大型トラックの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Heavy Duty Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日

- 商品コード

- 1666580

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

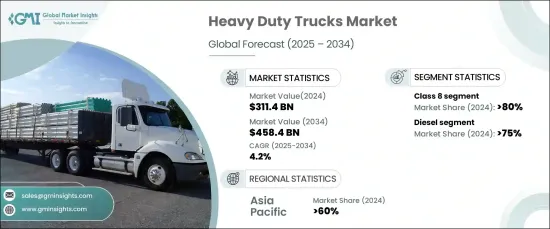

世界の大型トラック市場は2024年に3,114億米ドルとなり、2025年から2034年にかけてCAGR4.2%で成長すると予測されています。

この成長は、商業の繁栄と貿易活動の拡大により、効率的な物資輸送に対する世界のニーズが高まっていることが主な要因です。国境を越えた貿易は勢いを増しており、長距離で大量の貨物を処理できる高度な大型車両が必要とされています。貿易ロジスティクスを合理化し、インフラを改善するための地域間の協力的な取り組みが、大型トラック、特にクラス8車両の採用を強化しています。

技術革新は市場情勢を再構築し、車両性能、安全性、運転効率を向上させています。自律走行、テレマティックス、コネクティビティソリューションのような先進機能は、大型トラックにますます統合され、フリートオペレーターにとってより魅力的なものとなっています。これらのテクノロジーは、フリート管理を最適化し、ドライバーの安全性を向上させ、運転コストを削減し、近代化されたトラックモデルへの需要を促進しています。フリートオペレーターが性能とコスト効率を優先しているため、技術的に先進的な大型トラックの採用が世界的に増加しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 3,114億米ドル |

| 予測金額 | 4,584億米ドル |

| CAGR | 4.2% |

市場は車両クラス別に区分され、クラス8トラックがこの分野を支配し、2024年の市場シェアの80%以上を占めました。堅牢な設計と33,000ポンドを超える高い車両総重量定格(GVWR)で知られるクラス8トラックは、物流、建設、農業などの産業にとって不可欠な存在です。重い荷物を長距離にわたって効率的に輸送するその能力は、グローバルサプライチェーンにおけるその地位を確固たるものにしています。さらに、低燃費エンジンやスマートシステムといった最先端機能の搭載により、フリートオペレーターにとって好ましい選択肢となっています。

燃料タイプ別セグメンテーションでは、ディーゼルエンジン搭載トラックの優位性が明らかになり、2024年の市場シェアの75%以上を占めました。ディーゼルトラックは、比類のないパワー、信頼性、広範な航続距離で有名であり、長距離輸送や大型用途に不可欠です。その継続的な隆盛は、シームレスな運用を保証する、確立された給油インフラによって支えられています。代替燃料へと徐々にシフトしているにもかかわらず、ディーゼルトラックは、その実証済みの性能と多用途性により、大型輸送の要であり続けています。

アジア太平洋は大型トラック市場をリードしており、2023年の売上シェアの60%を占めました。中国やインドのような国々における急速な工業化と都市化が、効率的な輸送ソリューションへの需要を高めています。活況を呈するeコマース部門と拡大する物流ネットワークは、大型トラックに対するニーズをさらに増幅させています。さらに、政府主導のインフライニシアティブと経済開拓戦略は、引き続きこの地域の市場成長を推進しています。アジア太平洋が世界経済のハブとしての地位を強化するにつれ、大型トラック市場は力強い勢いを維持すると予想されます。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 一次調査と検証

- 一次情報

- データマイニングソース

- 市場範囲・定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 原材料サプライヤー

- 部品サプライヤー

- メーカー

- 技術プロバイダー

- 流通業者

- 最終用途

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 規制状況

- 価格分析

- 影響要因

- 成長促進要因

- 自律走行技術に対する需要の高まり

- 大型トラックの稼働率を高める長距離貨物輸送の増加

- 厳しい規制による高度な排ガス制御システムの採用

- 物流ネットワークとeコマースの世界的拡大

- トラック輸送の効率性と安全機能における技術的進歩

- 業界の潜在的リスク・課題

- 先端技術統合の高コスト

- 貨物需要に影響する経済減速

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:クラス別、2021年~2034年

- 主要動向

- クラス7

- アクスルタイプ

- 4X2

- 6X2

- 6X4

- アクスルタイプ

- クラス8

- 車軸タイプ

- 4X2

- 6X2

- 6X4

- キャブタイプ

- デイキャブ

- 寝台キャブ

- 車軸タイプ

第6章 市場推計・予測:燃料別、2021年~2034年

- 主要動向

- ディーゼル

- 天然ガス

- ハイブリッド電気

- ガソリン

第7章 市場推計・予測:馬力別、2021年~2034年

- 主要動向

- 300HP未満

- 300HP~400HP

- 400HP~500HP

- 500HP以上

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 貨物輸送

- 公益事業

- 建設・鉱業

- その他

第9章 市場推計・予測:所有者別、2021年~2034年

- 主要動向

- フリート事業者

- 独立事業者

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- ベルギー

- スウェーデン

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- BYD Auto

- Daimler Trucks

- Dongfeng

- Freightliner

- Hino Motors

- Isuzu Motors

- Kenworth

- MAN

- Navistar

- PACCAR Inc

- Peterbilt

- SCANIA

- SINOTRUK

- TRATON GROUP

- Volvo

目次

The Global Heavy Duty Trucks Market was valued at USD 311.4 billion in 2024 and is expected to grow at a CAGR of 4.2% from 2025 to 2034. This growth is largely attributed to the increasing global need for efficient goods transportation, driven by thriving commerce and expanding trade activities. Cross-border trade has gained momentum, necessitating advanced heavy-duty vehicles capable of handling substantial cargo volumes over long distances. Collaborative efforts among regions to streamline trade logistics and improve infrastructure are bolstering the adoption of heavy-duty trucks, particularly Class 8 vehicles.

Technological innovations are reshaping the market landscape, enhancing vehicle performance, safety, and operational efficiency. Advanced features like autonomous driving, telematics, and connectivity solutions are increasingly being integrated into heavy-duty trucks, making them more appealing to fleet operators. These technologies optimize fleet management, improve driver safety, and reduce operating costs, fostering demand for modernized truck models. With fleet operators prioritizing performance and cost efficiency, the adoption of technologically advanced heavy-duty trucks is on the rise globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $311.4 Billion |

| Forecast Value | $458.4 Billion |

| CAGR | 4.2% |

The market is segmented by vehicle class, with Class 8 trucks dominating the sector, accounting for over 80% of the market share in 2024. Known for their robust design and high gross vehicle weight rating (GVWR) exceeding 33,000 pounds, Class 8 trucks are indispensable for industries like logistics, construction, and agriculture. Their ability to transport heavy loads efficiently over long distances has solidified their position in global supply chains. Additionally, the incorporation of cutting-edge features such as fuel-efficient engines and smart systems makes them a preferred choice for fleet operators.

Fuel type segmentation reveals the dominance of diesel-powered trucks, which held over 75% of the market share in 2024. Diesel trucks are renowned for their unmatched power, reliability, and extensive range, making them essential for long-haul transportation and heavy-duty applications. Their continued prominence is supported by a well-established refueling infrastructure, ensuring seamless operations. Despite the gradual shift toward alternative fuels, diesel trucks remain a cornerstone of heavy-duty transportation due to their proven performance and versatility.

Asia Pacific leads the heavy-duty trucks market, contributing 60% of the revenue share in 2023. Rapid industrialization and urbanization across countries like China and India have heightened the demand for efficient transportation solutions. The booming e-commerce sector and expanding logistics networks further amplify the need for heavy-duty trucks. Additionally, government-led infrastructure initiatives and economic development strategies continue to propel market growth in the region. As Asia Pacific strengthens its position as a global economic hub, the heavy-duty trucks market is expected to maintain strong momentum.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component suppliers

- 3.2.3 Manufacturers

- 3.2.4 Technology providers

- 3.2.5 Distributors

- 3.2.6 End Use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Pricing analysis

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Escalating demand for autonomous driving technologies

- 3.8.1.2 Increasing long-haul freight activities bolstering heavy duty truck utilization

- 3.8.1.3 Introduction of advanced emission control systems due to strict regulations

- 3.8.1.4 Expansion of logistic networks and e-commerce globally

- 3.8.1.5 Technological advancements in trucking efficiency and safety features

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High cost of advanced technology integration

- 3.8.2.2 Economic slowdown affecting freight demand

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Class, 2021 - 2034 ($Bn, Unit)

- 5.1 Key trends

- 5.2 Class 7

- 5.2.1 Axle type

- 5.2.1.1 4X2

- 5.2.1.2 6X2

- 5.2.1.3 6X4

- 5.2.1 Axle type

- 5.3 Class 8

- 5.3.1 Axle type

- 5.3.1.1 4X2

- 5.3.1.2 6X2

- 5.3.1.3 6X4

- 5.3.2 Cab type

- 5.3.2.1 Day cab

- 5.3.2.2 Sleeper cab

- 5.3.1 Axle type

Chapter 6 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Unit)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 Natural gas

- 6.4 Hybrid electric

- 6.5 Gasoline

Chapter 7 Market Estimates & Forecast, By Horsepower, 2021 - 2034 ($Bn, Unit)

- 7.1 Key trends

- 7.2 Below 300HP

- 7.3 300HP-400HP

- 7.4 400HP-500HP

- 7.5 Above 500HP

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Unit)

- 8.1 Key trends

- 8.2 Freight delivery

- 8.3 Utility services

- 8.4 Construction & mining

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Ownership, 2021 - 2034 ($Bn, Unit)

- 9.1 Key trends

- 9.2 Fleet operator

- 9.3 Independent operator

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Unit)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Russia

- 10.3.6 Belgium

- 10.3.7 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 BYD Auto

- 11.2 Daimler Trucks

- 11.3 Dongfeng

- 11.4 Freightliner

- 11.5 Hino Motors

- 11.6 Isuzu Motors

- 11.7 Kenworth

- 11.8 MAN

- 11.9 Navistar

- 11.10 PACCAR Inc

- 11.11 Peterbilt

- 11.12 SCANIA

- 11.13 SINOTRUK

- 11.14 TRATON GROUP

- 11.15 Volvo

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日