|

市場調査レポート

商品コード

1822621

地域暖房の市場機会、成長促進要因、産業動向分析、2025~2034年予測District Heating Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 地域暖房の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年08月21日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

概要

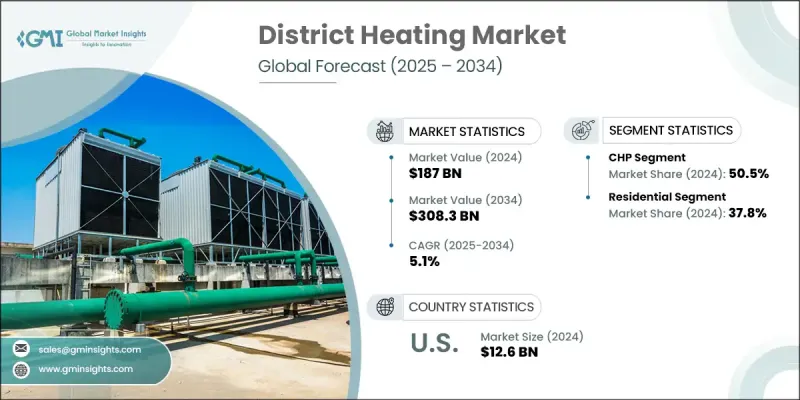

地域暖房の世界市場規模は、2024年に1,870億米ドルとなり、CAGR 5.1%で成長し、2034年には3,083億米ドルに達すると予測されています。

不安定な化石燃料に依存する個々の暖房システムとは異なり、地域暖房ネットワークは価格変動や供給の途絶の影響を受けにくいです。熱の生産と配給に集中的なアプローチを利用することで、これらのシステムは、住宅、商業、工業用ユーザーに一貫したエネルギーの利用可能性を保証します。この回復力は経済の安定を促進し、化石燃料への依存を減らし二酸化炭素排出量を削減することで持続可能性の目標をサポートします。そのため、2024年6月、ヒューレット・パッカード・エンタープライズとダンフォスは、データセンターのエネルギー使用量を削減するために提携しました。両社のモジュラー設計は、エッジでAIとコンピューティングタスクを加速するための熱回収システムを統合し、余剰熱は外部で再利用します。これは、エネルギー関連のリスクを軽減し、将来に向けてよりレジリエントなエネルギーインフラを構築するための世界的な取り組みと一致しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 1,870億米ドル |

| 予測金額 | 3,083億米ドル |

| CAGR | 5.1% |

都市化の進展と人口密集地における効率的で持続可能な暖房ソリューションの必要性により、住宅分野は2032年までに顕著な市場シェアを獲得します。住宅所有者は、エネルギーコストと二酸化炭素排出量を削減するため、環境に優しい選択肢を求めています。地域暖房システムは、個々のボイラーやメンテナンスの必要性をなくし、信頼性が高く便利な暖房源を提供します。さらに、エネルギー効率の高い建物を促進する政府の優遇措置や規制により、新しい住宅開発に地域暖房の採用が進んでいます。欧州の地域暖房市場は、二酸化炭素排出量の削減と気候変動目標の達成に取り組んでいるため、予測期間中に顕著なCAGRを示すと思われます。欧州諸国は、再生可能エネルギー源と高度な暖房インフラに多額の投資を行っています。都市化と老朽化した暖房システムの近代化により、より効率的な集中型ソリューションの必要性が高まっています。さらに、欧州連合(EU)の政策と資金援助は、持続可能な地域暖房ネットワークの開発を支援し、エネルギー効率の改善と環境負荷低減のために、公共部門と民間部門がこれらのシステムを採用することを奨励しています。これらの要因は、地域産業の成長を後押しすると思われます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 主要サプライヤーおよび技術プロバイダー

- 物流、流通、サービス

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

- 地域暖房のコスト構造分析

- 価格動向分析

- 地域別

- ソース別

- 将来の市場見通しと新たな機会

- 将来の地域暖房と冷却ソリューションの開発

- インジゴ

- フレキシネット

- E2地区

- インディール

- ケーススタディ分析- ストックホルムの統合DHCシステム

- プロジェクト概要

- 主要な事実と数字

- 顧客セグメンテーション

- DHCを支援する政策とインセンティブ

- 地域暖房システムの技術的および運用上のパラメータ

- 顧客と最終用途の分析

- 住宅、産業、商業部門での採用

- 都市部と農村部の浸透

- 需要動向と消費パターン

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析:地域別2024

- 北米

- 欧州

- アジア太平洋地域

- 戦略的ダッシュボード

- 戦略的取り組み

- 主要なM&A活動

- 主要なパートナーシップとコラボレーション

- 製品の革新と発売

- 市場拡大戦略

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:ソース別、2021-2034

- 主要動向

- CHP

- 地熱

- 太陽

- 暖房専用ボイラー

- その他

第6章 市場規模・予測:用途別、2021-2034

- 主要動向

- 住宅用

- 商業用

- 大学

- オフィス

- 政府/軍

- その他

- 産業

- 化学薬品

- 製油所

- 紙

- その他

第7章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- ポーランド

- ロシア

- スウェーデン

- フィンランド

- イタリア

- デンマーク

- 英国

- スロバキア

- オーストリア

- チェコ共和国

- フランス

- アジア太平洋地域

- 中国

- 日本

- 韓国

第8章 企業プロファイル

- A2A S.p.A.

- Alfa Laval

- Antin Infrastructure Partners

- BEW Berlin Energy and Heat

- CenTrio

- Cordia

- Danfoss

- E.ON

- EDF

- EnBW Energie Baden-Wurttemberg

- ENGIE

- Fortum

- Goteborg Energi

- Hafslund

- Iren S.p.A.

- Kelag Energie &Warme

- Keppel

- Korea District Heating

- LOGSTOR Denmark Holding

- Nevel

- Ørsted

- Ramboll

- RWE

- Shinryo Corporation

- Statkraft

- STEAG

- Vattenfall

- Veolia