|

市場調査レポート

商品コード

1636137

中国のサードパーティロジスティクス(3PL)-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)China Third-Party Logistics (3PL) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国のサードパーティロジスティクス(3PL)-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

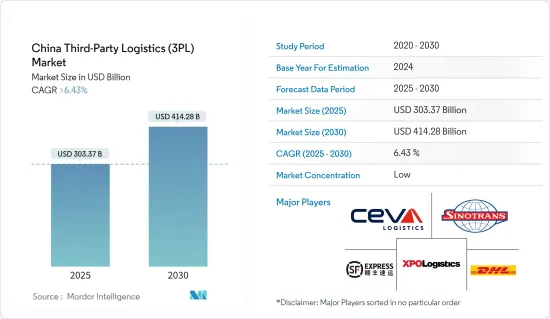

中国のサードパーティロジスティクス市場規模は2025年に3,033億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.43%を超え、2030年には4,142億8,000万米ドルに達すると予測されます。

主要ハイライト

- 中国のサードパーティロジスティクス市場は、主にeコマース活動の増加と可処分所得の増加によって牽引されています。

- 中国のeコマース市場は国の経済情勢を再構築しています。デジタル経済は、中国のGDPを押し上げる上でますます重要になってきています。2023年には、オンライン購入が中国の消費財販売の4分の1以上を占め、世界平均を上回ります。さらに、労働人口が豊富なeコマースは、中国の主要な雇用エンジンとして際立っています。

- 2024年上半期、中国のeコマース部門は著しい成長を遂げ、世界第2位の経済大国である中国の消費回復の勢いを強めました。この期間、オンライン小売売上高は前年同期比9.8%増の7兆1,000億元(約9,960億米ドル)に達しました。商務部(MOC)が発表したデータによると、このうち商品の小売売上高は5兆9,600億元で、8.8%の伸びを示しました。

- 中国のeコマース大手であるAlibabaとJD.comは、2024年の「ダブル11」ショッピング・フェスティバル期間中の売上が好調であったと報告し、中国の消費市場が着実に回復していることを強調しました。

- Alibaba GroupのプラットフォームであるタオバオとTmallは、「ダブル11」イベント期間中に顕著な売上急増を発表しました。合計589のブランドが1億人民元の売上を突破し、2023年から46.5%増加しました。同社は、消費者の関与が2024年に前例のないピークに達したことを強調しました。

- 北京を拠点とするJD.comは、ライブストリーミングの売上が急増し、2023年から3.8倍の伸びを記録したことを明らかにしました。1万7,000以上のブランドが5倍を超える売上の伸びを記録しました。タオバオとTmallの成長は様々なセグメントに及んでおり、特に民生用電子機器や装飾品で顕著でした。この勢いにより、139以上のブランドが売上高1億元の節目を突破し、9,600のブランドが2023年から売上高が倍増しました。したがって、eコマースの売上が急増するにつれて、国内の3PLロジスティクスの需要も連動して高まっています。

中国のサードパーティロジスティクス(3PL)市場動向

付加価値の高い倉庫業と流通業が大きく成長

- 中国がインダストリー4.0時代を迎える中、製造業は依然としてロジスティクス成長の重要な起爆剤となっています。ハイテクメーカーの急増により、グレードA倉庫の需要が顕著に増加しています。

- この傾向を浮き彫りにしているのは、太陽電池の生産が54.2%という著しい成長率を示していること、新エネルギー自動車(NEV)が30.4%も急増していることです。中国乗用車協会(CPCA)によると、中国におけるNEVの普及率は2023年に36.2%に達し、多くのブランドが生産拠点の設立や拡大に乗り出しています。

- リースの動向は地域によって異なる:中国南部の軽工業企業は、倉庫業務の柔軟性を重視しています。低炭素経済へのシフトをリードする中国東部では、LEED認証を誇る環境に優しい倉庫が続々と誕生しています。一方、中国西部ではNEVの急成長が倉庫賃貸の安定した需要を後押ししています。

- 2023年には、31の主要都市で非保税のグレードA倉庫のストックが9,000万m2を超えました。中国東部が圧倒的な存在感を示し、国内総ストックの3分の1以上を占めています。ここ数年、一貫して供給が増加しているため、一部の開発者は空室率の上昇を緩和するために賃貸料のトレードオフに頼った。

- 中国北部、特に廊坊、天津、北京などの都市では、2021年から新規供給が急増しました。逆に、中国西部は2020年以降徐々に減速し、空室ストックを吸収できるようになりました。

- 中国南部は、特に広州と東莞において、越境eコマースによる旺盛な需要に後押しされ、供給の頂点に達しました。一方、中国中部は、輸送と消費のために安定した需要を維持しながらも、過去3年間の供給流入による空室圧力に悩まされています。これは、産業全体で倉庫スペースに対する需要が顕著であることを裏付けています。

eコマースの急増が市場を牽引

- 中国のeコマース市場は、中国経済にとって変革の時代を迎えました。今日、デジタル経済は中国のGDPを押し上げる上でますます重要な役割を果たしています。2023年には、中国の消費財の4分の1以上がオンラインで購入され、世界平均を大幅に上回ります。さらに、eコマースはその膨大な労働力のおかげで、中国の雇用の重要な原動力となっています。

- 過去10年間、中国はeコマースの牽引役となり、売上高で米国を4,860億米ドル以上引き離しています。現在、中国は世界最大のデジタルバイヤー人口を誇っています。近年、ライブストリーミングや迅速な配送といった機能が中国のeコマース領域に統合され、顧客体験がさらに豊かになっています。

- 急速なデジタル化が生活のあらゆる面に浸透する中、オンラインに移行する中国企業の数も増えています。巨大な製造業と政府の後押しを受け、中国は世界最大のB2B eコマース市場を誇っています。しかし、オンライン小売セクターが繁栄する一方で、B2B eコマースの成長は最近減速しています。国境を越えた取引は、中国のB2Bの重要なセグメントとして浮上しており、主に輸出に傾いています。

- 世界最大級のeリテーラーの本拠地である中国では、eコマース売上が一貫して伸びています。インターネットの急速な普及により、オンラインショッピングの普及率は80%を超えています。モバイル機器の利用が急増し、スマートフォンやタブレット端末を使ったショッピングが一般的になっています。パンデミックによる社会的規制や閉鎖は、クイックコマース、オンラインフードデリバリー、コミュニティグループ購入など、オンラインツーオフラインベンチャーの台頭を加速させました。AIの進歩はeリテールを再形成し、オペレーションと顧客対応を最適化しています。さらに、拡張現実(AR)や仮想現実(VR)技術の採用は、ショッピング体験を豊かにし、顧客満足度の向上と売上増につながっています。

中国のサードパーティロジスティクス(3PL)産業概要

中国のサードパーティロジスティクス(3PL)市場は、多くの地元、地域、世界の参入企業によって高度にセグメント化されています。主要参入企業には、Ceva Logistics、Sinotrans、DHL Supply Chain、XPO Logistics、SF Expresなどがあります。

企業は巨大な可能性を利用するために、より競合を高めています。その結果、国際企業は新しい物流センターやスマート倉庫など、地域物流ネットワークを構築するための戦略的投資を行っています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析方法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場力学

- 市場促進要因

- 衣料品とアクセサリーのオンライン販売に対する旺盛な需要

- FMCG製品の需要が市場を牽引

- 市場抑制要因/課題

- 市場に影響を与える規制上の課題

- 労働力不足とコスト上昇が市場に影響

- 市場機会

- 市場を牽引する技術の進歩

- 市場促進要因

- バリューチェーン/サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 政府の規制と施策

- 倉庫市場の一般的動向

- CEP、ラストワンマイルデリバリー、コールドチェーンロジスティクスなど他のセグメントからの需要

- 電子商取引ビジネスに関する洞察

- ロジスティクスセグメントにおける技術開発

- 地政学とパンデミックが市場に与える影響

第5章 市場セグメンテーション

- サービス別

- 国内輸送管理

- 国際輸送管理

- 付加価値型倉庫・配送

- エンドユーザー別

- 航空宇宙

- 自動車

- 消費財・小売、エネルギー

- 医療

- 製造業

- 技術

- その他

第6章 競合情勢

- 市場集中概要

- 企業プロファイル

- Ceva Logistics

- Sinotrans

- DHL Supply Chain

- XPO Logistics

- SF Express

- XPO Logistics

- YTO Express

- ZTO Express

- JD Logistics

- Kerry Logistics*

- その他の企業

第7章 市場の将来

第8章 付録

- マクロ経済指標(GDP分布、活動別、運輸・倉庫部門の経済への寄与度)

- 対外貿易統計-輸出と輸入(製品別)

- 主要輸出先と輸入原産国に関する洞察

The China Third-Party Logistics Market size is estimated at USD 303.37 billion in 2025, and is expected to reach USD 414.28 billion by 2030, at a CAGR of greater than 6.43% during the forecast period (2025-2030).

Key Highlights

- The Chinese third-party logistics market is mainly driven by the rise in e-commerce activities and rising disposable income.

- China's e-commerce market is reshaping the nation's economic landscape. The digital economy is becoming ever more crucial in propelling China's GDP. In 2023, online purchases accounted for more than a quarter of China's consumer goods sales, outpacing the global average. Additionally, with its extensive workforce, e-commerce stands out as a major employment engine in the country.

- In the first half of 2024, China's e-commerce sector experienced significant growth, bolstering the momentum for consumption recovery in the world's second-largest economy. During this period, online retail sales jumped 9.8 percent year-on-year, totaling 7.1 trillion yuan (approximately USD 996 billion). Of this, retail sales of goods accounted for CNY 5.96 trillion, reflecting an 8.8 percent increase, as per data released by the Ministry of Commerce (MOC).

- Chinese e-commerce giants Alibaba and JD.com reported robust sales during the 2024 "Double 11" shopping festival, underscoring the steady recovery of China's consumer market.

- Alibaba Group's platforms, Taobao and Tmall, announced a notable surge in sales during the 'Double 11' event. A total of 589 brands surpassed the CNY 100 million sales mark, marking a 46.5 percent uptick from 2023. The company highlighted that consumer engagement reached an unprecedented peak in 2024.

- Beijing-based JD.com revealed that its live-streaming sales had skyrocketed, boasting a 3.8-fold increase from 2023. Over 17,000 brands celebrated sales growth exceeding five times. Taobao and Tmall's growth spanned various sectors, notably in home appliances and decoration. This momentum propelled over 139 brands past the 100-million-yuan sales milestone, with 9,600 brands experiencing a sales doubling from 2023. Hence, as e-commerce sales surge rapidly, the demand for 3PL logistics in the country is rising in tandem.

China Third-Party Logistics (3PL) Market Trends

Value-added warehousing and distribution experiencing substantial growth

- As China embraces the Industry 4.0 era, its manufacturing sector remains a key catalyst for logistics growth. The surge of high-tech manufacturers is driving a notable uptick in demand for Grade A warehouses.

- Highlighting this trend, solar cell production has seen a remarkable growth rate of 54.2%, while New Energy Vehicles (NEVs) have surged by 30.4%. According to the China Passenger Car Association (CPCA), NEV penetration in China hit 36.2% in 2023, leading many brands to either set up or expand their manufacturing bases.

- Leasing trends differ across regions: Southern China's light manufacturing firms are emphasizing flexibility in their warehouse operations. In Eastern China, a leader in the nation's shift towards a low-carbon economy, a flurry of eco-friendly warehouses boasting LEED certifications are springing up. On the other hand, Western China's rapid NEV growth is bolstering a steady demand for warehouse leases.

- In 2023, the stock of non-bonded Grade A warehouses in 31 major cities exceeded 90 million sqm. Eastern China emerged as a dominant player, representing over a third of the nation's total stock. As supply consistently flowed in recent years, some developers resorted to rental trade-offs to mitigate rising vacancy rates.

- Northern China, especially in cities like Langfang, Tianjin, and Beijing, saw a surge in new supply beginning in 2021. Conversely, Western China has been gradually slowing down since 2020, allowing it to absorb its vacant stock.

- Southern China reached a supply zenith, particularly in Guangzhou and Dongguan, spurred by strong demand from cross-border e-commerce. Meanwhile, Central China maintained steady demand for transportation and consumption, yet still grappled with vacancy pressures due to the influx of supply over the last three years. This underscores a pronounced demand for warehousing spaces across the industry.

Surge in e-commerce activities driving the market

- China's e-commerce market has ushered in a transformative era for the nation's economy. Today, the digital economy plays an increasingly pivotal role in bolstering China's GDP. In 2023, over a quarter of China's consumer goods were purchased online, significantly surpassing the global average. Moreover, e-commerce is a key driver of employment in the country, thanks to its vast workforce.

- For the past decade, China has led the e-commerce charge, outstripping the U.S. by over USD 486 billion in revenue. Currently, China boasts the world's largest population of digital buyers. Recent years have seen the integration of features like live streaming and swift delivery into China's e-commerce realm, further enriching the customer experience.

- With the rapid digitalization permeating every facet of life, a growing number of Chinese businesses are transitioning online. Bolstered by its vast manufacturing sector and governmental backing, China proudly hosts the globe's largest B2B e-commerce market. Yet, while the online retail sector flourishes, B2B e-commerce growth has recently decelerated. Cross-border transactions have emerged as a vital segment of China's B2B landscape, predominantly leaning towards exports, with the U.S. standing out as the primary destination for Chinese B2B goods.

- China, home to some of the world's largest e-retailers, has seen consistent growth in e-commerce sales. Rapid internet adoption has propelled online shopping penetration to over 80%. With the surge in mobile device usage, shopping via smartphones and tablets has become commonplace. The pandemic-induced social restrictions and lockdowns accelerated the rise of online-to-offline ventures, including quick commerce, online food delivery, and community group-buying. AI advancements are reshaping e-retail, optimizing operations and customer interactions. Furthermore, the adoption of augmented reality (AR) and virtual reality (VR) technologies is enriching shopping experiences, leading to heightened customer satisfaction and boosted sales.

China Third-Party Logistics (3PL) Industry Overview

The China third-party logistics (3PL) market is highly fragmented with a lot of local, regional, and global players. Some of the major players include Ceva Logistics, Sinotrans, DHL Supply Chain, XPO Logistics, SF Expres etc.

Companies are getting more competitive to capitalize on the enormous possibility. As a result, international firms are making strategic investments to build a regional logistics network, such as new distribution centers, smart warehouses, and so on.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Method

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS & DYNAMICS

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 Robust demand for online clothing and accessories

- 4.2.1.2 Demand for FMCG products driving the market

- 4.2.2 Market Restraints/challenges

- 4.2.2.1 Regulatory challenges affecting the market

- 4.2.2.2 Labour shortages and rising costs affecting the market

- 4.2.3 Market Opportunities

- 4.2.3.1 Technological advancements driving the market

- 4.2.1 Market Drivers

- 4.3 Value Chain / Supply Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Government Policies and Regulations

- 4.6 General Trends in Warehousing Market

- 4.7 Demand From Other Segments, such as CEP, Last Mile Delivery, Cold Chain Logistics Etc.

- 4.8 Insights on Ecommerce Business

- 4.9 Technological Developments in the Logistics Sector

- 4.10 Impact of Geopolitics and Pandemics on the Market

5 MARKET SEGMENTATION

- 5.1 By Services

- 5.1.1 Domestic Transportation Management

- 5.1.2 International Transportation Management

- 5.1.3 Value-added Warehousing and Distribution

- 5.2 By End User

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Consumer and Retail, Energy

- 5.2.4 Healthcare

- 5.2.5 Manufacturing

- 5.2.6 Technology

- 5.2.7 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Ceva Logistics

- 6.2.2 Sinotrans

- 6.2.3 DHL Supply Chain

- 6.2.4 XPO Logistics

- 6.2.5 SF Express

- 6.2.6 XPO Logistics

- 6.2.7 YTO Express

- 6.2.8 ZTO Express

- 6.2.9 JD Logistics

- 6.2.10 Kerry Logistics*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, by Activity, Contribution of Transport and Storage Sector to economy)

- 8.2 External Trade Statistics - Exports and Imports, by Product

- 8.3 Insights into Key Export Destinations and Import Origin Countries