|

市場調査レポート

商品コード

1940811

英国の地域熱供給:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)United Kingdom District Heating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国の地域熱供給:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 117 Pages

納期: 2~3営業日

|

概要

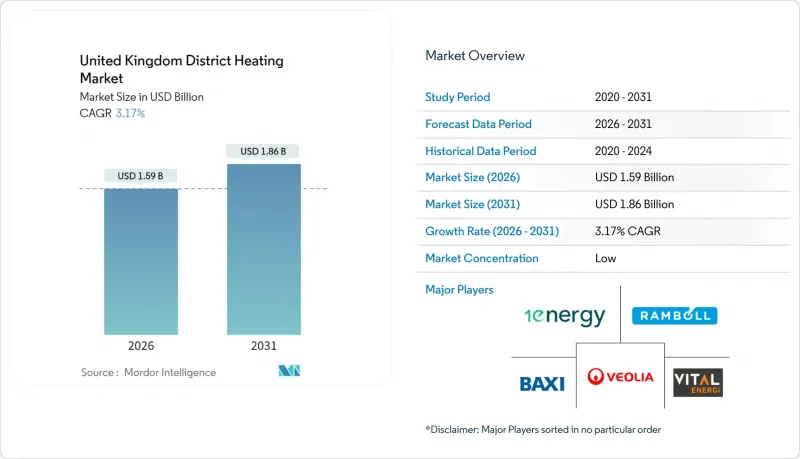

英国の地域熱供給市場は、2025年に15億4,000万米ドルと評価され、2026年の15億9,000万米ドルから2031年までに18億6,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは3.17%と見込まれています。

この予測は、ガス依存型資産から低炭素ヒートポンプ、廃熱回収、大規模熱貯蔵へのシステム全体の転換を反映しています。義務化された熱ネットワーク区域指定により、法的拘束力のある接続区域が設定され、顧客獲得のリスク低減が図られています。一方、グリーン熱ネットワーク基金は、廃棄物熱エネルギーや再生可能電力を利用するプロジェクトの資本支出を軽減します。政府補助金では現在、検証可能な炭素削減を実現する計画が優先され、事業者らは河川・鉱山水・廃水の熱源とネットワーク化された地中熱ヒートポンプを組み合わせたシステム導入を促進しています。投資家はこうした政策シグナルに応えています。機関投資家は、断片化したネットワークを専門的な管理下で統合する資産ロールアップを強化し、12時間貯蔵ピットなどの技術アップグレードを加速させています。熟練労働力や金属商品におけるサプライチェーンの制約は依然として逆風ですが、Ofgem(英国エネルギー市場規制機関)が導入予定の消費者保護制度は、エンドユーザーの信頼を強化し、接続率の向上を促すと期待されています。

英国の地域熱供給市場の動向と展望

2025-26年度からの法定熱ネットワーク区域指定

熱ネットワーク区域指定により、地方自治体は定められた境界内での顧客接続を義務付ける法的権限を獲得し、商業的実現可能性に不可欠な熱密度を確保します。エネルギー安全保障・ネットゼロ省は16地域を対象とした機会報告書を発表し、バーミンガム、リーズ、ニューカッスルに対し、新築物件及び多くの改修対象地をカバーする義務区域の策定を指導しました。この区域指定により、地域熱供給は任意の技術から遵守義務へと転換され、事業者の需要リスクが低減されるとともに、長期投資家にとって魅力的な予測可能な収益源が提供されます。開発事業者はネットワーク規模や段階的拡張の明確化を得られる一方、既存建物所有者は脱炭素化の明確な期限に直面します。したがって本政策は、迅速な資本投入と実証済みの運営能力を有するネットワーク所有者へ市場優位性を移行させるものです。

グリーン・ヒート・ネットワーク基金およびHNES助成金

グリーン・ヒート・ネットワーク基金は設立以来、3億8,000万ポンド(4億7,500万米ドル)以上を交付しており、これにはリーズのエア・バレー熱電ネットワーク向け1,950万ポンド、ロンドン大学ブルームズベリー・エネルギー・ネットワーク向け720万ポンドが含まれます。助成金は加重平均資本コストを低減し、廃棄物由来の大型熱源の開発を促進するとともに、内部収益率を最大2パーセントポイント改善します。採択基準では廃熱回収とヒートポンプを組み合わせたプロジェクトを評価対象としており、市場設計を50gCO2/kWh未満の目標達成が可能なハイブリッド構成へと導いています。資金調達の確実性は民間金融機関の参入も促進しており、複数の商業銀行がシニア債務組成時にGHNF助成金をリスク軽減手段として認めるようになりました。

初期設備投資の高騰

2024年から2025年にかけて、資材インフレにより断熱材価格が2~11.7%上昇し、銅や鋼材の価格変動がバランスシートにさらなる負担を加えました。アーループ社の試算によれば、地熱ネットワークの建設コストはMWth当たり200~400万ポンドで、掘削費用だけで支出の最大45%を占めます。この資本集約性は回収期間を延長し、小規模開発業者の資金調達可能性を制限します。GHNF助成金は、実現可能性調査や許可取得段階における沈没コストのリスクを緩和しますが、完全に排除するものではありません。そのため、エクイティ投資家はより高い内部収益率を要求し、アンカー負荷や長期熱購入契約のないプロジェクトの資金調達完了を遅らせています。

セグメント分析

2025年時点で、住宅接続が英国の地域熱供給市場の57.60%を占めました。これは都市住宅団地や複合用途再開発計画における高い熱密度が寄与しています。社会住宅パイロット事業はその価値提案を裏付けており、SHIELD試験では低所得者向け家賃の40%削減可能性を示しつつ、家主の改修義務も満たしています。非住宅需要はESG要件と公共部門のネットゼロ目標に牽引され、CAGR年平均4.41%で拡大しています。大学や病院は資本補助金と長期資産計画を背景に、ベースロード需要を固定する数メガワット規模の拡張を推進中です。

商業不動産所有者は、将来の建物排出税対策として熱ネットワークをヘッジ手段と捉える傾向が強まっています。賃貸契約における運用段階の炭素排出量開示義務化により、低炭素係数を保証するネットワークへの移行が促進されています。一方、地方自治体は住宅用と公共用需要を統合することで規模の経済を実現し、対象顧客基盤をさらに拡大しています。これにより形成される複合顧客構成はキャッシュフローを安定化させ、民間債務市場での再融資を可能にし、英国の地域熱供給市場の成長軌道を支えています。

2025年時点で、ガス焚きCHPは英国の地域熱供給市場規模の70.85%を占めておりますが、炭素価格設定やバイオマス持続可能性規制の強化に伴い、その優位性は低下傾向にあります。低炭素ヒートポンプと廃熱システムはCAGR5.08%で拡大しており、これはGHNFスコアの高評価対象となる資格とライフサイクル排出量の低さを反映したものです。MELヒートネットワークはミラーヒル廃棄物発電施設からの廃熱を回収し、大型ヒートポンプで増強してショーフェアタウンに供給しています。ヴァッテンフォール社の試算によれば、このハイブリッドシステムによりベースライン排出量の最大90%を削減できる見込みです。

地中熱システムは、住宅団地間で垂直ボーリング孔を共有するネットワーク型配列により規模拡大が進み、住戸当たりの掘削コストを3分の1削減します。空気熱源ユニットは単独供給源ではなく夏季の補助熱源として活用される傾向が強まり、季節ごとの性能最適化が図られています。都市部では粒子状物質規制によりバイオマスは依然ニッチな存在ですが、地方の団地では地元原料の活用が続いています。耐障害性確保のためバックアップ用ガスボイラーは存続するもの、蓄熱技術と需要応答の改善に伴い稼働時間は減少傾向にあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 2025-26年度からの法定熱供給ネットワーク区域指定

- グリーンヒートネットワーク基金およびHNES助成金

- 廃熱回収義務(エネルギー回収施設および下水処理)

- 河川・鉱山水熱ポンプのコスト低下

- 家主様への料金開示義務

- 熱貯蔵のESO柔軟性への統合

- 市場抑制要因

- 初期段階における高額な設備投資

- ガスと電力の価格差変動性

- 熟練労働者不足(配管溶接工/高圧配管工)

- 消費者による「独占的請求」の認識

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ファイブフォース分析分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- エンドユーザー別

- 住宅/一般家庭向け

- 非住宅

- 一次熱源別

- ガスCHP

- 低炭素ヒートポンプおよび廃熱

- バイオマス/バイオガス

- その他のバックアップ(ガス、電力)

- セクターおよび顧客別

- 複合用途再開発地区

- 公共住宅および社会住宅

- 大学・病院

- 商業施設/小売施設

- 蓄熱設備の使用状況別

- 統合型貯蔵なし

- 2時間以上の給湯タンク

- 12時間以上のピット/タンク貯蔵

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Vital Energi Utilities Ltd.

- 1Energy Group Ltd.

- Baxi Heating UK Ltd.

- Ramboll UK Ltd.

- Veolia Environnement SA

- Sweco UK Ltd.

- Vattenfall Heat UK Ltd.

- Equans Services Ltd.

- E.ON UK plc

- SSE Heat Networks Ltd.

- Metropolitan Infrastructure Ltd.

- ThamesWey Energy Ltd.

- Pinnacle Power Ltd.

- Fortum Carlisle Heat Networks Ltd.

- Cory Heat Networks Ltd.

- Kensa Utilities Ltd.

- Ener-Vate Ltd.

- Centrica Business Solutions UK Ltd.

- ENGIE(Energy Solutions UK)Ltd.

- Danpower UK Ltd.