|

市場調査レポート

商品コード

1871276

代替タンパク質市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測Alternative Protein Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 代替タンパク質市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年10月30日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

概要

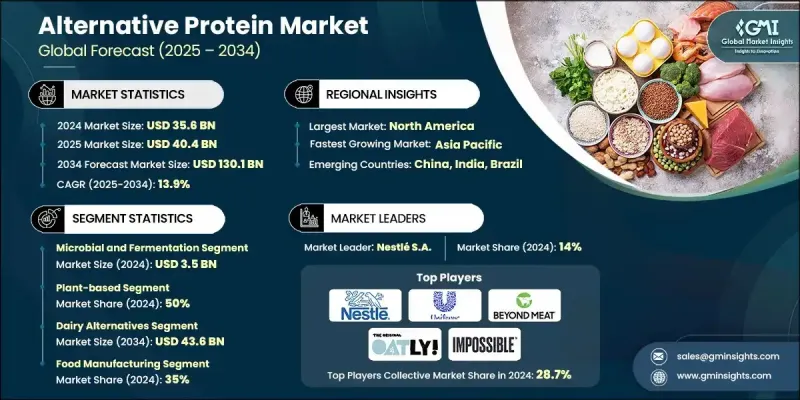

世界の代替タンパク質市場は、2024年に356億米ドルと評価され、2034年までにCAGR13.9%で成長し、1,301億米ドルに達すると予測されています。

市場成長は、消費者の行動変化、持続可能性への要請、そして継続的なバイオテクノロジーの進歩によって牽引されています。代替タンパク質は、世界のタンパク質安全保障に対応しつつ、従来の肉・乳製品産業の環境負荷を低減する、将来の食糧エコシステムにおける重要な構成要素として台頭しています。規制面の支援強化、ベンチャーキャピタル投資の増加、小売流通網の拡充が市場の拡大を加速させています。植物性タンパク質、培養肉、発酵由来タンパク質を合わせると、市場全体の約85%を占めています。複数の生産プラットフォームを組み合わせたハイブリッド技術の台頭により、製品の食感、栄養価、手頃な価格が向上しています。さらに、AI支援型分子農業や3D食品印刷といった新興技術は、プロセスの効率性、拡張性、カスタマイズ性を高め、より広範な商業的採用への道を開いています。精密発酵技術は、機能性を持つ動物由来と同等のタンパク質を大規模に生産することで、タンパク質製造の概念を再定義し続けております。これにより、持続可能なタンパク質代替品の選択肢がさらに多様化し、世界の食品サプライチェーンの変革に貢献しております。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025-2034 |

| 開始時価値 | 356億米ドル |

| 予測金額 | 1,301億米ドル |

| CAGR | 13.9% |

植物性タンパク質セグメントは、肉の繊維質を模倣するテクスチャリング、抽出、押出技術における大きな進歩に支えられ、2024年に50%のシェアを占めました。培養タンパク質技術は、高度な細胞培養システムと制御された成長環境を活用し、家畜を使用せずに本物の肉に似た代替品を生産します。これらの生産方法は、動物農業に関連する倫理的・環境的課題に対処する、拡張性と資源効率に優れた手法としてますます認知されています。

食品製造セグメントは2024年に35%のシェアを占めました。メーカー各社は代替タンパク質を採用し、既存製品のリフォーミュレーションや新たな持続可能な食品の開発を進めています。環境に配慮した食事への消費者関心が高まる中、食品メーカーや飲食店は植物性・細胞培養タンパク質を主流メニューに取り入れ、現代の食の嗜好や世界的な持続可能性目標への適合を図っています。

北米代替タンパク質市場は2024年に142億米ドルの規模に達し、2034年までCAGR10%で拡大が見込まれます。同地域は、充実した研究インフラ、強力な投資支援、代替タンパク源に対する広範な消費者受容という利点を有しています。北米市場を牽引するのは米国であり、支援的な規制枠組み、最先端の技術進歩、成熟した食品加工産業が成長の原動力となっています。政府機関は植物由来、発酵、培養タンパク質分野のイノベーションを促進するガイドラインを導入し、地域における商業化の拡大と製品多様化を後押ししています。

世界の代替タンパク質市場で事業を展開する主要企業には、Oatly Group AB、Beyond Meat Inc.、Impossible Foods Inc.、Perfect Day Inc.、Tyson Foods Inc.、Eat Just Inc.、Nestle S.A.、Aleph Farms Ltd.、Mosa Meat B.V.、ユニリーバ・ピーエルシー、クォーン・フーズ、ジボダン・エスエー、ザ・エブリ・カンパニー、イングレディオン・インコーポレイテッド、ネイチャーズ・ファインド・インク、プランテッド・フーズ・エーゲー、ロケット・フレール・エスエー、ダノン・エスエー、アップサイド・フーズ・インク、ウィルマー・インターナショナル・リミテッドなどが挙げられます。代替タンパク質市場の企業は、高度なバイオテクノロジー、パートナーシップ、ポートフォリオの多様化を活用し、市場での地位強化を図っています。多くの企業が、代替タンパク質の味、食感、栄養プロファイルを向上させ、動物由来の選択肢と競合できるようにするため、研究開発に多額の投資を行っています。スタートアップ企業と大手食品メーカーとの戦略的提携は、イノベーションを促進し、商業化を加速させています。企業は発酵技術や細胞培養技術による生産拡大を図ると同時に、ハイブリッド製造モデルでコスト最適化を進めています。小売チャネルやファストフード店を通じた新たな地域市場への進出により、消費者の入手可能性がさらに高まっています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域(MEA)

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品カテゴリー別

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)

(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントへの配慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協力関係

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:原料別、2021-2034

- 主要動向

- 植物由来

- 大豆ベース

- エンドウ豆タンパク質

- 小麦グルテン及び穀物タンパク質

- 豆類(緑豆、ソラマメ、ヒヨコ豆)

- 新規植物

- 微生物・発酵

- 培養培地

- 微生物株

- 発酵基質

- 細胞培養

- 機能性添加物・原料

- 乳化剤・安定剤

- 香味料・調味料

- 結合・食感付与

- 栄養強化

- その他

第6章 市場推計・予測:製造技術別、2021-2034

- 主要動向

- 植物由来

- 培養技術

- 発酵

- ハイブリッド加工

- 新興技術

- 3D食品印刷システム

- 新規抽出技術

- 高度なバイオプロセシング

第7章 市場推計・予測:製品カテゴリー別、2021-2034

- 主要動向

- プロテイン原料・中間体

- プロテイン分離物・濃縮物

- 機能性タンパク質原料

- 特殊タンパク質

- 肉代替品

- ひき肉

- 塊肉

- 加工肉(ソーセージ、ナゲット、パティ)

- 乳製品代替品

- 牛乳

- チーズ

- ヨーグルト・アイスクリーム

- 精密発酵乳タンパク質

- シーフード代替品

- 卵代替品

- ペットフード代替品

- 栄養補助食品・プロテインパウダー

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 食品製造業

- 外食産業

- クイックサービス

- フルサービス

- 施設向け食品サービス(病院、学校、企業向け)

- 小売/消費者向け

- 食料品小売

- 電子商取引

- 専門店・自然食品店

- その他(化粧品・パーソナルケア、医薬品)

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第10章 企業プロファイル

- Aleph Farms Ltd.

- Beyond Meat Inc.

- Danone S.A.

- Eat Just Inc.

- Givaudan S.A.

- Impossible Foods Inc.

- Ingredion Incorporated

- Mosa Meat B.V.

- Nature's Fynd Inc.

- Nestle S.A.

- Oatly Group AB

- Perfect Day Inc.

- Planted Foods AG

- Quorn Foods

- Roquette Freres S.A.

- The EVERY Company

- Tyson Foods Inc.

- Unilever PLC

- Upside Foods Inc.

- Wilmar International Limited