|

市場調査レポート

商品コード

1913404

サードパーティ・ロジスティクスの市場機会、成長要因、業界動向分析、および2026年から2035年までの予測Third-Party Logistics (3PL) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| サードパーティ・ロジスティクスの市場機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月19日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

概要

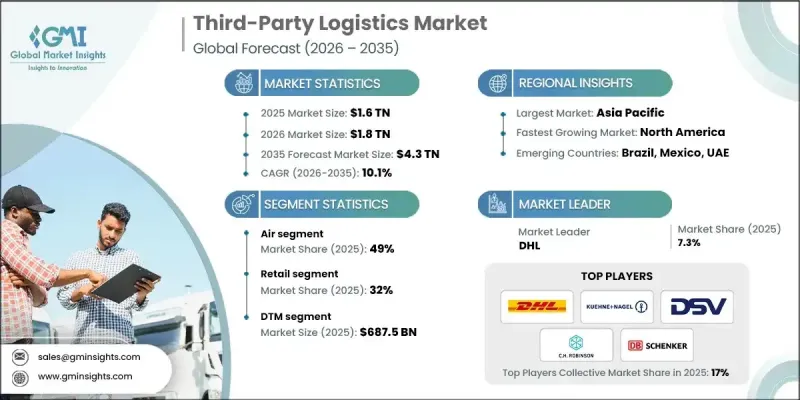

世界のサードパーティ・ロジスティクス(3PL)市場は、2025年に1兆6,000億米ドルと評価され、2035年までにCAGR 10.1%で成長し、4兆3,000億米ドルに達すると予測されています。

この市場の成長は、電子商取引の急速な拡大、サプライチェーンの世界の化の進展、顧客による迅速な配送への需要の高まり、そして物流・流通ネットワークの複雑化によって推進されています。企業はコスト効率、業務の柔軟性、リアルタイム可視性、拡張性のあるサプライチェーン運営を実現するため、専門の3PLプロバイダーへの物流機能のアウトソーシングを増加させています。クラウドベースの輸送管理システム(TMS)、倉庫管理システム(WMS)、AI・機械学習を活用した経路最適化、IoT対応の貨物追跡、ロボティクス、倉庫自動化、高度なデータ分析といった技術革新が、従来の物流を変革しています。これらのソリューションは在庫精度を高め、輸送を最適化し、輸送時間を短縮し、需要予測を改善します。オムニチャネル小売、越境貿易、ラストマイル配送ソリューションの導入拡大は、統合的で柔軟性があり、技術主導型の3PLサービスに対する世界の需要をさらに加速させています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 1兆6,000億米ドル |

| 予測金額 | 4兆3,000億米ドル |

| CAGR | 10.1% |

航空貨物セグメントは2025年に49%のシェアを占め、2026年から2035年にかけてCAGR11.2%で成長すると予測されています。航空物流は、時間厳守・高価値・緊急輸送を実現する上で不可欠な役割を担っているため、主導的な地位を占めています。迅速な配送を必要とする業界からの強い需要により、国境を越えた配送、ジャストインタイム在庫管理、プレミアム物流ニーズにおける航空貨物の採用が増加しています。高度な貨物取り扱い、リアルタイム追跡、優先配送、統合されたエクスプレスネットワークにより、速度、信頼性、サービス品質が確保され、航空輸送は緊急かつ高価値の貨物にとって最適なソリューションとしての地位を確立しています。

国内輸送管理(DTM)セグメントは2025年に6,875億米ドルに達しました。DTMソリューションは、高頻度・時間厳守・コスト効率を要する国内輸送において極めて重要です。最適化されたルート計画、運送業者選定、貨物追跡、ラストマイル配送管理を提供します。この機能性は、EC、小売、FMCG、製造業のサプライチェーンにおいて、迅速なフルフィルメント、ジャストインタイム配送、拡張可能なオペレーションを実現する上で不可欠です。効率性と信頼性を求める荷主と物流サービスプロバイダー双方にとって、DTMは引き続き重点領域です。

中国のサードパーティ・ロジスティクス(3PL)市場は2025年に3,749億米ドルを生み出し、57%のシェアを占めました。同地域の成長は、電子商取引の拡大、高い製造業生産量、技術主導型物流ソリューションの普及拡大によって牽引されています。AIベースのルート最適化、クラウドベースのTMS/WMS、リアルタイム追跡、自動化フルフィルメントシステムへの投資が、同地域の物流能力を加速させています。先進的なインフラ、膨大な貨物量、進化する規制基準が、アジア太平洋地域の世界の第三者物流(3PL)市場における地位をさらに強化しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 電子商取引(Eコマース)とオムニチャネル小売の急速な成長

- サプライチェーンの複雑化と世界の貿易の進展

- 技術導入とデジタルトランスフォーメーション

- コスト最適化と資産軽量型ビジネスモデル

- 業界の潜在的リスク&課題

- 上昇する運営費と人件費

- 規制・コンプライアンスの複雑性

- 市場機会

- ラストマイル配送及び付加価値物流サービス

- デジタル・持続可能な物流ソリューション

- AI、機械学習、IoT技術の採用状況

- 持続可能性とグリーン物流サービス

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 米国運輸省(DOT)及び連邦自動車運送安全局(FMCSA)の規制

- EPA排出基準

- カナダ運輸省基準

- 欧州

- ドイツTUVおよびBaFin準拠

- フランスDGCCRF及びCNITガイドライン

- 英国DVSAおよびFCA規制

- イタリア運輸省適合性

- アジア太平洋地域

- 中国工業情報化部(MIIT)ガイドライン

- 日本金融庁自動車コンプライアンス

- 韓国国土交通省(MOT)及び金融委員会(FSC)の規制

- インドBIS(インド規格協会)及び自動車研究協会ガイドライン

- ラテンアメリカ

- ブラジルANTT及びDENATRAN規制

- メキシコ環境天然資源省(SEMARNAT)及び通信運輸省(SCT)ガイドライン

- 中東・アフリカ

- アラブ首長国連邦道路交通局ガイドライン

- サウジアラビア運輸総局(GAT)の規制

- 北米

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 自動化とロボティクス

- 人工知能(AI)と機械学習

- モノのインターネット(IoT)

- クラウドベースのサプライチェーンプラットフォーム

- 新興技術

- ハイパーコネクテッド・サプライチェーン

- ロボティクス・アズ・ア・サービス(RAAS)

- AIを活用した動的価格設定と容量管理

- 拡張現実(AR)とウェアラブルデバイス

- 現在の技術動向

- 価格動向

- 地域別

- 製品別

- コスト内訳分析

- 特許分析

- 持続可能性と環境的側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- 使用事例シナリオ

- 地域別インフラと展開動向

- 輸送・物流インフラの評価

- デジタル・接続性への対応状況

- 港湾、鉄道及び複合輸送の容量動向

- スマート物流ハブ及びフリーゾーン

- 需要と供給側の評価

- 供給側分析

- プロバイダーのキャパシティ、インフラストラクチャー、および能力

- 技術導入と運用効率

- コスト構造と収益性

- 需要側分析

- エンドユーザー産業の要件

- 数量、頻度、およびサービスレベルの期待値

- 価格感応度と導入動向

- 供給側分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:ソリューション別、2022-2035

- 専用契約輸送(DCC)

- 専用輸送管理(DTM)

- 国際輸送管理(ITM)

- 倉庫保管・流通

- 物流ソフトウェア

第6章 市場推計・予測:モード別、2022-2035

- 航空

- 海上輸送

- 鉄道および道路

第7章 市場推計・予測:用途別、2022-2035

- 食品・飲料

- ヘルスケア

- 小売り

- 自動車

- 製造業

- 電子商取引および物流

- 化学品・石油化学製品

- 医薬品

- その他

第8章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ベルギー

- オランダ

- スウェーデン

- スイス

- オーストリア

- ノルウェー

- デンマーク

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- シンガポール

- 韓国

- ベトナム

- インドネシア

- マレーシア

- タイ

- フィリピン

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- チリ

- コロンビア

- ペルー

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- イスラエル

- カタール

第9章 企業プロファイル

- Global Player

- C.H. Robinson Worldwide

- Ceva Logistics

- DB Schenker Logistics

- DHL Supply Chain &Global Forwarding

- DSV A/S

- Expeditors International of Washington

- FedEx Supply Chain

- Kuehne+Nagel International AG

- Nippon Express

- XPO Logistics

- Regional Player

- Agility Logistics

- APL Logistics

- Bollore Logistics

- Geodis

- Hellmann Worldwide Logistics

- Hitachi Transport System

- Kerry Logistics

- Panalpina

- Toll Group

- Yusen Logistics

- 新興企業

- eBike Diagnostic Solutions

- MotoTech Diagnostics

- NeoMotor Diagnostics

- RideScan Electronics

- SmartMoto Diagnostics