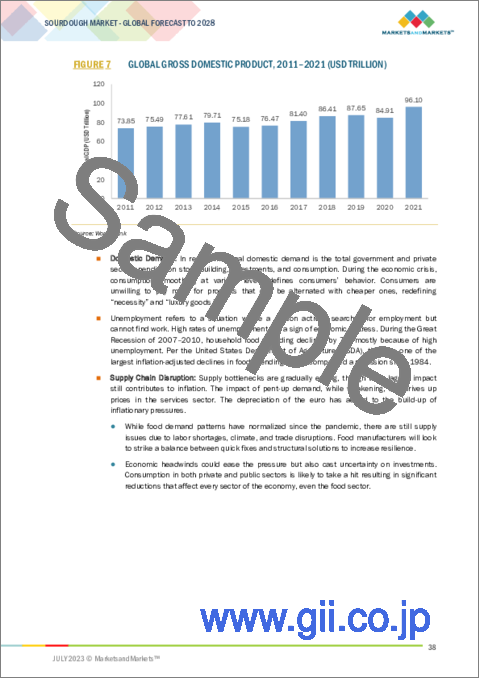

- FIGURE 6 GLOBAL INFLATION RATE, 2011-2021

- FIGURE 7 GLOBAL GROSS DOMESTIC PRODUCT, 2011-2021 (USD TRILLION)

- FIGURE 8 RECESSION INDICATORS AND THEIR IMPACT ON SOURDOUGH MARKET

- FIGURE 9 GLOBAL SOURDOUGH MARKET: CURRENT FORECAST VS. RECESSION FORECAST

3 EXECUTIVE SUMMARY

- TABLE 2 SOURDOUGH MARKET SNAPSHOT, 2023 VS. 2028

- FIGURE 10 SOURDOUGH MARKET, BY TYPE, 2023 VS. 2028 (USD MILLION)

- FIGURE 11 SOURDOUGH MARKET, BY INGREDIENT, 2023 VS. 2028 (USD MILLION)

- FIGURE 12 SOURDOUGH MARKET, BY APPLICATION, 2023 VS. 2028 (USD MILLION)

- FIGURE 13 SOURDOUGH MARKET SHARE AND GROWTH RATE, BY REGION

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SOURDOUGH MARKET

- FIGURE 14 POPULARITY OF ARTISANAL BAKING TRENDS AND RISING HEALTH AWARENESS AMONG CONSUMERS TO DRIVE GROWTH

- 4.2 SOURDOUGH MARKET: SHARE OF MAJOR REGIONAL SUBMARKETS

- FIGURE 15 CHINA TO ACHIEVE FASTEST GROWTH DURING FORECAST PERIOD

- 4.3 EUROPE: SOURDOUGH MARKET, BY TYPE AND KEY COUNTRY

- FIGURE 16 TYPE I SEGMENT AND GERMANY TO ACCOUNT FOR SIGNIFICANT SHARE IN 2023

- 4.4 SOURDOUGH MARKET, BY APPLICATION AND REGION

- FIGURE 17 BREAD & BUNS SEGMENT AND EUROPE TO ACCOUNT FOR SIGNIFICANT SHARE BY 2028

- 4.5 SOURDOUGH MARKET, BY TYPE

- FIGURE 18 TYPE I SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- 4.6 SOURDOUGH MARKET, BY APPLICATION

- FIGURE 19 BREAD & BUNS SEGMENT TO ACCOUNT FOR LARGEST SHARE BY 2028

- 4.7 SOURDOUGH MARKET, BY INGREDIENT

- FIGURE 20 WHEAT SEGMENT TO LEAD MARKET BY 2028

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- FIGURE 21 REVENUE SHARE OF US BAKERY PRODUCTS, 2021

- 5.2 MARKET DYNAMICS

- FIGURE 22 SOURDOUGH MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Rising health awareness among consumers

- 5.2.1.2 Popularity of authentic and artisanal food trends

- 5.2.1.3 Increasing demand for gluten-free products

- 5.2.2 RESTRAINTS

- 5.2.2.1 Limited shelf life and product inconsistency

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Demand for innovation and product diversification

- 5.2.3.2 Culinary exploration and changing taste preferences

- 5.2.4 CHALLENGES

- 5.2.4.1 Rising price sensitivity and market penetration

- 5.2.4.2 Intricate and time-consuming sourdough fermentation

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 VALUE CHAIN ANALYSIS

- FIGURE 23 VALUE CHAIN ANALYSIS

- 6.2.1 RESEARCH AND PRODUCT DEVELOPMENT

- 6.2.2 RAW MATERIAL SOURCING

- 6.2.3 PRODUCTION AND PROCESSING

- 6.2.4 BAKING

- 6.2.5 PACKAGING

- 6.2.6 MARKETING AND SALES

- 6.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 24 REVENUE SHIFT ANALYSIS

- 6.4 TARIFF AND REGULATORY LANDSCAPE

- TABLE 3 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 4 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 5 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 6 SOUTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 7 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.5 REGULATORY FRAMEWORK

- 6.6 NORTH AMERICA

- 6.6.1 US

- 6.6.1.1 Food and Drug Administration (FDA)

- 6.6.1.2 United States Department of Agriculture (USDA)

- 6.6.1.3 State and Local Health Departments

- 6.6.1.4 Occupational Safety and Health Administration (OSHA)

- 6.6.2 CANADA

- 6.6.3 MEXICO

- 6.6.1 US

- 6.7 EUROPEAN UNION (EU)

- 6.7.1 GERMANY

- 6.7.2 FRANCE

- 6.7.3 UK

- 6.7.4 ITALY

- 6.7.5 SPAIN

- 6.8 ASIA PACIFIC

- 6.8.1 CHINA

- 6.8.2 INDIA

- 6.8.3 JAPAN

- 6.8.4 AUSTRALIA & NEW ZEALAND

- 6.9 SOUTH AMERICA

- 6.9.1 BRAZIL

- 6.9.2 ARGENTINA

- 6.10 PATENT ANALYSIS

- FIGURE 25 PATENTS GRANTED GLOBALLY, 2013-2022

- FIGURE 26 MAJOR PATENTS GRANTED, BY REGION

- TABLE 8 LIST OF MAJOR PATENTS PERTAINING TO SOURDOUGH MARKET, 2013-2022

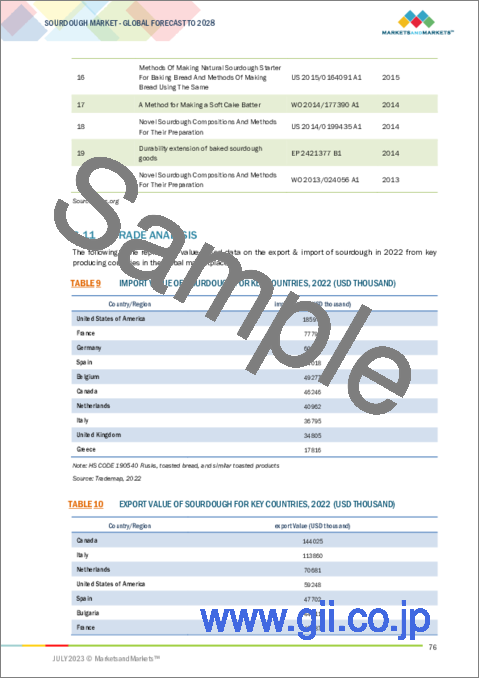

- 6.11 TRADE ANALYSIS

- TABLE 9 IMPORT VALUE OF SOURDOUGH FOR KEY COUNTRIES, 2022 (USD THOUSAND)

- TABLE 10 EXPORT VALUE OF SOURDOUGH FOR KEY COUNTRIES, 2022 (USD THOUSAND)

- 6.12 PRICING ANALYSIS

- 6.12.1 AVERAGE SELLING PRICE TRENDS

- TABLE 11 WHEAT: SOURDOUGH MARKET, BY REGION, 2020-2022 (USD PER TON)

- TABLE 12 BARLEY: SOURDOUGH MARKET, BY REGION, 2020-2022 (KILOTON)

- TABLE 13 OATS: SOURDOUGH MARKET, BY REGION, 2020-2022 (KILOTON)

- 6.13 ECOSYSTEM ANALYSIS

- 6.13.1 DEMAND SIDE

- 6.13.2 SUPPLY SIDE

- FIGURE 27 ECOSYSTEM MAP

- TABLE 14 ROLE OF PLAYERS IN MARKET ECOSYSTEM

- 6.14 TECHNOLOGY ANALYSIS

- 6.14.1 3D BREAD QUALITY X-RAYS

- 6.14.2 DIGITAL HUMIDITY SENSORS

- 6.15 PORTER'S FIVE FORCES ANALYSIS

- TABLE 15 PORTER'S FIVE FORCES ANALYSIS

- 6.15.1 INTENSITY OF COMPETITIVE RIVALRY

- 6.15.2 BARGAINING POWER OF SUPPLIERS

- 6.15.3 BARGAINING POWER OF BUYERS

- 6.15.4 THREAT OF SUBSTITUTES

- 6.15.5 THREAT OF NEW ENTRANTS

- 6.16 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.16.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 28 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR KEY APPLICATIONS

- TABLE 16 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR APPLICATIONS

- 6.16.2 KEY CRITERIA FOR SELECTING SUPPLIERS/VENDORS

- TABLE 17 KEY CRITERIA FOR SELECTING SUPPLIERS/VENDORS

- FIGURE 29 KEY CRITERIA FOR SELECTING SUPPLIERS/VENDORS

- 6.17 KEY CONFERENCES & EVENTS, 2023-2024

- TABLE 18 KEY CONFERENCES & EVENTS, 2023-2024

7 SOURDOUGH MARKET, BY INGREDIENT

- 7.1 INTRODUCTION

- FIGURE 30 SOURDOUGH MARKET, BY INGREDIENT, 2023 VS. 2028 (USD MILLION)

- TABLE 19 SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 20 SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 21 SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 22 SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 7.2 WHEAT

- 7.2.1 HEALTH BENEFITS OFFERED BY WHEAT TO DRIVE DEMAND FOR WHEAT SOURDOUGH

- TABLE 23 WHEAT: SOURDOUGH MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 24 WHEAT: SOURDOUGH MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 25 WHEAT: SOURDOUGH MARKET, BY REGION, 2019-2022 (KT)

- TABLE 26 WHEAT: SOURDOUGH MARKET, BY REGION, 2023-2028 (KT)

- 7.3 BARLEY

- 7.3.1 ABILITY OF BARLEY SOURDOUGH TO RETARD STALING PROCESS AND INHIBIT MOLD GROWTH TO PROPEL DEMAND

- TABLE 27 BARLEY: SOURDOUGH MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 28 BARLEY: SOURDOUGH MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 29 BARLEY: SOURDOUGH MARKET, BY REGION, 2019-2022 (KT)

- TABLE 30 BARLEY: SOURDOUGH MARKET, BY REGION, 2023-2028 (KT)

- 7.4 OATS

- 7.4.1 NUTRITIONAL ADVANTAGES AND EXCEPTIONAL NUTTY TASTE OF OATS SOURDOUGH TO BOOST MARKET

- TABLE 31 OATS: SOURDOUGH MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 32 OATS: SOURDOUGH MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 33 OATS: SOURDOUGH MARKET, BY REGION, 2019-2022 (KT)

- TABLE 34 OATS: SOURDOUGH MARKET, BY REGION, 2023-2028 (KT)

8 SOURDOUGH MARKET, BY TYPE

- 8.1 INTRODUCTION

- FIGURE 31 SOURDOUGH MARKET, BY TYPE, 2023 VS. 2028 (USD MILLION)

- TABLE 35 SOURDOUGH MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 36 SOURDOUGH MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 8.2 TYPE I

- 8.2.1 INCREASING APPLICATION OF TYPE I SOURDOUGH IN ARTISANAL BAKERIES TO DRIVE GROWTH

- TABLE 37 TYPE I: SOURDOUGH MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 38 TYPE I: SOURDOUGH MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.3 TYPE II

- 8.3.1 UNIQUE ORGANOLEPTIC PROPERTIES OF TYPE II SOURDOUGH TO PROPEL MARKET

- TABLE 39 TYPE II: SOURDOUGH MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 40 TYPE II: SOURDOUGH MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.4 TYPE III

- 8.4.1 EXTENDED SHELF-LIFE AND CONVENIENT HANDLING AND STORAGE OF TYPE III SOURDOUGH TO PROPEL GROWTH

- TABLE 41 TYPE III: SOURDOUGH MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 42 TYPE III: SOURDOUGH MARKET, BY REGION, 2023-2028 (USD MILLION)

9 SOURDOUGH MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- FIGURE 32 SOURDOUGH MARKET, BY APPLICATION, 2023 VS. 2028 (USD MILLION)

- TABLE 43 SOURDOUGH MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 44 SOURDOUGH MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 9.2 BREAD & BUNS

- 9.2.1 CONSUMER PREFERENCE FOR CLEAN-LABEL NATURAL FOOD PRODUCTS TO DRIVE DEMAND

- TABLE 45 BREAD & BUNS: SOURDOUGH MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 46 BREAD & BUNS: SOURDOUGH MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.3 COOKIES

- 9.3.1 RISING DEMAND FOR NUTRITIOUS COOKIES TO DRIVE MARKET

- TABLE 47 COOKIES: SOURDOUGH MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 48 COOKIES: SOURDOUGH MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.4 CAKES

- 9.4.1 INCREASED PREFERENCE FOR FLAVORFUL, TENDER CAKES TO PROPEL MARKET

- TABLE 49 CAKES: SOURDOUGH MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 50 CAKES: SOURDOUGH MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.5 PIZZAS

- 9.5.1 DEMAND FOR ARTISANAL AND PREMIUM PIZZA OPTIONS TO DRIVE MARKET EXPANSION

- TABLE 51 PIZZAS: SOURDOUGH MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 52 PIZZAS: SOURDOUGH MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.6 OTHER APPLICATIONS

- TABLE 53 OTHER APPLICATIONS: SOURDOUGH MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 54 OTHER APPLICATIONS: SOURDOUGH MARKET, BY REGION, 2023-2028 (USD MILLION)

10 SOURDOUGH MARKET, BY REGION

- 10.1 INTRODUCTION

- FIGURE 33 NEW HOTSPOTS TO EMERGE IN ASIA PACIFIC SOURDOUGH MARKET DURING FORECAST PERIOD

- TABLE 55 SOURDOUGH MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 56 SOURDOUGH MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 57 SOURDOUGH MARKET, BY REGION, 2019-2022 (KT)

- TABLE 58 SOURDOUGH MARKET, BY REGION, 2023-2028 (KT)

- 10.2 NORTH AMERICA

- FIGURE 34 NORTH AMERICA: SOURDOUGH MARKET SNAPSHOT

- 10.2.1 NORTH AMERICA: RECESSION IMPACT

- FIGURE 35 NORTH AMERICAN SOURDOUGH MARKET: RECESSION IMPACT ANALYSIS

- TABLE 59 NORTH AMERICA: SOURDOUGH MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 60 NORTH AMERICA: SOURDOUGH MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 61 NORTH AMERICA: SOURDOUGH MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 62 NORTH AMERICA: SOURDOUGH MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 63 NORTH AMERICA: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 64 NORTH AMERICA: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 65 NORTH AMERICA: SOURDOUGH MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 66 NORTH AMERICA: SOURDOUGH MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 10.2.2 US

- 10.2.2.1 Expanding bakery sector to encourage market growth

- TABLE 67 US: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 68 US: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 69 US: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 70 US: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.2.3 CANADA

- 10.2.3.1 Increased prevalence of celiac diseases to drive growth

- TABLE 71 CANADA: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 72 CANADA: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 73 CANADA: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 74 CANADA: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.2.4 MEXICO

- 10.2.4.1 Increase in demand for biodegradable plastics in various food packaging applications to drive growth

- TABLE 75 MEXICO: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 76 MEXICO: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 77 MEXICO: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 78 MEXICO: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.3 EUROPE

- 10.3.1 EUROPE: RECESSION IMPACT

- TABLE 79 EUROPE: SOURDOUGH MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 80 EUROPE: SOURDOUGH MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 81 EUROPE: SOURDOUGH MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 82 EUROPE: SOURDOUGH MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 83 EUROPE: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 84 EUROPE: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 85 EUROPE: SOURDOUGH MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 86 EUROPE: SOURDOUGH MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 10.3.2 GERMANY

- 10.3.2.1 Rising consumption of bread to boost market expansion

- TABLE 87 GERMANY: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 88 GERMANY: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 89 GERMANY: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 90 GERMANY: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.3.3 FRANCE

- 10.3.3.1 Rapid growth of bakery sector to offer favorable market opportunities

- TABLE 91 FRANCE: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 92 FRANCE: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 93 FRANCE: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 94 FRANCE: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.3.4 UK

- 10.3.4.1 Growing popularity of ready-to-eat food products to drive demand

- TABLE 95 UK: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 96 UK: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 97 UK: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 98 UK: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.3.5 ITALY

- 10.3.5.1 Increasing number of artisanal bakeries to foster market growth

- TABLE 99 ITALY: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 100 ITALY: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 101 ITALY: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 102 ITALY: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.3.6 SPAIN

- 10.3.6.1 Country's culinary heritage and deeply rooted gastronomic culture to drive preference for sourdough

- TABLE 103 SPAIN: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 104 SPAIN: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 105 SPAIN: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 106 SPAIN: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.3.7 REST OF EUROPE

- TABLE 107 REST OF EUROPE: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 108 REST OF EUROPE: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 109 REST OF EUROPE: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 110 REST OF EUROPE: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.4 ASIA PACIFIC

- 10.4.1 ASIA PACIFIC: RECESSION IMPACT

- TABLE 111 ASIA PACIFIC: SOURDOUGH MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 112 ASIA PACIFIC: SOURDOUGH MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 113 ASIA PACIFIC: SOURDOUGH MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 114 ASIA PACIFIC: SOURDOUGH MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 115 ASIA PACIFIC: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 116 ASIA PACIFIC: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 117 ASIA PACIFIC: SOURDOUGH MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 118 ASIA PACIFIC: SOURDOUGH MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 10.4.2 CHINA

- 10.4.2.1 High demand for convenient food options to drive growth

- TABLE 119 CHINA: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 120 CHINA: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 121 CHINA: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 122 CHINA: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.4.3 INDIA

- 10.4.3.1 Presence of numerous small-scale and industrial bakeries to drive demand

- TABLE 123 INDIA: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 124 INDIA: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 125 INDIA: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 126 INDIA: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.4.4 JAPAN

- 10.4.4.1 Remarkable surge in demand for bread to drive market

- TABLE 127 JAPAN: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 128 JAPAN: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 129 JAPAN: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 130 JAPAN: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.4.5 AUSTRALIA & NEW ZEALAND

- 10.4.5.1 Increase in healthy and sustainable food choices among consumers to drive demand

- TABLE 131 AUSTRALIA & NEW ZEALAND: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 132 AUSTRALIA & NEW ZEALAND: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 133 AUSTRALIA & NEW ZEALAND: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 134 AUSTRALIA & NEW ZEALAND: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.4.6 REST OF ASIA PACIFIC

- TABLE 135 REST OF ASIA PACIFIC: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 136 REST OF ASIA PACIFIC: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 137 REST OF ASIA PACIFIC: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 138 REST OF ASIA PACIFIC: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.5 SOUTH AMERICA

- 10.5.1 SOUTH AMERICA: RECESSION IMPACT

- TABLE 139 SOUTH AMERICA: SOURDOUGH MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 140 SOUTH AMERICA: SOURDOUGH MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 141 SOUTH AMERICA: SOURDOUGH MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 142 SOUTH AMERICA: SOURDOUGH MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 143 SOUTH AMERICA: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 144 SOUTH AMERICA: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 145 SOUTH AMERICA: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 146 SOUTH AMERICA: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- TABLE 147 SOUTH AMERICA: SOURDOUGH MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 148 SOUTH AMERICA: SOURDOUGH MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 10.5.2 BRAZIL

- 10.5.2.1 Growth of bread and bakery market to spur market expansion

- TABLE 149 BRAZIL: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 150 BRAZIL: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 151 BRAZIL: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 152 BRAZIL: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.5.3 ARGENTINA

- 10.5.3.1 Government initiatives to subsidize flour mills to boost demand

- TABLE 153 ARGENTINA: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 154 ARGENTINA: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 155 ARGENTINA: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 156 ARGENTINA: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.5.4 REST OF SOUTH AMERICA

- TABLE 157 REST OF SOUTH AMERICA: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 158 REST OF SOUTH AMERICA: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 159 REST OF SOUTH AMERICA: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 160 REST OF SOUTH AMERICA: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.6 REST OF THE WORLD (ROW)

- 10.6.1 ROW: RECESSION IMPACT

- TABLE 161 ROW: SOURDOUGH MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 162 ROW: SOURDOUGH MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 163 ROW: SOURDOUGH MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 164 ROW: SOURDOUGH MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 165 ROW: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 166 ROW: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 167 ROW: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 168 ROW: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- TABLE 169 ROW: SOURDOUGH MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 170 ROW: SOURDOUGH MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 10.6.2 MIDDLE EAST

- 10.6.2.1 Thriving bakery sector to drive growth

- TABLE 171 MIDDLE EAST: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 172 MIDDLE EAST: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 173 MIDDLE EAST: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 174 MIDDLE EAST: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

- 10.6.3 AFRICA

- 10.6.3.1 Ability of sourdough bread to suit diverse regional tastes and flour preferences to drive growth

- TABLE 175 AFRICA: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (USD MILLION)

- TABLE 176 AFRICA: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (USD MILLION)

- TABLE 177 AFRICA: SOURDOUGH MARKET, BY INGREDIENT, 2019-2022 (KT)

- TABLE 178 AFRICA: SOURDOUGH MARKET, BY INGREDIENT, 2023-2028 (KT)

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 HISTORICAL REVENUE ANALYSIS FOR KEY PLAYERS

- TABLE 179 REVENUE ANALYSIS FOR KEY PLAYERS, 2020-2022 (USD BILLION)

- 11.3 STRATEGIES ADOPTED BY KEY PLAYERS

- TABLE 180 STRATEGIES ADOPTED BY KEY PLAYERS

- 11.4 GLOBAL SNAPSHOT OF KEY MARKET PARTICIPANTS

- FIGURE 36 GLOBAL SNAPSHOT OF KEY PARTICIPANTS, 2022

- 11.5 MARKET SHARE ANALYSIS

- TABLE 181 MARKET SHARE ANALYSIS OF KEY PLAYERS, 2022

- 11.6 COMPANY EVALUATION MATRIX FOR KEY PLAYERS, 2022

- 11.6.1 STARS

- 11.6.2 PERVASIVE PLAYERS

- 11.6.3 EMERGING LEADERS

- 11.6.4 PARTICIPANTS

- FIGURE 37 COMPANY EVALUATION MATRIX FOR KEY PLAYERS, 2022

- 11.6.5 PRODUCT FOOTPRINT FOR KEY PLAYERS

- TABLE 182 SOURDOUGH MARKET: COMPANY FOOTPRINT FOR KEY PLAYERS, BY TYPE

- TABLE 183 SOURDOUGH MARKET: COMPANY FOOTPRINT FOR KEY PLAYERS, BY APPLICATION

- TABLE 184 SOURDOUGH MARKET: COMPANY FOOTPRINT FOR KEY PLAYERS, BY INGREDIENT

- TABLE 185 SOURDOUGH MARKET: COMPANY FOOTPRINT FOR KEY PLAYERS, BY REGION

- TABLE 186 SOURDOUGH MARKET: COMPETITIVE BENCHMARKING OF KEY PLAYERS

- 11.7 COMPANY EVALUATION MATRIX FOR STARTUPS/SMES, 2022

- 11.7.1 PROGRESSIVE COMPANIES

- 11.7.2 STARTING BLOCKS

- 11.7.3 RESPONSIVE COMPANIES

- 11.7.4 DYNAMIC COMPANIES

- FIGURE 38 COMPANY EVALUATION MATRIX FOR STARTUPS/SMES, 2022

- TABLE 187 SOURDOUGH MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMES

- 11.8 COMPETITIVE SCENARIO

- 11.8.1 PRODUCT LAUNCHES

- TABLE 188 SOURDOUGH MARKET: PRODUCT LAUNCHES, 2022

- TABLE 189 SOURDOUGH MARKET: DEALS, 2021

12 COMPANY PROFILES

- (Business overview, Products offered, Recent Developments, MNM view)**

- 12.1 KEY PLAYERS

- 12.1.1 PURATOS

- TABLE 190 PURATOS: BUSINESS OVERVIEW

- TABLE 191 PURATOS: PRODUCTS OFFERED

- TABLE 192 PURATOS: DEALS

- 12.1.2 IREKS GMBH

- TABLE 193 IREKS GMBH: BUSINESS OVERVIEW

- TABLE 194 IREKS GMBH: PRODUCTS OFFERED

- 12.1.3 LALLEMAND INC.

- TABLE 195 LALLEMAND INC.: BUSINESS OVERVIEW

- TABLE 196 LALLEMAND INC.: PRODUCTS OFFERED

- 12.1.4 LESAFFRE

- TABLE 197 LESAFFRE: BUSINESS OVERVIEW

- TABLE 198 LESAFFRE: PRODUCTS OFFERED

- 12.1.5 GOODMILLS

- TABLE 199 GOODMILLS: BUSINESS OVERVIEW

- TABLE 200 GOODMILLS: PRODUCTS OFFERED

- 12.1.6 GOLD COAST BAKING COMPANY

- TABLE 201 GOLD COAST BAKING COMPANY: BUSINESS OVERVIEW

- TABLE 202 GOLD COAST BAKING COMPANY: PRODUCTS OFFERED

- 12.1.7 BOUDIN BAKERY

- TABLE 203 BOUDIN BAKERY: BUSINESS OVERVIEW

- TABLE 204 BOUDIN BAKERY: PRODUCTS OFFERED

- 12.1.8 PHILIBERT SAVOURS

- TABLE 205 PHILIBERT SAVOURS: BUSINESS OVERVIEW

- TABLE 206 PHILIBERT SAVOURS: PRODUCTS OFFERED

- 12.1.9 ERNST BOCKER GMBH & CO. KG

- TABLE 207 ERNST BOCKER GMBH & CO. KG: BUSINESS OVERVIEW

- TABLE 208 ERNST BOCKER GMBH & CO. KG: PRODUCTS OFFERED

- TABLE 209 ERNST BOCKER GMBH & CO. KG: PRODUCT LAUNCHES

- 12.1.10 BAKE WITH BROLITE

- TABLE 210 BAKE WITH BROLITE: BUSINESS OVERVIEW

- TABLE 211 BAKE WITH BROLITE: PRODUCTS OFFERED

- 12.1.11 SEMIFREDDI'S

- TABLE 212 SEMIFREDDI'S: BUSINESS OVERVIEW

- TABLE 213 SEMIFREDDI'S: PRODUCTS OFFERED

- 12.1.12 KING ARTHUR BAKING COMPANY, INC.

- TABLE 214 KING ARTHUR BAKING COMPANY, INC.: BUSINESS OVERVIEW

- TABLE 215 KING ARTHUR BAKING COMPANY, INC.: PRODUCTS OFFERED

- 12.1.13 DR. SUWELACK

- TABLE 216 DR. SUWELACK: BUSINESS OVERVIEW

- TABLE 217 DR. SUWELACK: PRODUCTS OFFERED

- TABLE 218 DR. SUWELACK: PRODUCT LAUNCHES

- 12.1.14 CULTURES FOR HEALTH

- TABLE 219 CULTURES FOR HEALTH: BUSINESS OVERVIEW

- TABLE 220 CULTURES FOR HEALTH: PRODUCTS OFFERED

- 12.1.15 LA BREA BAKERY

- TABLE 221 LA BREA BAKERY: BUSINESS OVERVIEW

- TABLE 222 LA BREA BAKERY: PRODUCTS OFFERED

- *Details on Business overview, Products offered, Recent Developments, MNM view might not be captured in case of unlisted companies.

- 12.2 STARTUPS/SMES

- 12.2.1 ITALMILL

- 12.2.2 POILANE

- 12.2.3 THE ACME BREAD COMPANY

- 12.2.4 THE SOURDOUGH COMPANY

- 12.2.5 THEOBROMA

13 ADJACENT & RELATED MARKETS

- 13.1 INTRODUCTION

- 13.2 LIMITATIONS

- 13.3 STARTER CULTURES MARKET

- 13.3.1 MARKET DEFINITION

- 13.3.2 MARKET OVERVIEW

- 13.3.3 STARTER CULTURES MARKET, BY FORM

- TABLE 223 STARTER CULTURES MARKET, BY FORM, 2017-2021 (USD MILLION)

- TABLE 224 STARTER CULTURES MARKET, BY FORM, 2022-2027 (USD MILLION)

- TABLE 225 STARTER CULTURES MARKET, BY FORM, 2017-2021 (KT)

- TABLE 226 STARTER CULTURES MARKET, BY FORM, 2022-2027 (KT)

- 13.3.4 STARTER CULTURES MARKET, BY REGION

- TABLE 227 STARTER CULTURES MARKET, BY REGION, 2017-2021 (USD MILLION)

- TABLE 228 STARTER CULTURES MARKET, BY REGION, 2022-2027 (USD MILLION)

- 13.4 BAKERY PREMIXES MARKET

- 13.4.1 MARKET DEFINITION

- 13.4.2 MARKET OVERVIEW

- 13.4.3 BAKERY PREMIXES MARKET, BY TYPE

- TABLE 229 BAKERY PREMIXES MARKET, BY TYPE, 2017-2025 (USD THOUSAND)

- TABLE 230 BAKERY PREMIXES MARKET, BY TYPE, 2017-2025 (KT)

- 13.4.4 BAKERY PREMIXES MARKET, BY REGION

- TABLE 231 BAKERY PREMIXES MARKET, BY REGION, 2017-2025 (USD THOUSAND)

- TABLE 232 BAKERY PREMIXES MARKET, BY REGION, 2017-2025 (KT)

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS