|

市場調査レポート

商品コード

1708120

金属缶市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Metal Cans Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 金属缶市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月03日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

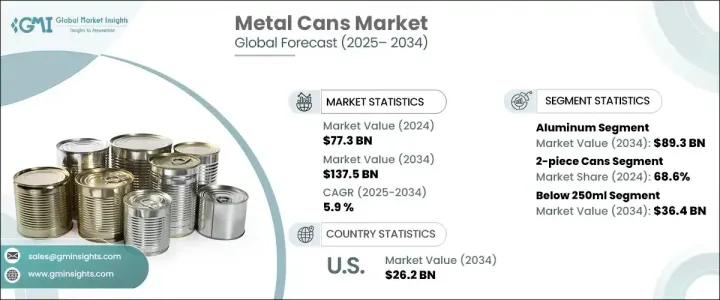

世界の金属缶市場は2024年に773億米ドルに達し、2025年から2034年にかけてCAGR 5.9%で成長すると予測されています。

金属缶の需要増加は、クラフトビールの人気急上昇、eコマースの拡大、持続可能なパッケージング・ソリューションに対する消費者の志向の高まりなど、いくつかの主要な要因によって後押しされています。環境にやさしく、効率的で耐久性のあるパッケージングに対する需要の高まりを受けて、各業界の企業が金属缶への移行を急速に進めています。持続可能性が最優先事項となる中、企業はプラスチック廃棄物の削減に注力しており、金属缶はそのリサイクル性、軽量性、製品保存能力の向上により、魅力的な代替品となっています。

クラフトビール業界は、金属缶の需要を押し上げる上で重要な役割を果たしています。製品の鮮度と品質を効果的に維持できるため、多くの独立系ビール会社がアルミ缶を採用しています。アルミ缶は光と酸素に対する保護に優れているため、飲料の風味を保ち、賞味期限を延ばすことができます。消費者の嗜好が便利で持続可能なパッケージへとシフトし続ける中、金属缶の需要は、特に飲料セクターで加速しています。企業はまた、高品質の印刷と鮮やかなデザインを可能にする金属缶がもたらすブランディングの機会を活用し、棚へのアピールと消費者の関心を高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 773億米ドル |

| 予測金額 | 1,375億米ドル |

| CAGR | 5.9% |

市場は主にアルミとスチールの2つの素材タイプに区分されます。アルミ缶は2034年までに893億米ドルに達すると予想され、その優位性はリサイクル性、軽量特性、環境への影響の低さに起因しています。世界中の政府や環境団体は、プラスチックの使用を抑制するためにより厳しい規制を実施しており、産業界は持続可能な代替手段としてアルミ缶の採用を促しています。また、各ブランドは、アルミ包装に切り替えることで持続可能性へのコミットメントを強調し、環境意識の高い企業としてのイメージを強化するために、協調的な努力を行っています。このシフトは消費者の嗜好によってさらに後押しされており、環境に優しい包装の製品を積極的に求める個人が増えています。

製品タイプ別では、金属缶には2ピースタイプと3ピースタイプがあります。ツーピース・セグメントは2024年に68.6%の市場シェアを占めたが、これは主に費用対効果、耐久性、材料消費量の少なさによるものです。ツーピース缶は、特に炭酸飲料や調理済み食品など、包装の完全性と使いやすさが重要な要素となる飲食品業界で広く好まれています。軽量でリサイクル性の高いパッケージングに対する需要は、今後数年間も2ピース金属缶の採用を促進すると予想されます。

北米の金属缶市場は2024年に25%のシェアを占め、持続可能性への取り組みが同地域の著しい成長を牽引しています。飲料メーカーは、企業の持続可能性目標に沿い、進化する規制基準に準拠するため、アルミ缶への移行を進めています。環境に優しい代替品を求める動きは、環境問題への懸念だけでなく、消費者の期待にも後押しされています。グリーン・パッケージングを推進する政府のプログラムや、プラスチック廃棄物の削減を優先する大手ブランドにより、北米の金属缶市場は着実に拡大する態勢を整えています。企業が革新的なパッケージング・ソリューションとリサイクル・イニシアチブに投資するにつれて、金属缶は様々な産業で持続可能なパッケージングの未来を形作る上で極めて重要な役割を果たすようになります。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- リサイクル効率の向上と循環経済の統合

- クラフトビールの売上増加

- 外出先での飲食品需要の高まり

- eコマース・プラットフォームの世界的拡大

- 缶入りノンアルコール飲料の普及

- 業界の潜在的リスク&課題

- 金属採掘による環境への影響

- 金属包装に対する規制の強化

- 促進要因

- 成長の可能性分析

- 規制状況

- 技術情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- アルミニウム

- スチール

第6章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 2ピース缶

- 3ピース缶

第7章 市場推計・予測:クロージャタイプ別、2021年~2034年

- 主要動向

- イージーオープンエンド(EOE)

- ピールオフエンド(POE)

- その他

第8章 市場推計・予測:容量別、2021年~2034年

- 主要動向

- 250ml未満

- 250ml~1リットル

- 1リットル以上

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 食品

- 果物・野菜

- コンビニエンス食品

- ペットフード

- 肉・魚介類

- その他

- 飲料

- アルコール飲料

- 炭酸飲料

- スポーツドリンク

- その他

- 化粧品・パーソナルケア

- 医薬品

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- Ardagh Group

- Ball Corporation

- Canpack

- CCL Industries

- CPMC Holdings

- Crown Holdings

- DS Containers

- Envases Group

- Hindustan Tin Works

- Kian Joo Group

- Mauser Packaging

- P Wilkinson Containers

- Sapin

- Silgan Holdings

- Toyo Seikan

- Universal Can

- Visy

The Global Metal Cans Market reached USD 77.3 billion in 2024 and is projected to grow at a CAGR of 5.9% between 2025 and 2034. The increasing demand for metal cans is being fueled by several key factors, including the surging popularity of craft beer, the expansion of e-commerce, and a growing consumer inclination toward sustainable packaging solutions. Companies across industries are rapidly shifting to metal cans to meet the rising demand for eco-friendly, efficient, and durable packaging. With sustainability becoming a top priority, businesses are focusing on reducing plastic waste, making metal cans an attractive alternative due to their recyclability, lightweight nature, and enhanced product preservation capabilities.

The craft beer industry is playing a crucial role in boosting the demand for metal cans. Many independent breweries are embracing aluminum cans because they effectively maintain product freshness and quality. Aluminum cans offer superior protection against light and oxygen, which helps retain the flavor and extend the shelf life of beverages. As consumer preferences continue to shift toward convenient and sustainable packaging, the demand for metal cans is accelerating, particularly within the beverage sector. Companies are also capitalizing on the branding opportunities presented by metal cans, which allow for high-quality printing and vibrant designs, enhancing shelf appeal and consumer engagement.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $77.3 Billion |

| Forecast Value | $137.5 Billion |

| CAGR | 5.9% |

The market is primarily segmented into two material types: aluminum and steel. Aluminum cans are expected to reach USD 89.3 billion by 2034, with their dominance attributed to their recyclability, lightweight properties, and low environmental impact. Governments and environmental organizations worldwide are enforcing stricter regulations to curb plastic usage, prompting industries to adopt aluminum cans as a sustainable alternative. Brands are also making concerted efforts to highlight their sustainability commitments by switching to aluminum packaging, reinforcing their image as eco-conscious enterprises. This shift is further supported by consumer preferences, as a growing number of individuals actively seek out products with environmentally friendly packaging.

In terms of product type, metal cans are available in two-piece and three-piece formats. The two-piece segment held a 68.6% market share in 2024, largely due to its cost-effectiveness, durability, and lower material consumption. Two-piece cans are widely preferred in the food and beverage industry, especially for carbonated drinks and ready-to-eat meals, where packaging integrity and ease of use are critical factors. The demand for lightweight and highly recyclable packaging is expected to continue driving the adoption of two-piece metal cans in the coming years.

North America Metal Cans Market held a 25% share in 2024, with sustainability initiatives driving significant growth in the region. Beverage companies are increasingly transitioning to aluminum cans to align with their corporate sustainability goals and comply with evolving regulatory standards. The push for eco-friendly alternatives is not only being driven by environmental concerns but also by consumer expectations. With government programs promoting green packaging and leading brands prioritizing the reduction of plastic waste, the metal cans market in North America is poised for steady expansion. As businesses invest in innovative packaging solutions and recycling initiatives, metal cans are set to play a pivotal role in shaping the future of sustainable packaging across various industries.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Enhanced recycling efficiency and circular economy integration

- 3.2.1.2 Increasing sales of craft beer

- 3.2.1.3 Rising demand for on-the-go food and beverages

- 3.2.1.4 Global expansion of e-commerce platforms

- 3.2.1.5 Proliferation of non-alcoholic beverages in cans

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Environmental impact of mining for metal

- 3.2.2.2 Increased regulatory scrutiny on metal packaging

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 - 2034 (USD Bn & Units)

- 5.1 Key trends

- 5.2 Aluminum

- 5.3 Steel

Chapter 6 Market Estimates and Forecast, By Product, 2021 - 2034 (USD Bn & Units)

- 6.1 Key trends

- 6.2 2-piece cans

- 6.3 3-piece cans

Chapter 7 Market Estimates and Forecast, By Closure Type, 2021 - 2034 (USD Bn & Units)

- 7.1 Key trends

- 7.2 Easy-open end (EOE)

- 7.3 Peel-off end (POE)

- 7.4 Others

Chapter 8 Market Estimates and Forecast, By Capacity, 2021 - 2034 (USD Bn & Units)

- 8.1 Key trends

- 8.2 Below 250ml

- 8.3 250ml - 1 liter

- 8.4 Above 1 liter

Chapter 9 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Bn & Units)

- 9.1 Key trends

- 9.2 Food

- 9.2.1 Fruits & vegetables

- 9.2.2 Convenience foods

- 9.2.3 Pet foods

- 9.2.4 Meat & seafood

- 9.2.5 Others

- 9.3 Beverages

- 9.3.1 Alcoholic beverages

- 9.3.2 Carbonated soft drinks

- 9.3.3 Sports & energy drinks

- 9.3.4 Others

- 9.5 Cosmetics and personal care

- 9.6 Pharmaceuticals

- 9.7 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Bn & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Ardagh Group

- 11.2 Ball Corporation

- 11.3 Canpack

- 11.4 CCL Industries

- 11.5 CPMC Holdings

- 11.6 Crown Holdings

- 11.7 DS Containers

- 11.8 Envases Group

- 11.9 Hindustan Tin Works

- 11.10 Kian Joo Group

- 11.11 Mauser Packaging

- 11.12 P Wilkinson Containers

- 11.13 Sapin

- 11.14 Silgan Holdings

- 11.15 Toyo Seikan

- 11.16 Universal Can

- 11.17 Visy