|

市場調査レポート

商品コード

1755313

ガス置換包装機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Modified Atmosphere Packaging Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ガス置換包装機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月23日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

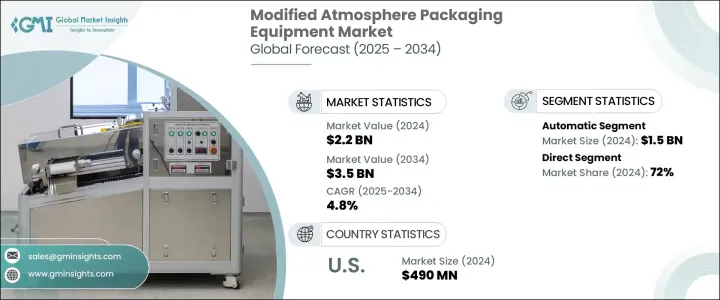

ガス置換包装機器の世界市場は、2024年には22億米ドルと評価され、CAGR 4.8%で成長し、2034年には35億米ドルに達すると推定されています。

この成長を牽引しているのは、賞味期限を延長した食品に対する需要の増加であり、食品廃棄物を最小限に抑える上で重要な役割を果たしています。これらの機械は、包装内の酸素を窒素や二酸化炭素のような不活性ガスに置き換えることで、腐敗を遅らせ、食品の鮮度を長く保つ。この技術は、食品包装産業、特に腐敗しやすい製品カテゴリーで急速に採用されています。

消費者の習慣が都市のライフスタイルとともに進化するにつれて、コンビニエンスフードやレディトゥイートミールへの嗜好が高まっています。調理済み食品やカット済み青果物の消費拡大により、持続可能で長期間鮮度を維持できる包装ソリューションに対する強い需要が生まれています。ガス置換包装機器は、エコフレンドリー材料との互換性を提供し、従来型使い捨てプラスチック包装の削減に貢献することで、このニーズをサポートします。製品の賞味期限延長と環境負荷低減という2つのメリットを持つこの機器は、世界中の食品メーカーや小売業者に好まれる選択肢となりつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 22億米ドル |

| 予測金額 | 35億米ドル |

| CAGR | 4.8% |

2024年、自動ガス置換包装システムは15億米ドルを生み出しました。その人気は、その効率性と食品加工のような大量生産セグメントに不可欠な大規模生産に対応する能力に起因しています。予知保全やリアルタイムのシステムモニタリングなどの先進的機能は、ダウンタイムを減らし生産性を高めることでその魅力を高めています。これらのスマート技術は、バッチ間で一貫した製品品質を維持しながら、メーカーが増大する生産量需要に対応するのに役立っています。

直接販売セグメントは、個別化されたソリューションを提供し、メーカーとエンドユーザー間の1対1のコラボレーションを促進する能力により、2024年に72%のシェアを占めました。ガス置換包装機は、特定の食品に合わせた先進的カスタマイズを必要とすることが多く、直接流通チャネルはこのカスタマイズプロセスをより合理的かつ効果的にします。このような販売戦略は、機器プロバイダとバイヤーの利益となる長期的なパートナーシップの構築にも役立ちます。

米国のガス置換包装機器2024年の市場規模は4億9,000万米ドルで、シェアは76%。多忙なライフスタイルに後押しされたクイックミール需要の高まりが、世界的に消費者の嗜好を形成し続けています。その結果、サステイナブル材料を使用しながら鮮度を長持ちさせる包装の必要性が高まっています。米国では、包装機器の技術革新と自動化が市場をさらに先進させており、性能向上と運用コスト削減のためにスマートシステムを採用する企業が増えています。

世界のガス置換包装機器市場をリードする主要企業には、ULMA Packaging、Webomatic、Proseal、Ross Industries、Robert Reiser、MULTIVAC Group、Ishida、ORICS Industries、GEA Group、Ilapak、Reepack、Henkelman、PFM Group、G. Mondini、Coesia Groupなどがあります。これらの主要参入企業は、技術革新、規模、カスタマイズで競争しています。市場での競合優位性を維持するため、大手メーカーは信頼性を向上させ、操業停止時間を減らすために、先進的自動化とデジタルモニタリング機能を機器に組み込むことに注力しています。カスタマイズ型機械や柔軟な価格設定モデルを通じて、食品加工会社とのパートナーシップを強化しています。さらに、サステイナブル包装材料への研究開発投資は、環境規制や消費者の期待の変化に対応するのに役立っています。直接販売戦略を通じて地理的な足跡を拡大し、アフターセールスサポートを強化することは、長期的な顧客維持と世界的プレゼンスを高めるための一般的なアプローチです。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 産業への影響

- 供給側の影響(原料)

- 主要原料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原料)

- 影響を受ける主要企業

- 戦略的な産業対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 施策関与

- 展望と今後の検討事項

- 貿易への影響

- サプライヤーの情勢

- 主要ニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 賞味期限の延長と食品廃棄物の削減

- インスタント食品とコンビニエンスフードの需要増加

- 持続可能性と規制遵守の圧力

- 産業の潜在的リスク・課題

- 高額な初期資本投資

- ガス混合物の校正とモニタリングの複雑さ

- プラスチック包装廃棄物に関する環境懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推定・予測:製品タイプ別、2021~2034年

- 主要動向

- 真空ベースMAP機器

- トレイシーリングMAP機器

- 水平フローパックMAP機器

- 垂直フローパックMAP機器

- その他(マルチレーンマシン、カスタムMAPシステムなど)

第6章 市場推定・予測:操作別、2021~2034年

- 主要動向

- 自動

- 半自動

第7章 市場推定・予測:包装形態別、2021~2034年

- 主要動向

- トレイのシーリング

- 熱成形

- ポーチ/バッグ

- 硬質容器

第8章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 肉、鶏肉、魚介類

- ベーカリー&菓子類

- 生鮮食品(果物と野菜)

- 乳製品

- レディトゥイート(RTE)食事

- その他

第9章 市場推定・予測:流通チャネル別、2021~2034年

- 主要動向

- 直接

- 間接的

第10章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Coesia Group

- G. Mondini

- GEA Group

- Henkelman

- Ilapak

- Ishida

- MULTIVAC Group

- ORICS Industries

- PFM Group

- Proseal

- Reepack

- Robert Reiser

- Ross Industries

- ULMA Packaging

- Webomatic

The Global Modified Atmosphere Packaging Equipment Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 3.5 billion by 2034. The growth is driven by the increasing demand for food products with extended shelf life, which plays a crucial role in minimizing food waste. These machines replace oxygen inside the packaging with inert gases like nitrogen and carbon dioxide, which slows down spoilage and keeps food fresh longer. This technology is rapidly being adopted in the food packaging industry, particularly in perishable product categories.

As consumer habits evolve with urban lifestyles, there is a rising preference for convenience foods and ready-to-eat meals. The growing consumption of pre-packed meals and precut produce is creating a strong demand for packaging solutions that are both sustainable and capable of maintaining freshness for extended durations. Modified atmosphere packaging equipment supports this need by offering compatibility with eco-friendly materials and helping reduce conventional single-use plastic packaging. With the dual benefit of extending product shelf life and reducing environmental impact, this equipment is becoming a preferred choice for food manufacturers and retailers worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $3.5 Billion |

| CAGR | 4.8% |

In 2024, automatic modified atmosphere packaging systems generated USD 1.5 billion. Their popularity stems from their efficiency and ability to handle large-scale production essential for high-volume sectors like food processing. Advanced features such as predictive maintenance and real-time system monitoring have increased their appeal by reducing downtime and enhancing productivity. These smart technologies help manufacturers meet growing output demands while maintaining consistent product quality across batches.

Direct sales segment accounted for a 72% share in 2024 due to its ability to provide personalized solutions and facilitate one-on-one collaborations between manufacturers and end-users. Modified atmosphere packaging machines often require high degrees of customization, tailored for specific food products, and direct sales channels make this customization process more streamlined and effective. Such sales strategies also help forge long-term partnerships that benefit equipment providers and buyers.

United States Modified Atmosphere Packaging Equipment Market was valued at USD 490 million in 2024, holding a 76% share. The rising demand for quick meals, driven by busy lifestyles, continues to shape consumer preferences globally. As a result, the need for packaging that extends freshness while using sustainable materials is becoming more important. Technological innovations and automation in packaging equipment have further advanced the market in the U.S., where companies are increasingly adopting smart systems to improve performance and reduce operational costs.

Major companies leading the Global Modified Atmosphere Packaging Equipment Market include ULMA Packaging, Webomatic, Proseal, Ross Industries, Robert Reiser, MULTIVAC Group, Ishida, ORICS Industries, GEA Group, Ilapak, Reepack, Henkelman, PFM Group, G. Mondini, and Coesia Group. These key players compete on innovation, scale, and customization. To maintain a competitive edge in the market, leading manufacturers focus on integrating advanced automation and digital monitoring features into their equipment to improve reliability and reduce operational downtimes. They strengthen partnerships with food processing companies through customized machinery and flexible pricing models. Additionally, R&D investment in sustainable packaging materials is helping them align with environmental regulations and shifting consumer expectations. Expanding their geographic footprint through direct sales strategies and enhancing after-sales support is a common approach to boost long-term client retention and global presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations.

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain.

- 3.1.2 Profit margin analysis.

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufactures

- 3.1.6 Distributors

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Shelf-Life Extension & Food Waste Reduction

- 3.6.1.2 Rising Demand for Ready-to-Eat & Convenience Foods

- 3.6.1.3 Sustainability & Regulatory Compliance Pressures

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High Initial Capital Investment

- 3.6.2.2 Complexity in Gas Mixture Calibration & Monitoring

- 3.6.2.3 Environmental Concerns Over Plastic Packaging Waste

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Vacuum-Based MAP Equipment

- 5.3 Tray Sealing MAP Equipment

- 5.4 Horizontal flow pack MAP

- 5.5 Vertical flow pack MAP

- 5.6 Others (multi-lane machines, custom MAP systems, etc.)

Chapter 6 Market Estimates & Forecast, By Operation, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Automated

- 6.3 Semi-automated

Chapter 7 Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Tray sealing

- 7.3 Thermoforming

- 7.4 Pouch/Bag

- 7.5 Rigid container

Chapter 8 Market Estimates & Forecast, By End Use Application, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Meat, poultry, and seafood

- 8.3 Bakery & confectionery

- 8.4 Fresh produce (fruits and vegetables)

- 8.5 Dairy products

- 8.6 Ready-to-Eat (RTE) meals

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Coesia Group

- 11.2 G. Mondini

- 11.3 GEA Group

- 11.4 Henkelman

- 11.5 Ilapak

- 11.6 Ishida

- 11.7 MULTIVAC Group

- 11.8 ORICS Industries

- 11.9 PFM Group

- 11.10 Proseal

- 11.11 Reepack

- 11.12 Robert Reiser

- 11.13 Ross Industries

- 11.14 ULMA Packaging

- 11.15 Webomatic