|

市場調査レポート

商品コード

1822650

代替タンパク質の市場機会と促進要因、産業動向分析、2025年~2034年予測Alternative Proteins Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 代替タンパク質の市場機会と促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年08月18日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

概要

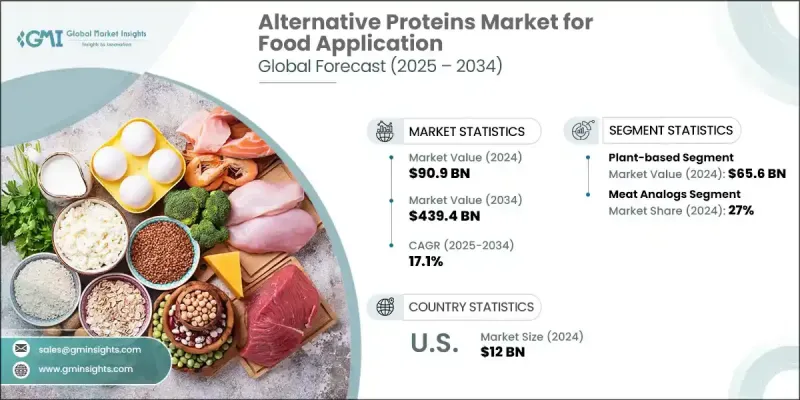

食品用途の代替タンパク質の世界市場は、2024年に909億米ドルと評価され、環境持続可能性への意識に後押しされ、CAGR 17.1%で成長し、2034年には4,394億米ドルに達すると推定されます。

消費者は環境に優しいライフスタイルを選ぶようになり、エコロジカル・フットプリントの少ないタンパク質源を求めるようになっています。さらに、健康や食生活に対する懸念が、より健康的で慢性疾患を引き起こしにくいと認識されている植物性タンパク質やラボ栽培タンパク質へのシフトを促しています。2023年にInternational Food Information Councilが実施した調査によると、アメリカ人の半数以上(57%)が代替タンパク質を試したことがあり、植物性挽肉が31%で最も多く、次いで牛肉代替が23%、植物性ソーセージが22%、植物性鶏肉代替が22%となっています。

さらに、食品生産における技術の進歩は、代替タンパク質をより入手しやすく、費用対効果の高いものにしており、市場の拡大を加速させています。代替タンパク質市場は、供給源、用途、地域によって分類されます。昆虫ベースのセグメントは、資源利用の効率性により、調査期間中に大きな成長率を記録するであろう。昆虫は従来の家畜に比べ、土地、水、飼料を大幅に削減できるため、持続可能性の高いタンパク質源となります。さらに、昆虫は飼料転換率が高く、迅速に栽培できるため、拡張可能で弾力性のある食糧システムに対するニーズの高まりに合致しています。持続可能性への懸念が高まり、消費者が革新的なタンパク質源を求める中、環境への影響を最小限に抑えながら世界的な食糧安全保障の課題に対処できる可能性があることから、昆虫をベースにした選択肢が支持を集めています。畜産業界における持続可能なタンパク質源の採用により、2032年までに動物飼料用途の代替タンパク質市場シェアが顕著になるとみられます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 909億米ドル |

| 予測金額 | 4,394億米ドル |

| CAGR | 17.1% |

畜産物の需要が増加するにつれて、農家は従来の飼料を補完できる代替タンパク質を模索しています。このシフトの背景には、飼料効率を高め、従来の飼料原料に関連する環境フットプリントを削減したいという願望があります。代替タンパク質を飼料に組み込むことで、生産者は全体的な資源利用を改善し、飼料不足の課題に対処することができます。欧州の代替タンパク質市場は、持続可能で倫理的な食品を求める消費者の旺盛な需要に牽引され、2032年まで力強い成長傾向を示すと思われます。従来の蛋白源が環境に与える影響に対する意識の高まりから、欧州の消費者はより環境に優しい代替蛋白源を求めるようになっています。さらに、食品生産における持続可能性を促進する厳しい規制と政府のインセンティブが市場の成長を後押ししています。健康志向の高まりと食品技術の革新が代替タンパク質の魅力をさらに高め、この地域の業界プレーヤーに有利な機会を創出しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:ソース別、2021-2034

- 主要動向

- 植物由来

- 大豆タンパク質分離物

- 大豆タンパク質濃縮物

- 発酵大豆タンパク質

- ウキクサタンパク質

- その他

- 昆虫ベース

- 微生物ベース

- 細菌

- 酵母

- 藻類

- その他

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 肉の代替品

- ベーカリー

- 乳製品の代替品

- シリアルとスナック

- 飲み物

- その他

第7章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第8章 企業プロファイル

- Archer Daniels Midland Company

- Cargill Inc.

- Ingredion Inc.

- Kerry Group

- Impossible Foods Inc.

- The Scoular Company

- DSM NV

- Lightlife Foods, Inc.

- Impossible Foods Inc.

- International Flavors &Fragrances, Inc.

- Glanbia plc

- Bunge Limited

- Axiom Foods Inc.